Banking

SCIL Appoints Adekunle Sonola as Polaris Bank MD/CEO as Ahmad Heads Board

By Aduragbemi Omiyale

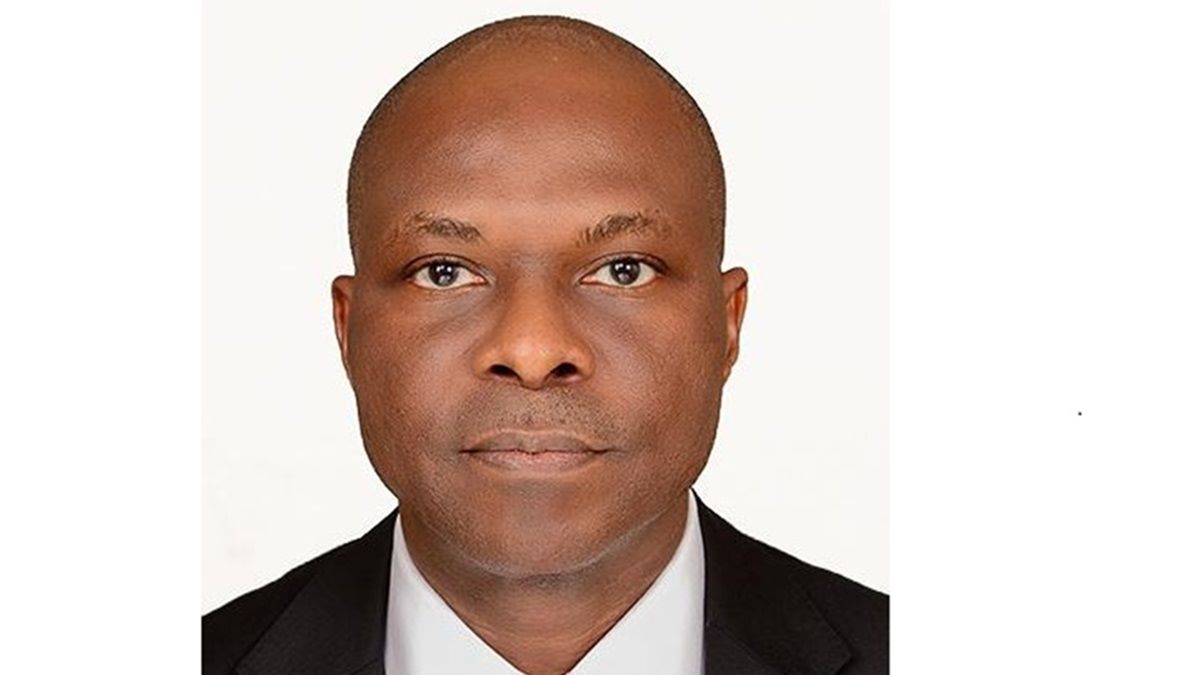

The new owners of Polaris Bank Limited, Strategic Capital Investment Limited (SCIL), have appointed Mr Adekunle Sonola as the new Managing Director/Chief Executive Officer.

This followed the acquisition of the 100 per cent equity stake in the bank for N50 billion and the agreement to pay the N1.3 trillion injected into the lender by the Central Bank of Nigeria (CBN) over the next 25 years.

Mr Sonola, who is replacing Mr Innocent C. Ike, has more than 33 years of experience in the African financial services sector, most recently as Executive Director of Commercial Banking at Union Bank Plc.

He was the pioneer Regional Managing Director of Guaranty Trust Bank East Africa and the Director of Investment Banking at Standard Bank in South Africa.

The banker has also served on the boards of Airtel Africa Plc and First Bank of Nigeria, where he chaired the board’s Risk Management Committee.

He would be expected to reposition the bank for greatness.

“We are excited to participate in the next phase of growth for Polaris Bank and to have been able to recruit such an experienced and diverse board of directors we are confident can lead Polaris Bank into a new era of sustainable growth.

“This is an exciting time for the Nigerian financial services industry, and we are committed to building on the strong foundations established by the departing board. We would like to thank them for their service and wish them well.

“We have mandated the incoming management to develop an innovative but sustainable growth strategy that prioritises the needs and aspirations of our current customers,” the MD/CEO said.

In a related development, Polaris Bank has announced the appointment of new board members to be headed by Mr M K Ahmad.

He has more than 37 years of experience and has been the Chairman of Polaris Bank since 2018, overseeing the stabilisation of the bank and the introduction of best-practice corporate governance.

He currently serves as the Chairman of the Interim Management Board of International Energy Assurance and the Technical Committee of the National Council on Privatisation.

Mr Ahmad is also a Board Director of Flour Mills of Nigeria Plc, MTN Nigeria Communications Plc and FBN Holdings. He was the pioneer Director-General of PENCOM.

The bank has also appointed Mr Abubakar Danlami Suleiman, Ms Salma Mohammed, Mr Adeleke Alex Adedipe, Mr Ahmed Almustapha, Mr Francesco Cuzzocrea, and Mrs Olabisi Olubunmi Odunowo as non-executive directors, while Mr Abdullahi S Mohammed and Mr Segun Opeke were chosen to be on the board as executive directors.

While commenting on the acquisition and board transition, the Chairman of Polaris Bank said, “I would like to thank the outgoing board members profusely for their hard work and dedication over the last four years as we have established a strong governance structure and stabilised the bank.

“I am very pleased with our progress and that we have delivered on our mandate to prepare the bank for a return to private ownership.

“I am personally proud to have been asked to lead the bank into an exciting new future, and I look forward to working with the new board and our core investors to build on the platform we have created.”

By Aduragbemi Omiyale

The dissolution of the board of Union Bank of Nigeria (CBN) by the Central Bank of Nigeria (CBN) in January 2024 has been nullified by a Federal High Court in Lagos.

In a judgment on Wednesday, Justice Chukwujekwu Aneke ordered the immediate reinstatement of the affected board members.

This ruling has now invalidated all actions taken by the central bank regarding the lender’s leadership change.

Justice Aneke held that the apex bank had no authority to remove the board members, declaring the CBN’s action as “ultra vires.”

Over two years ago, the central bank changed the boards of Union Bank, Polaris Bank, and Keystone Bank, accusing them of violating “sections of the Banks and Other Financial Institutions Act (BOFIA) 2020.”

The sacking of the Union Bank board happened after it was speculated that its acquisition by Titan Trust Bank was suspicious, with some alleging that the embattled former Governor of the CBN, Mr Godwin Emefiele, sold the lender to a proxy.

“This action became necessary due to the non-compliance of these banks and their respective boards with the provisions of Section 12(c), (f), (g), (h) of the Banks and Other Financial Institutions Act, 2020. The Bank’s infractions vary from regulatory non-compliance, corporate governance failure, disregarding the conditions under which their licenses were granted, and involvement in activities that pose a threat to financial stability, among others,” a part of the statement issued by the Acting Director for Corporate Communications at the CBN, Mrs Sidi Ali Hakama, said.

Later, the apex bank appointed Ms Yetunde Oni as the chief executive of Union Bank, with Mannir Ubali Ringim appointed as an executive director.

After the CBN’s action, Titan Trust Bank, Luxis International, and Magna International, which are the core shareholders of Union Bank, challenged the legality of the action in court.

They asked the court to restrain the CBN, Union Bank and the appointed directors from taking further steps pending the determination of the suit.

At today’s judgment, Justice Aneke granted this prayer, restraining the central bank, its agents and appointees from taking any further steps concerning the financial institution, including actions relating to its proposed recapitalisation or any associated measures.

By Modupe Gbadeyanka

A partnership to expand opportunity, entrepreneurship, and sustainable livelihoods for young people across Africa has been signed by Access Bank and King’s Trust International (KTI).

The cooperation marks a significant milestone in advancing cross‑sector collaboration to address youth unemployment, foster entrepreneurship, and drive inclusive growth across Africa.

Under the agreement, Access Bank will support the delivery of KTI’s programmes that empower young people across several African countries, supporting them to gain skills and find pathways into meaningful employment and self-employment across Africa.

It was learned that the collaboration brings together KTI’s expertise in youth development with Access Bank’s pan‑African reach and long‑standing commitment to inclusive and sustainable growth.

Through this alliance, the two organisations will work to equip young people with the skills, confidence and support needed to build successful futures through employment and entrepreneurship.

“At Access Bank, we believe that empowering young people is fundamental to Africa’s sustainable growth. Our partnership with King’s Trust International reinforces our commitment to entrepreneurship, job creation and inclusive development, while enabling us to play a purposeful role in shaping the continent’s future,” the chief executive of Access Bank, Mr Roosevelt Ogbonna, stated.

The chief executive of KTI, Mr Will Straw, while also commenting, said, “This partnership with Access Bank reflects a shared commitment to unlocking the potential of young people across Africa. By combining our experience in youth development with Access Bank’s scale and leadership across the continent, we can create meaningful pathways to opportunity and long‑term impact.”

The signing ceremony was witnessed by senior leaders and representatives from both organisations, alongside distinguished guests, including Mr Aigboje Aig‑Imoukhuede, who is the co-Chair of KTI Africa Advisory Board and Chairman of Access Holdings Plc.

By Aduragbemi Omiyale

Mr Kennedy Onuwa Okwudili has been appointed to the board of Zenith Bank Plc as an executive director with effect from May 1, 2026.

A statement signed by the company secretary, Mr Michael Otu, disclosed that the appointment aligns with the financial institution’s “tradition and succession strategy of grooming leaders from within” to strengthen its executive management further.

He is joining the board with over 25 years of cognate banking experience spanning credit and marketing, treasury, compliance, as well as operations and has at different times worked in various zones and departments of the lender.

Mr Okwudili graduated with a Bachelor of Science (Honours) in Accounting from the University of Maiduguri, Nigeria, in 1998, with a Second Class Upper Division. He obtained a Master’s of Business Administration (MBA) from Ahmadu Bello University, Zaria, Nigeria, in 2008 and a Master’s of Science in Accounting from Veritas University, Abuja, Nigeria, in 2021.

He is a Fellow of the Institute of Chartered Accountants of Nigeria (ICAN), 2013, and also a Fellow of the Chartered Institute of Bankers of Nigeria, 2024. He is an Associate of the Chartered Institute of Taxation of Nigeria (CITN), 2016.

The banker has attended several executive education programmes both within and outside the country, including Senior Leadership Development Programme at the Lagos Business School, Corporate Directorship Programme at the Harvard Business School and Oxford Advanced Management and Leadership Programme at the University of Oxford, SAID Business School.

He is currently the President of Catholic Bankers Association of Nigeria (CBAN) and a member of the Noble Order of the Knights of St. John International (KSJI).

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn