Banking

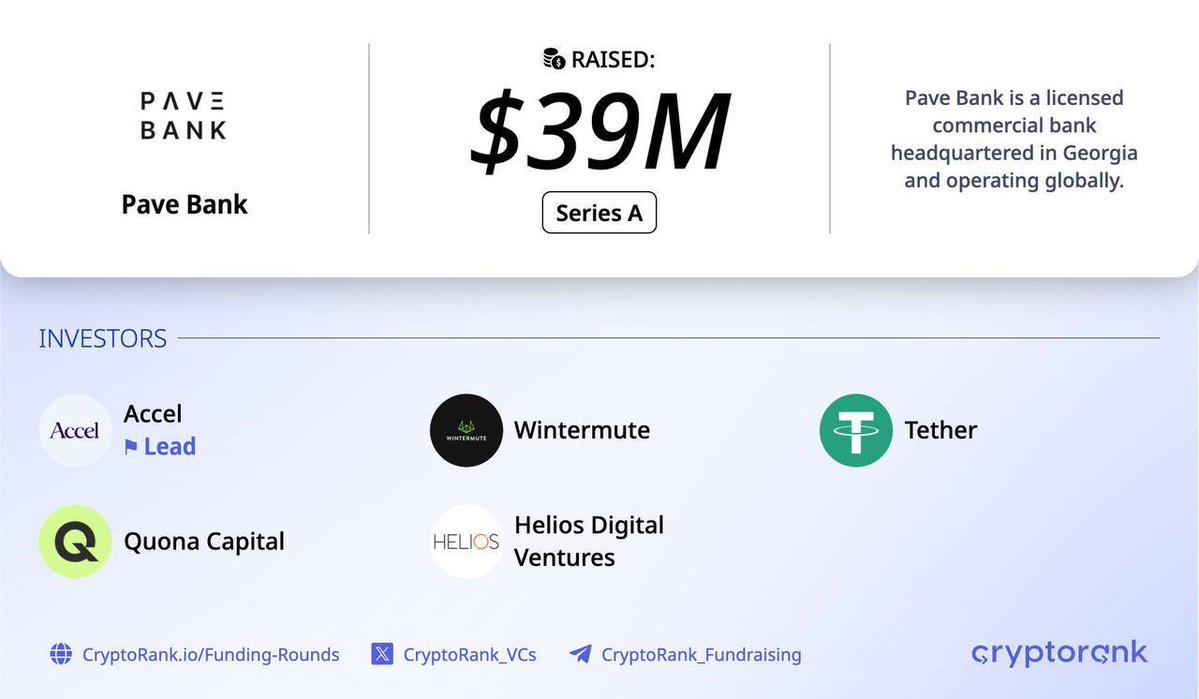

Accel, Tether, Others Pump $39m Into Pave Bank

By Modupe Gbadeyanka

The sum of $39 million has been raised by a fully licensed commercial bank in the United Kingdom, Pave Bank, to scale world’s first programmable bank built for digital assets and artificial intelligence (AI) era.

Much of the funds came from Accel, with support from Tether Investments, Quona Capital, Wintermute, Helios Digital Ventures, Financial Technology Partners, Yolo Investments, Kazea Fund, and GC&H Investments.

The lender will use the money from the fresh capital raising to expand its regulatory footprint, accelerate product development, continue to build institutional grade infrastructure and scale its client coverage across global markets.

Businesses using Pave Bank can manage both fiat and digital assets in real time, automate treasury operations, and reduce reliance on intermediaries.

An exchange or market maker can manage both digital assets, fiat and fixed income treasury products in one place, and at the same time, deal with their counterparties using the Pave Network – enhancing operational liquidity and mitigating operational risk.

Corporates exploring using stablecoins in their operations can unify digital assets and fiat corporate treasuries with regulatory clarity and in a secure manner – improving speed, control, and cost efficiency.

“The global financial system is moving towards regulated on-chain finance, and institutions need a trusted bridge between the old and the new.

