Economy

Global Crude Oil Market Regains Strength After Trump’s Speech

By Adedapo Adesanya

The oil markets wrapped up its worst week in 12 years with a marginal recovery on Friday. During the week, the market witnessed crash in prices of the commodity and an expected increase in production.

The Brent fell in the week by over 24 percent, the biggest weekly loss for the commodity since the 2008 global financial crisis, while the WTI registered a 23 percent drop.

But on Friday night, the Brent crude futures gained 0.73 percent or 23 cents to trade at $35.44 per barrel, while its US West Texas Intermediate (WTI) crude counterpart registered a 24 cents or 0.68 percent growth to sell at $31.73 per barrel.

On Wednesday, President of the United States, Mr Donald Trump, banned foreign travels mostly from European countries into America and last night, he declared a national emergency for the coronavirus, which has nearly shutdown global economy.

The US President’s speech contained some pointers that boosted the confidence of a waning market, even by a little.

According to Mr Trump, the US government will buy large quantities of crude for the Strategic Petroleum Reserve, mentioning that this would save the taxpayer billions of dollars, while helping out the oil industry, and working towards the goal of energy independence.

Prices crashed on Monday by over 25 percent when Saudi Arabia placed discounts on all its crude grades, leading an already affected market into a more dangerous territory. This move was taken after a plan to cut oil production by 1.5 million barrels with Russia did not work.

The Kingdom, Russia, and the United Arab Emirates have also made intentions known that when the current deal of 1.7 million barrels per day cut made by the Organisation of the Petroleum Exporting Countries and its allies (OPEC+) expires on March 31, they will increase output as part of plans to capture their own market share.

Saudi Arabia is looking to increase its daily production to 13 million barrels per day, while the UAE national oil company, ADNOC, said it would raise crude supply to more than four million barrels per day in April and would accelerate plans to boost its capacity to five million barrels per day, a target it previously planned to achieve by 2030.

The extra oil the two Gulf allies plan to add is equivalent to 3.6 percent of global supplies and will pour into the market at a time when global fuel demand in 2020 is waning.

According to forecast by OPEC, global oil demand is expected to rise by 60,000 barrels per day in 2020 after it has slashed its forecasts by 920,000 barrels per day in February.

The International Energy Agency (IEA) also noted that oil demand was set to drop this year for the first time since the financial crisis due to the coronavirus outbreak and its impact on economies. The IEA now sees global oil demand falling by 90,000 barrels per day, in 2020.

By Modupe Gbadeyanka

The Lagos-based Dangote Petroleum Refinery has been described by Standard Bank Group as a transformational industrial project with far-reaching implications for Nigeria and Africa.

The company, which is Africa’s largest financial institution, gave this description after a tour of the facility recently.

Standard Bank, the parent company of Stanbic IBTC Holdings, has promised to support the planned listing of the 650,000 barrels per day refinery and expressed readiness to finance future expansion projects across the continent.

The chief executive of the lender, Mr Sim Tshabalala, said, “We are here because the Dangote Group is a large and important global player and a significant force on the African continent.”

“Standard Bank is the largest financial institution in Africa, and we have partnered with Dangote on a variety of initiatives. We are here to lend support, to see this magnificent refinery and to discuss Vision 2030 and how we can continue supporting the Group’s growth ambitions,” he added.

Mr Tshabalala disclosed that Standard Bank intends to play a leading role in the refinery’s planned Initial Public Offering and future growth initiatives.

“As Dangote lists, there is an IPO coming up, and we are a leading player in that process,” he said, adding that, “As the group continues to expand in Nigeria and across Africa, there will be opportunities for financial advisory services and balance sheet support, and we stand ready to provide both.”

He further described the refinery as “a wonder of the world,” noting that its impact is already being felt through stronger foreign exchange earnings, improved balance-of-payments performance and enhanced energy security.

“This is a wonder to behold. It is massive, productive and transformative. It is already making a significant contribution to Nigeria’s economy through its impact on foreign reserves, the balance of payments and the lives of ordinary Nigerians,” he said.

The Group Vice President for Oil and Gas at Dangote Industries Limited, Mr Devakumar Edwin, said the visit represented a significant milestone in a partnership that began during the refinery’s construction phase.

“The bank visited us during construction and understood the scale of what we were building,” Mr Edwin said. “Today, the refinery is fully operational, and they can see what their support has helped to create. It is like nurturing a tree and eventually seeing it bear fruit.”

He added that both organisations are exploring opportunities to deepen collaboration as Dangote expands its industrial footprint across Africa.

Also speaking, the chief executive of Dangote Petroleum Refinery, Mr David Bird, said the visit highlighted the importance of long-term partnerships in delivering large-scale industrial projects.

“Standard Bank has been one of our strongest supporters throughout the history of the refinery and the broader Dangote Group.

“This visit was an opportunity to demonstrate what that support has enabled. Seeing is believing, and it allows our partners to appreciate the scale of what has been achieved,” Mr Bird stated.

The visit also coincided with a major operational milestone for the refinery, which has now exceeded its original design capacity.

Mr Bird disclosed that the refinery recently completed performance test runs at 700,000 barrels per day, above its nameplate capacity of 650,000 barrels per day.

“We have always believed there was engineering flexibility built into the design,” he said. “Achieving sustained production of 700,000 barrels per day is a testament to the technical capability of our people and the strength of the systems we have built.”

By Adedapo Adesanya

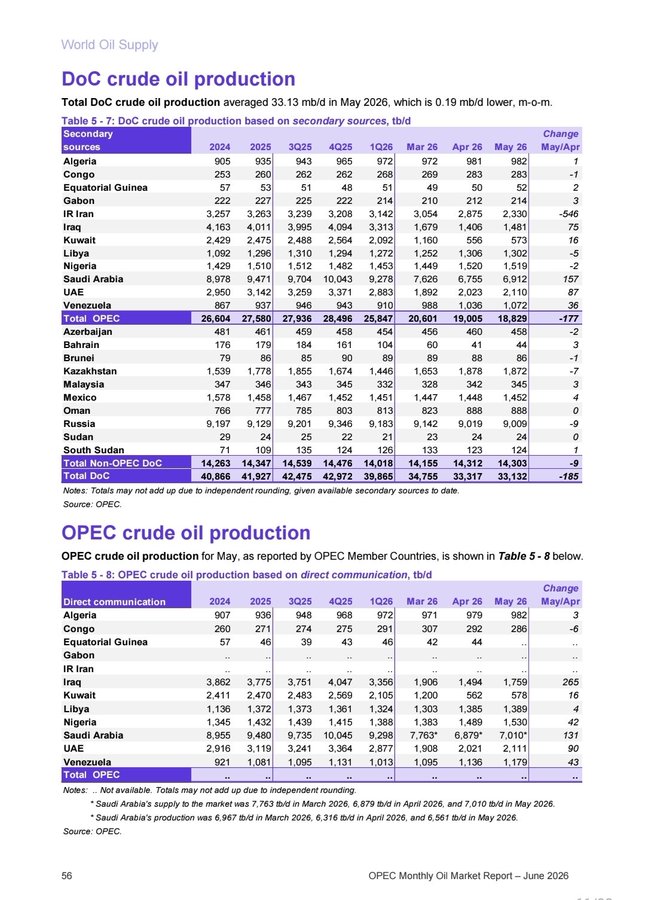

Nigeria produced about 1.530 million barrels of crude oil per day in May 2026, beating its Organisation of Petroleum Exporting Countries (OPEC) quota by 42,000 barrels per day. In the preceding month, the country only produced 1.489 million barrels per day.

In the latest OPEC’s Monthly Oil Market Report (MOMR), it was also revealed that Iraq in April supplied 1.494 million barrels per day while in May, it produced 1.759 million barrels per day, an increase 265,000 barrels per day; Saudi Arabia, 6.879 million barrels per day in April, 7.010 million barrels per day in May, an increase of 131,000 barrels per day; United Arab Emirate (UAE), 2.021 million barrels per day in April and in May 2.111 million barrels per day, an increase of 90,000 barrels per day while Venezuela, 1.136 million barrels per day in April and 1.179 million barrels per day in May, an increase of 43,000 barrels per day.

Using secondary sources, Nigeria’s production decreased from 1.520 million barrels per day in April to 1.519 million barrels per day; Saudi Arabia, 6.755 million barrels per day in April and 6.912 million barrels per day in May; UAE, 2.023 million barrels per day in April, 2.110 million barrels per day in May; and Venezuela, 1.036 million barrels per day in April and 1.072 million barrels per day in May.

Nigerian Upstream Petroleum Regulatory Commission (NUPRC), in a statement by its Head, Media and Corporate Communications, Mr Eniola Akinkuotu, confirmed that Nigeria, in May, met 102 per cent of OPEC quota as production hit an 11-month high.

According to it, Nigeria’s oil production witnessed an upswing in May 2026, averaging 1,530,354 barrels of crude oil and 170,446 barrels of condensates per day, bringing the total combined production to 1, 700, 800 barrels per day and consolidating Nigeria’s position as Africa’s largest oil producer.

It stated that the average crude oil production recorded in May represents 102 per cent of Nigeria’s 1.5mbpd of production quota allocated by OPEC.

It explained that production performance during the review period remained robust, with combined crude oil and condensate output ranging between a low of 1.51 million barrels per day and a peak of 1.86 million barrels per day.

The organisation added that the May 2026 production figures represented the highest recorded by Nigeria since July 2025, when output surged to 1,712,282.

NUPRC said: “In strict crude oil terms (excluding condensates), the 1.53 million barrels recorded in May 2026 represents the highest Nigeria has witnessed since January 2025 when crude oil production hit 1.538 mbpd.”

“On a month-on-month basis, production rose by 2.77 per cent in May 2026 as against 1.48mbpd in April. The broader production trend over the last five months has also remained positive.

“Combined crude oil and condensate output increased from 1.48 mbpd in February to 1.54 mbpd in March, 1.66 mbpd in April, and then 1.7 mbpd in May, underscoring sustained growth in Nigeria’s hydrocarbon production levels.

“Among production streams, Bonny Terminal led the pack with a total blend of 293,870 bpd, closely followed by Forcados Terminal at 289,900 bpd. Qua Iboe ranked third with 173,360 bpd, while Escravos Oil Terminal contributed 135,470 bpd. Odudu (Amenam Blend) completed the top five production streams, accounting for 63,250 bpd during the month under review.”

The commission attributed the rise in production to a sustained positive momentum as operations remained stable throughout the reporting period with no significant pipeline or facility outages recorded.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange broke a three-day losing streak after it gained 1.04 per cent on Thursday, June 11, on the back of a strong showing by Central Securities Clearing System (CSCS) Plc.

The Nigerian securities depository company recorded a N5.61 growth during the session to finish at N83.93 per share compared with the previous day’s N78.32 per share.

The rise in the share price of the company overpowered the losses printed by three other securities at the close of business.

Consequently, the market capitalisation of the trading platform went up by N26.68 billion to N2.617 trillion from N2.590 trillion, and the NASD Unlisted Security Index (NSI) closed higher by 44.89 points to 4,375.01 points from 4,330.12 points.

Yesterday, Nitrox Industrial Gases Plc declined by N2.38 to N21.48 per unit from N23.80 per unit, UBN Property Plc went down by 13 Kobo to N1.98 per share from N2.11 per share, and MRS Oil Plc dropped 10 Kobo to close at N158.00 per unit, in contrast to Wednesday’s closing price of N158.10 per unit.

The volume of securities transacted by investors during the session significantly went up by 2,558.6 per cent to 3.1 million units from 117,374 units, and the value of securities traded improved by 463.1 per cent to N68.5 million from the preceding session’s N12.2 million, while the number of deals moderated by 37.2 per cent to 27 deals from 43 deals.

At the close of business, Great Nigeria Insurance (GNI) Plc was the most traded stock by value on a year-to-date basis, with 3.4 billion units traded for N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units transacted for N6.5 billion, and CSCS Plc with 65.9 million units sold for N4.5 billion.

GNI Plc remained the most traded stock by volume on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, followed by Infracredit Plc with 2.3 billion units valued at N6.5 billion, and Resourcery Plc with 1.1 billion units worth N415.7 million.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn