Feature/OPED

The Coming of Barry Ndiomu as Presidential Amnesty Interim Coordinator

By Jerome-Mario Chijioke Utomi

The recent disengagement of Colonel Milland Dixon Dikio (rtd) as the interim Coordinator, Amnesty Programme, after two years of being in the saddle by President Muhammadu Buhari precisely on Thursday, September 15, 2022, and has in his place appointed Major-General Barry Ndiomu (retd) has again shown that bosses are neither a title on the organisation chart nor a function. But they are individuals and are entitled to do their work. It is incumbent for the occupier to do this work or be shown the way out by the real job owner.

Qualifying this recent development as a departure from the old order is the new awareness that the Dikio has, unlike his predecessors, congratulated the Odoni, Sagbama Local Government Area, Bayelsa State-born, and Nigerian Defence Academy 29th Regular Combatant Course trained Ndiomu for succeeding him as the new boss of the programme.

While thanking God for His grace and profound gratitude to President Buhari for allowing him to serve the country, Dikkio, in that report, explained that he has firmly set on the course the mission to transform ex-agitators to become net contributors to the economy of the Niger Delta and the nation at large.

To keep issues where they belong, it is important to underline that the purpose of this present intervention is not to subject Dikkio’s tenure to intensive scrutiny. Rather, it is aimed at assisting the Coordinator in succeeding in his new responsibility. That notwithstanding, the truth must be told that Dikkio’s claim of transforming ex-agitators into net contributors to the economy of the Niger Delta and the nation at large had not gone without eliciting reactions from stakeholders and the general public.

For instance, while some consider the claim true and objective, others view it with scepticism.

Moreover, from the above experience, Ndiomu, the new interim boss of the organisation, must, as an incentive to success, design a circle of learning and empowerment for himself that will allow him to see things that his predecessors did not see and formulate transformational strategies.

He must not fail to remember that the luxury of a leisurely approach to an urgent challenge is no longer permissible in the modern-day leadership arena. He must recognise the fact that what partially explains the failure of his predecessors is traceable to their decision to do good instead of doing well.

For a better understanding of this position, ‘doing-good entails charity service or so-called selfless service where one renders assistance and walks away without waiting for any returns. On the other hand, doing well describes reciprocation and ‘win-win’ because the doer is also a stakeholder and intends to benefit at least in goodwill and friendship’.

To change this trend, localise, grasp and find solutions to the critical issues plaguing the programme, it is important to recognise that bringing a radical improvement or achieving sustainable development will not be possible if you present yourself as an all-knowing, more generous, more nationalistic, selfless, more honest or kind, more intelligent, good looking or well-briefed than other stakeholders.

Again, succeeding on this job will, among other things, require two things: first, you should guard against the euphoria inspired by such appointments; make no grandiose plans or claims while your thinking is altered by feelings inspired by triumph; and secondly, the corrupting tendency of the additional power you have won. Try not to feel that much less accountability because you have that much power. You still must answer to yourself, and you must more than ever lead.

Another point you must not also fail to remember is that your enemies are everywhere and have with this appointment increased in number, locations and forms. “You must love your neighbour but keep your neighbourhood’, view corruption as something/act that destroys and breaks that trust which is essential for the delicate alchemy at the heart of representative democracy.

You must avoid the ongoing experience at the Niger Delta Development Commission (NDDC). A sister initiative was also established by the federal government to facilitate integrated development in the region but has yet to be identified because a sheep has gone its way ’abandoning the people of the coastal areas it was created to protect. There is an urgent imperative to carry the stakeholders along, particularly the Niger Delta youths who are supposedly the real beneficiary of the programme.

At this point, it is important to remember that the original amnesty document, as proclaimed by Yar’Adua, was meant to stand on a tripod-with the first part of the tripod targeted at disarmament and demobilisation process; the second phase to capture rehabilitation which is the training processes, while the third phase is the Strategic Implementation Action Plan. This last phase was designed to develop the Niger Delta massively but was unfortunately ignored by the federal government. You must look into this to succeed.

Remember, stakeholders have recently questioned the wisdom behind teaching a man to fish in an environment where there is no river to fish or training a man without a job creation plan. They are particularly unhappy that the amnesty initiative, which was programmed to empower the youths of the region via employment, has finally left the large army of professionally-trained ex-militants without jobs.

In fact, the region is in a dire state of strait because unemployment has diverse implications. While pointing out that security wise, a large unemployed youth population is a threat to the security of the few that are employed, and any transformation agenda that does not have job creation at the centre of its programme will take us nowhere’.

In making this call, it is obvious that there is nothing more ‘difficult to handle, more doubtful of success, and more dangerous to carry through than initiating such changes as the innovator will make more enemies of all those who prospered under old order’. But any leader that does come out powerful secured, respected and happy. This is an opportunity you must not miss.

Finally, as a flood of congratulatory messages continues to flow into your home, two things stand out. The moment portrays you as lucky. But like every success which comes with new challenges, the appointment has thrust yet another responsibility on you- an extremely important destiny; to complete a process of socioeconomic rejuvenation of the Niger Delta youths, which we have spent far too long a time to do.

Therefore, you must study history, study the actions of your predecessors, see how they conducted themselves and discover the reasons for their victories or defeats so you can avoid the latter and imitate the former.

If you can correct the above challenge, it will be your most powerful accomplishment for earning new respect and emulation. And if you are not, it will equally go down the anal of history.

Jerome-Mario Utomi is the Programme Coordinator (Media and Public Policy), Social and Economic Justice Advocacy (SEJA), a Lagos-based Non-Governmental Organization (NGO)

By Blaise Udunze

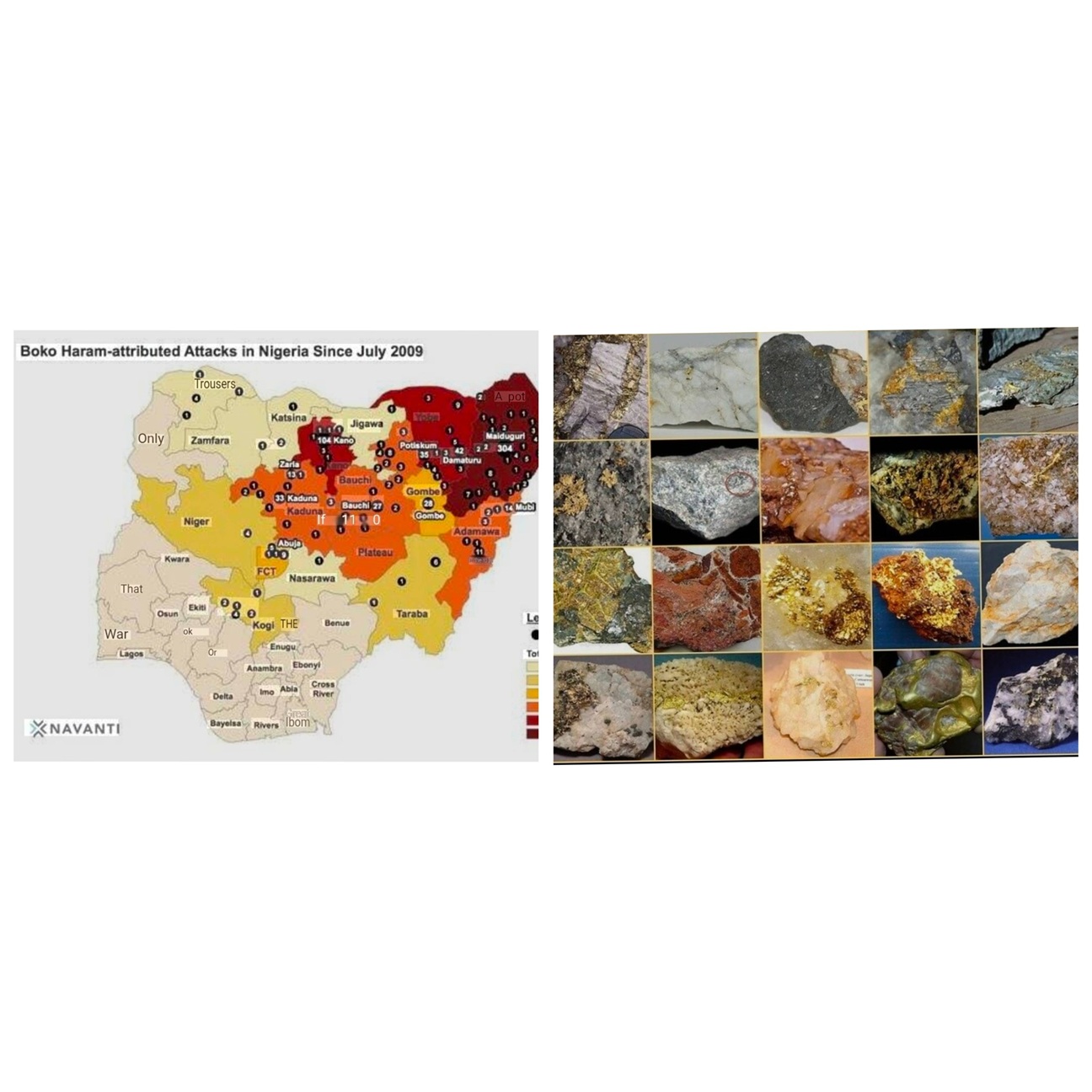

Daily, the world watches Nigeria through a familiar lens in what appears to be a gory situation. Especially in cases when the news headlines tell stories of farmer-herder clashes, bandit attacks, kidnappings, villages reduced to ashes or deserted by the dwellers, as thousands of Nigerians have been displaced across states such as Zamfara, Plateau, Benue, Niger, Kaduna and Nasarawa. Subliminally, this is about to become a similarly ugly occurrence in southwestern Nigeria, which is fast becoming obvious if not nipped in the bud quickly.

Recorded data have shown that bandits, Boko Haram, and others killed over 190,000 Nigerians in 17 years and displaced 3.7 million people.

A human rights organisation, the International Society for Civil Liberties and Rule of Law (Intersociety), in its fearful revelation, has said that no fewer than 190,150 Nigerians have been killed by bandits, Boko Haram insurgents, and suspected armed herdsmen between July 2009 and March 19, 2026, as this calls for concern.

The dominant explanations often point to ethnic tensions, religious divisions, climate change, shrinking grazing routes or weak security institutions. No doubt, those factors are certainly part of Nigeria’s complex security crisis. Yet another question deserves serious examination.

What if, in some locations, the violence is also serving another purpose? What if some of the territories experiencing repeated displacement are the same places sitting atop some of Nigeria’s most valuable mineral deposits? More importantly, if such a pattern exists, who benefits when communities disappear?

Of a truth, these questions are uncomfortable, but undeniably they deserve careful investigation rather than dismissal.

For ages, Nigeria has been naturally endowed, and it is estimated to be rich in enormous significant reserves of gold, lithium, uranium, tin, columbite and other strategic minerals increasingly sought after in the global transition to clean energy technologies. As international demand for battery minerals continues to rise, these resources have become far more valuable than they were only a decade ago.

If one overlays publicly available geological information with maps showing persistent violence, some observers argue that striking geographical overlaps appear in several regions. Such overlaps alone cannot establish causation. Correlation is not proof of conspiracy. However, they raise questions worthy of independent scrutiny.

One issue attracting increasing attention and adequately yearns for answer is whether prolonged insecurity may inadvertently or deliberately create conditions that make mineral extraction easier.

Under Nigeria’s Nigerian Minerals and Mining Act 2007, mineral resources belong to the Federal Government, while mining rights are granted through licences and leases. Community engagement and land access are expected to form part of the licensing process, although implementation varies depending on circumstances. This raises an important policy question.

What happens when the communities expected to participate in those processes have already fled because of violence?

Displacement changes the dynamics of land ownership, consent and access. While no evidence automatically proves that attacks are orchestrated to facilitate mining, the sequence of violence followed by renewed commercial activity in some locations deserves closer examination by regulators, lawmakers and investigative journalists.

In conflict studies, researchers have long observed that wars often generate economic winners alongside humanitarian losers. Could elements of Nigeria’s insecurity also be producing economic beneficiaries?

