Media OutReach

DFI Retail Group Holdings Limited 2024 Preliminary Announcement of Results

The following announcement was issued today to a Regulatory Information Service approved by the Financial Conduct Authority in the United Kingdom.

Highlights

- 30% growth in underlying profit to US$201 million

- Health and Beauty delivered a stable performance

- Convenience saw strong profit growth due to favourable product mix

- Food profit improved, driven by significant Singapore Food earnings recovery

- Portfolio simplification progressed further with Yonghui and Hero Supermarket divestments

- Net cash position achieved in February 2025 with completion of Yonghui sale

- Final dividend of US¢7.00 per share

“Effective strategy execution led to strong underlying profit growth in 2024, despite a challenging retail environment. We aim to remain relevant to consumers and to increase market share further, by evolving our offering through leveraging data and expanding our omnichannel presence. We are well-positioned for sustainable growth and increased shareholder returns over the mid-term.”

John Witt

Chairman

PRELIMINARY ANNOUNCEMENT OF RESULTS

FOR THE YEAR ENDED 31 DECEMBER 2024

PERFORMANCE

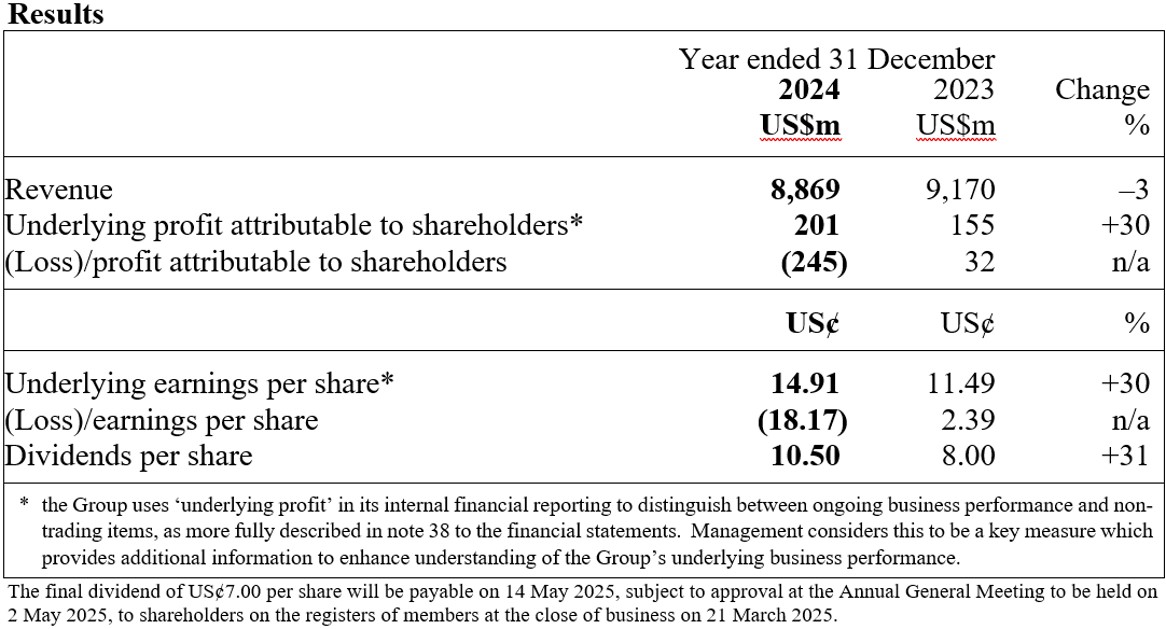

I am pleased to report that DFI Retail Group (‘DFI’ or the Group) delivered a significantly improved underlying performance and a good partial recovery in results in 2024, despite a challenging retail environment. For the full year, underlying profit attributable to shareholders reached US$201 million, a 30% increase from the previous year.

Our diverse portfolio and effective operational execution enabled us to gain market share across key businesses, even as we faced shifts in consumer behaviour and macroeconomic headwinds. Profit growth was driven by improved profit in Food and Convenience, supported by growth in digital channels.

We are confident that the Group’s new strategy will drive further profit growth in the coming years, and are particularly optimistic about the growth prospects for our Health and Beauty business, which represents 55% of the Group’s total operating profit. We also see strong growth opportunities in our Convenience business. Our other businesses continue to face challenges, but we are confident in the ability of DFI’s senior leadership team to navigate short-term uncertainties, evolve the portfolio and invest in strengthening our core businesses to drive long-term growth in shareholder value.

The Board recommends a final dividend for 2024 of US¢7.00 per share (2023 final dividend: US¢5.00).

STRATEGIC HIGHLIGHTS

Under the capable leadership of our Group Chief Executive, Scott Price, we have made significant strides in implementing our strategic framework, which centres around three core pillars:

Customer First

Across our business, we have an ongoing commitment to putting our customers first, and we have made significant progress to better serve them over the past year. The yuu Rewards loyalty programme continues to strengthen, with a substantial increase in members and the addition of a number of further partners. We have also begun harnessing our proprietary customer data to refine our product assortment and revamp our Own Brand and digital strategies. We are driving a more transparent and collaborative approach to our negotiations with suppliers, leading to a better outcome for customers. As well as better serving our customers, these efforts aim to bolster market share growth and enhance margins across our businesses.

People Led

We have refined our organisation structure over the past year. Our new senior leadership team, with its deep industry expertise, shares a vision for strategic growth and operational excellence. Key appointments across the business have strengthened our capability to drive these initiatives forward, and we have reduced spans and layers within the organisation to streamline operations and expedite decision-making. Diversity across our business has also improved significantly.

Shareholder Driven

In alignment with our strategic and capital allocation priorities, we continued to simplify the Group’s portfolio and divested our Hero Supermarket business and investment in Yonghui Superstores.

Following the disposal of Hero Supermarket, the Guardian and IKEA businesses will be our focus in Indonesia and we are confident in the long-term prospects for these two businesses to increase market share as the Indonesian market grows. These disposals allow us to reinvest in our subsidiaries’ growth, deleverage our balance sheet and grow total shareholder returns.

Sustainability remains at the top of our agenda, and we are collaborating closely with our stakeholders and setting ambitious targets across the business. There was strong progress in 2024 against the Group’s sustainability strategy in areas including emissions reduction and waste diversion. Our efforts were recognised in improvements in our ESG ratings, including a significant improvement in the Group’s S&P Global Corporate Sustainability Assessment. We will continue to promote and drive sustainable business practices in our end-to-end value chain.

GOVERNANCE AND PEOPLE

The Board and its Committees, and senior leadership team, together play a key role in delivering against our priorities. The effective execution of our strategy depends on high quality debate around the boardroom table, with strong contributions from all Directors.

There have been a number of significant Board and executive leadership changes since the start of 2024:

– In July, I succeeded Ben Keswick as Chairman. On behalf of the Board, I would like to express our gratitude to Ben for his 11 years of service as Chairman.

– I also wish to thank Adam Keswick for his contribution to the Board and Nominations Committee as he steps down.

– We welcomed Elaine Chang to the Board as an Independent Non-Executive Director and Graham Baker as a Non-Executive Director. Elaine has 30 years of leadership experience across industries such as semiconductors, digital content, e-commerce, cloud computing and artificial intelligence, and her expertise in leveraging technology to drive growth will greatly benefit the Group.

– Christian Nothhaft was appointed as a member of the Remuneration and Nominations Committees.

– Tom van der Lee took over as Group Chief Financial Officer from Clem Constantine. We thank Clem for his significant contribution, especially during the pandemic and in strengthening the Group’s financial position. Tom, who joined DFI in 2016, brings a wealth of experience from his various senior financial roles within the organisation.

– Sean Ward succeeded Jonathan Lloyd as our Company Secretary in December 2024. I want to thank Jonathan for his years of valued service.

PROSPECTS

We are pleased by the Group’s strong underlying profit growth in 2024, despite a challenging retail backdrop, providing encouraging early support for our new strategy. We aim to consolidate our position in markets such as Hong Kong where we have strong businesses, while at the same time aiming to achieve long-term growth as we expand key businesses such as Health and Beauty and Convenience.

By evolving our offerings through data-driven insights and expanding our omnichannel presence, we will remain relevant to consumers and continue capturing market share. Our deleveraged balance sheet and strategic initiatives position us well for sustainable growth and increased shareholder returns in the years to come.

I should like to express my appreciation to our shareholders, our valued partners and to the wider community for your continued support. Most of all, thanks must go to our team members, who are key to our success, for their exceptional work and unwavering commitment throughout the past year, despite challenging market conditions.

John Witt

Chairman

GROUP CHIEF EXECUTIVE’S REVIEW

INTRODUCTION

As I reflect on my first full year as DFI’s Group Chief Executive, I am incredibly proud of the significant progress we have made executing in alignment to our strategic framework: Customer First, People Led, Shareholder Driven.

Despite the challenging macroeconomic backdrop, we demonstrated resilience in our business performance, reporting underlying profit attributable to shareholders of US$201 million in 2024, up 30% year-on-year. During the year, we announced the divestment of our minority stake in Yonghui, a transaction that aligns with our strategic and capital allocation framework and enables us to reinvest in the future growth of our subsidiary businesses. While our reported results were impacted by one-off items, including fair value loss, impairment of equity interest and goodwill, we have continued to significantly deleverage our balance sheet with a net cash position following the completion of the Yonghui transaction in February 2025.

As we head into the new financial year, we remain laser focused on executing our strategic priorities to drive revenue growth and enhance profitability. Our 2025 financial guidance of US$230 million to US$270 million underlying profit attributable to shareholders, reflects our confidence in further building on our momentum and delivering greater value for our stakeholders.

STRATEGIC FRAMEWORK – KEY PROGRESS

We developed our strategic framework of Customer First, People Led, Shareholder Driven in the second half of 2023 to guide the Group’s capital allocation priorities and growth plans over the coming years. I am both pleased and proud of the progress made by the team over the past 12 months in executing on this framework.

Customer First

I continue to see value unlock across our uniquely diverse businesses across Asia. We are proud to serve millions of customers in various formats and banners with nearly 11,000 outlets across 13 markets in Asia. What stands out is our ongoing commitment to putting our customers first and serving with passion and care. Our purpose has always been part of who we are. During the year, we launched our DFI purpose to articulate it in a way that unites our organisation, which is to Sustainably Serve Asia for Generations with Everyday Moments. This statement underscores our commitment to meeting the everyday needs of our customers across Asia, while emphasising their interests in sustainable solutions.

Aligned with our purpose, we have made significant progress in a number of areas to better serve our customers over the past year.

yuu Rewards

Our yuu Rewards coalition loyalty programme continues to strengthen. In our home market of Hong Kong, total members have reached 5.3 million with over 3 million monthly active members. The active use of purchases across all our formats, restaurants and partners creates substantial volume of unique data insights. In 2024, the yuu Rewards programme in Hong Kong added a number of additional partners including Starbucks and FWD Insurance. Our members have engaged across a variety of redemption offers that incorporate new travel, entertainment and dining options, driving enhanced customer engagement.

In Singapore, the yuu Rewards programme has grown to over 1.8 million members. A number of new partners joined the programme during the year including Suntec City and Singapore Airlines.

Improving assortment

We are now leveraging our broad yuu Rewards customer data to improve assortment in our stores. At Wellcome, we have leveraged our proprietary data and cutting-edge data analytics capabilities to execute a reset of 14 categories in stores. The improved assortment has seen very encouraging initial results with uplifts in both sales and gross profits. We are now also leveraging the learnings from Wellcome to support assortment optimisation for our Health and Beauty and Convenience businesses across Hong Kong and Singapore.

Improving supplier collaboration

We are beginning to better leverage our data to support enhanced supplier collaboration. By creating a more transparent and collaborative approach to negotiations with suppliers, we are working together to drive market growth and a better outcome for customers.

Own Brand

We have reset our Own Brand strategy to better align with customer needs while delivering stronger margins for our business. By optimising our product range, redesigning packaging for greater customer appeal and maximising cross-selling opportunities across our formats, we have made meaningful improvements in margin and sales productivity, which includes a more than 300bps increase in our Food Own Brand margin and close to a 40% increase in sales productivity compared to 2023. Following the success of our reset of the Own Brand portfolio across our Food business, we have integrated the Health and Beauty Own Brand assortment into this center of excellence to replicate the same success in Health and Beauty as we reset its private label strategy.

Digital

Following our digital strategy reset in September 2023, customers are now able to access our retail portfolio through a wider range of digital assets including apps, websites and third-party platforms. Our expanded omnichannel presence includes Wellcome’s quick-commerce partnership with foodpanda, a new 7-Eleven app with approximately 137,000 monthly active users and 30,000 daily active users in Hong Kong as of December 2024. Including a new Mannings Hong Kong app and Guardian Singapore app, we have launched more than 20 new channels in 2024 across apps, websites and third-party platforms. Our strengthened digital proposition was underpinned by a 31% growth in e-commerce order volume with strong profitability turnaround.

Retail Media

DFI launched our own Retail Media network in the first quarter of 2024. Initial performance has been encouraging, with more than 100 targeted marketing campaigns sold in less than a year since the launch, supported by strong sales acceleration in the second half. We have partnered with leading suppliers such as Procter & Gamble, Unilever, Coca-Cola, Nestlé and Reckitt. Importantly, the integrated online and offline advertising proposition for Retail Media has supported the improved Return on Ad Spend for our supplier partners. We are in the early days of a potentially significant source of profit to invest in the business.

People Led

In alignment with our strategic framework, we refined our organisation structure in the second half of 2023 by moving accountability to a format structure, thereby improving agility while reducing overhead costs. Throughout 2024, we have been focused on deeply embedding our values, underpinned by our purpose statement across the Group. We have reduced spans and layers within the organisation to streamline operations and expedite decision making. Diversity representation across formats has been significantly improved to ensure local relevancy of decision-making to customers. We have strengthened our leadership succession planning and development with a meaningfully improved team member engagement score, supported by a new incentive structure for senior management that aligns with shareholder interests, based on total shareholder return and business performance targets.

Shareholder Driven

Our strategic framework has been developed with the primary aim of improving shareholder returns. We have approached capital allocation in a disciplined manner, both from a capex and working capital management perspective. Over the course of the year, we executed the divestment of a number of company-owned properties, which has supported a US$150 million reduction in net debt at the end of 2024.

Concurrently, the Group continues to execute M&A transactions in a manner that is accretive to return on capital and total shareholder return based on a strategic review of our businesses in 2024. In June 2024, the Group completed the divestment of the Hero Supermarket business in Indonesia. Post-completion, DFI’s operations in Indonesia has fully pivoted to the Guardian and IKEA businesses. In September 2024, the Group announced the divestment of its entire stake in Yonghui Superstores Co., Ltd. This transaction was subsequently completed in February 2025. The Group is in a net cash position following the completion of the Yonghui transaction.

2024 PERFORMANCE

The Group reported total revenue from subsidiaries in 2024 of US$8.9 billion, down 3% year-on-year. However, excluding the impact of a significant tobacco tax increase in Hong Kong, the divestment of our Malaysia Food business in 2023 and Hero Supermarket operation in Indonesia, operating revenue was largely stable. This broadly represents market share gains in all formats except IKEA.

Total revenue for the Group, including 100% of associates and joint ventures, was US$24.9 billion, down 6% compared to 2023, largely due to lower sales at Yonghui. Total underlying profit attributable to shareholders was US$201 million for the year, up 30% year-on-year.

The Group reported subsidiaries underlying profit attributable to shareholders of US$158 million for the full year, 42% higher than the prior year. This was driven by significant earnings recovery in Singapore Food and favourable product mix shift towards non-cigarette categories in our Convenience business, partially offset by lower contribution from Home Furnishings as a result of weak property market activity and intensifying competition.

The Group’s share of underlying profit from associates was US$43 million, down 2% year-on-year. Lower contribution from Maxim’s due to weaker mooncake sales and restaurant performance in the Chinese mainland was partially offset by reduced losses from Yonghui and a 15% profit growth at Robinsons Retail.

The Group’s reported results for the year were impacted by non-trading losses attributable to shareholders of US$445 million. This was predominantly due to loss of US$114 million associated with the divestment of Yonghui, a US$231 million impairment of interest in Robinsons Retail and US$133 million goodwill impairment of Macau and Cambodia Food businesses. These losses were partially offset by gains from divestment of Singapore property assets and the Group’s share of one-off gains from the Bank of the Philippine Islands (BPI)-Robinsons Bank merger. Despite the large non-trading losses reported, the Group is now in a net cash position following the completion of Yonghui transaction in February 2025.

The Group reported operating cash flow after lease payments of US$331 million, 21% lower than the prior year, mainly due to unfavourable movement in working capital year-end timing difference, partially offset by underlying operating profit growth. Operating cash flow after lease payments and normal capital expenditure was US$158 million, down 29% year-on-year.

ENVIRONMENTAL, SOCIAL, GOVERNANCE (ESG)

As a leading Asian retailer, we recognise our unique opportunity to promote and drive sustainable business practices in response to the preference of our customers. By positioning our ESG commitment as a core pillar of our Group Strategy, we have made meaningful progress in various initiatives, including emissions reduction and waste diversion. Our efforts are reflected in a significant improvement in the S&P Global Corporate Sustainability Assessment, with our score improving to 49 as at 8 January 2025, placing DFI in the 84th percentile within the Food and Staples Retailing industry, up from the 47th percentile in 2023.

Our strong commitment to ESG is underscored by our target to halve Scope 1 & 2 greenhouse gas (GHG) emissions by 2030 and achieve net-zero by 2050. Throughout 2024, we have made significant investments in upgrading and converting our existing refrigeration systems to more environmentally friendly options. We successfully completed trials of natural gas and ultra-low global warming potential gases as refrigerant alternatives for our food stores. Following a comprehensive analysis of our Scope 3 emissions, we have identified key product categories and realistic decarbonisation opportunities within our supply chain. For example, our Low Carbon Rice Project, launching in Thailand this year, aims to drive decarbonisation by promoting low-carbon farming practices among local farmers, implementing field monitoring and tracking to measure carbon emission reductions. We have made notable progress in improving our waste diversion and are constantly exploring innovative ways to foster a transition towards a local circular economy. Wellcome has partnered with a Hong Kong-based recycling facility to convert trimmed fats into biodiesel for powering essential generators.

While we are still early in the journey, these initiatives collectively demonstrate our efforts and commitment to serving communities sustainable and affordable products, sustaining the planet and sourcing responsibly while meeting the return objectives of our shareholders.

BUSINESS REVIEW

HEALTH AND BEAUTY

Sales for the Health and Beauty division came in slightly higher than the prior year at US$2.5 billion, with like-for-like (LFL) sales remaining broadly stable. Underlying operating profit was US$211 million for the year, slightly below 2023.

Hong Kong reported strong LFL sales performance in the first quarter, which then decelerated in the second and third quarters due to a strong comparable period in 2023 when consumption vouchers were disbursed in April and July 2023. Sales momentum improved in the fourth quarter with Mannings continuing to gain market share. Profit for the year increased 6%, attributable to gross margin improvement and disciplined cost control, despite a 2% decline in full-year LFL sales. Guided by a customer-first proposition, the Pharmacare programme reached a significant milestone since its launch in 2023. In partnership with Bupa, one of Hong Kong’s major medical insurers, the Mannings team further expanded Pharmacare into its network of more than 150,000 members. Leveraging Mannings’ position as the largest pharmacist network, the programme offers free consultations and medication for a range of common illness. The Mannings team continued to enhance in-store experience with the launch of the Health Pod at our International Finance Centre flagship store in Hong Kong. This innovative service offers an AI wellness assessment that measures over 20 metrics, followed by personalised consultations and product recommendations. Initial results have been promising, with customers using the service showing a basket size three times higher than average. In addition, the team also launched a new Mannings app in December to grow its digital footprint. LFL sales of Mannings China declined as the business pivots away from offline stores to online channels which involves the closure of the majority of its offline network.

Guardian in South East Asia reported US$857 million in sales, reflecting a 5% year-on-year increase, driven by growth in basket size across all key markets. Indonesia, in particular, saw a 17% LFL sales growth supported by increased mall traffic and strong execution of promotional campaigns. Strong profit growth was reported across most key markets, underpinned by gross margin expansion and operating leverage. In Singapore, strong commercial execution and a favourable product mix contributed to gross margin expansion, with healthcare products accounting for more than 60% of sales.

CONVENIENCE

Total Convenience sales were US$2.4 billion, representing a decline of 3% year-on-year. LFL sales were 5% behind the prior year, impacted by a decline in lower-margin cigarette volumes following tax increases in Hong Kong at the end of February 2024. Excluding cigarette sales, overall Convenience LFL sales were up 2%, with continued market share gain across markets. Convenience underlying operating profit was US$102 million for the year, an increase of 17% compared to 2023. Hong Kong operating profit has grown 10% year-on-year, driven by a favourable mix shift towards higher-margin categories, with ready-to-eat (RTE) accounting for 16% of total sales for the full year. The newly launched 7-Eleven app offers discounted RTE bundles, pre-order functions, and digital stamps for IP collectibles to drive purchase frequency and customer loyalty.

7-Eleven South China and Singapore reported largely stable LFL sales supported by robust growth in RTE, which accounted for 40% and 23% of sales, respectively. Favourable margin impact from product mix shift and ongoing cost control contributed to meaningful profit growth in both markets. 7-Eleven continued to grow its store network in the South China region with 103 net openings during the year. The Group aims to drive further network expansion primarily through a capex-light franchise model.

FOOD

Reported sales for the Food division in 2024 were US$3.1 billion, down 5% year-on-year. Excluding the impact of the divestment of the Malaysia Food business in 2023 and Hero Supermarket operation in Indonesia, revenue for the division was 2% lower than the prior year. Underlying operating profit for the division was US$58 million for the year, up from US$45 million in 2023.

While increased outbound travel of Hong Kong residents to the Chinese mainland has affected food consumption for the majority of 2024, the situation has begun to normalise with total retail sales of supermarkets in Hong Kong returning to growth in the fourth quarter of 2024. Wellcome saw improving sales momentum in the fourth quarter with full-year LFL sales marginally below those of the prior year despite challenging trading conditions. Strong in-store execution and effective promotional campaigns have supported consistent market share gain over the course of the year. The Wellcome team has strengthened its omnichannel presence through the wellcome.com.hk website, its app and a quick-commerce partnership with foodpanda, contributing to a more than 20% sales growth in overall Food e-commerce with significantly improved profitability.

South East Asia Food sales performance was adversely affected by intense competition and soft consumer sentiment due to cost-of-living pressures. Improved sales mix, effective cost control and optimisation of the store portfolio led to a meaningful earnings recovery, with Singapore Food turning profitable in the fourth quarter of 2024. The Group continues to serve the Singapore market with different propositions through its various brands.

In June 2024, the Group completed the divestment of its Hero Supermarket business in Indonesia. Post-completion, DFI’s operations in Indonesia have fully pivoted to the Guardian and IKEA businesses.

HOME FURNISHINGS

IKEA reported sales of US$701 million, representing a 12% drop compared to the prior year. Overall, LFL sales reduced by 11% in 2024. Operating profit was US$16 million, down 13% year-on-year.

IKEA’s business performance has been hampered by reduced customer traffic due to weak property market activity across regions. While IKEA Taiwan demonstrated relative resilience, sales in Hong Kong and Indonesia were affected by intensified competition and basket mix change as customers reduced purchases of big-ticket items.

In response to the challenging sales environment, the IKEA team continues to implement strong cost control measures across our markets. The IKEA Hong Kong business is pivoting towards a more value-driven omnichannel proposition to compete with Chinese mainland digital platforms. E-commerce penetration has now surpassed 10% across all markets. The IKEA Indonesia team remains focused on driving sales through enhancing store commerciality, increasing local sourcing, and adopting a more effective marketing strategy to improve local relevancy. Implementation of cost-saving measures contributed to narrowing losses compared to the prior year.

RESTAURANTS

The Group’s share of Maxim’s underlying profits was US$66 million in 2024, down from US$79 million in the prior year, largely due to lower mooncake sales and weaker restaurant performance on the Chinese mainland. Maxim’s continued to expand its presence in South East Asia, adding 76 net new stores during the year, mainly in Thailand and Vietnam. Benefiting from a diversified portfolio, restaurant sales performance in Hong Kong remained resilient despite an increase in outbound travel on weekends and public holidays.

OTHER ASSOCIATES

The Group’s share of Yonghui’s underlying losses was US$33 million for the year, compared to a US$36 million share of underlying losses in the prior year. Continued macro headwinds and intense competition led to lower LFL sales. The reduction in losses was underpinned by ongoing cost optimisation, partially offset by a decline in gross margin. The divestment of the Group’s minority stake in Yonghui was completed in February 2025.

Robinsons Retail’s underlying profit contribution was US$17 million, up 15% year-on-year. Robinsons Retail reported low single-digit growth in LFL and robust growth in operating profit driven by the Food and Drugstore segments. Reported profit contribution grew close to 90% year-on-year, supported by one-off gains following the BPI-Robinsons Bank merger in early 2024.

OUTLOOK

We have navigated 2024 with resilient business performance and continued market share gains for our key business units by proactively adapting to changing market conditions through a stronger value proposition, expanded omnichannel presence and disciplined cost control. While challenges remain, we are cautiously optimistic about the outlook for 2025. The Group expects underlying profit attributable to shareholders to be between US$230 million and US$270 million in 2025, supported by an organic revenue growth of approximately 2%.

The Group will continue to execute against its strategic framework. By enhancing the local relevancy of our product offerings, deepening monetisation of our digital assets, and executing value-enhancing M&A transactions, we have put in place solid foundations in 2024, and we remain confident in driving sustained, profitable growth and shareholder returns in the years ahead.

Scott Price

Group Chief Executive

Hashtag: #DFIRetailGroup #Mannings #Guardian #7-Eleven #Wellcome #MarketPlace #ColdStorage #Giant #IKEA #yuuRewards #Maxim’s #RobinsonsRetail

![]() https://www.dfiretailgroup.com/

https://www.dfiretailgroup.com/

The issuer is solely responsible for the content of this announcement.

DFI Retail Group

DFI Retail Group is a leading Asian retailer. At 31 December 2024, the Group, its associates and joint ventures operated over 10,700 outlets, of which more than 5,000 stores were operated by subsidiaries. The Group, together with associates and joint ventures, employed over 190,000 people, with over 45,000 people employed by its subsidiaries. The Group had total annual revenue in 2024 of US$24.9 billion and reported revenue of US$8.9 billion.

DFI Retail Group is dedicated to delivering quality, value and exceptional service to Asian consumers through a compelling retail experience, supported by an extensive store network and highly efficient supply chains.

The Group (including associates and joint ventures) operates a portfolio of well-known brands across six key divisions. The principal brands are:

Health and Beauty

- Mannings on the Chinese mainland, Hong Kong and Macau S.A.R.; Guardian in Brunei, Indonesia, Malaysia, Singapore and Vietnam.

Convenience

- 7-Eleven in Hong Kong and Macau S.A.R., Singapore and Southern China.

Food

- Wellcome and Market Place in Hong Kong S.A.R.; Cold Storage and Giant in Singapore; Lucky in Cambodia; and Robinsons in the Philippines.

Home Furnishings

- IKEA in Hong Kong and Macau S.A.R., Indonesia and Taiwan.

Restaurants

- Hong Kong Maxim’s group on the Chinese mainland, Hong Kong and Macau S.A.R., Cambodia, Laos, Malaysia, Singapore, Thailand and Vietnam.

Other Retailing

- Robinsons in the Philippines operating department stores, specialty and DIY stores.

At the heart of its business, DFI Retail Group is driven by its purpose to ‘Sustainably Serve Asia for Generations with Everyday Moments’.

The Group’s parent company, DFI Retail Group Holdings Limited, is incorporated in Bermuda and has a primary listing in the equity shares (transition) category of the London Stock Exchange, with secondary listings in Bermuda and Singapore. The Group’s businesses are managed from Hong Kong. DFI Retail Group is a member of the Jardine Matheson Group.

Investors

Christine Chung

Mengniu’s Chinese Culture Pavilion Debuts at the FIFA World Cup, Showcasing Chinese Culture to the World

On the pitch, a single football captures the attention of billions. Beyond the stadium, civilizations come together through cultural exchange.

The Mengniu Chinese Culture Pavilion marks the first comprehensive international presentation of Beijing Central Axis since its inscription as a UNESCO World Heritage Site and debuts at one of the world’s premier sporting events. Inspired by the architectural aesthetics of traditional Chinese architecture and the spatial order of Beijing Central Axis, the pavilion follows a symmetrical layout centered on a principal axis. At its entrance stands the monumental painting Magnificent Central Axis, offering a panoramic bird’s-eye view of Beijing’s historic Central Axis while conveying, through artistic expression, the Eastern philosophy and cultural values it embodies. As visitors explore the pavilion, football fans from around the world pause to experience its interactive exhibits, immersing themselves in the richness of Chinese traditional culture. Standing outside New York New Jersey Stadium, the pavilion continues to tell vivid, contemporary stories of China to a global audience.

Beyond Football: Mengniu Elevates Cultural Exchange on the World Cup Stage

For Mengniu, building a Chinese Culture Pavilion at this FIFA World Cup reflects a deeper understanding of the powerful connection between sport and cultural exchange. Mengniu believes that the FIFA World Cup is not only the pinnacle of football competition but also a global platform where diverse civilizations meet, connect, and learn from one another. As an Official Sponsor of the 2026 FIFA World Cup from China, Mengniu sees it as both an opportunity and a responsibility to share China’s stories and showcase the richness of Chinese civilization with audiences worldwide. This commitment extends beyond football. During the Paris Summer Olympic Games and the Milan Winter Olympic Games, Mengniu, as a Worldwide Olympic Partner (TOP), continuously hosted its signature “China Night” events, integrating Chinese culture into the narrative of the world’s most prestigious sporting competitions.

Beyond a Pavilion: Mengniu’s Multi-Dimensional Presence at the FIFA World Cup

As an Official Sponsor of the 2026 FIFA World Cup, Mengniu’s presence extends far beyond traditional brand visibility. Its participation represents a comprehensive global strategy that integrates products, brand values, and corporate social responsibility.

On the product front, Mengniu Ice Cream has officially become the Official Ice Cream of the 2026 FIFA World Cup. Mengniu Ice Cream is available at all tournament venues and has simultaneously expanded into 11 major U.S. cities, including Los Angeles and New York. By bringing world-class-quality products to international consumers, Mengniu continues to strengthen the commercial foundation for its global growth.

At the brand level, together with global brand ambassadors Lionel Messi, Kylian Mbappé, and Lamine Yamal, Mengniu brings its corporate spirit, “Born for Greatness,” to life on football’s biggest stage. The company has also partnered with Hisense to launch a series of coordinated Chinese-character pitch-side advertising campaigns during the tournament. Moving beyond individual brand promotion, the two companies present a united expression of Chinese brands, confidently demonstrating the growing global influence of Chinese enterprises.

In terms of corporate social responsibility, Mengniu not only brings Chinese culture to the international stage but also demonstrates the commitment of a responsible Chinese enterprise through meaningful public initiatives. At the opening match of this year’s FIFA World Cup, six teenage footballers from Inner Mongolia were selected by Mengniu to escort the FIFA flag onto the field, creating an inspiring example of how businesses can promote youth football development while fulfilling their social responsibilities.

From a glass of milk on store shelves to a cultural journey within the pavilion, Mengniu’s World Cup presence reflects the remarkable evolution of Chinese enterprises on the global stage. Looking ahead, Mengniu will continue to leverage the world’s premier sporting events to advance health, boost brand power, strengthen global presence, and fulfill social responsibilities, contributing the strength of China’s dairy industry to sharing China’s stories and showcasing the enduring appeal of Chinese civilization with the world.

Hashtag: #Mengniu

The issuer is solely responsible for the content of this announcement.

Media OutReach

House of Origin Elevates the Cantonese Culinary Canon with Pristine Expressions for Summer

Michelin-starred culinary director Chef Xu Jingye alongside Resident Chef Tim Lam accentuate the essence of Cantonese cuisine while presenting his signature philosophy of “Refined Homeliness”

MACAU SAR – Media OutReach Newswire – 24 July 2026 – House of Origin, the exclusive private Cantonese dining destination at Galaxy Macau, the world-class luxury integrated resort renowned for its award-winning hospitality and signature “World Class, Asian Heart” service philosophy, continues to captivate discerning gourmands with its exceptional culinary craftsmanship and elegant residential-style setting. Guided by its philosophy of “Refined Homeliness”, House of Origin presents thoughtfully curated dining experiences that reinterpret the rich heritage of Cantonese gastronomy through a contemporary lens.

This season, House of Origin joins forces with China’s iconic baijiu Moutai to present an exclusive “A Journey of Craft and Time – 15-Year Moutai Pairing Dinner presented by House of Origin Masters”, where exquisite aged liquors and masterfully crafted Cantonese delicacies come together in a remarkable celebration of time, terroir and craftsmanship. Complementing this exceptional offering, House of Origin will now cater to patrons with a newly introduced lunch service that unveils an array of new signature dishes, inviting guests to savour its refined Cantonese dining by day for convenience.

When Fine Aged Liquor Meets Vibrant Cantonese Fare

Presented by House of Origin and China’s premium Moutai, the exclusive “A Journey of Craft and Time – 15-Year Moutai Pairing Dinner presented by House of Origin Masters” brings together the artistry of Cantonese cuisine and the timeless character of one of China’s most revered spirits. Available at MOP2,888 per guest for just two evenings on 31 July and 1 August, with only two tables available per night, this intimate experience is designed for discerning guests seeking a truly unique culinary journey.

Curated by two-Michelin-starred Culinary Director Xu and brought to life by Resident Chef Lam, the special menu showcases traditional Cantonese craftsmanship elevated by rare premium ingredients. Each dish has been thoughtfully paired with three remarkable aged Moutai expressions, creating a harmonious dialogue between flavour, aroma and heritage.

The pairing experience features the benchmark 15-Year Aged Moutai, a rare 2011 Feitian Moutai that has matured gracefully in bottle for fifteen years, and an extraordinary 2010 Aged Moutai 15-Year, distinguished by its exceptional depth, richness and complexity. Together, these celebrated spirits offer guests a rare opportunity to appreciate the transformative beauty of time and maturation.

The dinner unfolds as an elegant expression of Cantonese culinary heritage, where tradition and innovation converge in a harmonious journey of flavour. From the nostalgic craftsmanship of the Golden Oyster Roll Wrapped in Caul Fat to the signature House of Origin Abalone infused with Moutai aroma, each course is thoughtfully designed to complement the character and complexity of the accompanying aged Moutai, creating a sensory voyage enriched by time.

The special menu features refined creations such as Wok-fried Conch Slices with Shrimp Paste, Braised Pomelo Pith with Crab Roe and Fish Intestine, Crispy Cinnamon-infused Beef Short Rib, Roasted Goose with Fermented Black Bean and Mint, and Wok-fried Wild Mushroom Medley. Together, the dishes reveal a sophisticated progression of flavours, from rich sauce aromas and deep umami notes to the pure elegance of seasonal ingredients.

Highlights include the Braised Pomelo Pith with Crab Roe and Fish Intestine, a masterful composition balancing freshness, sweetness and savoury complexity with a lingering, refined finish. The Crispy Cinnamon-infused Beef Short Rib captivates with the gentle fragrance of cinnamon and red dates, unfolding layers of warmth and richness. The experience culminates with a comforting Pork and Rice Noodle Roll with Macau’s century-old miso sauce, a tribute to local culinary heritage that provides a memorable and deeply authentic finale.

Complemented by a nourishing herbal soup and delicate petit fours, this exclusive dining experience is more than a pairing of rare aged Moutai and exceptional Cantonese cuisine, offering an unforgettable encounter with the artistry and enduring elegance of Cantonese gastronomy.

The signature dishes featured in “A Journey of Craft and Time – 15-Year Moutai Pairing Dinner” will remain available at House of Origin, offering guests the opportunity to savour the exceptional creations born from the collaboration between Galaxy Macau’s newest Cantonese dining destination and China’s iconic Moutai. Each dish elevates heritage, craftsmanship and refined Cantonese artistry.

Introducing a New Lunch Experience Inspired by the Seasons

Honouring the Cantonese philosophy of seasonal dining, Chef Xu and Chef Lam capture the essence of summer through House of Origin’s newly launched lunch service and seasonal menu. Showcasing an abundance of fresh gourds, vegetables and premium seasonal seafood, the menu also pays tribute to Macau’s culinary heritage through the thoughtful use of ingredients such as shrimp paste by the century-old Kong Hing Loong, reflecting respect for local flavours and traditions.

Designed to meet growing demand for an elevated daytime Cantonese dining experience, the new lunch service extends the warmth and intimacy of House of Origin’s authentic, refined dining concept into the afternoon. Upholding the restaurant’s signature “Refined Homeliness” philosophy, the menu celebrates ingredient purity, seasonality and meticulous craftsmanship.

Leading the “Exquisite Lunch Signature” menu are two newly introduced signature dishes: Crab Meat and Bitter Melon Silky Soup and Black Pepper Geoduck Clam Soup Rice Noodle.

The former combines sweet local bitter melon with fresh crab meat and crab stock to create a silky, refreshing soup with remarkable depth and elegance. The latter showcases a rich ivory-coloured broth simmered for four hours with pork tripe, old hen, pork bones and white peppercorns, accompanied by geoduck clam, wild sole fish fillet and sliced tripe. Finished tableside with the pouring of the fragrant hot broth, the dish delivers both culinary theatre and heart-warming comfort.

The summer menu further celebrates seasonal ingredients such as bitter melon, night-blooming jasmine and winter gourd, alongside premium seafood including young mud crab, fresh abalone, wild grouper and razor clams. Through masterful Cantonese techniques ranging from slow-simmered soups and velvety broths to expertly executed wok-frying, Chef Xu reveals the purest expression of each ingredient.

Among the highlights, Stir-Fried Conch and Partridge with Night-Scented Flower combines the delicate floral fragrance of jasmine blossoms with conch, shrimp, partridge and fresh lily bulbs, finished with crunchy walnuts for added texture and a captivating wok hei. The classic Double-Boiled Winter Melon and Frog with Dried Scallop, inspired by the celebrated Tai Shi Banquet tradition, features tender frog leg and sweet winter melon in a crystal-clear broth simmered for four hours. Equally enticing is Braised Hairy Gourd with Crab Roe Paste, where the natural sweetness of the gourd is elevated by the rich umami of aromatic crab paste.

Meanwhile, the comforting Rice Noodle Soup with Geoduck and Wild Sole embodies the warmth of a traditional family banquet, while the Crab Meat and Duran Bitter Melon Soup, featured on both the lunch and seasonal menus, offers guests a refreshing expression of summer that is both heart-warming and refined.

For the latest updates on Galaxy Macau and House of Origin, please visit: www.galaxymacau.com.

Hashtag: #GalaxyMacau

The issuer is solely responsible for the content of this announcement.

About Galaxy Macau Integrated Resort

Galaxy Macau, The World-class Luxury Integrated Resort delivers the “Most Spectacular Entertainment and Leisure Destination in the World”. Developed at an investment of HK$43 billion, the property covers 1.1 million-square-meter of unique entertainment and leisure attractions that are unlike anything else in Macau. Nine award-winning world-class luxury hotels provide close to 5,000 rooms, suites and villas. They include Banyan Tree Macau, Galaxy Hotel™, Hotel Okura Macau, JW Marriott Hotel Macau, The Ritz-Carlton, Macau, Broadway Hotel, Raffles at Galaxy Macau, Andaz Macau and Capella at Galaxy Macau. Unique to Galaxy Macau, the 75,000-square-meter Grand Resort Deck features the world’s longest Skytop Adventure Rapids at 575-meters, the largest Skytop Wave Pool with waves up to 1.5-meters high and 150-meters pristine white sand beach. Two five-star spas from Banyan Tree Spa Macau and The Ritz-Carlton Spa, Macau help guests relax and rejuvenate.

As the dining destination in Asia, Galaxy Macau offers a wide variety of gastronomic delights, exquisite experiences and ingredients of the finest quality with over 120 dining options from Michelin dining to authentic delicacies; Galaxy Promenade is the hottest shopping destination featuring the latest in fashion and curated experiences in Macau. Spanning over 100,000-square-meter, luxury flagship stores, lifestyle boutiques and our selection of labels are among the more than 200 world-renowned brands for a world-class shopping journey; Galaxy Cinemas, immersive thrills and luxurious comfort go hand in hand at Galaxy Cinemas. All 10 theatres are equipped with the latest audio-visual technology; CHINA ROUGE, one-of-a-kind deluxe lounge that evokes the glitz and glamor of Shanghai’s golden era with entertainment in luxury and style; and Foot Hub presents the traditional art of reflexology to make you feel more relaxed and revitalized. For Authentic Macau Flavours & Vibrant Asian Experiences, Broadway Macau – just a 90-second walk via a bridge from Galaxy Macau, has over 35 Authentic Macau & Asian Flavours at its Broadway Food Street. The 2,500-seat Broadway Theatre plays host to world-class entertainers and a diverse array of cultural events. Meeting, incentive and banquet groups are also well looked after with a portfolio of unique venues in Galaxy Macau and a professional service staff.

Galaxy International Convention Center (GICC) is the latest addition to the Group’s ever-expanding integrated resort precinct and will usher in a new era for the MICE industry in Macau. GICC is a world-class event venue featuring 40,000-square-meter of total flexible MICE, and a 16,000-seat Galaxy Arena – the largest indoor arena in Macau.

For more details, please visit ![]() www.galaxymacau.com,

www.galaxymacau.com, ![]() www.broadwaymacau.com.mo and

www.broadwaymacau.com.mo and ![]() www.galaxyicc.com.

www.galaxyicc.com.

Media OutReach

Breaking the Bed Bug Control Industry Bottleneck: Nobedbugs-HK Redefines Global Bed Bug Eradication Standards with Proprietary Technology

Targeting Limitations of Conventional Practices: Nobedbugs-HK Engineers Precision-Driven Bed Bug Remediation Solutions

The pest control industry is marked by uneven entry barriers. Most traditional exterminators rely solely on chemical sprays, which only eliminate surface bed bugs. Eggs and nymphs concealed within wall crevices and furniture remain untouched, failing to resolve infestations at their source and leading to frequent recurrences. This superficial treatment model has triggered a steady stream of consumer complaints and dissatisfaction. Compounding the issue, many pest control firms lack the technical expertise and field experience to address tight spaces or cluttered environments, creating treatment blind spots that compromise eradication efficacy and introduce potential safety hazards during operations.

Contrary to the industry’s prevalent profit-driven, perfunctory service model that overpromises underdelivers, Nobedbugs-HK upholds its founding mission of sharing technical expertise to advance the entire sector. Its team regularly conducts technical seminars and exchange programs for property management, hospitality and pest control practitioners across multiple countries and regions. These sessions elaborate on bed bug breeding triggers, transmission pathways, scientific eradication methodologies and routine prevention protocols. The global pest control industry has long grappled with stagnant technology and outdated operational standards. Nobedbugs-HK’s cross-border knowledge exchange initiatives bridge regional technical gaps, steering the industry away from crude, slipshod treatment protocols toward rigorous, science-led remediation. These global outreach efforts have also equipped the brand with an extensive international perspective and cross-jurisdictional service expertise.

Driven by proprietary technological innovation and a global operational vision, Nobedbugs-HK has built its market footprint and sterling professional reputation through consistent, reliable eradication results. Its technological breakthroughs and contributions to the industry have garnered coverage from leading international media outlets. This authoritative global recognition underscores overseas markets’ high regard for Hong Kong’s pest control innovations and validates the city-developed bed bug treatment framework as a benchmark for global adoption.

Self-Developed Thermal Treatment Technology Boosts Bed Bug Remediation Efficiency in High-Rise Buildings

Bed bug control in high-rise structures remains a longstanding technical challenge plaguing pest control professionals worldwide. Conventional extermination methods are only viable for low-rise or open-plan spaces and prove ineffective against the complex structural layouts of high-rises, enabling persistent, recurring bed bug infestations. Addressing this global technical gap, Nobedbugs-HK independently engineered the world’s exclusive thermal treatment system and custom operating procedures tailored specifically for high-rise complexes, delivering a transformative solution to this decades-long industry pain point.

A radical departure from traditional chemical pesticide applications, this proprietary technology leverages physical high-temperature treatment to penetrate the most concealed structural recesses. It eliminates 95% of all bed bug life stages—adults, nymphs and deeply embedded eggs—to sever their reproductive cycle at the root. Complemented by the brand’s exclusive formulations, the treatment creates a long-lasting residual protective barrier that blocks cross-unit bed bug migration from adjacent premises. Unlike chemical-based extermination, high-temperature thermal treatment leaves zero chemical residues, generates no indoor contamination and poses no harm to human occupants, rendering it ideal for residential complexes, hotels, office towers and shopping malls. It resolves the core challenges of bed bug remediation in high-rise buildings with unmatched precision, with no comparable technology or service available globally to date.

Over 10,000 Cases Inform Standardised Service Protocols

Real-world case outcomes serve as the ultimate metric for gauging technological performance. Many industry players offer no efficacy guarantees and provide virtually non-existent after-sales support, leaving clients burdened with recurring infestations and repeated service fees. To date, Nobedbugs-HK has completed over 10,000 bed bug remediation projects solely within Hong Kong, serving residential properties, five-star hotels, corporate office towers and chain enterprises across diverse urban residential and commercial environments. Backed by its proprietary thermal treatment technology and standardised construction workflows, the brand maintains a flawless 100% permanent eradication track record across all cases, effectively suppressing bed bug resurgence with zero treatment failures. Its proven track record of thousands of successful cases has countered widespread industry malpractice, earning widespread acclaim and positive client testimonials across Hong Kong’s online forums and social media platforms.

Beyond its core treatment technology, mainstream commercial pest control products lack targeted efficacy against bed bugs’ unique nesting and reproductive traits, a key driver of recurring infestations. Generic formulations fail to counter the pests’ elusive hiding instincts and rapid breeding cycles, drastically diminishing treatment outcomes. Drawing on data accumulated from over 10,000 field cases, Nobedbugs-HK independently develops and manufactures custom bed bug control formulations. Iteratively refined for deployment across diverse global environments, these safe, non-toxic and long-lasting products are widely recognised by industry practitioners as the gold standard for bed bug mitigation. The brand delivers bespoke, meticulous bed bug eradication solutions tailored for Hong Kong residents, standing in stark contrast to competing service providers that offer minimal after-sales support.

Industry specialists identify two critical barriers to effective bed bug control: the stringent technical requirements for densely populated premises and the complete elimination of infestations at their source—two persistent flaws that have hindered conventional pest control operations for years. Armed with its one-of-a-kind global thermal treatment technology, in-house proprietary formulations, international operational insights and thousands of successful remediation cases, Nobedbugs-HK comprehensively rectifies the shortcomings of traditional extermination models. Beyond providing permanent relief for household and commercial bed bug infestations, the brand has established a new universal benchmark for the global bed bug control industry.

Hashtag: #NobedbugsHK

The issuer is solely responsible for the content of this announcement.