Economy

All IOCs’ Divestments Followed PIA Guidelines—NUPRC

By Adedapo Adesanya

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) has reaffirmed its commitment to transparency and regulatory compliance in overseeing the divestment activities of International Oil Companies (IOCs) operating in Nigeria.

In a press statement released on Monday signed by the Head of the Public Affairs Unit, Mr Olaide Shonola, the regulator provided detailed updates on several high-profile divestments, emphasising that all transactions were conducted in strict adherence to the Petroleum Industry Act (PIA) 2021 and other applicable legal frameworks.

The NUPRC highlighted the successful divestments of Nigerian Agip Oil Company (NAOC) to Oando Petroleum and Natural Gas Company Limited (Oando PNGCL) and Equinor Nigeria to Chappal Energies, noting that these approvals were granted only after thorough evaluations.

“The approvals given to the NAOC-Oando and Equinor-Chappal divestments were in accordance with the Petroleum Industry Act (PIA) 2021, defined regulatory framework, and standard consent approval process set by the Commission under the PIA,” the statement said.

The statement went on to highlight the Commission’s meticulous approach to ensuring that all regulatory and legal requirements were met before any divestment could proceed.

Specifically, the NUPRC detailed the multi-stage process involved in the NAOC-Oando transaction, which included technical evaluations, commercial negotiations, and the final ministerial consent.

“The process was conducted in compliance with the requirements of relevant legislation, regulations, and guidelines including the Petroleum Act, Petroleum Industry Act, Petroleum Drilling and Production Regulations, and the Upstream Asset Divestment and Exit Guidance Framework,” the statement read.

The NUPRC then elaborated on its thorough due diligence process, which involved evaluating potential assignees based on factors such as technical capacity, financial viability, legal compliance, and environmental responsibilities.

“The Commission’s thorough evaluation and due diligence process, anchored on the Seven Pillars of the Divestment Framework, ensured that potential assignees were capable and compliant with legal requirements and that all legacy liabilities were identified and appropriately managed,” the statement noted.

The regulator also addressed the ongoing divestment by Mobil Producing Nigeria Unlimited (MPNU) to Seplat Energy Offshore Limited, a transaction that has attracted significant public attention.

It was disclosed that initially, the commission withheld its consent due to MPNU’s failure to obtain a waiver of pre-emption rights and the necessary consent from the Nigerian National Petroleum Corporation (NNPC).

However, following the resolution of these issues, the NUPRC has resumed its due diligence on the transaction, as the statement clarified, “MPNU’s application to the Commission for consent is currently undergoing due diligence review, under the same Divestment Framework applied to the NAOC-Oando and Equinor-Chappal divestment.”

The NUPRC further emphasised that the public’s right to know remains central to its operations, aiming to build trust by providing transparency in the high-stakes divestment processes and ensuring that stakeholders are fully informed about the Commission’s activities.

“NUPRC, as an organisation guided by law and professionalism, will continue to pursue its statutory mandate in a legal, independent, technical, commercial, and professional manner, operating under the authority of the PIA,” the statement concluded.

By Adedapo Adesanya

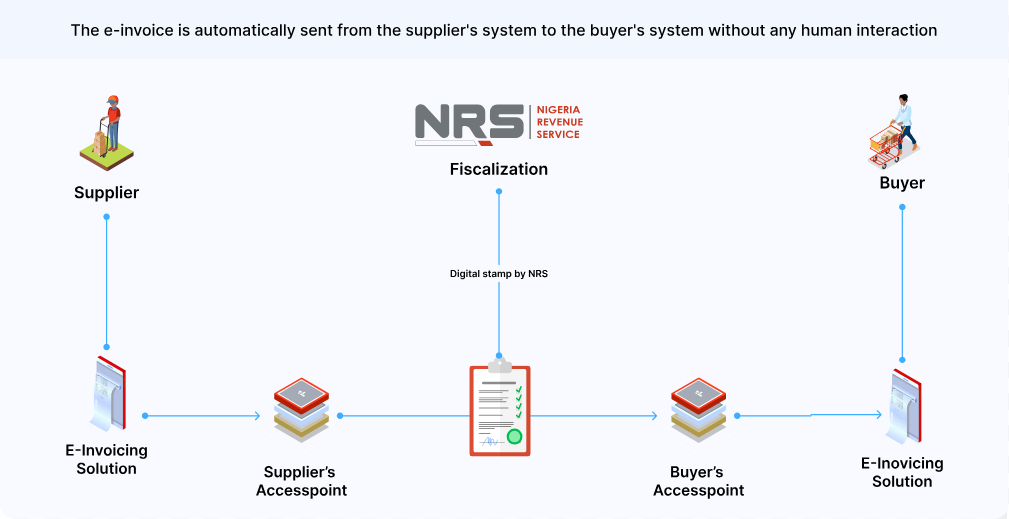

The Nigeria Revenue Service (NRS) says the rollout of electronic invoicing (e-invoicing) will strengthen tax compliance, curb revenue leakages and improve transparency in tax administration as it moves to fully digitise the country’s tax system.

The Project Lead for the NRS e-Invoicing Project, Mr Mohammed Bawa, stated this at the DigiTax E-Invoicing Compliance Breakfast Session held in Lagos on Wednesday.

The event, organised by DigiTax, an NRS-accredited e-invoicing platform, formed part of efforts to support the agency’s ongoing education and sensitisation campaign on the e-invoicing mandate.

Mr Bawa said the initiative aligns with global trends in tax digitisation and is expected to help improve Nigeria’s tax-to-GDP ratio, which remains one of the lowest in Africa.

According to him, the system will provide the NRS with greater visibility into transactions across sectors, formalise activities within the informal economy and standardise invoice formats nationwide using globally recognised invoice schemas.

He added that e-invoicing would improve operational efficiency for both businesses and tax authorities while supporting the NRS’ transition from manual and electronic tax administration processes to a fully automated system-to-system interaction model.

Mr Bawa noted that the legal framework for implementation is backed by the Nigeria Tax Administration Act, which prescribes penalties for non-compliance.

He disclosed that the NRS has completed onboarding large taxpayers and is preparing to enforce compliance with defaulting entities.

According to him, medium taxpayers are expected to begin compliance in the third quarter of 2026, while onboarding of emerging taxpayers will commence in 2027, with full adoption targeted for all taxpayers by the end of 2028.

Mr Bawa urged taxpayers yet to be onboarded onto the platform to begin the process and work with accredited service providers to ensure compliance.

On his part, Country Director of DigiTax Nigeria, Mr Olumide Akinsola, urged businesses to look beyond their internal systems and assess the compliance status of suppliers and counterparties.

He warned that businesses whose suppliers fail to transmit invoices through the MBS platform risk losing eligibility to claim Value Added Tax (VAT) input credits on such transactions, describing the resulting supply chain exposure as a significant commercial risk that many organisations have yet to quantify.

Mr Akinsola also announced the launch of DigiTax’s white paper, The State of E-Invoicing Readiness in Nigeria, which examines compliance adoption trends and the readiness gap across different taxpayer segments.

He added that DigiTax operates in Nigeria, Kenya, Zambia and the United Arab Emirates (UAE), noting that experience from those markets shows businesses that integrate early are better positioned to avoid disruptions when enforcement begins.

By Aduragbemi Omiyale

The names of about 100,000 companies registered by the Corporate Affairs Commission (CAC) are about to be deleted for inactivity, especially for failing to file their annual tax returns, Business Post reports.

This information was disclosed by the CAC via a notice signed by its management on Wednesday, July 15, 2026.

The list contains organisations like the Nigeria-Poland Chamber of Trade Invest Ltd, Alariwo of Afrika Ltd, Ovation Sports International, First Union Pension Fund Administrators, Investopedia Limited, Baptist High School Abuja Ltd, and Yobe Aluminium Manufacturing Industries Ltd, amongst others.

In the statement, the commission said its decision to strike off the names of the affected firms from the register aligns with the provisions of Section 692(3) (3) and (4) of the Companies and Allied Matters Act (CAMA), 2020.

However, the affected companies can still salvage the situation by filing all outstanding annual returns and regularising their records within 90 days.

“Please note that companies that fail to comply within the stipulated timeline shall be struck off the register without further notice,” it declared, expressing its continued commitment to providing prompt and efficient registration and regulatory services to the satisfaction of its valued customers.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange gained 1.75 per cent on Wednesday, July 15, pushing the NASD Security Index (NSI) up by 74.20 points to 4,316.51 points from 4,242.31 points, as the market capitalisation added N44.54 billion to finish at N2.590 trillion compared with the preceding session’s N2.546 trillion.

During the session, there was an 11.5 per cent rise in the value of transactions at midweek to N72.7 million from the preceding session’s N65.2 million, as there was a 3.7 per cent growth in the number of deals to 28 deals from the previous session’s 27 deals, while the volume of securities slumped by 64.5 per cent to 4.9 million units from 13.7 million units.

At the close of trades, Great Nigeria Insurance (GNI) Plc ended as the most active security by value on a year-to-date basis, with 3.4 billion units worth N8.4 billion, with the second spot occupied by Infrastructure Credit Guarantee (Infracredit) Plc after selling 2.3 billion units valued at N6.5 billion, and the third position was taken by Central Securities Clearing System (CSCS) Plc, which exchanged 74.3 million units for N5.3 billion.

GNI Plc also finished the trading day as the most traded stock by volume on a year-to-date basis, with a turnover of 3.4 billion units traded for N8.4 billion, followed by Infracredit Plc with 2.3 billion units transacted for N6.5 billion, and Resourcery Plc with 1.1 billion units sold for N415.7 million.

Business Post reports that the market breadth index was negative yesterday, as there were two price gainers and three price losers.

11 Plc added N22.36 to its value to close at N250.00 per share versus N227.64 per share, and CSCS Plc improved by N7.95 to N90.35 per unit from N82.40 per unit.

On the flip side, FrieslandCampina Wamco Nigeria Plc lost N1.37 to end at N150.00 per share versus N151.37 per share, UBN Property Plc depreciated by 6 Kobo to N1.75 per unit from N1.81 per unit, and Food Concepts Plc dropped 1 Kobo to close at N2.49 per share versus N2.50 per share.