Economy

Tinubu Eyes German Investments in Targeted Sectors

By Adedapo Adesanya

Nigeria is determined to pursue German investments in targeted sectors of the Nigerian economy, President Bola Tinubu told German Federal Chancellor, Mr Olaf Scholz, on the sidelines of the G20 Compact with Africa Economic Conference on Monday.

President Tinubu drew the attention of the German leader to the need for his business community to focus their attention on value-additive processing in Nigerian solid minerals, agricultural goods, automobile production, and other job-creating sub-sectors of the economy.

He recognized the success of Siemens AG in positively transforming the quantity and quality of electric power supply.

The President noted that under his leadership, the staggered and unsteady implementation of the Siemens-supported Presidential Power Initiative (PPI) would take on new urgency with a more deliberate process of project execution.

He also recognized the need to embrace Siemens technology in all aspects of the project for sustainability.

“For me, I am very much committed to pursuing all aspects of the Siemens Power project and the skill development opportunities that will emerge from that project for our talented youths who can participate in sustaining the industry,” the President affirmed, according to a statement by his spokesman, Mr Ajuri Ngelale.

The President further expressed his keen interest in the role Siemens can play in modernizing and expanding Nigeria’s rail network with the provision of ultra-modern trains and railways which can more than double the speed of existing 100km/hour standard-gauge systems presently operating in Nigeria.

To this, the German Chancellor expressed readiness but with an acknowledgement of the need to resolve administrative and financial hurdles brought about by governance problems emanating from prior administrations in the sector.

“I know that there is a lot of work that has been done. There is already a big production of electricity in Nigeria, but it is not getting to the population. Of course, this has to do with the need for a provision of stations and infrastructure on the grid.

“Siemens has developed the plan and is ready to deepen implementation, but it is now up to your new government to take the follow-up action that you are now committed to taking.

“On the railway plans, Siemens will be very happy to do this when more progress is made on the power project which has been started already,” the German Chancellor said.

Mr Tinubu also said, “Everything the world requires in terms of business environment reforms are underway in Nigeria. Perhaps our foreign investors are still a bit paranoid that those old Nigerian issues are intractable. But my track record speaks for itself. I have transformed an entity before now. I am here to do it again, and I will.”

The German Chancellor nodded in agreement and said, “There is nothing too unique about the growth of China. It came down to a lot of investment from overseas that leveraged cheap and skilled labour with adequate internal infrastructure and shipping infrastructure for imports and exports to flow easily. These things are possible in Nigeria. You even have abundant natural resources. Step by step, it is achievable, Mr President.”

The two leaders of the largest economies in Africa and Europe, respectively, agreed to deepen collaboration on the utilization of advanced biometric systems and border control technology to check irregular migration.

The statement also added that the two leaders agreed that investments in labour-intensive industries will go a long way toward resolving the root causes of the problem.

By Adedapo Adesanya

Brent crude prices fell by $3.05 or 3.37 per cent to $87.33 per barrel on Friday, the lowest level since early March, triggered by expectations of an imminent peace agreement between the United States and Iran.

Also, the US West Texas Intermediate (WTI) crude finished at $84.88 a barrel after it gave up $2.83 or 3.23 per cent. It was its lowest level since April 17.

Reuters reported that a memorandum between the US and Iran to halt the war in the Gulf could be signed as soon as Sunday, citing sources.

The sources indicate that the US would immediately begin releasing billions of Dollars in frozen Iranian assets and waive sanctions on its oil exports, in return for Iran opening the strait.

The proposals also include discussion of possible war reparations for Iran and dropping longstanding US demands for limits on Iran’s missile program, the sources were quoted as saying.

Meanwhile, Iranian Foreign Minister Abbas Araqchi said on Friday that a memorandum of understanding had not yet been signed and could still change.

He also said that management of the Strait of Hormuz would not return to the pre-war era, that sovereignty over the strait belonged to Iran and Oman, and that Iran would secure safe passage for ships through it.

US President Donald Trump called off threatened air strikes against Iran on Thursday, while it was reported that final negotiations on the memorandum would focus on nuclear and economic issues but would exclude discussions about Iran’s missile programme.

On Thursday, Iran announced a complete closure of the Strait of Hormuz, saying it would fire on any ship trying to pass through.

Traffic through the strait, which normally carries a fifth of global oil and liquefied natural gas shipments, has been extremely limited as a result of the war.

The US military, however, said on social media that commercial ships continued to transit the waterway.

Goldman Sachs lowered its 2027 average Brent forecast to $80 a barrel on higher supply and lower demand, but expects prices to exceed the 2025 average on stockpiling of OECD commercial oil stocks and a security premium for disruptions.

The Organisation of the Petroleum Exporting Countries (OPEC) on Thursday lowered its forecast for 2026 world oil demand growth to 970,000 barrels per day from a previous 1.17 million barrels per day, its second straight downward revision.

By Modupe Gbadeyanka

The Lagos-based Dangote Petroleum Refinery has been described by Standard Bank Group as a transformational industrial project with far-reaching implications for Nigeria and Africa.

The company, which is Africa’s largest financial institution, gave this description after a tour of the facility recently.

Standard Bank, the parent company of Stanbic IBTC Holdings, has promised to support the planned listing of the 650,000 barrels per day refinery and expressed readiness to finance future expansion projects across the continent.

The chief executive of the lender, Mr Sim Tshabalala, said, “We are here because the Dangote Group is a large and important global player and a significant force on the African continent.”

“Standard Bank is the largest financial institution in Africa, and we have partnered with Dangote on a variety of initiatives. We are here to lend support, to see this magnificent refinery and to discuss Vision 2030 and how we can continue supporting the Group’s growth ambitions,” he added.

Mr Tshabalala disclosed that Standard Bank intends to play a leading role in the refinery’s planned Initial Public Offering and future growth initiatives.

“As Dangote lists, there is an IPO coming up, and we are a leading player in that process,” he said, adding that, “As the group continues to expand in Nigeria and across Africa, there will be opportunities for financial advisory services and balance sheet support, and we stand ready to provide both.”

He further described the refinery as “a wonder of the world,” noting that its impact is already being felt through stronger foreign exchange earnings, improved balance-of-payments performance and enhanced energy security.

“This is a wonder to behold. It is massive, productive and transformative. It is already making a significant contribution to Nigeria’s economy through its impact on foreign reserves, the balance of payments and the lives of ordinary Nigerians,” he said.

The Group Vice President for Oil and Gas at Dangote Industries Limited, Mr Devakumar Edwin, said the visit represented a significant milestone in a partnership that began during the refinery’s construction phase.

“The bank visited us during construction and understood the scale of what we were building,” Mr Edwin said. “Today, the refinery is fully operational, and they can see what their support has helped to create. It is like nurturing a tree and eventually seeing it bear fruit.”

He added that both organisations are exploring opportunities to deepen collaboration as Dangote expands its industrial footprint across Africa.

Also speaking, the chief executive of Dangote Petroleum Refinery, Mr David Bird, said the visit highlighted the importance of long-term partnerships in delivering large-scale industrial projects.

“Standard Bank has been one of our strongest supporters throughout the history of the refinery and the broader Dangote Group.

“This visit was an opportunity to demonstrate what that support has enabled. Seeing is believing, and it allows our partners to appreciate the scale of what has been achieved,” Mr Bird stated.

The visit also coincided with a major operational milestone for the refinery, which has now exceeded its original design capacity.

Mr Bird disclosed that the refinery recently completed performance test runs at 700,000 barrels per day, above its nameplate capacity of 650,000 barrels per day.

“We have always believed there was engineering flexibility built into the design,” he said. “Achieving sustained production of 700,000 barrels per day is a testament to the technical capability of our people and the strength of the systems we have built.”

By Adedapo Adesanya

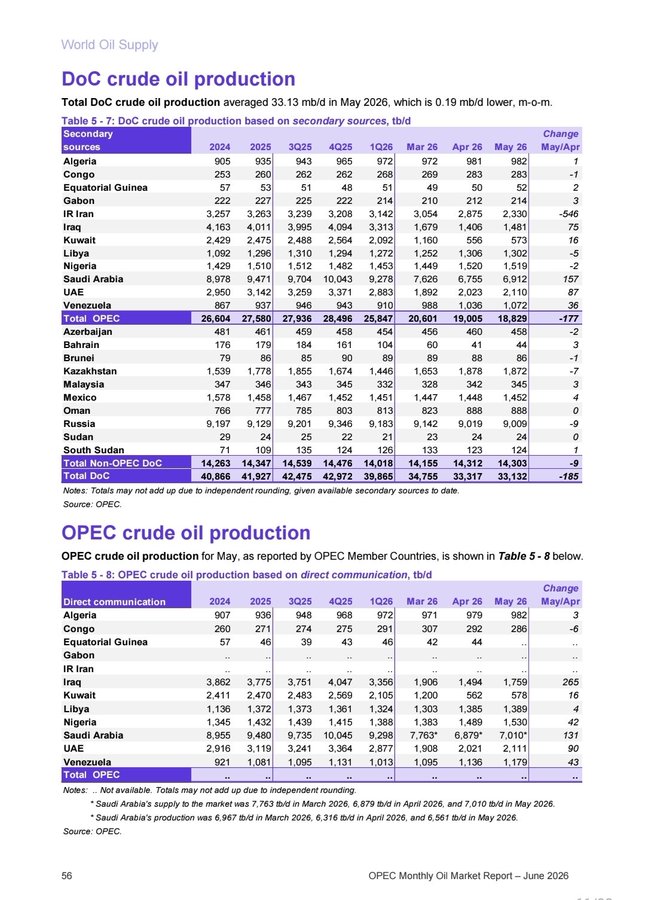

Nigeria produced about 1.530 million barrels of crude oil per day in May 2026, beating its Organisation of Petroleum Exporting Countries (OPEC) quota by 42,000 barrels per day. In the preceding month, the country only produced 1.489 million barrels per day.

In the latest OPEC’s Monthly Oil Market Report (MOMR), it was also revealed that Iraq in April supplied 1.494 million barrels per day while in May, it produced 1.759 million barrels per day, an increase 265,000 barrels per day; Saudi Arabia, 6.879 million barrels per day in April, 7.010 million barrels per day in May, an increase of 131,000 barrels per day; United Arab Emirate (UAE), 2.021 million barrels per day in April and in May 2.111 million barrels per day, an increase of 90,000 barrels per day while Venezuela, 1.136 million barrels per day in April and 1.179 million barrels per day in May, an increase of 43,000 barrels per day.

Using secondary sources, Nigeria’s production decreased from 1.520 million barrels per day in April to 1.519 million barrels per day; Saudi Arabia, 6.755 million barrels per day in April and 6.912 million barrels per day in May; UAE, 2.023 million barrels per day in April, 2.110 million barrels per day in May; and Venezuela, 1.036 million barrels per day in April and 1.072 million barrels per day in May.

Nigerian Upstream Petroleum Regulatory Commission (NUPRC), in a statement by its Head, Media and Corporate Communications, Mr Eniola Akinkuotu, confirmed that Nigeria, in May, met 102 per cent of OPEC quota as production hit an 11-month high.

According to it, Nigeria’s oil production witnessed an upswing in May 2026, averaging 1,530,354 barrels of crude oil and 170,446 barrels of condensates per day, bringing the total combined production to 1, 700, 800 barrels per day and consolidating Nigeria’s position as Africa’s largest oil producer.

It stated that the average crude oil production recorded in May represents 102 per cent of Nigeria’s 1.5mbpd of production quota allocated by OPEC.

It explained that production performance during the review period remained robust, with combined crude oil and condensate output ranging between a low of 1.51 million barrels per day and a peak of 1.86 million barrels per day.

The organisation added that the May 2026 production figures represented the highest recorded by Nigeria since July 2025, when output surged to 1,712,282.

NUPRC said: “In strict crude oil terms (excluding condensates), the 1.53 million barrels recorded in May 2026 represents the highest Nigeria has witnessed since January 2025 when crude oil production hit 1.538 mbpd.”

“On a month-on-month basis, production rose by 2.77 per cent in May 2026 as against 1.48mbpd in April. The broader production trend over the last five months has also remained positive.

“Combined crude oil and condensate output increased from 1.48 mbpd in February to 1.54 mbpd in March, 1.66 mbpd in April, and then 1.7 mbpd in May, underscoring sustained growth in Nigeria’s hydrocarbon production levels.

“Among production streams, Bonny Terminal led the pack with a total blend of 293,870 bpd, closely followed by Forcados Terminal at 289,900 bpd. Qua Iboe ranked third with 173,360 bpd, while Escravos Oil Terminal contributed 135,470 bpd. Odudu (Amenam Blend) completed the top five production streams, accounting for 63,250 bpd during the month under review.”

The commission attributed the rise in production to a sustained positive momentum as operations remained stable throughout the reporting period with no significant pipeline or facility outages recorded.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn