Economy

FG Begins Ease of Doing Business Action Plan 2

By Modupe Gbadeyanka

On Tuesday, the Federal Government kicked off the implementation of its ease of doing business action plan tagged National Action Plan (NAP) 2.0.

This is part of President Muhammadu Buhari administration’s medium term Economic Growth & Recovery Plan (EGRP) to build a globally competitive economy.

The new action plan, which will run from October 3, to December 1, 2017, is expected to further reduce the challenges faced by SMEs when getting credit, paying taxes, or moving goods across the country, amongst others, by removing critical bottlenecks and bureaucratic constraints to doing business in Nigeria.

It will be recalled that the Presidential Enabling Business Environment Council (PEBEC), which is chaired by Vice President, Prof Yemi Osinbajo, had, on September 26, 2017, approved a second 60-day National Action Plan (NAP 2.0) to drive reforms aimed at making Nigeria a progressively easier place to do business.

The NAP 2.0 marks the beginning of another reform cycle 2017/2018 which aims to deepen the ease of doing business reforms implemented across the various Ministries, Departments, and Agencies (MDAs) in the last 12 months and will in turn increase productivity through industrialization, enhanced exports and foreign exchange earnings, while creating jobs and reducing poverty.

A previous 60-day National Action Plan on Ease of Doing Business was approved on February 21, 2017. The National Action Plan contained initiatives and actions implemented by responsible Ministries, Departments and Agencies (MDAs), the National Assembly, the Governments of Lagos and Kano states, as well as some private sector stakeholders.

Some of the reforms to be implemented to ease the process of starting a business include eliminating the manual registration process at Corporate Affairs Commission in 10 additional states, increase access to credit for SMEs by registering at least 300 micro-finance banks on the collateral registry, and enforce the elimination of illegal roadblocks on major trading routes across the country.

MDAs have been charged by the council to treat the Ease of Doing Business initiatives with a sense of urgency and deliver impactful results by implementing the Executive Order 001 on transparency and efficiency. The Executive Order E01, which was signed Prof. Osinbajo on 18th May, 2017, ensures that citizens have complete clarity on all government requirements and processes, better cooperation and improved information sharing among MDAs, as well as requiring proper communication of approval or rejection of applications to Nigerians within the stipulated timeframe.

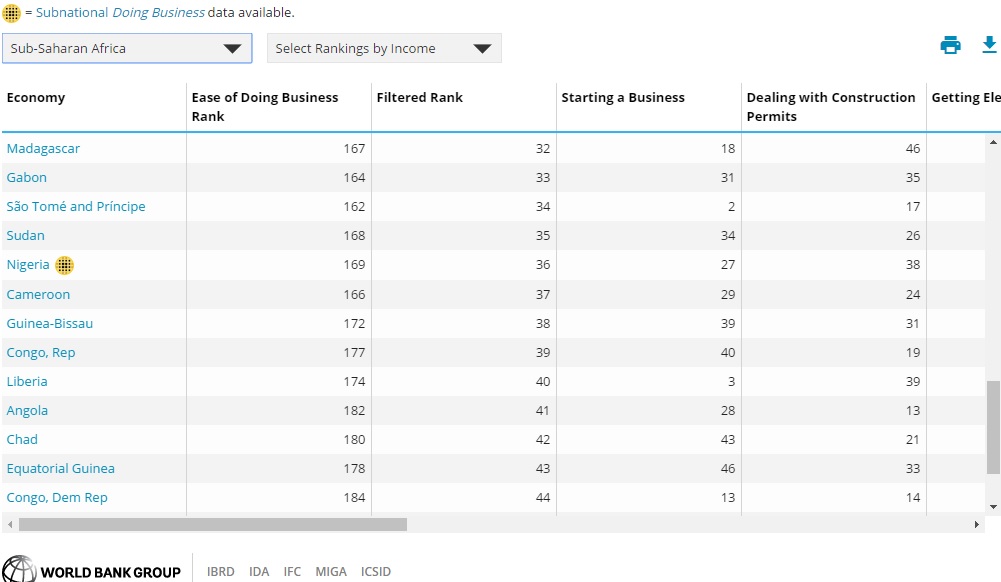

The reforms will also improve the country’s ranking in the World Bank’s Ease of Doing Business Index 2019. Recently, Nigeria rose two ranks up from its previous 127th to 125th position in the World Economic Forum’s Global Competitiveness Index (GCI) for 2017-2018. The country moved up marginally by one step from 170 to 169 in the 2017 World Bank Doing Business Report.

PEBEC, which was inaugurated in July 2016 by President Muhammadu Buhari, to remove critical bottlenecks and bureaucratic constraints to doing business in Nigeria, comprises 10 Honourable Ministers, with the Honourable Minister of Industry, Trade and Investment, Dr. Okey Enelamah, as Vice Chair, along with the Head of Service, the Central Bank Governor, representatives of the National Assembly, Lagos and Kano state governments, and the private sector.

The Ease of Doing Business reforms will be implemented over the next 60 days by the Enabling Business Environment Secretariat (EBES), which became fully operational in October 2016. It would be recalled that the EBES implemented PEBEC’s inaugural National Action Plan (NAP 60) from February to April 2017. The EBES is coordinated by Dr Jumoke Oduwole, the Senior Special Assistant to the President on Industry, Trade and Investment (OVP).

By Adedapo Adesanya

The oil market was down $100 per barrel on Wednesday after US President Donald Trump said he had agreed to a two-week ceasefire with Iran, subject to the immediate and safe reopening of the Strait of Hormuz.

Brent futures lost $14.51 or 13.3 per cent to sell for $94.76 a barrel, while the US West Texas Intermediate (WTI) futures fell by $17.16 or 15.2 per cent to $95.79 a barrel.

WTI has maintained its price premium over Brent in a reversal of typical price patterns due to its delivery contract being for May while Brent is for June, reflecting that barrels with an earlier delivery date are commanding a higher price.

President Trump’s turnaround came shortly before his deadline for Iran to open the Strait of Hormuz, where 20 per cent of the world’s oil transits, or face widespread attacks on its civilian infrastructure.

“This will be a double-sided CEASEFIRE!” he wrote on social media, after posting earlier on Tuesday that “a whole civilisation will die tonight” if his demands were not met.

President Trump indicated that negotiations may be progressing toward a more durable agreement, citing a 10-point proposal from Iran that he described as a “workable basis” for long-term peace.

Iran said it would halt its attacks if attacks against it stopped and that safe transit through the Strait of Hormuz would be possible for two weeks in coordination with Iranian armed forces.

Despite the breakthrough, tensions remain elevated across the region, with several Gulf states reporting missile launches, drone activity, or issuing civil defence warnings.

The single most important factor to watch will be how many tankers cross the Strait of Hormuz with this new agreement in place. Already, another tanker operated by Malaysia’s Petronas and carrying Iraqi crude was allowed passage in the latest sign of a modest restoration of oil flows via the chokepoint.

Earlier in the week, two tankers carrying LPG for India were also allowed to pass the strait after Iran began making individual passage deals with foreign governments. The past few days have also seen three Oman-operated vessels clear the chokepoint, as well as a French container ship and a Japanese gas carrier. China, Russia, Turkey, and Pakistan are also among the countries that Iran is allowing to send ships via the waterway.

The US-Israeli war with Iran saw the steepest monthly oil price rise in history in March of more than 50 per cent.

By Adedapo Adesanya

Vert, a global cross-border payments platform, has announced a new solution under Verto Business Accounts that enables US-registered businesses to move money seamlessly between the United States and Africa.

With the ability to open a US Dollar account in their business name and have access to trusted emerging market payment rails, companies can now receive, hold, and transfer funds faster, more cost-effectively, and with greater control.

US-registered businesses with operations in Africa often encounter significant banking limitations, with US banks frequently delaying or blocking transactions to or from African markets, imposing high or hidden FX costs, and offering limited access to Emerging Market payment corridors. Businesses without a US bank account registered in their own name must rely on fragmented tools or intermediaries to move funds to Africa, creating operational inefficiencies and slowing growth.

Verto’s new solution directly addresses these challenges by giving US-domiciled businesses access to named USD accounts and a robust cross-border payment infrastructure, enabling them to move funds and settle transactions in local currencies with speed and efficiency.

Built for venture-backed startups, import-export SMEs, and investors funding emerging market innovation, this solution will enable clients to receive funds directly into a named USD business account from US based customers or investors, convert and settle between USD and local currencies such as NGN and KES quickly and at lower cost, as well as hold, receive, and pay in 48 currencies from a single dashboard.

The solution will also allow users to pay contractors, suppliers, and offshore teams instantly via local payment rails. It also equips teams with virtual cards to spend in 11 currencies without fees and leverage specialised onboarding and monitoring that navigates both US and African regulatory requirements

By combining US and African compliance expertise, Verto’s Business Accounts empowers companies to maintain a US domestic presence for investors, customers, and suppliers while using deep-liquidity rails to pay global contractors and settle trades in local currencies efficiently, ensuring uninterrupted trade, payroll, and investment flows, without the risk of blocked or delayed transactions.

“We believe founders building across borders should not be constrained by the limitations of traditional banking,” said Ola Oyetayo, CEO of Verto. “Providing named accounts in the US empowers businesses with the funds they need to operate globally, connecting the US and Africa more efficiently without friction.”

With over 8 years of experience and $25 billion in annual global cross-border transaction volume, Verto continues to provide the infrastructure, expertise, and trusted payment rails businesses need to operate confidently across borders and scale globally.

By Adedapo Adesanya

The Presidential Enabling Business Environment Council (PEBEC) has directed Ministries, Departments, and Agencies (MDAs) to suspend the introduction of new policies and regulatory changes to prevent disruptions to businesses.

The directive was issued in a statement by PEBEC director-general, Mrs Zahrah Mustapha-Audu, on Monday in Abuja, noting that the move is part of the Federal Government’s broader effort to improve regulatory quality, ensure policy consistency, and strengthen Nigeria’s ease of doing business environment.

The council emphasised that the suspension will remain in place until all MDAs fully comply with the Regulatory Impact Analysis (RIA) Framework, which governs evidence-based policymaking across government institutions.

The council said the directive is aimed at ensuring that all government policies are backed by verifiable data and do not negatively impact businesses or investors.

“It is imperative to emphasise that no new reform or policy will be permitted to proceed without being grounded in clear, verifiable evidence,” said Mrs Mustapha-Audu.

“The framework provides the structured mechanism through which such evidence-based decisions can be rigorously developed, assessed, and validated.

“This directive is necessary to prevent policy shocks that may adversely affect businesses, investors, and citizens, as well as to eliminate policy inconsistencies and frequent reversals.”

She added that the government remains committed to working collaboratively with regulators and does not intend to embarrass any institution.

The Regulatory Impact Analysis (RIA) Framework, introduced in January 2025, is designed to improve transparency and ensure that policies undergo proper evaluation before implementation.

All MDAs are required to align new policies and amendments with the RIA framework before approval and rollout.

The framework has been circulated by the Office of the Secretary to the Government of the Federation (SGF) and is available on the PEBEC website.

MDAs are encouraged to seek technical support from the PEBEC Secretariat to ensure proper implementation.

Exceptions to the directive will only be granted in cases of urgent national interest, subject to appropriate approvals.

PEBEC noted that the framework will help institutionalise evidence-based policymaking, enhance transparency, and improve stakeholder confidence in government decisions.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn