Media OutReach

Octa broker’s take on CBDCs vs. crypto: key insights for traders in 2025

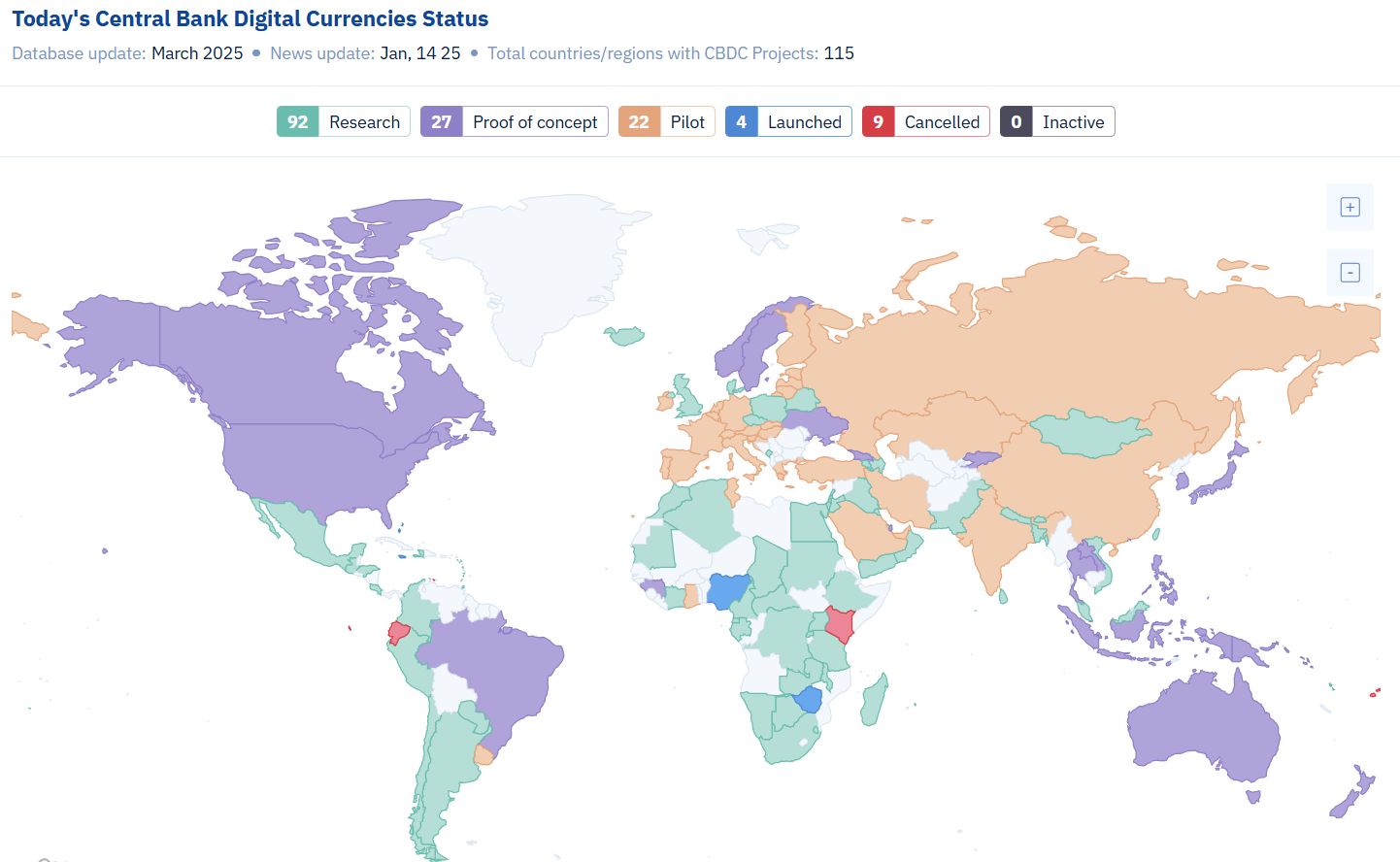

According to recent data, over 130 countries representing 98% of global GDP are now exploring CBDCs in some form, including pilots, development, or research (albeit few have fully adopted them). This rise reflects both technological momentum and regulatory intent to reclaim control over digital currency ecosystems, especially as private stablecoins and decentralised crypto assets have proliferated.

The main differences between CBDCs and cryptocurrencies

Stability and trust

While cryptocurrencies like Bitcoin or Ethereum operate in highly volatile and speculative environments, CBDCs are anchored to fiat currencies and issued by central banks. This offers higher value stability and institutional backing, reducing the risk profile for users.

Design and oversight

CBDCs are programmable but centrally managed. Governments can impose compliance measures and offer consumer protection in ways decentralised crypto systems cannot. Moreover, unlike crypto assets, CBDCs are not mined or privately issued, ensuring state control over monetary supply and transaction oversight.

Kar Yong Ang, financial market analyst at Octa, notes: ‘CBDCs offer a new model of digital liquidity—blending state trust and legal tender with tech efficiency. For traders, this opens doors to a more secure and transparent digital finance ecosystem.’

The global race to develop CBDCs and the drivers behind it

Here are three key reasons why central banks invest resources in CBDSs:

- The decline of cash and rise of digital payments. As societies increasingly favour digital over physical money, central banks face pressure to modernise public currency formats. In Sweden, for example, cash transactions make up less than 10% of payments. CBDCs are seen as a public alternative to private payment apps and platforms, ensuring monetary sovereignty in the digital realm.

- Controlling private stablecoin risks. Private stablecoins like USDT and USDC have raised concerns over systemic risk and shadow banking practices. A CBDC can serve as a stable counterbalance to these instruments, offering liquidity and legal clarity in fast-evolving financial markets.

- Financial inclusion and transparency. CBDCs can increase financial inclusion by offering digital wallets to unbanked populations, especially in developing economies. They also offer governments more visibility into money flows, enhancing tax collection and curbing illicit finance—though this has sparked debate around surveillance and privacy.

Pros and cons of CBDCs

CBDCs offer notable advantages: their value is typically pegged to fiat currencies, ensuring greater price stability than most cryptocurrencies. With full state backing, they function as legal tender and may include programmable features like conditional payments. For underbanked populations, they also present a path toward improved financial access.

However, concerns remain. Privacy is a major issue, as CBDCs could give governments visibility into personal transactions. They also pose cybersecurity risks, potentially becoming targets for large-scale attacks. Moreover, they could interfere with traditional monetary policy and financial market dynamics if not carefully designed. For instance, commercial banks could experience deposit runs if individuals perceive CBDCs as a safer alternative to traditional money for savings.

Real-world cases

Although the majority of countries still research CBDC and their application in the economy, some have already implemented them.

- Bahamas. The Sand Dollar became the first nationwide CBDC in 2020. It now serves all islands through a network of mobile-based wallets.

- Nigeria. The eNaira, launched in 2021, has seen a slow adoption of less than 0.5% as of 2025. The government continues to offer incentives to boost usage.

- China. The e-CNY has been piloted in over 25 cities and integrated into public transit and e-commerce platforms. Its scale makes it the most advanced major-economy CBDC.

Looking ahead: the road to adoption

While CBDCs promise greater efficiency and offer more tools for governments to implement social objectives, they also pose new governance challenges. To thrive, states will have to balance innovation with civil liberties, infrastructure resilience, and global interoperability. As the world of digital currencies continues to develop, CBDCs are increasingly important for progressive traders to grasp. Keeping up with developments can give a vital advantage in understanding the future of money.

___

Disclaimer: This content is for general informational purposes only and does not constitute investment advice, a recommendation, or an offer to engage in any investment activity. It does not take into account your investment objectives, financial situation, or individual needs. Any action you take based on this content is at your sole discretion and risk. Octa and its affiliates accept no liability for any losses or consequences resulting from reliance on this material.

Trading involves risks and may not be suitable for all investors. Use your expertise wisely and evaluate all associated risks before making an investment decision. Past performance is not a reliable indicator of future results.

Availability of products and services may vary by jurisdiction. Please ensure compliance with your local laws before accessing them.

Hashtag: #Octa

The issuer is solely responsible for the content of this announcement.

Octa

![]() Octa is an international CFD broker that has been providing online trading services worldwide since 2011. It offers commission-free access to financial markets and various services used by clients from 180 countries who have opened more than 52 million trading accounts. To help its clients reach their investment goals, Octa offers free educational webinars, articles, and analytical tools.

Octa is an international CFD broker that has been providing online trading services worldwide since 2011. It offers commission-free access to financial markets and various services used by clients from 180 countries who have opened more than 52 million trading accounts. To help its clients reach their investment goals, Octa offers free educational webinars, articles, and analytical tools.

The company is involved in a comprehensive network of charitable and humanitarian initiatives, including the improvement of educational infrastructure and short-notice relief projects supporting local communities.

In Southeast Asia, Octa received the ‘Best Trading Platform Malaysia 2024’ and the ‘Most Reliable Broker Asia 2023’ awards from Brands and Business Magazine and International Global Forex Awards, respectively.