“We have built a mulit-asset bank that merges the stability and prudential oversight of traditional finance with the automation, speed, and intelligence of digital assets.

“This is about redefining how money moves safely, transparently, and automatically across the world’s financial systems,” the chief executive and co-founder of Pave Ban, Mr Salim Dhanani, stated.

Also commenting, a partner at Accel, Rachit Parekh, said, “As digital assets become an integral part of the global financial ecosystem, there is a strong need for a well regulated, full reserve approach to banking at the intersection of fiat and digital assets.

“Pave Bank is at the forefront of this fundamental shift in how financial infrastructure operates and we are excited to partner with them.”

Business Post gathered that with this $39 million in funding secured by Pave Bank, its total funding have risen more than $44 million.

The firm was established on two core ideas: that the future of money is programmable, and that businesses need a regulated, bank-grade counterparty capable of operating seamlessly across both traditional and digital asset rails.

Today, the company offers a single platform that unifies commercial banking services – deposit accounts, broad payment coverage, deep FX liquidity, payment card issuance and corporate treasury management – with institutional-grade digital asset management, an instant settlement network and an OTC trading desk.

Instead of managing multiple providers for fiat banking, custody, and liquidity, clients can operate across both systems under one regulatory framework, one compliance standard, and one interface.

By Modupe Gbadeyanka

About N2 billion is expected to be used to finance renewable energy products for customers by the end of 2026 in an effort to accelerate Nigeria’s clean energy transition.

To meet this goal, Sterling Bank is launching Sterling Solar Financing Hubs inside StarTimes retail outlets to embed on-the-spot solar financing at the point of purchase.

From the N2 billion earmarked for this initiative, N600 million has already been used up.

Under this programme, customers can now walk into participating outlets, select their preferred solar solution, receive financial guidance from dedicated Sterling Solar Financing Advisors, and begin the financing process immediately, subject to the bank’s credit assessment.

The first phase of the rollout commenced this July with five Solar Financing Hubs across Lagos, located in Lekki, Ikeja, Festac, Surulere, and Victoria Island.

The network will expand rapidly to 46 StarTimes outlets nationwide before the end of the third quarter of 2026, with a view to extending the model to more than 200 StarTimes locations nationwide.

Both parties have promised to continue working together to democratise access to clean energy financing, empowering more Nigerians to solarise their homes and businesses while contributing to a greener future.

“Sterling exists to enrich lives, and we believe that access to clean, reliable energy should be within everyone’s reach. Through this partnership with StarTimes, we are democratising access to solar by bringing financing directly to the point of need, enabling more families and businesses to transition to sustainable energy without the burden of prohibitive upfront costs. This is about unlocking opportunity, improving livelihoods, and powering Nigeria’s future,” the Divisional Head of Renewable Energy and Mobility at Sterling Bank, Mr Darlington Nwankwo, said.

Also commenting, the Vice President of StarTimes Nigeria, Mr Eric Xiao, said, “With the rollout of the Sterling Solar Financing Hubs, we are doing more than just selling solar products; we are building a sustainable energy ecosystem. By integrating StarTimes’ extensive service network with Sterling Bank’s professional financial services, we are significantly lowering the barrier for Nigerian households and small businesses to access clean energy.

“Moving forward, we will continue to deepen this partnership, ensuring that more Nigerians can enjoy reliable, affordable, and smart energy solutions, ultimately turning our vision of energy accessibility into a reality for all.”

By Modupe Gbadeyanka

The Nigeria Business Summit Regional Tour of Stanbic IBTC Bank made a detour to Jogor Centre, Ibadan, Oyo State, on Wednesday, July 15, 2026, to empower Micro, Small, and Medium Enterprises (MSMEs).

The event brought together business leaders, development partners and government representatives to discuss pathways for sustainable enterprise development across the South-West.

Participants engaged in practical masterclasses on export opportunities; access to finance and business growth strategies; gaining actionable insights into market expansion; trade documentation; credit readiness; financial record-keeping; and structured financing solutions designed to support long-term business success.

The Head of Enterprise Banking at Stanbic IBTC Bank, Ms Olajumoke Bello, informed participants that the programme is part of the lender’s commitments to supporting MSMEs through practical business education, strategic partnerships and improved access to growth opportunities.

The Executive Director of Business and Commercial Banking at Stanbic IBTC Bank, Mr Remy Osuagwu, on his part, said, “Our ambition is to be more than a financial institution to Nigerian businesses. We want to be a trusted growth partner, providing the financing, business insights and advisory support entrepreneurs need to build sustainable enterprises and unlock new opportunities.”

Similarly, the chief executive of Stanbic IBTC Bank, Mr Wole Adeniyi, who reinforced the company’s commitment to enterprise development, highlighted the importance of providing businesses with the right support structures to enable sustainable growth and long-term competitiveness.

“At Stanbic IBTC, we believe that sustainable economic growth depends on the success of small and growing businesses. That is why we are focused on providing access to finance, practical advisory support and the connections businesses need to move from ambition to scale,” he stated.

The Oyo State Commissioner for Investment, Trade, Cooperatives, and Industry, Professor Soliu Adelabu, said the initiative was designed to support businesses and strengthen the state’s entrepreneurship ecosystem, praising the bank for its support for traders, entrepreneurs, and artisans in the state.

The Permanent Secretary in the Oyo State Ministry of Women Affairs and Social Inclusion, Mrs O.M. Shotonwa-Roagess, highlighted the importance of strategic partnerships in expanding economic opportunities for women and vulnerable groups across Oyo State. She noted that the ministry remains open to collaborating with organisations such as Stanbic IBTC, development partners and the private sector to drive financial inclusion, entrepreneurship and sustainable economic empowerment.

The Nigeria Business Summit Regional Tour forms part of Stanbic IBTC’s broader commitment to empowering entrepreneurs through capacity building, financial inclusion and strategic business support, helping enterprises unlock new opportunities for growth and long-term success.

The Ibadan leg built on the momentum of previous tour stops in Katsina and Aba.

By Adedapo Adesanya

The Governor of the Central Bank of Nigeria (CBN), Mr Yemi Cardoso, says Nigeria anticipates remittances from citizens living abroad to increase by two-thirds in 2026 as it seeks to bolster its foreign-exchange reserves to $1 billion monthly.

“We are expecting that by the end of the year, we will hit about a billion Dollars a month from diaspora remittances,” he said at the 14th Annual BusinessDay CEO Forum in Lagos on Thursday, themed From Stability to Shared Prosperity.

Mr Cardoso said remittances are expected to be boosted from more than $600 million currently, banking on the CBN’s deliberate target at remittances to diversify reserve sources beyond oil earnings.

According to him, the apex bank engaged Nigerians abroad, banks and international partners to identify barriers to official remittance flows.

He said the lender subsequently reviewed policies to ensure easier movement of funds into and out of the country.

Mr Cardoso described the approach as providing free entry and free exit for foreign exchange.

He said the reforms helped double diaspora inflows within one year and exceeded initial expectations, also projecting annual remittances could reach about $8 billion if the current momentum was sustained, adding that the development reflected growing confidence in Nigeria’s financial system and foreign exchange market.

Mr Cardoso said reforms introduced by the apex bank had restored stability in the foreign exchange market and improved investors’ confidence.

He identified exchange rate unification as one of the central bank’s major achievements under the reforms programme.

According to him, replacing multiple exchange rate windows with a market-driven system eliminated distortions and improved transparency.

Mr Cardoso said improved foreign exchange liquidity and stronger reserves were among the gains from the reforms.

He said Nigeria’s net external reserves had risen from about $3 billion at the start of the reforms to above $40 billion currently, noting that gross external reserves had grown to about $52 billion, representing about 10 months of import cover.

According to him, the reserves are designed to shield the economy from external shocks and excessive market volatility.

He said the reserves were not meant for routine interventions or day-to-day exchange rate management.