Economy

MAN Forecasts Challenging Environment for Manufacturers in 2024

By Adedapo Adesanya

The Manufacturers Association of Nigeria (MAN) has said that the outlook for the Nigerian manufacturing sector in 2024 would be challenging, adding that it will only be eased by some positive policy directions.

According to the MAN Director General, Mr Segun Ajayi-Kadir, the year would be challenging, with a subtle possibility of recovery from the third quarter of 2023.

He said the envisaged recovery was highly dependent on the deployment of policy stimulus supported by a synthesis of domestic growth driven by export-focused and offensive trade strategies.

This, he said, would promote resilience, and steady growth and ensure that the sector gains meaningful traction in the later part of the year, noting that a quick examination of the trajectory of manufacturing globally portrayed a struggling sector challenged by key macroeconomic variables and externalities, leading to dwindling growth.

This, he said, was evidenced by the manufacturing growth rates in China, the United States of America, and South Africa with Nigeria not exempted, averring that the manufacturing growth rate nosedived to 0.48 per cent in Q3 2023 as against 2.4 per cent in 2021.

“Drawing from likely economic dynamics and in the light of the aforementioned, the projections for the manufacturing sector in 2024 are as follows— there will be clarity on the actual and specific policy direction and priority areas of the current administration, especially around deepening industrialisation and we look forward to engaging government in this regard.

“In 2024, sectoral real growth is expected to hit about 3.2 per cent; contribution to the economy will most likely exceed 10 per cent and the Manufacturers’ CEOs Confidence Index is predicted to rise above 55 points threshold by the end of Q4 2023.

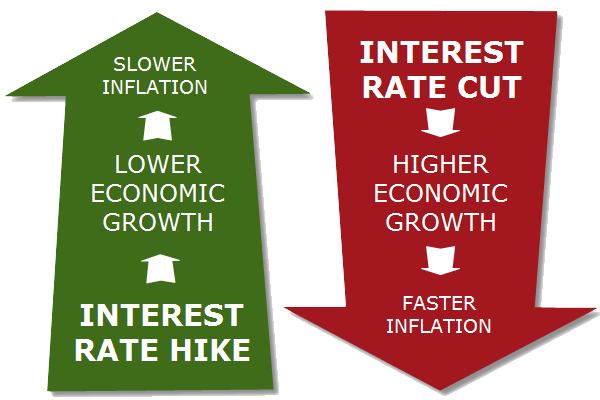

“Average capacity utilisation will still hover around the 50 per cent threshold as the foreign exchange related challenges and high inflation rate limiting manufacturing performance may linger until mid-year.

“The sector may experience a meagre improvement in manufacturing output as foreign exchange and interest rates related challenges are expected to subside from the third quarter,” he said.

Mr Ajayi-Kadir added that higher manufacturing output was envisaged from the beginning of the third quarter of the year.

This, he explained, would happen as the government disburses capital provisions of the budget to abandoned, ongoing and new capital projects with expected special preference for locally made products.

He said the ongoing concessions of seaports, airports, and roads may also provide opportunities for the cement sub-sector and contribute to infrastructure upgrades needed to enhance manufacturing productivity.

He said the results of the emerging upward surge in global oil prices, domestic oil and gas production, local refining of petroleum products and projected gains of exchange rate unification would promote stability in the foreign exchange market.

This, he stated, would impact manufacturing positively from the second half of the year lead to a reduction in the pressure on demand for foreign exchange and improve the inflow of export proceeds from oil and gas.

“We should expect dynamic implementation of the Electricity Act 2023, which will increase private investment in renewable energy, enhance energy efficiency and improve electricity supply to the manufacturing sector.

“The improved electricity supply will ameliorate the issue of inadequacy, reduce the disruptions occasioned by frequent outages and in turn improve energy security.

“In broad terms, the year 2024 may start on a tough note for manufacturing but may end with some measured improvements because the envisaged policy reforms, improved commitment to domestic production and general positive outlook seem favourable for the sector,” he said.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange rallied by 1.70 per cent on Thursday, June 25, after three price gainers overpowered the two price losers recorded at the close of business.

Consequently, the market capitalisation of the trading platform increased by N43.79 billion to N2.618 trillion from N2.574 trillion, and the NASD Security Index (NSI) improved by 72.96 points to close at 4,362.32 points, in contrast to Wednesday’s 4,289.36 points.

Yesterday, the price advancers were led by Nipco Plc, which chalked up N31.79 to close at N349.76 per unit versus the preceding day’s N317.97 per unit. Okitipupa Plc gained N18.00 to end at N298.00 per share versus the previous session’s N280.00 per share, and Central Securities Clearing System (CSCS) Plc went up by N7.11 to N86.79 per unit from N79.68 per unit.

On the flip side, Nitrox Industrial Gases Plc crumbled by 32 Kobo to close at N21.09 per share compared with the N21.41 per share it closed at midweek, and Food Concepts Plc depreciated by 25 Kobo to N2.51 per unit from N2.76 per unit.

During the session, the value of securities traded by investors went down by 86.7 per cent to N10.9 million from the preceding session’s N82.9 million, and the volume of securities dropped 84.9 per cent to 10.9 million units from the previous 82.9 million, while the number of deals grew by 84.2 per cent to 35 deals from 19 deals.

At the close of trades, Great Nigeria Insurance (GNI) Plc remained the most traded stock by value on a year-to-date basis, with 3.4 billion units sold for N8.4 billion, trailed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units valued at N6.5 billion, and CSCS Plc with 68.4 million units exchanged for N4.7 billion.

GNI Plc was also the most traded stock by volume on a year-to-date basis, with 3.4 billion units worth N8.4 billion, followed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units transacted for N415.7 million.

By Dipo Olowookere

The Nigerian Exchange (NGX) Limited further suffered a 0.64 per cent decline on Thursday as the bears tightened their grip on the bourse.

For the second straight session, all the key sectors of Customs Street pointed south, with the energy counter down by 5.22 per cent. The insurance index slumped by 2.59 per cent, the banking space depreciated by 0.28 per cent, and the consumer goods segment moderated by 0.06 per cent, while the industrial goods sector was flat, though with a marginal fall.

As a result, the All-Share Index (ASI) contracted by 1,493.71 points to 233,580.83 points from 235,074.54 points, and the market capitalisation retreated by N959 billion to N149.888 trillion from N150.847 trillion.

Investor sentiment remained weak after a negative market breadth index, as there were 21 price gainers and 34 price losers.

Aradel and Deap Capital went down by 10.00 per cent each to N1,575.00 and N4.05, respectively. Trans-Nationwide Express fell by 9.90 per cent to N3.64, Regency Alliance slipped by 9.57 per cent to N85 Kobo, and C&I Leasing dipped by 9.48 per cent to N28.12.

Conversely, Red Star Express grew by 9.60 per cent to N24.55, Legend Internet expanded by 9.09 per cent to N6.00, Neimeth appreciated by 7.10 per cent to N8.30, Abbey Mortgage Bank rose by 5.45 per cent to N8.70, and Ellah Lakes improved by 4.65 per cent to N9.00.

Yesterday, market participants traded 393.7 million equities valued at N19.2 billion in 45,813 deals compared with the 488.1 million equities worth N20.9 billion transacted in 46,239 deals recorded a day earlier, implying a shortfall in the trading volume, value, and number of deals by 19.34 per cent, 8.13 per cent, and 0.92 per cent, respectively.

The most active stock for the session was Access Holdings with a turnover of 39.1 million units worth N896.2 million, Chams traded 24.5 million units valued at N96.5 million, Fidelity Bank sold 24.1 million units for N436.9 million, Sterling Holdings exchanged 23.8 million units valued at N182.2 million, and Zenith Bank transacted 18.9 million units worth N2.1 billion.

By Adedapo Adesanya

The Naira recorded a marginal gain of 43 Kobo or 0.03 per cent against the United States Dollar on Wednesday, June 25, in the Nigerian Autonomous Foreign Exchange Market (NAFEX) to sell for N1,380.11/$1 compared with the previous day’s N1,380.54/$1.

However, the Nigerian currency lost N3.21 against the Pound Sterling in the official market during the session to close at N1,818.84/£1, in contrast to Wednesday’s exchange rate of N1,815.63/£1, and against the Euro, it fell by N3.21 to trade at N1,566.84/€1 versus midweek’s value of N1,563.63/€1.

In the same vein, the Nigerian Naira depreciated against the Dollar at the GTBank FX deck yesterday by N3 to sell for N1,383/$1 compared with the preceding session’s value of N1,380/$1, and at the black market window, it remained unchanged at N1,395/$1.

Interbank FX turnover at the NFEM window surged by about 56 per cent day-on-day to close at $195.371 million from $125.588 million reported on Wednesday, according to data from the Central Bank of Nigeria (CBN).

The Naira continues to feel the impact of rising FX payments and a strong US Dollar amid a sharp slowdown in forex market interventions by the central bank, with more than six weeks of no support for the local currency.

Nigeria’s foreign reserves increased further to $51.142 billion, while oil prices continue to be held in the $70 range by developments in the geopolitical scene.

Meanwhile, in the cryptocurrency market, Bitcoin sank below $60,000 as more than $1 billion in crypto positions were liquidated over the past 24 hours, with longs accounting for $842 million of the damage. About 148,500 traders were wiped out. The largest single position was a $38 million bitcoin-dollar bet on Hyperliquid. It led at $489 million in liquidations and dropped 2.8 per cent to sell at $59,862.61.

Ethereum (ETH) crashed by 5.5 per cent to $1,554.57, Ripple (XRP) declined by 4.8 per cent to $1.03, Cardano (ADA) fell by 4.3 per cent to $0.1433, Dogecoin (DOGE) dropped 3.4 per cent to sell at $0.0745, TRON (TRX) slid 2.2 per cent to $0.3215, Binance Coin (BNB) slumped by 1.8 per cent to $561.34, and Solana (SOL) dipped by 0.3 per cent to $62.94, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) sold flat at $1.00 each.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn