Economy

Conflict Diamonds From CAR Enter Int’l Markets via Cameroon

By Modupe Gbadeyanka

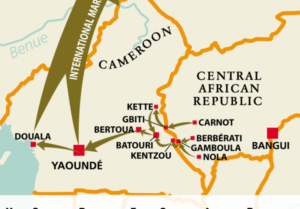

Cameroon is allowing conflict diamonds from the Central African Republic to cross over its borders and into the legal supply chain due to poor controls, smuggling and corruption, Partnership Africa Canada said in a report published today.

The report, From Conflict to Illicit: Mapping the Diamond Trade from Central African Republic to Cameroon, investigates the failure of Cameroon’s implementation of the Kimberley Process—the international diamond certification scheme meant to stop the trade of conflict diamonds. The report comes on the eve of the Kimberley Process Review Visit to Cameroon which evaluates the country’s implementation of internal controls that govern diamond production and trade.

Diamond exports from the Central Africa Republic were internationally embargoed after a coup d’état in 2013 sparked a civil war. The Kimberley Process partially lifted the embargo on zones it deemed compliant and conflict-free earlier this year. Yet, Partnership Africa Canada found the illicit trade of conflict diamonds is ongoing.

“While international outcry about ‘blood diamonds’ financing war in the Central African Republic sparked action to stop the trade, the same spotlight has not been turned on CAR’s neighbours.

“Our investigation shows the reality on the ground and how conflict diamonds from CAR still have entry points to international markets through Cameroon,” said Joanne Lebert, Partnership Africa Canada’s Executive Director.

Interviews with miners, traders and exporters detail the smuggling of Central African Republic’s diamonds across the 900km border its shares with Cameroon, corruption amongst officials charged with verifying the origins of diamonds, and large shipments of embargoed conflict diamonds passing through Cameroon’s transit hubs undeclared.

The report follows Cameroonian traders who buy diamonds from across the river—in the Central African Republic—and then on to buying houses in Cameroon’s East region. Diamonds are “self-declared” as originating in Cameroon and Kimberley Process Certificates are issued attesting to their conflict-free status, allowing for their export to international markets.

“As the Kimberley Process visits Cameroon, it must take action immediately and demonstrate to companies, retailers—and most importantly to consumers—that it is able to stop the flow of conflict diamonds,” said Offah Obale, Researcher for Partnership Africa Canada, and the report’s author.

Partnership Africa Canada calls on the Kimberley Process to place Cameroon under Special Measures which would require a tightening of internal controls within a three month period, during which time no diamond would leave Cameroon without expert and external oversight.

The report also calls on a Regional Approach to tackle the illicit trade of CAR’s conflict diamonds, bringing in other neighbours such as Democratic Republic of Congo and Angola, for a harmonized strategy.

By Dipo Olowookere

The Nigerian Exchange (NGX) Limited rallied by 0.28 per cent on Wednesday despite weak investor sentiment, as the bourse ended with 18 price gainers and 38 price losers, implying a negative market breadth index.

The growth recorded yesterday by Customs Street was influenced by the 2.11 per cent rise posted by the energy index, and the 1.79 per cent jump achieved by the banking sector.

The other sectors experienced profit-taking, with the consumer goods losing 1.07 per cent, the insurance counter down by 0.36 per cent, and the industrial goods space down by 0.19 per cent.

Universal Insurance chalked up 10.00 per cent to sell for N1.21, Omatek improved by 9.78 per cent to N2.47, VFD Group expanded by 9.71 per cent to N11.30, CWG appreciated by 9.64 per cent to N21.05, and Livestock Feeds gained 9.56 per cent to close at N7.45.

On the flip side, UPDC REIT lost 10.00 per cent to settle at N6.75, Fortis Global Insurance shed 9.92 per cent to quote at N1.18, Deap Capital depreciated by 9.85 per cent to N5.40, Chams went down by 9.47 per cent to N3.06, and Japaul declined by 8.82 per cent to N3.10.

Yesterday, the All-Share Index (ASI) went up by 562.43 points to 202,585.53 points from 202,023.10 points, and the market capitalisation advanced by N389 billion to N130.404 trillion from N130.015 trillion.

During the session, 1.0 billion stocks worth N40.6 billion exchanged hands in 52,723 deals compared with the 1.1 billion stocks valued at N40.3 billion executed in 78,006 deals a day earlier, indicating an uptick in the trading value by 0.74 per cent, and a shortfall in the trading volume and number of deals by 9.09 per cent and 32.41 per cent apiece.

The activity chart was led by Access Holdings, which sold 233.0 million units valued at N6.1 billion, Fidelity Bank exchanged 113.1 million units worth N2.2 billion, Wema Bank recorded a turnover of 103.3 million units valued at N2.7 billion, Zenith Bank transacted 60.6 million units for N6.5 billion, and Chams traded 47.5 million units worth N154.6 million.

By Adedapo Adesanya

Crude oil plummeted on Wednesday on hopes of the reopening of the Strait of Hormuz after US President Donald Trump agreed to a two-week ceasefire with Iran.

Brent crude futures moderated to $94.75 a barrel, while the US West Texas Intermediate (WTI) crude eased to $94.41 a barrel.

President Trump said on Wednesday that the US will work closely with Iran and will be talking about tariff and sanctions relief with Iran.

However, analysts cautioned that the ceasefire is a temporary two-week reprieve rather than a permanent resolution, and the global energy system remains fragile due to structural damage to regional infrastructure.

Reuters reported that Iran could open the strait in a limited and controlled way on Thursday or Friday ahead of a meeting between U.S. and Iranian officials in Pakistan.

Agence France-Presse (AFP) reported that two ships appeared to have transited the Strait of Hormuz since the US-Iran ceasefire deal. A Greek-owned bulk carrier and a Liberia-flagged vessel both transited the waterway early on Wednesday.

Meanwhile, Israel carried out its heaviest strikes on Lebanon since the conflict with Hezbollah broke out last month, even as the Iran-aligned group paused attacks on northern Israel and Israeli troops in Lebanon under the ceasefire.

Also, Saudi Arabia’s East-West Pipeline, a critical artery bypassing the Strait of Hormuz, was reportedly hit in an Iranian drone attack. Prior to the attack, the pipeline was pumping at its emergency capacity of 7 million barrels per day to bypass the shuttered strait.

The strikes occurred just hours after a US-Iran ceasefire announcement, which has so far failed to halt regional hostilities. Other facilities in the kingdom were also targeted in the wave of strikes, which the Islamic Revolutionary Guard Corps (IRGC) claimed included oil facilities owned by American companies in Yanbu.

US crude stocks rose by 3.1 million barrels to 464.7 million barrels during the week ended April 3, the Energy Information Administration (EIA) said.

By Adedapo Adesanya

The National Insurance Commission has issued new guidelines for the collection, management, and administration of the Insurance Policyholders’ Protection Fund.

In a circular issued to all insurance institutions on Tuesday, the regulator also set May 31, 2026, as the deadline for insurers to submit their assessment returns for the 2025 financial year.

Recall that on August 5, 2025, President Bola Tinubu signed into law the Nigerian Insurance Industry Reform Act ( NIIRA 2025).

This landmark legislation repeals the Insurance Act 2003, and consolidates related provisions, ushering in a modern regulatory framework. It lays a strong foundation for sustainable growth and increased investment in the country’s insurance sector.

The commission said the guidelines were issued in exercise of its powers under the 2025 Act and other existing insurance laws and regulations to provide regulatory clarity, improve guidance, and ensure ease of compliance across the industry.

According to NAICOM, the guidelines establish a comprehensive structure for the operation of the IPPF, which serves as a statutory safety net to protect insurance policyholders in the event of distress or insolvency of a licensed insurer or reinsurer. The framework also provides direction on the reimbursement of loans by insurers and reinsurers.

NAICOM stated, “The guidelines ensure regulatory clarity, guidance and ease of compliance, as it provides a comprehensive regulatory framework for the collection, management, and administration of the Fund, which serves as a statutory safety net designed to protect insurance policyholders against distress and insolvency of a licensed insurer or reinsurer, including guidance for the reimbursement of loans by an insurer or reinsurer.

“Please be informed that the IPPF Assessment Returns in respect of the year 2025 shall be submitted to the Commission not later than 31st May 2026, while subsequent submissions shall be in line with Section 4.3 of the Guideline on Insurance Policyholders Protection Fund.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn