Economy

Tinubu Defends Subsidy Removal

By Adedapo Adesanya

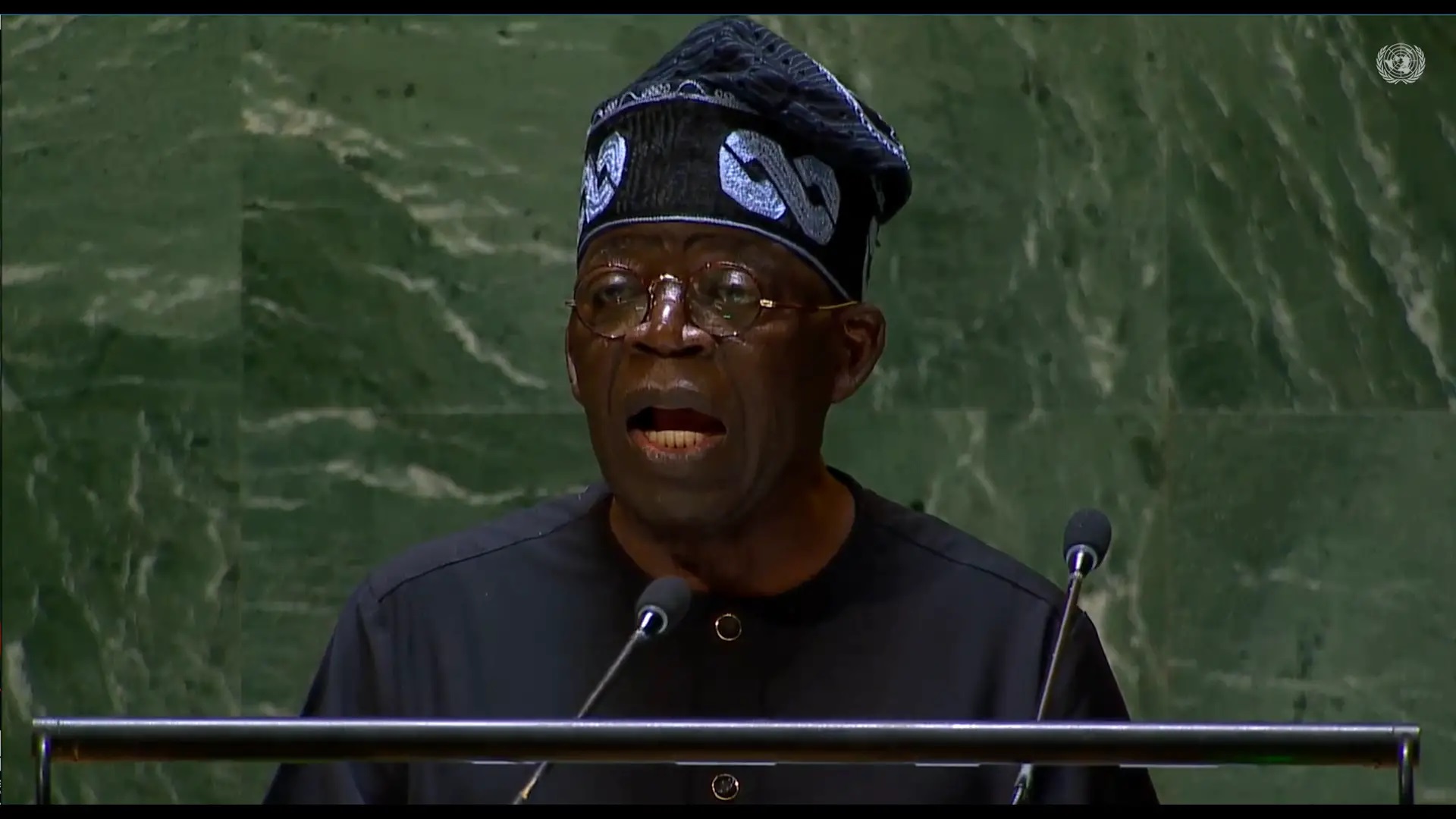

President Bola Tinubu has once again defended his administration’s decision to remove the petrol subsidy, saying it was indispensable to prevent the country from going bankrupt.

He made the statement on Sunday as one of the panellists at the ongoing World Economic Forum (WEF) in Riyadh, Saudi Arabia, monitored by Business Post.

Recall that Mr Tinubu announced the removal of subsidy on petrol the day he was inaugurated into office on May 29, 2023, saying that subsidy is gone. This led to increases in the prices of commodities to rise through the roof, increasing hardship in the country.

However, recent revelations have shown that subsidy remains, a fact that the administration has not acknowledged. The IMF had in February said the policy has returned.

Yet during the session, President Tinubu justified the petrol subsidy removal, maintaining that it was needed to reset the economy.

“For Nigeria, we are immensely consistent with the belief that the economic collaboration and inclusiveness are necessary to engender stability in the rest of the world.

“Concerning the question of the subsidy removal, there is no doubt that it was a necessary action for my country not to go bankrupt, to reset the economy and pathway to growth,” he said.

He admitted the difficulty associated with his decision to remove the policy which has allowed Nigerians to purchase petrol at cheaper rates for years but said that he was convinced it was in the best interest of the people.

“It is going to be difficult, but the hallmark of leadership is taking difficult decisions at the time it ought to be taken decisively. That was necessary for the country. Yes, there will be blowback, there is an expectation that the difficulty in it will be felt by a greater number of the people, but once I believe it is their interest that is the focus of the government, it is easier to manage and explain the difficulties.

“Along the line, there is a parallel arrangement to cushion the effect of the subsidy removal on the vulnerable population of the country. We share the pain across the board, we cannot but include those who are vulnerable.

“Luckily, we have a very vibrant youthful population interested in discoveries by themselves and they are highly ready for technology, good education committed to growth. We can manage that and partition the economic drawback and the fallout of subsidy removal.”

President Tinubu also said that the petrol subsidy removal equally engendered accountability, transparency and physical discipline for the country.

By Adedapo Adesanya

The duo of MRS Oil and FrieslandCampina Wamco Nigeria Plc weakened the NASD Over-the-Counter (OTC) Securities Exchange by 0.68 per cent on Friday, June 5.

MRS Plc lost N19.00 during the session to sell at N171.00 per share compared with Thursday’s value of N190.00 per share, and FrieslandCampina Wamco Nigeria Plc depreciated by N8.70 to finish at N181.68 per unit compared with the preceding session’s N190.38 per unit.

As a result, the market capitalisation further lost N22.59 billion to close at N2.607 trillion versus the N2.630 trillion it ended a day earlier, and the NASD Unlisted Security Index (NSI) dropped 37.76 points to settle at 4,358.32 points, in contrast to the previous day’s 4,396.08 points.

The alternative stock market closed the last trading day of this week with a price gainer, Central Securities Clearing System (CSCS) Plc, which gained 6 Kobo to quote at N78.40 per share compared with the preceding session’s N78.34 per share. However, it could not prevent the market from going down at the close of business.

Yesterday, the volume of securities bought and sold by investors went down by 50.0 per cent to 140,345 units from the preceding day’s 280,714 units, the value of stocks decreased by 16.5 per cent to N17.9 million from the previous session’s N21.5 million, and the number of deals carried out by market participants fell by 35.7 per cent to 27 deals from the 42 deals recorded on Thursday.

When trading activities closed for the day, Great Nigeria Insurance (GNI) Plc remained the most active stock by value on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, trailed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units sold for N6.5 billion, and CSCS Plc with 64.7 million units traded for N4.4 billion.

GNI Plc also ended the session as the most traded stock by volume on a year-to-date basis, with 3.4 billion units worth N8.4 billion, followed by Infracredit Plc with 2.3 billion units transacted for N6.5 billion, and Resourcery Plc with 1.1 billion units valued at N415.7 million.

By Dipo Olowookere

Renewed interest in financial stocks and others lifted the Nigerian Exchange (NGX) Limited by 0.15 per cent on Friday.

Customs Street closed higher yesterday despite the 1.37 per cent loss recorded by the consumer goods sector as a result of profit-taking.

This was offset by gains in the other key sectors of the local bourse, as the insurance counter chalked up 1,14 per cent. The banking space appreciated by 0.90 per cent, the industrial goods segment grew by 0.46 per cent, and the energy sector expanded by 0.01 per cent.

Consequently, the All-Share Index (ASI) went up by 366.00 points to 242,593.31 points from 242,227.31 points, and the market capitalisation gained N235 billion to close at N155.594 trillion compared with the previous day’s N155.359 trillion.

The trio of International Energy Insurance, Abbey Mortgage Bank, and DAAR Communications improved by 10.00 per cent each yesterday to N7.26, N9.35, and N1.98, respectively, while Zichis advanced by 9.39 per cent to N32.38, with Sovereign Trust Insurance up by 8.70 per cent to N2.50.

On the flip side, Academy Press lost 9.84 per cent to quote at N8.25, University Press depreciated by 9.73 per cent to N5.10, Africa Prudential dipped by 2.63 per cent to N12.95, Chams crumbled by 2.44 per cent to N4.00, and International Breweries slipped by 1.59 per cent to N12.35.

Business Post reports that the market breadth index was positive during the session after recording 37 appreciating equities and 14 depreciating equities, implying strong investor sentiment.

Abbey Mortgage Bank led the activity chart with a turnover of 164.1 million units worth N1.5 billion, Ellah Lakes sold 76.7 million units for N767.2 million, Access Holdings transacted 44.8 million units valued at N1.1 billion, Linkage Assurance exchanged 23.0 million units worth N41.2 million, and The Initiates traded 20.2 million units for N562.1 million.

At the close of trades, market participants transacted 608.5 million units worth N32.0 billion in 53,826 deals versus the 588.5 million units valued at N27.9 billion executed in 57,352 deals in the previous session. This showed that the number of deals eased by 6.15 per cent, the volume of transactions rose by 3.40 per cent, and the value of transactions soared by 14.70 per cent.

By Adedapo Adesanya

The Naira further depreciated against the United States Dollar by N3.46 or 0.25 per cent to N1,362.21/$1 from N1,358.75/$1 in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Friday, June 5.

However, it appreciated against the Pound Sterling in the same market window during the session by N4.47 to trade at N1,823.59/£1 compared with the previous day’s N1,828.06/£1, and gained N7.00 against the Euro to sell at N1,574.58/€1, in contrast to Thursday’s closing price of N1,581.58/€1.

For another trading session, the Nigerian Naira maintained stability against the Dollar in the parallel market and the GTBank forex counter on Friday at N1,375/$1 and N1,372/$1, respectively.

The Naira is expected to remain strong in the near term, backed by a rise in external reserves, which are nearing $50 billion, enhancing analysts’ confidence about its outlook in the second half of 2026.

Heightened global uncertainty has reduced the incentive for importers and corporates to demand FX, as cautious trade weighs on import needs. Analysts estimate a $40 billion net FX position for the year, a projection anchored in oil windfall gains.

As for the cryptocurrency market, prices remained depressed following a strong US jobs report that spurred markets to price in higher-for-longer interest rates, sending Treasury yields and the dollar up while hammering stocks, especially AI-related names. Crypto markets saw heavy leverage washouts with about $1.6 billion in positions liquidated over 24 hours.

Ethereum (ETH) gave up 4.9 per cent to trade at $1,584.68, Solana (SOL) fell by 3.3 per cent to $63.22, Bitcoin (BTC) crashed by 1.9 per cent to $61,333.23, Dogecoin (DOGE) slipped by 1.8 per cent to $0.0821, and Ripple (XRP) moderated by 1.8 per cent to $1.09.

Further, TRON (TRX) dropped 1.6 per cent to sell at $0.3197, Binance Coin (BNB) slumped by 1.0 per cent to $581.18, and Cardano (ADA) declined by 0.4 per cent to $0.1589, while the US Dollar Tether (USDT) gained 0.07 to sell at $0.9997, and US Dollar Coin (USDC) closed flat at $0.9998.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn