By Modupe Gbadeyanka

The globally recognised real estate-focused West African Property Investment (WAPI) Summit, which recently took place between the 28th and 29th of November 2017 provided delegates with insight into a real estate sector that is set to rebound strongly in 2018.

During the summit, two of the continent’s foremost real estate analysts presented a collaborative white paper: Nigeria’s Real Estate Investment Trust (REITs) market, which provides cause of optimism in one of the most underinvested and marginalised markets of the Nigerian stock market.

The white paper is authored by Stanbic IBTC’s head of real estate finance for West Africa, Mr Adeniyi Adeleye, and global commercial real estate provider JLL’s advisory head for Sub-Saharan Africa, Thomas Mundy.

It provides an analysis of underlying structural weaknesses that have contributed to the historical negative performance of this market.

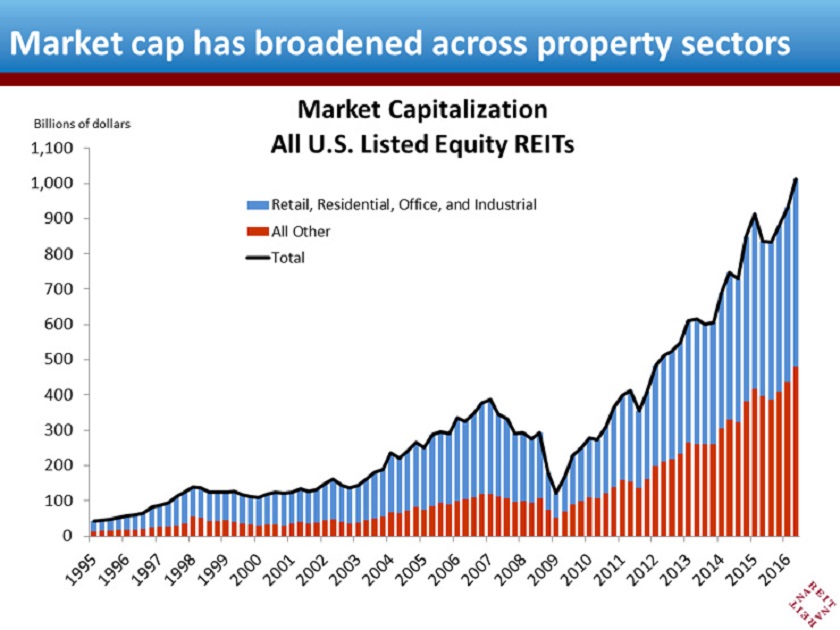

Despite its existence for more than ten years, the Nigerian REITs market is underdeveloped with only three established and with a combined market capitalisation of $151 million, or 0.36% of the local stock market.

This low investment is a result of Nigeria’s deficit of A-grade real estate compared to similar urbanising environments combined with an inherently volatile and non-diversified economy overly reliant on crude oil.

These factors have created cycles of boom and bust which have negatively impacted the real estate sector and crucially investor confidence.

An additional factor cited was a lack of assurance on ambiguous ‘tax pass through’ laws, that have not provided comfort to institutional investors, both local and foreign, resulting in a REITs market that has failed to develop to its potential, which new reforms hope to address.

Mundy and Adeleye predict that an evolving and reformed REITs market will strengthen and deepen capital markets.

It will also assist in providing greater transparency and data to a traditionally opaque market, which has resulted in mispricing and undermining confidence in real estate assets.

Additional benefits stated include greater diversification of portfolios to help break concentration risk and result in increased exposure for Nigeria’s pension funds to the property market.

Currently, the pension fund exposure is 0,36% compared to South Africa’s pension fund exposure to REITs which stands at 2.6%.

Provided that regulatory improvements take place coupled with the sustainable creation of assets to reduce the supply gap in Nigeria, Adeleye and Mundy are optimistic that these changes will lead to a vibrant REITs market, which will transform the real estate sector and the larger economy.