Economy

Golden Guinea Breweries Gets N3.6b Grant to Revive Operations

By Dipo Olowookere

A grant of N3.6 billion has been given to the management of Golden Guinea Breweries Plc to get the company back to life.

The firm, listed on the Nigerian Stock Exchange (NSE) on January 1, 1979, is located on Aba Road, Afara Layout, Umuahia in Abia State and it produces Golden Guinea beer.

A statement issued by the company disclosed that the funding package was provided by the Nigerian Export Import Bank (NEXIM) with the Bank of Industry also pitching in with an Economic Revival Facility.

These new funds have granted a new lease of life to the company and installation works have resumed in earnest.

The statement said in the next couple of months, barring new untoward developments, Golden Guinea Breweries Plc, Umuahia will be reopened to the public.

Golden Guinea was originally named Independence Brewery Limited. It started production in 1963 with an annual capacity of 1 million gallons.

The company introduced Eagle Stout to the market in 1967 but between 1967 and 1970, further production was hampered by the Nigerian Civil War.

In 1971, the company changed its name to Golden Guinea Breweries and four years later, it was revamped and an extension built by the German firm Coutinho Caro which later participated in an equity offering issued by the firm.

However, production at the brewery was hampered by a fire incident in 2003 but recent attempts have been made to resuscitate the firm. The company holds franchise rights to produce and market Golden Guinea Beer, Holsten Brewery’s Bergedorf premium lager beer and Bergedorf Malta in Nigeria.

Majority shares in the company were later purchased by Pan Martine Investments Ltd promoted by Mr Okey Nzenwa from Mbaise in Imo State.

Mr Nzenwa then set about resuscitating ailing company. His company replaced the burnt boilers and proceeded to install an entirely new line of production making Golden Guinea the company with the most modern brewery in West Africa.

However, due to the financial crisis of 2015 and the skyrocketing cost of the dollar, the company ran into problems actuated by the cost at which needed equipment was invoiced and the prevailing cost of FOREX at the time of payment and delivery.

The crisis affected the ability of the company to meet projected resumption timelines.

The company needed more funds to complete its retooling works and because of its existing debt exposures, lenders were wary. Events ground to a halt.

Thus was the state of affairs until the Governor of Abia State, Dr. Okezie Ikpeazu decided to lead a drive to resuscitate all moribund industries in Abia State irrespective of ownership.

It bears stating that almost all the industries in Abia State hitherto owned by Government have been privatised preceeding the assumption of office of Dr. Ikpeazu as Governor.

Leveraging on the solid relationship he had built with the Federal Government, Dr Ikpeazu took Mr Okay Nzenwa to Vice President Yemi Osinbajo where the promoter of Golden Guinea stated his case and explained how macro-economic policy of the Federal Government affected his investment and has hampered his ability to raise new funds to restart the company.

The Vice President graciously approved the request of Mr. Nzenwa for Federal Government lending institutions to grant him facilities.

By Adedapo Adesanya

The Nigeria Revenue Service (NRS) and the Joint Revenue Board (JRB) have issued new guidelines clarifying the taxation of virtual assets in Nigeria.

The guidelines provide an administrative framework for the taxation of virtual assets and specify the tax obligations of individuals and businesses operating in the sector.

According to a public notice issued by the two agencies, the framework covers registration, reporting and record-keeping requirements, valuation principles and the tax treatment of virtual asset transactions.

It applies to taxpayers, Virtual Asset Service Providers (VASPs), peer-to-peer (P2P) marketplace operators, tax practitioners and other persons engaged in virtual asset-related activities.

The NRS and JRB said the guidelines were developed in line with the provisions of the Nigeria Tax Act 2025 and the Nigeria Tax Administration Act 2025.

The two bodies said the release was aimed at providing clarity, certainty and consistency in the administration of Nigeria’s tax laws as the country’s virtual asset ecosystem continues to evolve.

The agencies added that the framework would promote voluntary compliance, enhance transparency and support the development of a fair and efficient tax system for digital asset transactions.

They urged all affected taxpayers and stakeholders to familiarise themselves with the guidelines and ensure compliance with the applicable tax obligations.

The guidelines are available on the official websites of the two agencies.

By Adedapo Adesanya

Manufacturers are yet to benefit from relief on the burden of multiple taxes and levies despite the enactment of the Nigeria Tax Act 2025, according to the Manufacturers Association of Nigeria (MAN).

The association, in its Manufacturers CEO Confidence Index (MCCI) report for the second quarter of 2026, said manufacturers continued to face multiple tax collectors and regulatory agencies during the period.

Director-General of MAN, Mr Segun Ajayi-Kadir, said the new tax law, which was expected to reduce the burden of multiple taxation, had yet to deliver the intended benefits.

“Manufacturers complained that they were still met with multiple tax collectors and regulators in Q2 2026. It follows that the implementation of the Nigeria Tax Act 2025 is yet to achieve its objective of relieving manufacturers of the burden of taxes and levies,” he said.

According to the report, Nigeria’s business environment remains largely unsupportive of manufacturing growth, with local sourcing of raw materials emerging as the only indicator that recorded noticeable improvement.

MAN, however, warned that the gains in local sourcing could be undermined by worsening insecurity in parts of the country.

The association attributed the improvement largely to persistent foreign exchange constraints, which have forced many manufacturers to source inputs locally.

Despite this, it said excessive regulation and multiple taxation continue to weigh heavily on manufacturers.

The report showed that manufacturers recorded a modest increase in sales volume during the second quarter, but rising production, distribution and logistics costs continued to erode profitability.

It added that capacity utilisation, production levels, investment and employment remained broadly unchanged during the review period.

MAN further observed that although recent foreign exchange reforms had helped stabilise the naira, inadequate foreign currency supply remained a major constraint to manufacturing operations.

Other key challenges identified in the report include poor infrastructure, high production costs, raw material shortages and unfavourable trade policies.

The association said the findings underscore the continued pressure on manufacturers despite recent fiscal and foreign exchange reforms, stressing the need for more effective implementation of policies aimed at improving the operating environment for the real sector.

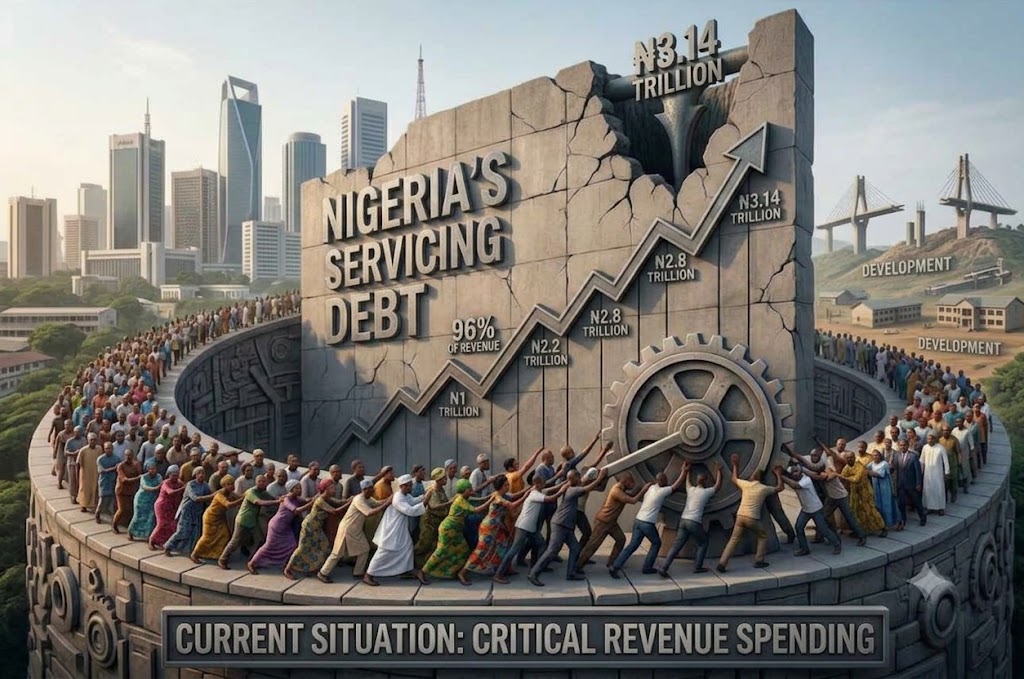

By Adedapo Adesanya

The federal government spent N3.14 trillion on servicing its domestic debt in the first quarter (Q1) of 2026, according to the Debt Management Office (DMO).

The figure, contained in the DMO’s latest domestic debt service report for Q1 2026, comprised N2.97 trillion in interest payments and N169.68 billion in principal repayments.

According to the report, the government spent N741.82 billion on domestic debt service in January before the figure rose to N967.67 billion in February.

Debt service increased further to N1.43 trillion in March, bringing total spending for the quarter to N3.14 trillion.

The March figure represented a 47.7 per cent increase from the N967.67 billion recorded in February and was 92.7 per cent higher than the N741.82 billion spent in January.

The debt office said interest payments accounted for approximately 94.6 per cent of the total domestic debt service during the quarter.

Treasury bills accounted for the largest share of interest payments at N1 trillion, while interest payments on Federal Government bonds stood at N1.96 trillion.

The government also paid N4.24 billion in interest on FGN savings bonds during the period.

The debt management body said the principal component of the debt service comprised N169.68 billion in repayments on local-denominated promissory notes.

Overall, domestic debt service rose significantly throughout the quarter, with March alone accounting for nearly half of the N3.14 trillion spent between January and March.