Economy

Nigeria’s Tax Base to Increase by 40 million

By Adedapo Adesanya

The Nigerian government is planning to increase the country’s tax base by 40 million in an effort to raise its revenue, which is needed to execute some projects and run the economy smoothly.

It plans to achieve this through the collaboration between the Federal Inland Revenue Service (FIRS) and the Market Traders Association of Nigeria (MATAN).

The two organisations are planning to collect taxes from 40 million traders across the country in order to bring them out of the informal environment into the nation’s wider tax base.

They have teamed up to facilitate the collection and remittance of value-added tax (VAT) from its members using a unified systems technology.

The tax authority made the announcement on Monday via its official Twitter handle, saying this was particularly for those working in the informal sector.

The statement noted that a unified systems technology would be used to carry out the collaboration, also known as the VAT direct initiative (VDI).

MATAN is the umbrella organisation for all commercial associations in Nigeria and has over 40 million traders as members all over the country’s market.

According to the federal revenue service, MATAN is anticipated to “promote awareness on VAT collection and remittance in the marketplace and informal sector, while also simplifying VAT payment and remittance for the marketplace and informal sector using a purpose-built digital platform” through the program.

“MATAN has a digital platform which enumerates their members, giving them a digital ID and tracks their turnover so that VAT accrued is collected and remitted to the FIRS,” the statement read.

“The VDI is the first of its kind programme that will utilise technology to foster collaboration between FIRS and the marketplace for the collection and remittance of VAT,” it added.

FIRS said that the agreement will allow it to work with security organisations “to curb the activities of touts, miscreants, and self-imposed tax collectors involved in illegal tax collection in Nigeria’s market spaces.”

The agency added that the Value Added Tax (VAT) will increase VAT revenue for the three levels of government, which in turn will provide more funds for infrastructure, social services and the general well-being of the people.

According to FIRS, every member of MATAN will be issued with an identity card upon enumeration for the purpose of ensuring compliance and accountability.

“This card contains their tax identification number (TIN) and other personal details for tax purposes,” the agency said.

This move is part of efforts by President Bola Tinubu’s new administration to expand the country’s tax revenue.

He announced that he would increase Nigeria’s tax-to-GDP ratio, which is currently estimated at 10.21 per cent, despite the recent improvements in collection. This is still below Africa’s average of 16 per cent, and during his inauguration, he promised to increase public revenue after announcing the removal of fuel subsidies and later defending the unification of foreign exchange rates.

By Aduragbemi Omiyale

The Global Banking and Finance Review has named Stanbic IBTC Capital, a subsidiary of Stanbic IBTC Holdings, as the Best Investment Bank in Nigeria for 2026.

The leading financial publication picked Stanbic IBTC Capital for the honour in recognition of its commitment to leadership and excellence in Nigeria’s investment banking sector.

The selection process involves an extensive evaluation of performance across critical metrics, including innovation, client service, financial health, and industry advancement.

Stanbic IBTC Capital’s accolade reflects its strong dedication to delivering capital markets and financial advisory solutions for clients in both the public and private sectors.

The firm has made significant strides in facilitating groundbreaking transactions, offering market-leading expertise in equity, debt, and structured finance, while nurturing the growth ambitions of businesses and institutions across Nigeria.

“We are truly pleased to be acknowledged for our relentless pursuit of excellence in the investment banking arena.

“This honour reflects our commitment to hard work and further establishes the deep trust our clients have in our expertise and service.

“It further motivates us to maintain our dedication to exceptional service, cultivate impactful partnerships, and continue delivering innovative financial solutions that meet our clients’ aspirations,” the chief executive of Stanbic IBTC Capital, Mr Oladele Sotubo, stated.

The Executive Director of Corporate and Transaction Banking at Stanbic IBTC Bank, Mr Eric Fajemisin, on his part, said, “Receiving this esteemed acknowledgement from the Global Banking and Finance Review Awards underscores our commitment to driving innovation and excellence within Nigeria’s investment banking landscape.

“This accolade highlights the significant role our skilled team plays in fostering economic growth and stability.

“We are dedicated to delivering exceptional value to our clients, which not only supports their financial success but also contributes to the broader development of the nation’s financial ecosystem.”

The Global Banking and Finance Review annually celebrates institutions that demonstrate quality, innovation, and contributions to the advancement of banking and financial services worldwide.

Now in its 16th edition, the awards honour organisations that uphold outstanding service standards, strategic execution, and industry leadership.

By Aduragbemi Omiyale

The Governor of Rivers State, Mr Siminalayi Fubara, has presented the 2026 Appropriation Bill to the Rivers State House of Assembly.

The 2026 budget estimate of N1.85 trillion, christened Budget of Resilience for Growth and Development, was presented to the state parliament on Friday.

Mr Fubara stated that the proposed spending for the 2026 fiscal year represents a 24.49 per cent increase over the adjusted 2025 budget, driven by anticipated growth in Federation Account Allocation Committee (FAAC) allocations, derivation revenue and internally generated revenue.

He informed the lawmakers that the state hopes to earn N487.61 billion from internally generated revenue, N936.05 billion from FAAC allocations, derivation funds, Value Added Tax (VAT) and exchange gains, and N382.48 billion from capital receipts, including loans, grants and asset sales.

According to him, N413.11 billion is for recurrent expenditure and N1.405 trillion for capital projects, underscoring his administration’s commitment to accelerating development across the state.

He added that personnel costs would gulp N154.77 billion, while N15.22 billion would fund new recruitments, stating that the budget also provides for pensions, gratuities, death benefits and debt servicing.

Governor Fubara further proposed a 50 per cent increase in overhead expenditure for Ministries, Departments and Agencies (MDAs) to strengthen their operational capacity immediately after the budget is signed into law.

He also stated that the largest allocation under the capital budget is the Works and Infrastructure sector with N533.32 billion, followed by Education with N315 billion and Healthcare with N105.43 billion.

In addition, N41.44 billion is for the Rivers State House of Assembly, N30 billion for the Judiciary, N19.26 billion for Agriculture, N15 billion for Power, N8.5 billion for Chieftaincy and Community Development, N7.98 billion for Sports, N7 billion for Youth Development, N6.5 billion for Women Affairs, and N6.61 billion for Environment and Sustainable Development.

The Governor noted that the budget was designed to sustain economic growth, expand critical infrastructure and improve the welfare of residents, pointing out that it builds on the achievements of his administration despite the challenges experienced by the state.

According to him, the budget prioritises the completion of ongoing road projects, new infrastructure investments, improved education and healthcare services, job creation and expanded economic opportunities for residents.

Describing the proposal as a people-centred budget, he assured Rivers people that every public fund would be judiciously utilised to deliver quality services, attract investment and stimulate inclusive development.

Mr Fubara acknowledged the delayed presentation of the budget and appealed to members of the House of Assembly to give the appropriation bill speedy consideration and passage to facilitate timely implementation.

In his remarks, the Speaker of the Rivers State House of Assembly, Mr Martin Amaewhule, acknowledged that the 2026 Appropriation Bill was presented later than expected but assured the Governor that the legislature would expedite its consideration in the interest of the people of Rivers State.

By Adedapo Adesanya

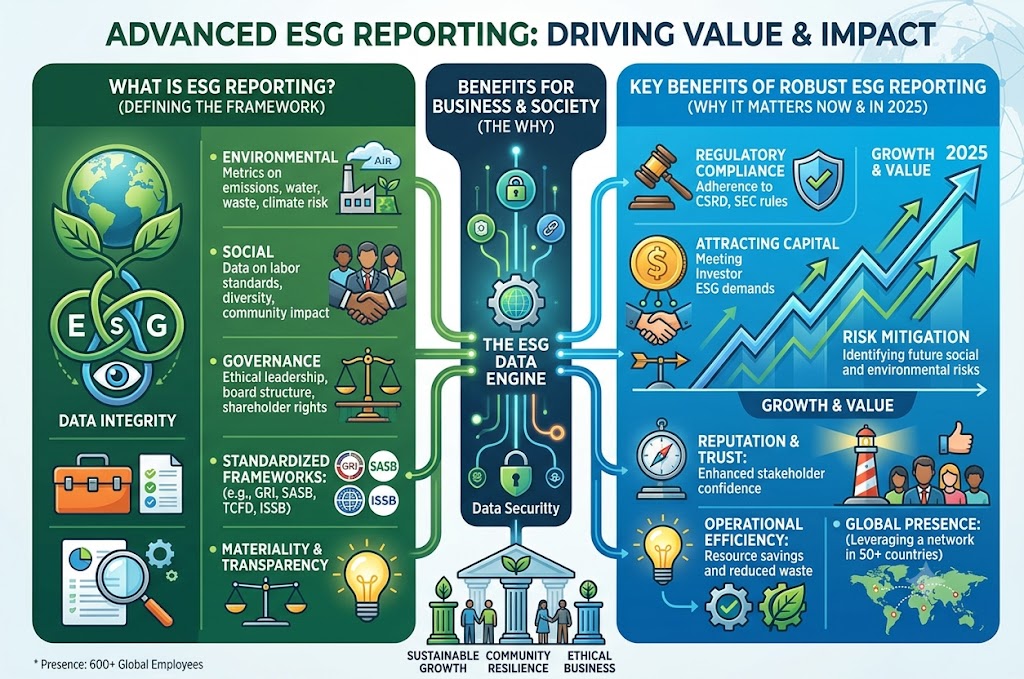

The Securities and Exchange Commission (SEC) has unveiled plans to make sustainability reporting mandatory for large public interest entities from 2027.

This comes as Nigeria moves to align its corporate disclosure framework with global environmental, social and governance (ESG) reporting standards.

The phased implementation will begin with voluntary adoption by early adopters and large public interest entities before becoming mandatory in 2027. The requirement will extend to other public interest entities in 2028 and small and medium-scale enterprises (SMEs) by 2030.

The Director-General of the SEC, Mr Emomotimi Agama, disclosed this at the 2026 Financial Institutions Training Centre (FITC) Sustainability and ESG Conference 3.0, themed ‘Building a Sustainable Africa: Integrating Environmental Stewardship, Social Investment, and Strong Governance for a Prosperous Future’ in Lagos.

Mr Agama said Nigeria’s sustainability disclosure regime is being aligned with the International Sustainability Standards Board (ISSB) framework, including IFRS S1 and IFRS S2, which have emerged as the global benchmark for sustainability reporting.

He said that institutional investors increasingly consider ESG performance a key determinant of capital allocation rather than a peripheral corporate responsibility issue, noting that the price of entry is disclosure.

He said the reforms would strengthen investor confidence and position Nigerian businesses to access global capital markets, where sustainability disclosures are becoming an essential investment requirement.

According to him, Nigeria’s capital market has recorded significant expansion, with market capitalisation growing from about N130 trillion to nearly N160 trillion following recent market reforms, while assets under management have surpassed N9 trillion.

To deepen sustainable finance, Agama said the commission was promoting infrastructure, green and municipal bonds, alongside infrastructure-focused investment funds, to mobilise long-term capital for critical national projects.

He added that the commission would also encourage investments in the blue economy and support financing for the power sector through green energy bonds, project bonds and public-private investment structures.

The SEC chief cited the recent launch of the Nigerian Exchange (NGX) Impact Board as another milestone in advancing sustainable finance and urged companies, regulators and investors to move beyond commitments by embedding sustainability into governance, operations and investment decisions.