Media OutReach

Siam Piwat appoints The Bureau of Wonders as international public relations consultant for Siam Paragon Bangkok Watch Week 2026

The Bureau of Wonders (BOW), a leading strategic communications and luxury brand consultancy, will collaborate with Siam Piwat to lead international market communications, elevate global awareness, and strengthen Siam Piwat’s position as a leading luxury destination developer.

Returning for its second edition, Siam Paragon Bangkok Watch Week 2026 will take place from 22–27 September 2026, reinforcing Bangkok’s position as Southeast Asia’s emerging capital of watch culture and haute horology. The event will bring together renowned watchmaking maisons, collectors, and connoisseurs from around the world to celebrate craftsmanship, innovation, and the heritage of fine timepieces.

Through this partnership, Siam Piwat aims to enhance international media engagement and further establish Thailand as a global destination for luxury, tourism, and retail experiences.

Hashtag: #SiamPiwat #BangkokWatchWeek2026 #TheBureauOfWonders #SiamParagon #SiamParagonBangkokWatchWeek2026 #LuxuryWatchDestination

![]() https://www.siampiwat.com/en/home

https://www.siampiwat.com/en/home![]() https://www.linkedin.com/company/siam-piwat/

https://www.linkedin.com/company/siam-piwat/![]() https://www.facebook.com/siampiwat.official/

https://www.facebook.com/siampiwat.official/![]() https://www.instagram.com/siampiwat_official/

https://www.instagram.com/siampiwat_official/

The issuer is solely responsible for the content of this announcement.

Siam Piwat

Siam Piwat is a leading retail and real estate developer behind Bangkok’s most iconic destinations, including Siam Paragon, Siam Center, Siam Discovery, ICONSIAM, and Siam Premium Outlets Bangkok, globally recognized for pioneering experiential destinations.

For over six decades, Siam Piwat has been renowned for creating iconic destinations and world-class experiences, continuously redefining Bangkok’s retail landscape through award-winning developments that set new global benchmarks. Guided by creativity, innovation, and sustainability, the company continues to lead with a bold vision that inspire, engage, and delight customers from around the world, while creating long-term value for society, businesses, and future generations.

The Bureau of Wonders

The Bureau of Wonders is an innovative communications agency renowned for its expertise in public relations, events, content creation, and brand strategy. With a focus on luxury, fashion, retail, beauty, lifestyle, hospitality, F&B, and the arts, we craft compelling narratives that resonate with an exclusive clientele across Southeast Asia’s vibrant markets.

Media OutReach

Construction Management Awards 2026 – Now open for nomination Introduction of the Inaugural “Excellent Construction Safety Culture Award” Guides the Construction Industry Toward a New Milestone in Safety

Deepening “Corporate Leadership, On-Site Implementation” to Reflect Excellent Governance Standards

Entering its sixth edition, the Awards continue to uphold their mission of creating a credible exchange platform for industry elites. In recent years, with society’s high emphasis on occupational safety and health, along with the widespread application of smart construction technologies, site safety has gone far beyond the traditional, rigid mindset of “checking in and re-inspecting”. The Institute thoroughly understands that excellent site safety performance does not rely solely on the routine compliance execution of frontline sites; it must stem from the forward-looking vision and comprehensive policy drive of corporate management.

To this end, this year’s Awards have comprehensively enhanced the judging criteria. Building upon the existing award categories, the judging perspective has been extended from frontline construction management to the macro corporate level, significantly increasing the weight of the “Safety” element in scoring to elevate industry standards. This edition will more comprehensively and deeply review the effectiveness of corporations in formulating and implementing safety management policies. In addition to frontline execution capabilities, the judging panel will place greater emphasis on how corporations promote an excellent construction safety culture from a policy level, including integrating tech solutions like Smart Site Safety Systems (SSSS) into long-term development strategies to safeguard site safety. Furthermore, special emphasis is placed this year on how corporations establish long-term accident prevention and continuous improvement mechanisms through institutional frameworks, embedding safety concepts into the core of corporate governance to lead a comprehensive transformation of the safety culture in Hong Kong’s construction industry.

Inaugural “Excellent Construction Safety Culture Award” with a Dedicated Judging Panel Establishes Industry Authority

Cr Alfred TANG, President of the Hong Kong Institute of Construction Managers, stated: “Site safety has always been the core focus most valued by the Government and the Institute. The Institute firmly believes that ‘Corporate Leadership, Safety Implementation, Everyone’s Responsibility’ is the key to driving industry transformation. To encourage more developers, main contractors, and stakeholders to actively play a top-down driving role, this year’s Awards have introduced the ‘Excellent Construction Safety Culture Award’, supported by an independent ‘Dedicated Safety Judging Panel’ composed of top senior safety experts and consultants in the industry to review the long-term effectiveness of corporate safety policies from the most rigorous and professional perspective. We firmly believe that this brand-new award and dedicated judging mechanism will effectively drive continuous progress in Hong Kong’s construction industry, laying a solid foundation for building a sustainable, safe, and highly efficient future.”

The “Construction Management Awards 2026” is opening for nominations from today until 31 August 2026. For details about the Awards, nomination forms, and judging criteria, please visit the Awards website (www.hkicm-cma.com).

Award Categories Overview

| Award Categories | Team / Corporate Awards | Corresponding Individual Award Categories |

| Building Project | Excellent Construction Team Award (Building Project) | A) Construction Manager Award B) Site Manager Award C) Engineer Award D) EHS Officer Award E) Construction Supervisor Award |

| Civil Project | Excellent Construction Team Award (Civil Project) | A) Construction Manager Award B) Site Manager Award C) Technical Manager Award D) Engineer Award E) EHS Officer Award F) Construction Supervisor Award |

| Corporate Project | A) Excellent Construction Safety Culture Award B) Excellent Construction Innovation Enterprise |

/ |

| Individual Project | / | Young Construction Manager Award |

Jury Panel

Chairman of the Judging Panel (Building Project):

Mr HO Chun Hung, JP, Director of Buildings, Buildings Department, HKSARG

Members of the Judging Panel (In apathetical order of surnames):

- Ir CHAN Siu Chung, Cedric, Chairman of Building Division, The Hong Kong Institution of Engineers

- Prof CHAN, Isabelle Y. S., Associate Dean of the Faculty of Architecture; Associate Professor at the Department of Real Estate and Construction, The University of Hong Kong

- Mr LEE Hok-yin, Arthur, JP, Deputy Director/Regulatory Services, Electrical & Mechanical Services Department, HKSARG

- Cr TANG Yu-chi, Alfred, President, The Hong Kong Institute of Construction Managers

- Sr WAN Wai Ming, Tony, President, The Hong Kong Institute of Surveyors

- Ir Prof Michael C. H. YAM, Head of Department of Building and Real Estate, The Hong Kong Polytechnic University

- Mr Emil YU Chen-on, President, The Hong Kong Federation of Electrical & Mechanical Contractors Limited

Chairman of the Judging Panel (Civil Project):

Mr HO Ying Kit, Tony, JP, Deputy Secretary for Development (Works) 3, Development Bureau, HKSARG

Members of the Judging Panel (In apathetical order of surnames):

- Ir Benjamin CHAN, JP, Project Manager (West), Civil Engineering and Development Department, HKSARG

- Cr CHAN Chi-man, Vice President, The Hong Kong Institute of Construction Managers

- Ir CHAN Ho-yee, Vice chairperson of Civil Division, The Hong Kong Institution of Engineers

- Prof Jack Chin Pang CHENG, Associate Head of Civil and Environmental Engineering, The Hong Kong University of Science and Technology

- Mr HO Kwing-kwong, Alex, Director – Industry Development, Construction Industry Council

- Mr NG Wai-hong, Patrick, Project Manager/Major Works, Highways Department, HKSARG

- Prof Songye ZHU, Interim Head of Department of Civil and Environmental Engineering, The Hong Kong Polytechnic University

Members of the Excellent Construction Safety Culture Award Judging Panel (In alphabetical order of surnames):

- Prof Dr Daron Wai Kwong LEUNG, Safety Adviser, The Hong Kong Institute of Construction Managers

- Dr Winson YEUNG, Principal Consultant, Occupational Safety & Health Council

Hashtag: #HKICM

The issuer is solely responsible for the content of this announcement.

About HKICM

Established in 1997 with the sovereignty handover, Hong Kong Institute of Construction Managers (“Institute” or “HKICM”) is the only local professional institution representing the construction management profession in Hong Kong. The Institute has developed rapidly, with its members reached 3,439, of which 1,285 were Corporate Members (including Fellows and Members).

Our objectives are to secure the advancement and facilitate the acquisition of knowledge and expertise which constitutes and promotes the practice of and professionalism in construction management. The works of the Institute include setting standards for professional services and performance, establishing rules of conduct, promoting Registered Construction Managers and Construction Supervisors and promulgating the recognition of professional site supervisors. We believe that all construction sites need to be managed by registered professional construction managers to ensure compliance of operation with government laws, safety and environmental protection requirements. In order to improve the professional standard of technical personnel in an orderly manner, the government needs to register and recognize the professional qualifications of site supervisors.

In a rapidly evolving employment landscape, higher education institutions are expected not only to provide academic knowledge but also to support students in developing the relationships and networks that can contribute to personal growth and professional readiness.

The Role of Peer Connections in Student Development

University friendships often form an important part of the student experience. Developed through classes, group projects, student organisations, volunteering initiatives and campus activities, these relationships can provide a sense of community and belonging throughout a student’s academic journey.

Research has consistently highlighted the role of peer support in student engagement, wellbeing and academic persistence. Strong social connections can help students adapt to new learning environments, navigate challenges and participate more actively in campus life. For international students in particular, peer networks often play an important role in easing cultural transitions and fostering inclusion.

Beyond graduation, these relationships frequently evolve into long-term personal and professional networks that continue to provide support throughout different stages of life and career development.

Professional Networks and Career Readiness

Alongside peer relationships, professional networks have become an increasingly important component of higher education. Connections with alumni, faculty members, career advisors, employers and industry practitioners can provide students with valuable insights into workplace expectations, emerging industry trends and potential career pathways.

Such interactions help bridge the gap between academic learning and employment by exposing students to real-world perspectives and opportunities. Early engagement with industry networks can also support career planning, mentorship and professional development, equipping students with a deeper understanding of the skills and competencies required in the workforce.

As employers place greater emphasis on workplace readiness and transferable skills, access to professional networks can complement academic qualifications and enhance graduates’ ability to navigate competitive labour markets.

Integrating Student Life and Career Development

Many higher education institutions are responding to evolving student expectations by adopting a more holistic approach to education. This includes creating opportunities for students to engage in co-curricular activities, leadership development programmes, community initiatives and career-related experiences alongside their academic studies.

At SIM Global Education (SIM GE), student engagement initiatives and career development resources form part of a broader ecosystem designed to support both personal and professional growth. Through student clubs, leadership opportunities and career advisory services, students can build interpersonal skills, expand their networks and explore future career possibilities throughout their studies.

For prospective students comparing higher education options, the question is not whether university friendships or professional networks matter more. Both are important. University friends provide belonging, encouragement and shared experiences, while professional networks provide exposure, guidance and access to future opportunities. In an education environment where students are increasingly conscious of wellbeing, employability and return on education, institutions that integrate student life, career development and holistic support are better positioned to meet evolving expectations. A meaningful higher education experience is shaped not only by qualifications, but also by the relationships, confidence and networks that students carry forward.

Looking Ahead

As higher education continues to evolve, students are increasingly seeking learning environments that support both academic achievement and broader developmental outcomes. While qualifications remain important, the relationships, experiences and networks developed during university can also play a significant role in shaping future opportunities.

For prospective students, evaluating higher education options may therefore involve looking beyond curriculum and rankings to consider how institutions foster community, professional engagement and personal development. Together, these elements contribute to a more holistic educational experience and can support students as they prepare for the next stage of their academic, professional and personal journeys.

Reference:

- SIM Global Education Overview – https://www.sim.edu.sg/degrees-diplomas/sim-global-education/university-partners-sim-ge/sim-ge

- SIM CCA – https://www.sim.edu.sg/degrees-diplomas/life-at-sim/co-curricular-activities

- SIM Project 1095 – https://project1095.simge.edu.sg

- SIM Student Life – https://project1095.simge.edu.sg/student-life

- SIM Student Care – https://project1095.simge.edu.sg/student-care

- SIM Career Services – https://www.sim.edu.sg/degrees-diplomas/life-at-sim/career-services

- SIM Advantage – https://www.sim.edu.sg/degrees-diplomas/sim-global-education/sim-advantage

- NDPI Peer Support – https://www.mdpi.com/2227-7102/15/5/602

Hashtag: #SIMGlobalEducation #SIMGE #GlobalEducation #InternationalDegree #CareerReady #FutureSkills

The issuer is solely responsible for the content of this announcement.

About SIM Global Education

SIM Global Education (SIM GE) is a leading private education institution in Singapore and the region. We offer more than 140 academic programmes ranging from diplomas and graduate diploma programmes to bachelor’s and master’s degree programmes with some of the world’s most reputable universities from Australia, Canada, Europe, United Kingdom, and the United States. SIM GE’s cohort is made up of 17,000 full- and part-time students and adult learners, of which approximately 41% are international students hailing from over 50 countries.

SIM GE’s holistic learning approach and culturally diverse learning environment aim to equip students with knowledge, industry skills and employability competencies, as well as a global perspective to succeed as future leaders in a fast-changing, technologically driven world.

For more information on SIM Global Education, visit www.sim.edu.sg

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn