Economy

Tinubu Not Responsible for Closure of 767 Companies in Nigeria—Wale Edun

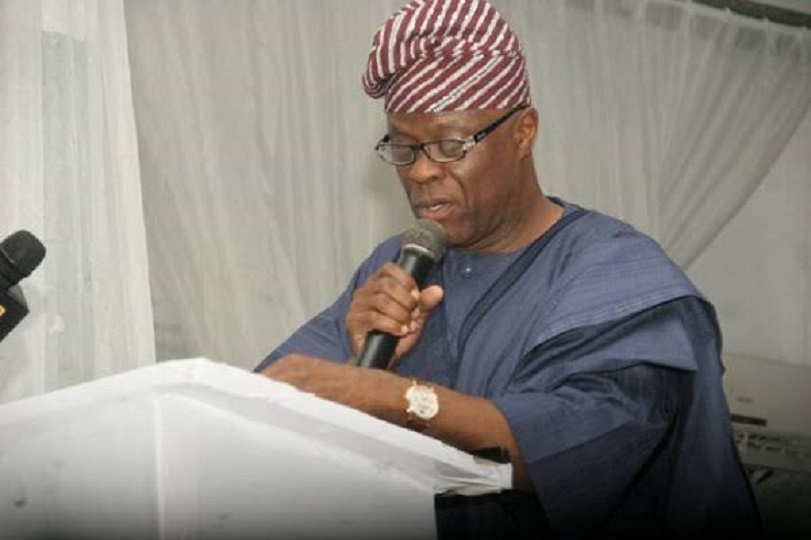

By Adedapo Adesanya

The Minister of Finance and Coordinating Minister of the Economy, Mr Wale Edun, has stated that the government of President Bola Tinubu was not responsible for the economic conditions that led to the shutdown of over 700 companies in 2023.

In a statement on Tuesday, Mr Edun explained that the closure of 767 companies in the country did not happen overnight, noting that the affected businesses were chased out of the system due to market instability, unfulfilled promises and breaches of contracts.

Recall that the Manufacturing Association of Nigeria (MAN) in a report in February indicated that about 767 manufacturing companies shut down operations in Nigeria in 2023. In addition, the association noted that another 335 companies were in distress financially in the same year, but Mr Edun said the government was already looking at the issues that led to the exit of the organisations.

“Our government inherited the assets and liabilities of the previous administration. The 800 companies or so did not make up their minds overnight. They stayed until they could stay no more.

“The conditions which sent them packing are no more. Those conditions were a foreign exchange market that was in no way fit for business where there was no liquidity.

“They were the general economic regime marked by instability, broken promises, lack of adherence to contract and so on.

“The new environment which investors face is one in which inflation is being attacked which will eventually lead to lower interest rates where investors can use the very vibrant domestic market to add their equities and invest,” he said.

Mr Edun also disclosed that the oil and gas sector received approximately $7 billion investment pledge due to the new incentive frameworks introduced by President Tinubu’s administration.

He said that the investment had been dormant for years, awaiting the appropriate economic conditions for inflow.

He also highlighted the CNG-fueled conversion programme as part of the administration’s policy framework to drive growth.

“CNG is a government policy not just for vehicles, but for generators. They have to be either CNG-fueled or solar-based or electric vehicles.

“That is the new incentive structure. And it continues also in the oil and gas sector. There has just been a new set of incentives that are encouraging new investments.

“We expect $7bn worth of investments that have been sitting on the sidelines to now come in.

“A stable, growing economy attracts investment that increases productivity, grows the economy further, creates jobs and reduces poverty. That is the trajectory that Nigeria is now on,” he noted.

The Minister also disclosed that Nigeria’s economy was returning to the path of positive growth with a Gross Domestic Product (GDP) growth rate of 2.98 per cent in the first quarter of 2024, adding that the 2.98 per cent growth rate was higher than last year’s GDP growth rate of 2.31 per cent.

Speaking on interventions of the government in the last year, he said, “Efforts have been made to improve food security, with N200bn allocated to programmes.

“Also, access to credit has also been improved, with N100bn allocated to consumer credit and grants of N50,000 being given to one million nano industries.”

By Aduragbemi Omiyale

The pre-registration training and examination for capital market operators (CMOs) for the second quarter of 2026 has been postponed.

Business Post gathered that the new date for the exercise is now Monday, June 15, 2026.

This information was disclosed by the Securities and Exchange Commission (SEC) through a circular on Monday, June 8, 2026.

The Nigerian capital market regulator stated that this postponement has also resulted in the extension of the deadline for registration to Friday, June 12, 2026.

In the notice today, the SEC expressed its regret for the inconvenience this action may cause operators, who had prepared for the initial date of the training and examination.

“Further to the recent circular on Q2 2026 Pre-registration Training and Examination, the Securities and Exchange Commission (SEC) hereby informs all eligible applicants for the Q2 2026 Pre-registration Training and Examination that the commencement date has been postponed to Monday, June 15, 2026.

“Registration on the designated portal has also been extended to Friday, June 12, 2026. All other conditions contained in the circular remain unchanged.

“The commission regrets any inconvenience this postponement may cause and appreciates the understanding of all applicants,” the disclosure noted.

By Aduragbemi Omiyale

One of the leading healthcare firms in Nigeria, Fidson Healthcare Plc, has listed additional shares on the Nigerian Exchange (NGX) Limited.

The new stocks absorbed into the stock market were 600 million units, raising the total issued and fully paid-up shares of Fidson to 3,000,000,000 ordinary shares of 50 Kobo each from 2,400,000,000 ordinary shares of 50 Kobo each.

The fresh equities came from the company’s rights issue of 600,000,000 ordinary shares of 50 Kobo each at N35.00 per share.

They were issued to existing investors on the basis of one new ordinary share for every existing four ordinary shares held as of the close of business on Wednesday, November 12, 2025.

Confirming the development, the regulator in a notice said, “Trading licence holders are hereby notified that an additional 600,000,000 ordinary shares of 50 Kobo each of Fidson Healthcare Plc were on Tuesday, June 2, 2026, listed on the daily official list of Nigerian Exchange Limited.

“The additional shares arose from the company’s rights issue of 600,000,000 ordinary shares of 50 Kobo each at N35.00 per share on the basis of one new ordinary share for every existing four ordinary shares held as at the close of business on Wednesday, November 12, 2025.

“With the listing of the additional 600,000,000 ordinary shares, the total issued and fully paid-up shares of Fidson Healthcare Plc have now increased from 2,400,000,000 to 3,000,000,000 ordinary shares of 50 Kobo each.”

By Modupe Gbadeyanka

This news will surely excite local contractors with verified claims of N100 million or less, as the federal government has approved their payments.

This approval for the disbursement was given by the Minister of Finance and Coordinating Minister of the Economy, Mr Taiwo Oyedele.

This followed a verification and reconciliation exercise designed to ensure only validated claims qualify for payment.

The beneficiaries cover contractors across multiple ministries, departments and agencies. The release of the funds is expected to enable contractors to return to project sites, pay workers, settle suppliers and meet outstanding financial commitments.

In an announcement on Monday, the Federal Ministry of Finance also said this latest batch of payments would ease liquidity pressure on small businesses and accelerate economic activity nationwide.

It was noted that the payments for verified claims of N100 million below were strategically done to spread economic impact broadly rather than concentrate disbursements among a handful of large firms.

The payments form part of a broader push to clear inherited contractor obligations, with over N700 billion verified in recent months.

“For many beneficiaries, the release of funds represents more than a financial transaction. It provides the certainty needed to sustain operations, preserve jobs, complete ongoing projects, and contribute to economic recovery and growth,” the ministry said in a statement.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn