Economy

October FAAC: FG, States, Councils Share N2.103trn From September Earnings

By Adedapo Adesanya

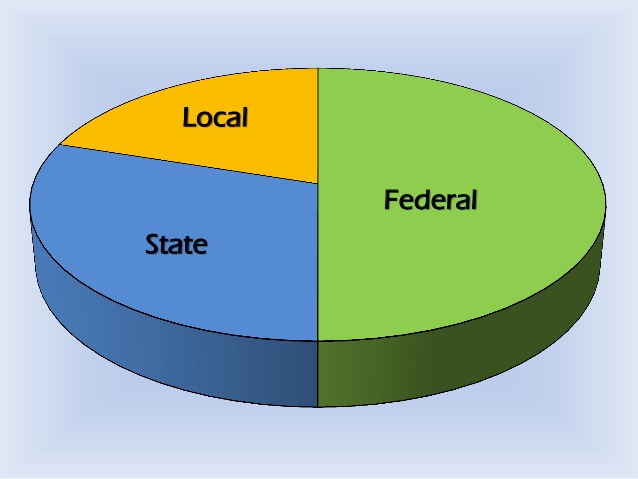

The Federation Account Allocation Committee (FAAC) shared N2.103 trillion from the revenue generated by the nation in September 2025 to the federal government, states, and local government councils.

The allocation was made at the October 2025 FAAC meeting held in Abuja.

The N2.103 trillion total distributable revenue comprised statutory revenue of N1.239 trillion; Value Added Tax (VAT) of N812.593 billion; and Electronic Money Transfer Levy (EMTL) of N51.684 billion.

A statement issued by the Director of Information in OAGF, Mr Bawa Mokwa, revealed that gross total revenue available in September 2025 stood at N3.054 trillion.

From this amount, N116.149 billion was deducted as the cost of collection, while N835.005 billion went to transfers, interventions, refunds, and savings.

The gross statutory revenue for the month was N2.128 trillion, lower than the N2.838 trillion recorded in August 2025 by N710.134 billion.

Conversely, VAT revenue rose to N872.630 billion in September, compared to N722.619 billion in August—an increase of N150.011 billion.

From the total distributable revenue of N2.103 trillion, allocations were as follows, federal government: N711.314 billion, state governments: N727.170 billion, Local Government Councils: N529.954 billion, and derivation (13 per cent of mineral revenue): N134.956 billion to benefiting states.

Of the N1.239 trillion statutory revenue, the federal government received N581.672 billion, the states received N295.032 billion, and the Local Governments got N227.457 billion, with N134.956 billion shared as 13% derivation revenue to oil-producing states.

From the N812.593 billion VAT revenue, the Federal Government received N121.889 billion, the States got N406.297 billion, and the Local Governments received N284.408 billion.

Additionally, from the N51.684 billion EMTL, the federal government received N7.753 billion, the States got N25.842 billion, and the Local Governments received N18.089 billion.

The communiqué noted that in September 2025, Import Duty, VAT, and EMTL recorded significant increases, while Companies Income Tax (CIT) and CET Levies declined considerably. Petroleum Profit Tax (PPT) increased marginally, whereas Oil and Gas Royalties and Excise Duty experienced slight decreases.

By Aduragbemi Omiyale

The Stanbic IBTC Bank Nigeria Purchasing Managers’ Index (PMI) for the Nigerian private sector in July 2026 contracted to 52.5 points from 53.4 points in June 2026, a statement made available to Business Post has shown.

This occurred despite the business environment sustaining its growth last month, with an increase in new orders experienced, as inflationary pressures softened, and output and employment modestly rising.

The Head of Equity Research West Africa at Stanbic IBTC Bank, Mr Muyiwa Oni, said the PMI indicated that the private sector recorded its slowest since March 2026, as businesses also increased their input purchasing activity to keep up with current demand requirements and prepare for future workloads.

“Nigerian businesses reported improved customer demand in July while better pricing and new product launches also helped them to capture new orders arising from the increase in demand. These factors helped to keep the private sector activity in an expansionary territory, although this moderated when compared to June,” he was quoted as saying.

It was stated that while input costs increased at their slowest pace in five months, panellists reported higher costs for fuel and raw materials. Selling prices also softened in line with the picture for input costs in July.

Headline inflation eased slightly to 15.91 per cent y/y in June from 15.93 per cent y/y in May, snapping three consecutive months of price increases.

Although July inflation is likely to be higher m/m, it is expected to print lower, likely at 15.72 per cent y/y, primarily driven by favourable base effects from the corresponding period of last year, because there are no expectations of the magnitude of m/m inflation witnessed in July 2025 (1.99 per cent) to materialise this year.

“We retain our 2026 growth forecasts at 4.1 per cent as we see the oil sector growing by 3.45 per cent y/y in 2026, from 8.50 per cent y/y in 2025, while the non-oil sector is likely to grow by 4.11 per cent y/y, from 3.71 per cent y/y in 2025.

“The risks to our outlook include country-wide insecurity which may constrain food production, exchange rate pressures resurfacing, extreme-weather related conditions and higher fertiliser prices impacting crop yield, and a volatile global environment which may affect sentiment and constrain capital flows,” Mr Oni noted.

By Adedapo Adesanya

Sahara Upstream, a Nigeria-focused crude producer, has deployed a new 380,000-barrel tanker to boost exports from the OML 18 block as part of a wider push by domestic operators to invest in infrastructure and lift output and exports for Africa’s biggest oil producer.

The MT D Adesanya, which can hold more than 62,000 cubic metres of crude, will operate alongside the MT D Bayero, receiving crude from shuttle vessels at Bonny Anchorage, one of Nigeria’s main crude export hubs, before transferring it to the FSO Cawthorne storage facility.

Sahara said the tanker would help cut turnaround times, currently about 30 to 48 hours, and support a planned 50 per cent increase in exports from the block’s current level of about 950,000 barrels per month.

The block currently produces about 36,000 barrels per day, according to data from the Nigerian Upstream Petroleum Regulatory Commission (NUPRC), with Sahara targeting output of 60,000 barrels per day.

OML 18 is one of the Niger Delta’s oldest producing assets. It began production in 1970 and contains an estimated 1.5 billion barrels of oil equivalent in reserves.

Shell, Total and Eni sold their combined interests to Eroton in 2015 as part of a broader shift toward domestic ownership in Nigeria’s upstream sector.

This development comes as Sahara Upstream is deepening its exploration and production footprint through Asharami Energy Limited (AEL), its upstream E&P business, which says it is targeting 350,000 barrels of oil per day by 2030 through its subsidiary, Enageed Resources Limited (ERL).

The growth target comes as AEL also marks a major safety milestone, achieving 6 million Lost Time Injury (LTI)-free man-hours in its OML-148 operations — reinforcing the company’s commitment to operational excellence and safety leadership.

According to Asharami Energy, the milestone reflects its ability to execute complex operations safely, in line with Sahara’s Beyond XXX vision, which builds on the group’s 30-year legacy of responsible enterprise while marking its next chapter of impact, innovation, and sustainable growth.

The developments position Sahara Upstream and its subsidiaries among the domestic operators driving increased investment in Nigeria’s oil and gas infrastructure, as the group works to scale up production and exports for Africa’s biggest oil producer.

By Aduragbemi Omiyale

One of the leading energy firms in Nigeria, Aradel Holdings Plc, has expressed its desire to optimise its enlarged portfolio and improve operational efficiency in the second half of 2026.

The company is planning to build on the success it recorded in the first half of the year, where it grew its revenue by 577 per cent to N2.5 trillion from N368.1 billion in H1 2025.

The significant rise in earnings was driven by higher production volumes together with stronger realised crude oil and gas prices, with the average at $90.4/bbl and $2.08/mmscf, respectively.

In the period under review, the Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) increased by 688 per cent to N1.4 trillion from N176.4 billion in the corresponding period of last year, while the operating profit surged by 789 per cent to N1.1 trillion from N118.6 billion due to higher revenue and crude handling income at N149.8 billion, partly offset by underlift cost and general and administrative costs.

The net cash generated from operations was N975.6 billion between January and June 2026 versus N140.8 billion in the same period of 2025, reflecting the cash generation of the enlarged organisation.

The net debt contracted by 70 per cent on a year-to-date basis to N46.5 billion from N475.1 billion as of December 31, 2025.

Aradel, in the period under consideration, improved its post-tax profit by 30 per cent to N191.0 billion from N146.4 billion, a development that impressed its chief executive, Mr Adegbite Falade, who said, “A firmer price environment supported performance, generating net cash from operating activities of N975.6 billion and a closing cash balance of N1.7 trillion.”

“Our enlarged portfolio provides more opportunities to generate stronger cash flow and returns for shareholders and unlocking that potential is our main focus.

“We reaffirm our full year production guidance of 110 – 140 kboepd and remain committed to operating responsibly in a changing energy landscape and to delivering lasting value for our stakeholders,” he stated.