Economy

NNPC Lying About Reason for Fuel Scarcity—Oil Marketers

By Dipo Olowookere

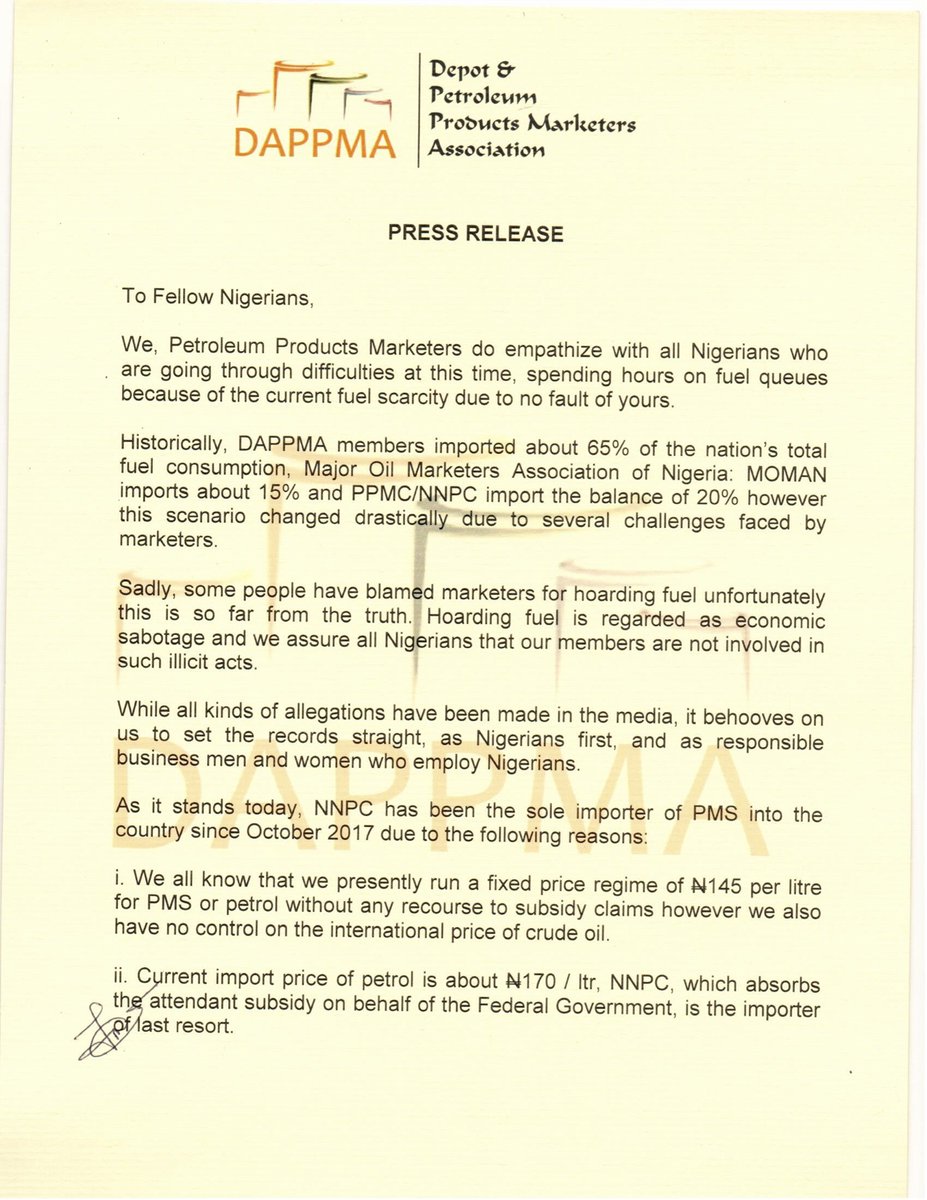

Nigerian National Petroleum Corporation (NNPC) has been accused of not being truthful to Nigerians on the main cause of the present shortage of Premium Motor Spirit (PMS), otherwise known as petrol, across the country.

Oil marketers, under the umbrella of Depot and Petroleum Products Marketers Association (DAPPMA), in a statement dated Monday, December 25, 2017, denied claimed by government that they were behind the situation through hoarding of the product.

In the statement signed by the Executive Secretary of DAPPMA, Mr Olufemi Adewole, it was explained that the main reason for the shortage was because the state-owned oil firm was not importing enough fuel that will meet the demand of citizens.

“Some people have blamed marketers for hoarding fuel. Unfortunately, this is so far from the truth. Hoarding fuel is regarded as economic sabotage and we assure all Nigerians that our members are not involved in such illicit acts,” the oil marketers said.

Speaking further, DAPPMA said normally, it imports 65 percent of the country’s consumption with Major Oil Marketers Association of Nigeria (MOMAN) bringing in 15 percent, and the NNPC importing the remaining 20 percent.

The group said however, since October 2017, the NNPC has been the sole importer of petrol into the country.

Giving reason for this, DAPPMA said the landing cost of petrol was now N170 per litre and with the government capping pump price at N145 per litre without room for increment, it was impossible for its members to import fuel into Nigeria and still sell at N145 per litre to Nigerians.

“As it stands today, NNPC has been the sole importer of PMS into the country since October 2017 due to the following reasons’

“We all know that we presently run a fixed price regime of N145 per litre for PMS without any recourse to subsidy claims, however, we also have no control on the international price of crude oil.

“Current import price of petrol is about N170 per litre, NNPC, which absorbs the attendant subsidy on behalf of the Federal Government, is the importer of last resort.

“We understand that the NNPC meets this demand largely through its DSDP framework; however, due to price challenges on the DSDP platform, some participants in the scheme failed to meet their supply quota of refined petroleum products, especially PMS, to NNPC. This is the main reason for this scarcity.”

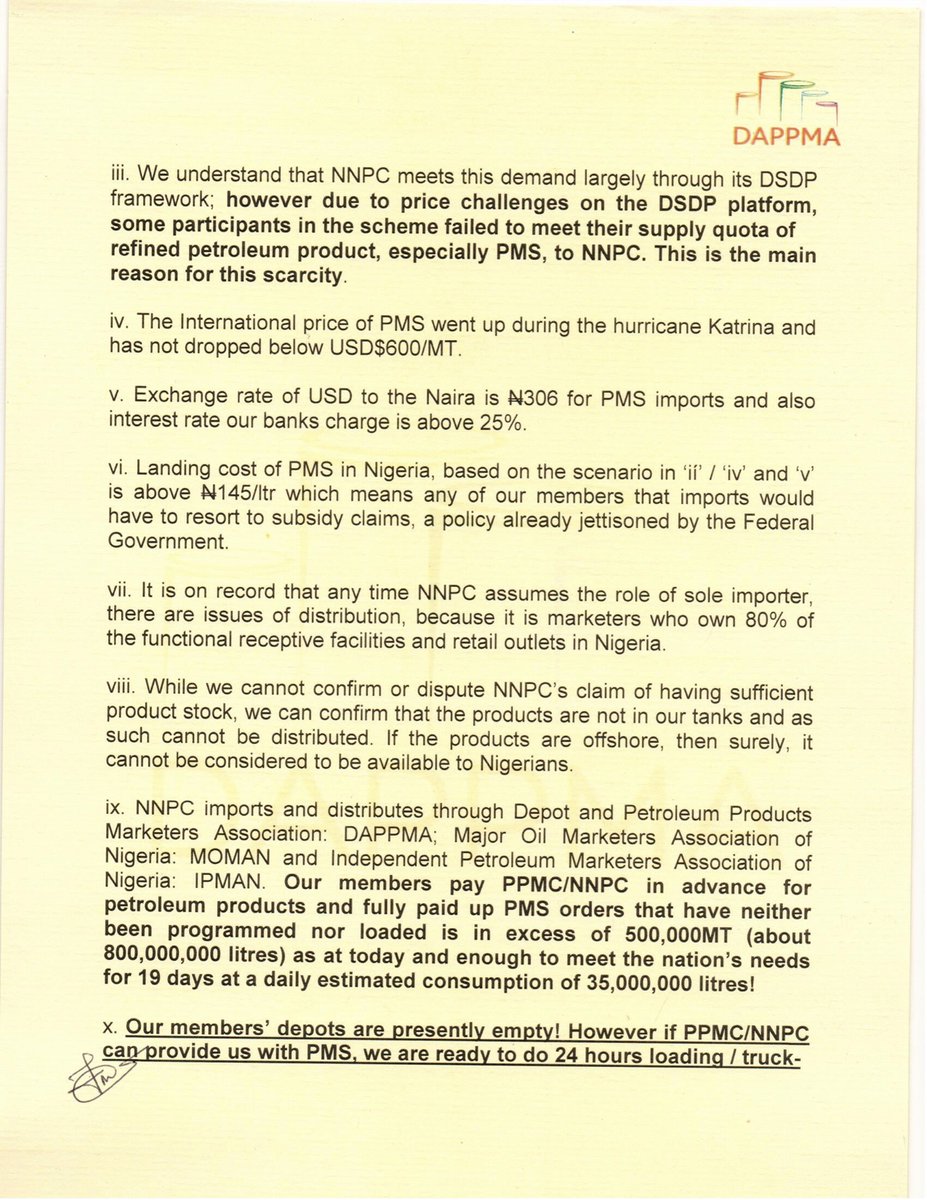

“The international price of PMS went up during the Hurricane Katrina and has not dropped below $600 per metric tonne.

“The exchange rate of the Dollar to the Naira is N306 for PMS imports and also interest rate our banks charge is above 25 percent.

“Landing cost of PMS in Nigeria, based on the scenario above is more than N145 per litre, which means any of our member that imports would have to resort to subsidy claims, a policy already jettisoned by the Federal Government,” it said.

Reacting to the claims by NNPC that it has enough fuel to meet the demands on Nigerians, the association said, “It is on record that anytime the NNPC assumes the role of sole importer, there are issues of distribution, because it is marketers who own 80 percent of the functional receptive facilities and retail outlets in Nigeria.

“While we cannot confirm or dispute NNPC’S claims of having sufficient product stock, we can confirm that the products are not in our tanks and as such cannot be distributed. If the products are offshore, then surely, it cannot be considered to be available to Nigerians.”

It further noted that, “NNPC imports and distributes through DAPPMA, Major Oil Marketers Association of Nigeria (MOMAN), and Independent Petroleum Marketers Association of Nigeria (IPMAN).

“Our members pay PPMC/NNPC in advance for petroleum products, and fully paid up PMS orders that have neither been programmed nor loaded is in excess of 500,000 metric tonnes, about 800 million litres, as at today, and enough to meet the nation’s needs for 19 days at a daily estimated consumption of 35 million litres.”

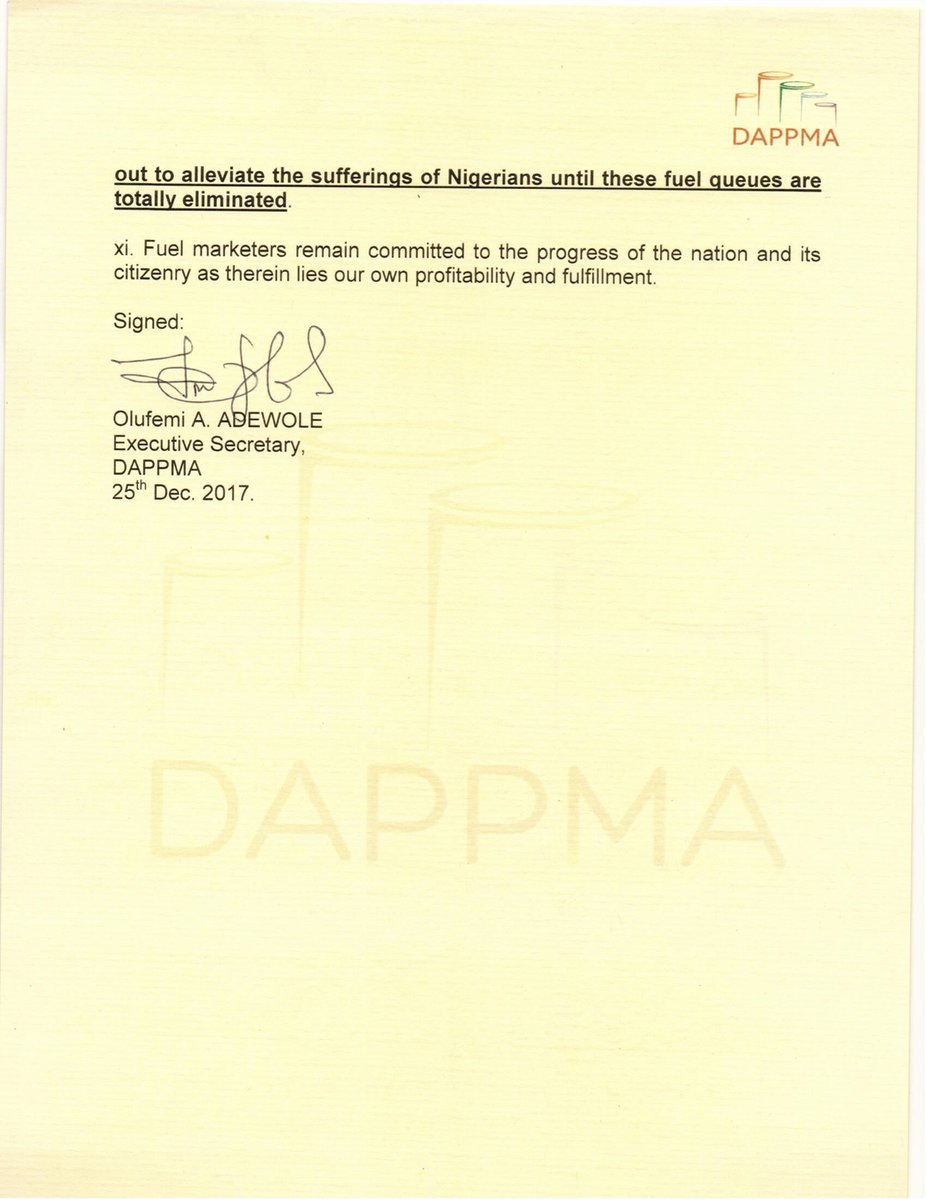

Concluding, DAPPMA said, “Our members’ depots are presently empty! However, if the PPMC/NNPC can provide us with PMS, we are ready to do 24 hours loading/truck out to alleviate the sufferings of Nigerians until these fuel queues are totally eliminated.

“Fuel marketers remain committed to the progress of the nation and its citizenry as therein lies our own profitability and fulfilment.”

By Adedapo Adesanya

Nigerian businessman and chief executive of Dangote Industries Limited, Mr Aliko Dangote, has unveiled plans for a new phase of investments and acquisitions as the conglomerate pushes towards its target of generating $100 billion in annual revenue by 2030.

Mr Dangote disclosed this while receiving a delegation of senior executives from global investment banking and financial services firm Goldman Sachs, led by co-chief executive of Goldman Sachs International and Global Co-Head of Investment Banking, Mr Anthony Gutman, during a tour of the Dangote Petroleum Refinery & Petrochemicals and Dangote Fertiliser Limited complex in Lagos.

Speaking after the visit, Mr Dangote said the refinery and associated industrial facilities underscore the transformative impact of long-term investment in Africa, stressing that the group’s ambitions extend beyond its current strategic plan.

“No matter how we try to explain what we have built, you cannot fully appreciate it until you see it. But this is only the beginning. We need to look beyond 2030.

“The next phase of our journey will include new investments and acquisitions as we continue to scale the business,” he said.

He added that detailed internal modelling had reinforced management’s confidence that the Group’s target of generating $100 billion in annual revenue by 2030 was achievable.

According to him, the projections were based on conservative assumptions and had strengthened the company’s conviction to pursue an even more ambitious long-term growth strategy.

Mr Dangote also revealed that the strong participation of employees in the refinery’s recent private placement reflected growing internal confidence in the company’s long-term strategy and future prospects.

The Goldman Sachs delegation, after an extensive tour of the 700,000 barrels-per-day refinery, described the project as an extraordinary achievement.

“It is extraordinary what Mr Dangote and the whole organisation have achieved. The ambition, the scale of the project, the quality of the project and the culture of the people is very impressive,” the executives said.

According to a statement issued by Dangote Group on Friday, the delegation was led by Mr Anthony Gutman and included Mr Adib N. Zouein, Co-Head of EMEA Emerging Markets Regional Sales and Head of the Middle East and North Africa region for Global Banking & Markets Public; Mr Ryad Yousuf, Global Head of FICC Sales Strats and Structuring; and Mr Jimi Adesanya, Head of Sub-Saharan Africa Sales (excluding South Africa).

The visitors were received by Dangote; Group Vice President, Oil & Gas, Mr Devakumar Edwin; Managing Director and Chief Executive Officer of Dangote Petroleum Refinery & Petrochemicals, Mr David Bird; Group Executive Director, Oil & Gas, Ms Fatima Aliko Dangote; Chief of Staff to the President/CEO, Ibrahim Dikko; Group Chief Branding and Communication Officer, Mr Anthony Chiejina; Group Chief Economist, Mr Hassan Mahmud; Group Chief Strategy Officer, Mr Aliyu Suleiman; and Head of Administration, Dangote Petroleum Refinery & Petrochemicals, Mr Musa Bala, among other senior executives.

By Adedapo Adesanya

The Senate Public Accounts Committee has heard that Nigeria spent N1.16 trillion on fuel subsidy in 2021, while N1.20 trillion was deducted from federation crude oil sales proceeds during the same period.

The disclosure came from the Chairman of the Revenue Mobilisation Allocation and Fiscal Commission (RMAFC), Mr Mohammed Bello Shehu, during the committee’s ongoing investigation into the 2021 to 2023 Nigeria Extractive Industries Transparency Initiative (NEITI) audit reports on the oil and gas sector.

According to the commission, crude and petroleum product losses cost N16.2 billion, pipeline repairs accounted for N22.05 billion, while strategic stock holding attracted N6.75 billion.

The revelations come against the backdrop of Nigeria’s long-running fuel subsidy regime, which successive governments maintained to keep the pump price of petrol artificially low despite mounting fiscal pressures.

Over the years, subsidy payments consumed trillions of Naira, significantly reducing revenues available to the three tiers of government and contributing to widening budget deficits.

The issue reached a turning point in May 2023 when President Bola Tinubu announced the removal of fuel subsidy during his inauguration speech, declaring that “fuel subsidy is gone.” The decision followed years of concerns over the rising cost of the programme, allegations of fraud, and repeated recommendations by fiscal authorities and international financial institutions that the subsidy had become unsustainable.

The removal triggered a sharp increase in the pump price of Premium Motor Spirit (petrol), leading to higher transportation and living costs across the country. In response, the federal government introduced a series of palliative measures, including cash transfers, support for mass transit, and wage-related interventions, while arguing that savings from the subsidy would be redirected to infrastructure, education, healthcare, and other critical sectors of the economy.

The commission also argued that the current method of calculating the 13 per cent derivation fund undermines the constitutional intention of the policy.

Meanwhile, the committee stood down the Niger Delta Development Commission’s presentation until next Wednesday to allow lawmakers review its submission.

The committee also expressed displeasure over the absence of the Auditor-General of the Federation, warning that he must appear before lawmakers next Tuesday or face compulsory appearance through the constitutional powers of the National Assembly.

By Adedapo Adesanya

Businesses in the country expect the Naira to gradually appreciate against the US Dollar between now and January 2027, according to the Central Bank of Nigeria’s (CBN) July 2026 Business Expectations Survey Report released on Thursday.

The report showed that the Business Confidence Index (BCI) remained positive throughout the review period despite perceived macroeconomic challenges. It noted that all sectors expressed optimism about the economy, with the electricity, gas and water sector posting the highest Business Confidence Index of 59.4 points and the strongest expansion prospects for August 2026.

According to the report, “In July 2026, the Business Confidence Index was 5.7 points, reflecting continued optimistic sentiment among formal businesses.”

It attributed the positive sentiment mainly to increased demand (22.3 per cent), economic diversification (21.4 per cent), and improved access to finance (15.0 per cent). However, respondents identified inflation (27.7 per cent), energy-related challenges (23.4 per cent), insecurity (22.4 per cent), and heightened geopolitical uncertainties (16.5 per cent) as the major factors weighing on business confidence.

On the outlook by broad sector, the central bank said confidence remained positive across all sectors in July. The Industry sector recorded a modest improvement, with its index rising to 11.5 points from 10.5 points, while the Services sector increased to 3.6 points from 2.9 points.

By contrast, the Agriculture sector recorded a significant moderation, with its index falling to 3.4 points from 12.2 points.

Despite this, the apex bank said the six-month outlook remained upbeat, with confidence indices across all sectors indicating positive expectations over the review period.

On the macroeconomic outlook by region, the report noted a divergence in sentiment, with businesses in Northern Nigeria expressing stronger confidence than their Southern counterparts in July. Nevertheless, respondents across all regions maintained positive expectations for August.