Reports over the years have documented concerns about illegal mining operations across parts of northern Nigeria. Government agencies themselves have repeatedly acknowledged that criminal networks profit from the country’s vast mineral wealth. The unresolved question is whether isolated criminality has, in some instances, evolved into more sophisticated alliances involving political influence, financial interests and international supply chains. If so, the implications extend far beyond Nigeria.

Invariably, it is clearly known that lithium has become one of the world’s most strategic commodities, powering electric vehicle batteries and renewable energy storage systems. Gold has always remained one of the safest global investment assets during periods of uncertainty. Meanwhile, it is well confirmed that the global appetite for these minerals creates enormous financial incentives.

Suppose violent displacement reduces resistance to extraction. Suppose shell companies subsequently acquire mining interests. Suppose minerals then leave Nigeria through legitimate-looking export documentation while their true value remains understated.

These scenarios remain allegations unless supported by verifiable evidence. Yet they outline a framework that investigators may wish to test rather than ignore. Financial crime experts frequently identify trade mis-invoicing as one of the most common methods of illicit financial flows worldwide.

Could Nigeria’s solid minerals sector be vulnerable to similar practices? If valuable lithium ore is deliberately but inaccurately described as lower-value material on export documents, substantial wealth could potentially leave the country without reflecting its true market value. Likewise, if unrefined gold exits through privileged channels with limited scrutiny, questions naturally arise about oversight, transparency and accountability over criminal activities which have continued to stunt and disrupt the country’s socio-economic growth and at the same time cause carnage.

Such possibilities are not accusations against any particular institution or company. Rather, they illustrate why stronger monitoring systems are increasingly essential. Another question concerns logistics.

With the high level of criminal activities, industrial mining requires heavy machinery, diesel supplies, transportation networks and specialised personnel. These are not operations that can remain invisible indefinitely.

If certain territories are genuinely too dangerous for security agencies, how do industrial-scale extraction activities reportedly continue in some remote locations? If they do, who protects those operations? Who authorises their movement? Who verifies what is extracted? Who ensures royalties and export revenues reach public coffers? These are governance questions that demand institutional answers.

Equally important is the international dimension. Minerals extracted in Nigeria ultimately enter global supply chains. Gold may pass through international refining hubs before entering financial markets. Lithium may become part of battery manufacturing destined for electric vehicles, which are being sold across Europe, North America and Asia.

One known fact is that consumers purchasing products containing these minerals rarely know the full story of where they originated.

Increasingly, however, investors and governments are demanding ethical sourcing standards that trace minerals from extraction to final manufacture.

A critical factor that must be taken into cognisance is that if insecurity is creating opportunities for illegal or unethical extraction anywhere in the world, multinational companies have responsibilities alongside national governments, of which the onus falls on the Nigerian government.

Transparency cannot stop at the mine gate. Nor should accountability end at national borders. Another issue requiring attention concerns beneficial ownership.

Across many jurisdictions, shell companies can obscure the identities of individuals ultimately controlling commercial assets. If politically exposed persons or powerful business interests are hidden behind complex corporate structures registered offshore, identifying beneficiaries becomes significantly more difficult. This challenge is hardly unique to Nigeria.

Findings showed that from Latin America to Central Africa and Southeast Asia, resistant corporate networks have frequently complicated efforts to combat corruption and illicit resource extraction. That is precisely why open corporate registries, beneficial ownership databases and transparent mining licence disclosures are becoming global governance priorities. For Nigeria, the stakes could hardly be higher.

The country stands at the centre of the world’s emerging critical minerals economy. The Nigerian government can’t feign ignorance of the fact that, when handled transparently, these resources could finance infrastructure, education, healthcare, and industrial development for generations.

In no way would the government claim not knowing that when handled poorly, they risk becoming another chapter in the well-documented “resource curse,” where extraordinary natural wealth coincides with persistent poverty, insecurity and institutional weakness.

The ultimate challenge, therefore, is not simply about mining. It is about governance. It is about whether public institutions possess both the independence and capacity to ensure that natural resources benefit citizens rather than narrow interests. It is about whether conflict zones receive genuine peacebuilding efforts instead of becoming forgotten frontiers. And it is about whether international markets demand accountability with the same enthusiasm they demand raw materials.

None of these questions should be answered through speculation. They require rigorous investigations, forensic financial analysis, satellite imagery, mining license audits, customs records, beneficial ownership disclosures and courageous journalism.

They require governments willing to open their books. They require international cooperation capable of tracing money across borders. Most importantly, they require asking questions that have too often remained unasked.

Perhaps Nigeria’s security crisis is exactly what it appears to be: a tragic convergence of historical grievances, weak institutions, criminality and environmental pressures. Or perhaps, in some places, another layer of economic incentive deserves closer scrutiny.

Until those questions are thoroughly investigated, one possibility will continue to linger. Maybe the world’s attention has been fixed on the blood spilt above ground, while too little attention has been paid to the extraordinary wealth lying beneath it.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com

Feature/OPED

What Does Nigeria’s $51bn Reserves Milestone Mean if Most New Foreign Money Can Leave Quickly?

Nigeria’s foreign reserves have climbed to about $51 billion, a decade-plus high, according to the Central Bank of Nigeria (CBN). EBC Financial Group (EBC) notes that this reflects stronger investor confidence, but the second half may show whether it holds, as the build rests on three cyclical drivers: oil earnings, short-term foreign money and a narrowing official-to-street naira gap.

Reserves rose from about $32 billion in April 2024, during a dollar shortage, to about $51 billion now, near the CBN’s target. Much came from two cyclical sources, strong oil earnings and money chasing high-yielding naira assets, so EBC expects the pace to slow or reverse. Fitch Ratings, a major international credit rating agency, expects a marginal decline to about $47 billion by the end of 2026, citing higher spending and external pressures.

David Precious, Senior Market Analyst at EBC Financial Group, said, “Nigeria’s reserve build is real but may not be durable yet, because nearly all of the new money is the kind that can leave quickly. Of the $10.37 billion that came in over the first quarter, the overwhelming majority was short-term portfolio funds rather than long-term investment, so a shift in oil prices, global interest rates or confidence in the naira might pull a large part of it straight back out.”

Most New Money Can Still Leave Quickly

The composition of the foreign inflows explains the caution over how long the build can last. The country attracted $10.37 billion in foreign investment in the first quarter of 2026, up 83.83 per cent year-on-year, according to the National Bureau of Statistics (NBS). Of that, $9.86 billion or 95.09 per cent, was portfolio money, largely short-term naira debt such as Treasury bills that investors can sell at the next auction, while foreign direct investment, the long-term kind that builds factories and jobs, was $135.08 million, or 1.30 per cent. Put simply, of each dollar coming in, about 95 cents can leave quickly, and barely one cent stays.

That money supports reserves while it stays. Dollars brought in to buy naira assets add to market supply, letting the CBN hold more reserves and steady the naira. It leaves when conditions change. Nigeria earns most of its export dollars from oil and gas, so lower oil prices mean fewer dollars, and as a member of the Organisation of the Petroleum Exporting Countries (OPEC), it cannot simply produce more, output capped by quota and reduced by theft and ageing fields. Higher global interest rates draw money toward safer returns abroad, and a weakening naira prompts investors to sell early. When oil fell in 2016 and 2020, foreign investors withdrew and could not convert naira to dollars as supply dried up, leaving the CBN to clear more than $7 billion in trapped obligations into 2024.

The Oil Boost is No Longer Certain

Oil looked like a dependable source of the dollars behind the reserves only months ago. Earlier in 2026, concern over disruption around the Strait of Hormuz lifted crude prices, and stronger receipts flowed in, with crude oil export earnings of $8.11 billion in the first quarter in the CBN’s balance-of-payments data. That support is now easing. The tension has subsided, and Brent traded near $72 on June 29, down about 24 per cent over the month, back to pre-conflict levels. With the price boost gone and output constrained, reserves are more exposed, leaning on non-oil earnings and investor patience rather than oil.

The Naira Still Trades at Two Prices

The naira has traded at two prices, an official rate and a higher parallel-market rate, and closing that gap into one trusted price is what many investors might watch most. Before committing funds, they may want assurance they can convert naira to dollars at a fair rate when they exit, and a wide gap revives the fear of being trapped that lingers from earlier shortages. The gap has narrowed to roughly N20 to N30, with the CBN’s official rate near N1,380 per dollar on June 26 against parallel-market quotes around N1,400. The International Monetary Fund (IMF) 2026 Article IV review urged Nigeria to depend less on this fast-moving portfolio money and to keep phasing out its multiple exchange-rate practices. The CBN’s Foreign Exchange Manual, in force from 1 June, is intended to make the market clearer, though such rules build confidence only once investors can freely trade dollars at the posted rate.

What could Make the Build Durable

A few signs that may show the build turning durable include a smaller gap between the official and street naira rates, more long-term foreign investment, and steadier oil earnings. A gap that stays small, now roughly N20 to N30, may mean investors trust the official rate and no longer need the street market. A clear rise in foreign direct investment, only $135 million last quarter against $9.86 billion of short-term money, might mean lasting capital is replacing funds that can leave at the next auction. Oil earnings that hold up, rather than sliding from the low $70s, should help keep reserves steady, since oil and gas bring in most of Nigeria’s export dollars.

“Reserves built on money chasing high yields can fall as fast as they rose, as they did after the last two oil shocks, when investors left, and the CBN spent years clearing a foreign-exchange backlog,” Precious added. “What holds through a downturn is slower money, direct investment, steady oil and non-oil export earnings and one credible naira rate, and that is the shift Nigeria has yet to make.”

By Olajumoke Bello

Across Nigeria, small and medium enterprises remain the backbone of economic activity. They drive trade, create jobs, and sustain millions of livelihoods. Yet, despite their importance, many SMEs continue to operate below their full potential due to persistent structural challenges.

Access to finance remains one of the most cited constraints. However, the issue today goes beyond the availability of capital. Many businesses struggle with financial readiness, weak documentation, and limited understanding of what lenders require. This often leads to missed opportunities, even when funding options exist.

At the same time, SMEs face gaps in market access and visibility. Business owners operate in highly localised environments, with limited exposure to broader networks that can unlock partnerships, new markets, and growth opportunities. This isolation can constrain scalability and reduce long-term competitiveness.

Equally important is the capability gap. Many entrepreneurs grow through resilience and experience but lack structured knowledge on critical areas such as financial management, export readiness, and digital adoption. Without this, even well-capitalised businesses can struggle to sustain growth.

These challenges point to a clear need for a more practical and integrated approach to SME support. It is no longer sufficient to offer standalone solutions. SMEs require ecosystems that combine knowledge, access, and direct engagement in ways that reflect how they actually operate.

A key shift is the move from centralised interventions to localised engagement. SMEs are deeply influenced by their immediate environments, whether markets, industrial clusters, or trade corridors. Solutions must therefore be brought closer to where these businesses function, allowing for more relevant support and stronger relationships.

Another important shift is from awareness to action. Business owners do not only need information; they need insights that they can apply immediately. This includes understanding how to structure their finances, how to access trade opportunities, and how to connect with the right partners to scale their operations.

There is also a growing need for continuity. Many SME-focused initiatives deliver strong initial impact but lack follow-through. For support to be effective, it must extend beyond one-off engagements into sustained relationships, with clear pathways for onboarding, advisory, and growth.

For financial institutions, this presents both responsibility and an opportunity. Supporting SMEs now requires moving beyond transactional banking to deeper partnership models. It requires understanding businesses at a granular level and co-creating solutions that evolve with their needs.

At Stanbic IBTC, this perspective continues to shape our approach to SME development. Our focus is on delivering practical support that translates into real business outcomes, helping enterprises grow, compete, and contribute more meaningfully to the economy.

As part of this commitment, we are extending our SME engagement to the regions through the Nigeria Business Summit Regional Tour. The tour will take structured, on-ground activations into key commercial hubs, where SMEs can access funding guidance, trade insights, advisory support, and direct engagement with financial experts.

The regional tour will take place across five strategic locations, bringing these solutions closer to business owners in Aba, Onitsha, Ibadan and Kano.

This approach reflects an important principle. When support moves closer to businesses and when solutions are delivered in ways that are practical and continuous, SMEs are better positioned to grow sustainably. In turn, this strengthens not only individual enterprises but the broader economy.

Olajumoke Bello is the Head of Enterprise Banking at Stanbic IBTC Bank