Economy

Lagos Assures Investors Judicious Use of N100bn Bond

By Adedapo Adesanya

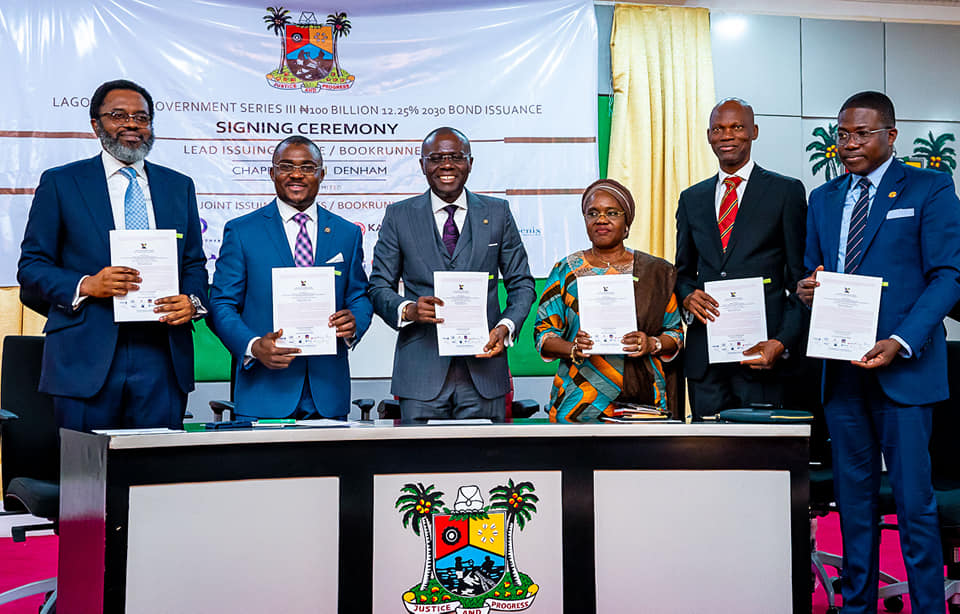

Governor of Lagos State, Mr Babajide Sanwo-Olu, on Wednesday, January 29 signed documents for the issuance of N100.33 billion bond, which was raised from capital market to fund infrastructure and ongoing projects in the state.

The signing ceremony which took place at the State House in Alausa, featured investors and issuing parties present when the governor signed the over-subscribed Series III Bond Issuance of N100 billion, which was issued and raised by the state under its N500 billion bond Programme approved four years ago.

Speaking at the event, the governor said the financial intervention was important to the Lagos economy, saying it is the largest bond programme ever embarked on by any state in the country.

“We have embarked on a new journey that is not meant to serve our personal interest, but to activate more prosperity for our dear Lagos and give our people the hope for better tomorrow we all dreamed.

“When we came into government, we made commitment to all Lagosians that we are coming to pursue and implement an agenda that will build our capacity to achieve Greater Lagos we all will be proud of.

“Today, I am standing in from you all to say we are writing the financial history of Lagos in another chapter and it will bring good dividends to all residents. With this N100 billion bond, we will ensure that all Lagosians feel the direct impact of this intervention in their homes and on the roads.

“We are bringing new infrastructure and repairing the existing ones, including bridges and hospitals. We are going to renovate schools and build new ones for our children; slums will be regenerated and pressing environmental issues will be solves. We are going to make people feel the essence of governance.”

Mr Sanwo-Olu recalled that the effort to raise the bond started three months ago with a simple discussion with professional partners led by Chapel Hill Denham, which worked effortlessly to ensure that the statutory period recommended by Securities and Exchange Commission (SEC) to raise such bond was met.

The Governor applauded the efforts made by partners to secure essential requirements to access the capital for the bond, which involved the reduction of the state’s interest expense by N17 billion, giving the state the opportunity to raise the bond from the capital market.

“Less than three months down the line, we are celebrating the biggest sub-national bond issuance today and the team of partners has also helped us to restructure our entire balance sheet.

“We have been able to revert the entire borrowing of Lagos from very high rate to acceptable numbers. The team has also helped us to reduce interest expense by N17 billion, which made it easy for us to approach the financial market,” he said.

Mr Sanwo-Olu assured investors who subscribed to the N100 billion bond that the funds would be disbursed strictly to finance infrastructural projects required to boost Lagos State’s economy.

Business Post reports that the n100 billion bond was issued at 12.25 percent with a 10-year maturity.

By Dipo Olowookere

The Nigerian Exchange (NGX) Limited shed 0.66 per cent on Thursday, driven primarily by sell-offs in financial stocks.

During the session, the insurance counter depreciated by 2.26 per cent, the banking space dropped 2.04 per cent, the consumer goods index tumbled by 1.18 per cent, and the industrial goods sector gave up 0.70 per cent. They offset the 0.01 per cent leap recorded by the energy segment at the close of business.

Consequently, the All-Share Index (ASI) moderated by 1,617.91 points to 245,362.26 points from the previous day’s 246,980.17 points, and the market capitalisation retreated by N1.005 trillion to N158.340 trillion from Wednesday’s N159.345 trillion.

The worst-performing equity was Tripple Gee, which crashed by 10.00 per cent to N2.88. Lasaco Assurance declined by 9.92 per cent to N2.18, C&I Leasing slumped by 9.84 per cent to N5.50, Mutual Benefits depreciated by 9.80 per cent to N3.22, and Trans-Nationwide Express decreased by 9.03 per cent to N2.82.

The best-performing equity was Legend Internet, which chalked up 8.64 per cent to close at N4.40. DAAR Communications advanced by 7.32 per cent to N1.76, Sterling Holdings grew by 6.67 per cent to N8.00, Sovereign Trust Insurance expanded by 5.73 per cent to N2.03, and Royal Exchange soared by 4.69 per cent to N1.34.

Trading activity yesterday improved when compared with midweek’s, with the volume of trades up by 176.72 per cent to 2.1 billion shares from the 758.9 million shares recorded a day earlier. The value of transactions increased by 582.84 per cent to N230.8 billion from N33.8 billion, and the number of deals shrank by 12.71 per cent to 48,231 deals from the 55,251 deals executed on Wednesday.

First Holdco was the busiest stock for the day, with a turnover of 1.6 billion units valued at N196.2 billion, Access Holdings sold 37.4 million units for N998.5 million, Sterling Holdings exchanged 36.0 million units worth N286.8 million, Ellah Lakes transacted 34.8 million units for N297.8 million, and Zenith Bank traded 33.1 million units valued at N4.0 billion.

By Adedapo Adesanya

The oil market settled lower by 1 per cent on Thursday as traders digested proposed plans for a Saudi Arabia-led maritime coalition to boost defence cooperation around the Red Sea.

Brent futures slipped by $1.71 or 1.88 per cent to $89.03 a barrel, while the US West Texas Intermediate (WTI) crude futures declined by 87 cents or 1.03 per cent to trade at $83.59 per barrel.

Saudi Arabia seeks to lead a coalition to boost defence cooperation in the Bab El-Mandeb Strait, the Red Sea and the Gulf of Aden.

The Saudi defence ministry said 14 states, including Turkey, Pakistan, Egypt, Sudan and Djibouti, have issued a joint statement in support of the proposed multinational maritime defence coalition.

This comes after Iran-aligned Houthi militants in Yemen declared a naval blockade last week on Saudi Arabia, threatening the Red Sea route for its oil exports, an alternative to the largely blockaded Strait of Hormuz. The strait, which normally handles around a fifth of global oil and liquefied natural gas flows, has remained a focal point for oil markets since the US and Israel launched the war on Iran on February 28.

Houthis had attacked Saudi Arabia this week from Iraqi territory in coordination with Iraqi armed groups, reflecting growing coordination among Iran-aligned militias, two officials in the region said. The attacks included strikes on oil facilities in Saudi Arabia’s eastern province, the kingdom’s main crude hub.

Iran and Oman also continued talks on the management of the Strait of Hormuz, after Iran previously ruled out Oman’s proposal for regional joint management of the waterway.

It also denied that it is negotiating with US officials and gave no sign that it was ready to make new concessions over its effective closure of the strait.

Meanwhile, the US military said it had hit dozens of Islamic Revolutionary Guard Corps (IRGC) targets in Iran in an operation launched after it fired ballistic missiles at U.S. forces in the Middle East.

Fresh supply worries also emerged after tankers loading at the Caspian Pipeline Consortium (CPC) terminal headed away from the Black Sea after a vessel was hit during loading at the terminal on Thursday.

A Ukrainian drone attack caused a fire at Lukoil’s Perm refinery that damaged and forced the shutdown of one of its crude distillation units.

By Modupe Gbadeyanka

The federal government has been urged to give all the necessary support to indigenous investors, as they remain Nigeria’s most important drivers of employment, foreign exchange generation and long-term economic resilience.

This advice was given by foremost businessman, Mr Aliko Dangote, when he welcomed the Minister of State for Industry, Mr John Owan Enoh, to the Dangote Petroleum Refinery and Petrochemicals in Lagos recently.

The business mogul noted that efforts must be made to place industrialisation at the centre of the government’s economic strategy, insisting that no nation has attained prosperity without a strong manufacturing base.

“If Nigeria is to achieve sustainable growth and become a trillion-dollar economy, industrialisation must be the foundation. Indigenous investors remain the strongest catalysts for that transformation,” Mr Dangote stated.

He further stated that, “There is no way to create jobs and prosperity without industrialisation,” declaring that, “The greatest attraction for foreign investors is the success of domestic investors. When local investors thrive, they send a powerful signal that the environment is conducive for investment.”

In his remarks, the Minister promised deeper collaboration with the private sector to accelerate industrialisation, job creation and economic transformation.

He also pledged that the Ministry and its agencies would remain strong advocates of the refinery and the broader industrialisation agenda, adding that the government would continue to engage Dangote Industries Limited through the Industrial Revolution Work Group and ministerial roundtables to address challenges facing manufacturers, particularly access to affordable long-term financing.

Mr Enoh described the integrated industrial complex as one of the most significant investments in Africa and a model for the type of industrial development required to drive Nigeria’s economic growth aspirations.

“This facility matters because of what it represents for Nigerian industry, for our people and for the realisation of President Bola Tinubu’s vision of a one trillion-dollar economy,” he stated, noting that the refinery has emerged as a powerful symbol of value addition, industrial competitiveness and Nigeria’s growing manufacturing capability.

The Minister noted that the refinery has fundamentally changed global perceptions of Nigeria by helping to transform the country from a major importer of refined petroleum products into an exporter serving international markets.

“When global supply disruptions occurred, Nigeria was able to export petroleum products to markets in the Middle East and beyond. That is an extraordinary achievement and one that deserves recognition,” he added.