Economy

Nigeria’s Excess Crude Account Remains Static, FAAC Revenue Rises 9.8%

By Aduragbemi Omiyale

The balance in Nigeria’s excess crude account (ECA), as of January 17, 2023, stood at $473,754.57, the same amount in the purse as of December 15, 2022, according to an analysis by Business Post.

This was confirmed in a statement issued by the director of information and press at the Ministry of Finance, Mr Phil Abiamuwe-Mowete.

The ECA is an account created to save the extra funds made anytime the country sells crude oil higher than the approved benchmark in the budget. For example, if the crude oil benchmark is $70 per barrel and the commodity sells for $75 per barrel, the excess $5 is saved for rainy days.

In the 2022 budget, the benchmark was $70 per barrel, and in the 2023 appropriation bill, it was raised by the National Assembly to $75 per barrel. Yesterday, the price of Brent crude, which Nigeria’s crude is graded, was sold at $82.84 per barrel in the international market, indicating that Nigeria made an extra $7.84 per barrel.

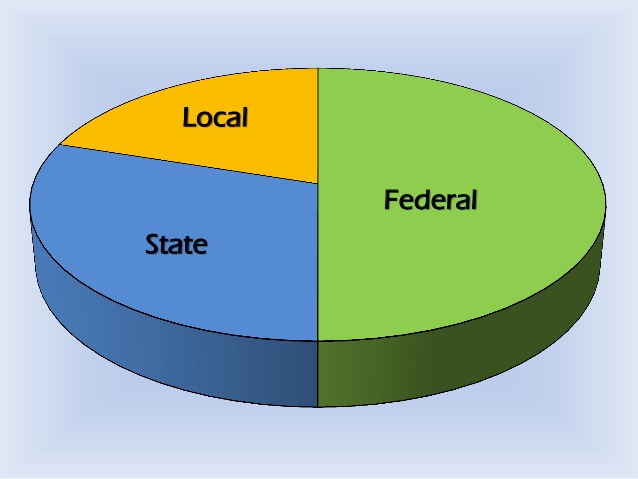

In the statement, it was disclosed that the distributed revenue generated by the country in December 2022 increased by 9.8 per cent to N990.2 billion from the N902.1 billion recorded in November 2022.

The increase was buoyed by an improvement in revenues from Petroleum Profit Tax (PPT), Companies’ Income Tax (CIT) and VAT, offsetting the decline in import duty.

The N990.2 billion shared last month comprised statutory revenue of N707.756 billion, VAT of N233.277 billion, Exchange Gain of N24.841 billion, and N24.315 billion Electronic Money Transfer Levies (EMTL).

This was disclosed at the meeting of the Federation Account Allocation Committee (FAAC) in Abuja, attended by the Commissioners of Finance of the states of the federation.

The money, which was shared by the three tiers of government, was inclusive of Gross Statutory Revenue, Value Added Tax (VAT), Exchange Gain and Electronic Money Transfer Levies (EMTL).

From the amount, the federal government received N375.306 billion, the states received N299.557 billion, the local government councils got N221.807 billion, and the oil-producing states received N93.519 billion as 13 per cent derivation of mineral revenue.

According to a communiqué issued after the gathering, the gross revenue available from VAT was N250.512 billion, which was an increase distributed in the preceding month, with N7.215 billion allocated to the NEDC project, N10.020 billion given the Federal Inland Revenue Service (FIRS) as cost of collection, and the balance of N233.277 billion given to the Nigeria Customs Service (NCS).

From the VAT earnings, the central government received N34.992 billion, the states received N116.639 billion, and the councils got N81.647 billion.

In the month, the country earned N1.1 trillion as Gross Statutory Revenue, with N31.531 billion removed as cost of collection and N396.896 billion to transfers, savings and refunds, and the balance of N707.756 billion distributed among the tiers of the government.

The federal government took N325.105 billion, states went with N165.897 billion, LGCs got N127.129 billion, and oil-producing states received N90.625 billion.

Also, the sum of N24.315 billion from EMTL was distributed last month, with the national government taking N3.648 billion, states receiving N12.157 billion, and the local councils getting N8.510 billion.

The communiqué further disclosed that N24.841 billion from Exchange Gain was shared, with the federal government receiving N11.562 billion. The states got N5.864 billion, local government councils received N4.521 billion, and oil-producing states had N2.894 billion.

By Adedapo Adesanya

Four securities weakened the NASD Over-the-Counter (OTC) Securities Exchange by 1.95 per cent on Friday, erasing N41.17 billion from the bourse, which had its market capitalisation at N2.567 trillion compared with the previous session’s N2.618 trillion.

In the same vein, the NASD Unlisted Security Index (NSI) decreased at the close of business by 85.28 points to 4,277.07 points from 4,362.32 points.

The price decliners were led by 11 Plc, which gave up N20.50 to sell at N200.50 per share compared with the preceding day’s N221.00 per share, FrieslandCampina Wamco Nigeria Plc dropped N16.94 to close at N155.20 per unit versus Thursday’s closing price of N172.14 per unit, Central Securities Clearing System (CSCS) Plc went down by N2.11 to N84.68 per share from N86.79 per share, and Afriland Properties Plc lost 11 Kobo to end at N16.74 per unit, in contrast to the N16.85 per unit it closed a day earlier.

During the trading day, the value of transactions jumped by 172.1 per cent to N29.9 million from the preceding session’s N10.9 million, and the volume of trades soared by 136.5 per cent to 955,096 units from the previous 403,901 units, while the number of deals went down by 11.4 per cent to 31 deals from 35 deals.

Great Nigeria Insurance (GNI) Plc remained the most active stock by value on a year-to-date basis, with 3.4 billion units valued at N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units worth N6.5 billion, and CSCS Plc with 68.6 million units sold for N4.7 billion.

GNI Plc also ended the session as the most traded stock by volume on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, trailed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units transacted for N415.7 million.

By Dipo Olowookere

The last trading session of this week on the floor of the Nigerian Exchange (NGX) Limited ended on a negative note, with a 0.66 per cent loss on Friday.

This was influenced by sustained selling pressure and cautious trading, which forced investors into profit-taking.

Data obtained by Business Post showed that the energy sector fell by 4.66 per cent, the insurance counter dipped by 2.23 per cent, the consumer goods index depreciated by 0.96 per cent, and the banking segment shed 0.28 per cent, while the industrial goods space remained unchanged.

At the close of business, the All-Share Index (ASI) of Nigeria’s stock exchange went down by 1,531.81 points to 232,049.02 points from 233,580.83 points, and the market capitalisation dropped N983 billion to settle at N148.905 trillion compared with Thursday’s N149.888 trillion.

Aradel was the worst-performing equity after it lost 10.00 per cent to close at N1,417.50. International Energy Insurance slipped by 9.95 per cent to N5.79, Trans-Nationwide Express depreciated by 9.89 per cent to N3.28, eTranzact crashed by 9.79 per cent to N14.75, and UPDC slumped by 9.72 per cent to N28.12.

The best-performing equity for the day was Universal Insurance, which gained 6.32 per cent to close at N1.01, McNichols grew by 5.52 per cent to N8.60, Linkage Assurance expanded by 4.67 per cent to N1.57, NGX Group appreciated by 4.35 per cent to N120.00, and Transcorp increased by 3.62 per cent to N41.50.

As look at the activity level indicated that investors traded 388.7 million stocks worth N18.4 billion in 44,631 deals compared with the 393.7 million stocks valued at N19.2 billion executed in 45,813 deals a day earlier, representing a decline in the trading volume, value, and number of deals by 1.27 per cent, 4.17 per cent, and 2.58 per cent, respectively.

By Adedapo Adesanya

The Naira recorded a loss of 82 Kobo or 0.06 per cent against the United States Dollar in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Friday, June 26, exchanging at N1,380.93/$1, in contrast to the previous day’s rate of N1,380.11/$1.

Equally, the domestic currency further weakened against the Pound Sterling in the official FX market yesterday by N6.06 to settle at N1,824.90/£1 versus the preceding session’s N1,818.84/£1, and lost N10.74 on the Euro to sell at N1,577 .58/€1 versus N1,566.84/€1.

At the GTBank forex counter, the Naira depreciated against the greenback during the session by N4 to close at N1,387/$1, in contrast to Thursday’s value of N1,383/$1, and at the parallel market, it was unchanged at N1,395/$1.

Interbank FX activity among financial institutions has fluctuated amid a sharp slowdown in forex market interventions by the Central Bank of Nigeria (CBN), as it allows demand and supply to move the market.

Also, a stronger greenback has generally put significant pressure on emerging-market currencies.

Nigeria has accessed the first tranche of a proposed $5 billion derivatives financing arrangement with First Abu Dhabi Bank PJSC, the largest lender in the United Arab Emirates (UAE).

The $5 billion facility, approved by the National Assembly earlier this year, is part of the federal government’s plan to diversify external financing sources and reduce borrowing costs. Structured as a Total Return Swap with First Abu Dhabi Bank, proceeds are earmarked for refinancing debt and supporting infrastructure financing.

If the proceeds are brought into the country through the official FX market, the transaction will increase the currency reserves or Dollar liquidity.

At the cryptocurrency market, Solana (SOL) grew by 2.2 per cent to $71.92, Cardano (ADA) gained 1.1 per cent to trade at $0.1474, Ripple (XRP) also appreciated by 1.1 per cent to $1.05, Dogecoin (DOGE) expanded by 0.9 per cent to $0.0755, and Ethereum (ETH) improved by 0.4 per cent to $1,578.84.

On the flip side, TRON (TRX) slid 0.6 per cent to $0.3203, Binance Coin (BNB) slumped by 0.3 per cent to $564.33, and Bitcoin fell by 0.2 per cent to $60,219.37, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) traded flat at $1.00 each.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn