Economy

Africa’s Economy to Rebound 5% in 2021—ECA

By Adedapo Adesanya

The economy of Africa is expected to rebound by 5 per cent next year after declining by 4.1 per cent this year, the UN Economic Commission for Africa (ECA) has said in its new report.

In its report tagged Innovative finance for private sector development in Africa, it was stated that the recovery would be supported by effective response to the COVID-19 pandemic and the measures taken globally to aid economic recovery.

According to the report, imported pharmaceutical products in the middle of a pandemic worth $44 billion would be required for the testing, personal protective equipment for frontline medical staff, equipment and treatment of the coronavirus (COVID-19).

In 2020, spending on health will increase as governments set aside funds to sustain their health systems and absorb costs related to the COVID-19 lockdowns.

In a best-case scenario, $44 billion would be required across Africa for testing, personal protective equipment and treatment of COVID-19 patients requiring hospitalisation and intensive care treatment, the report said.

The report further said that due to the resources being redirected to COVID-19, Africa’s existing health challenges will face spillover costs, as happened in the Ebola crisis. It calls on countries to look into investments in non-COVID-19 health issues which should be kept in view.

The impact of the pandemic will push between 5 million and 29 million people below the extreme poverty line of $1.90 per day, compared with a baseline 2020 African growth scenario, according to ECA projections.

Moreover, reduced demand due to COVID-19 has depressed the prices of agricultural commodities such as coffee, tea and cocoa, which is expected to affect vulnerable small-scale farmers in Africa.

The report advocates for investment to build key infrastructure and foster innovation. Despite Africa’s growth, many economies remain unsophisticated or undiversified, due to low levels of innovation, limited productive capabilities, low investment and poor quality of education.

Building capabilities will require investments in human and physical capital.

The report projected that an estimated financing gap of $2.5 trillion will be for all emerging and developing countries and $200 billion– $1.3 trillion for Africa.

This is because Africa’s population is expected to grow by 43 per cent over 2015–2030, the gap could reach $19.5 trillion by 2030.

Meanwhile, climate change is increasing seasonal variability, frequency and intensity of droughts and floods, and shifting habitats and agro-ecological zones due to climate change can cause food insecurity, lower trade balances, raise inflation pressure and fiscal imbalances.

For instance, cyclone Idai, which hit Mozambique in March–April 2019, weakened the economy, took 1,000 lives and caused $700 million–$1 billion in damages to property and other losses.

African economies remained the second fastest-growing region in the world with growth estimated at 3.4 per cent in 2019. The COVID-19 pandemic will impact growth to decelerate to between 1.8 per cent and -4.1 per cent in 2020.

In order to promote the recovery from the COVID-19 impact, the report calls on African countries to regulate their bank sector to limit the possible harm from banking crises or from more general system-wide misallocation of resources.

For the sake of private sector development, the regulation of banks and other sources of capital for funding private industry, such as equity and debt capital markets and digital platforms, needs to be strengthened.

The report noted that the regulations that concern the banking sector alone may be insufficient to safeguard the financial system against some of the risks fintech services pose, such as data privacy, money laundering, mismatched risk and return, and systemic risk.

Africa needs to rethink its financial services regulation so that innovation is fully functional, the environment enables innovation, transparency is enhanced, and financing for private sector development is delivered, the report stated.

These new risks call for financial regulation to be reviewed to provide a flexible environment for fintech to develop that is strict enough to limit the risks. Some African countries have limited fiscal space and international reserves and thus lack the necessary resources to implement COVID-19 responses.

According to IMF data, African countries will record fiscal deficits averaging 5.8 per cent in 2020 and 4.4 per cent in 2021, compared with 3 per cent in 2019.

However, African policymakers’ and regulators’ experience with the 2008–2009 financial crisis and the use of various measures to cushion its impact give them an advantage in rapidly responding to the COVID-19 crisis.

By Aduragbemi Omiyale

The Global Banking and Finance Review has named Stanbic IBTC Capital, a subsidiary of Stanbic IBTC Holdings, as the Best Investment Bank in Nigeria for 2026.

The leading financial publication picked Stanbic IBTC Capital for the honour in recognition of its commitment to leadership and excellence in Nigeria’s investment banking sector.

The selection process involves an extensive evaluation of performance across critical metrics, including innovation, client service, financial health, and industry advancement.

Stanbic IBTC Capital’s accolade reflects its strong dedication to delivering capital markets and financial advisory solutions for clients in both the public and private sectors.

The firm has made significant strides in facilitating groundbreaking transactions, offering market-leading expertise in equity, debt, and structured finance, while nurturing the growth ambitions of businesses and institutions across Nigeria.

“We are truly pleased to be acknowledged for our relentless pursuit of excellence in the investment banking arena.

“This honour reflects our commitment to hard work and further establishes the deep trust our clients have in our expertise and service.

“It further motivates us to maintain our dedication to exceptional service, cultivate impactful partnerships, and continue delivering innovative financial solutions that meet our clients’ aspirations,” the chief executive of Stanbic IBTC Capital, Mr Oladele Sotubo, stated.

The Executive Director of Corporate and Transaction Banking at Stanbic IBTC Bank, Mr Eric Fajemisin, on his part, said, “Receiving this esteemed acknowledgement from the Global Banking and Finance Review Awards underscores our commitment to driving innovation and excellence within Nigeria’s investment banking landscape.

“This accolade highlights the significant role our skilled team plays in fostering economic growth and stability.

“We are dedicated to delivering exceptional value to our clients, which not only supports their financial success but also contributes to the broader development of the nation’s financial ecosystem.”

The Global Banking and Finance Review annually celebrates institutions that demonstrate quality, innovation, and contributions to the advancement of banking and financial services worldwide.

Now in its 16th edition, the awards honour organisations that uphold outstanding service standards, strategic execution, and industry leadership.

By Aduragbemi Omiyale

The Governor of Rivers State, Mr Siminalayi Fubara, has presented the 2026 Appropriation Bill to the Rivers State House of Assembly.

The 2026 budget estimate of N1.85 trillion, christened Budget of Resilience for Growth and Development, was presented to the state parliament on Friday.

Mr Fubara stated that the proposed spending for the 2026 fiscal year represents a 24.49 per cent increase over the adjusted 2025 budget, driven by anticipated growth in Federation Account Allocation Committee (FAAC) allocations, derivation revenue and internally generated revenue.

He informed the lawmakers that the state hopes to earn N487.61 billion from internally generated revenue, N936.05 billion from FAAC allocations, derivation funds, Value Added Tax (VAT) and exchange gains, and N382.48 billion from capital receipts, including loans, grants and asset sales.

According to him, N413.11 billion is for recurrent expenditure and N1.405 trillion for capital projects, underscoring his administration’s commitment to accelerating development across the state.

He added that personnel costs would gulp N154.77 billion, while N15.22 billion would fund new recruitments, stating that the budget also provides for pensions, gratuities, death benefits and debt servicing.

Governor Fubara further proposed a 50 per cent increase in overhead expenditure for Ministries, Departments and Agencies (MDAs) to strengthen their operational capacity immediately after the budget is signed into law.

He also stated that the largest allocation under the capital budget is the Works and Infrastructure sector with N533.32 billion, followed by Education with N315 billion and Healthcare with N105.43 billion.

In addition, N41.44 billion is for the Rivers State House of Assembly, N30 billion for the Judiciary, N19.26 billion for Agriculture, N15 billion for Power, N8.5 billion for Chieftaincy and Community Development, N7.98 billion for Sports, N7 billion for Youth Development, N6.5 billion for Women Affairs, and N6.61 billion for Environment and Sustainable Development.

The Governor noted that the budget was designed to sustain economic growth, expand critical infrastructure and improve the welfare of residents, pointing out that it builds on the achievements of his administration despite the challenges experienced by the state.

According to him, the budget prioritises the completion of ongoing road projects, new infrastructure investments, improved education and healthcare services, job creation and expanded economic opportunities for residents.

Describing the proposal as a people-centred budget, he assured Rivers people that every public fund would be judiciously utilised to deliver quality services, attract investment and stimulate inclusive development.

Mr Fubara acknowledged the delayed presentation of the budget and appealed to members of the House of Assembly to give the appropriation bill speedy consideration and passage to facilitate timely implementation.

In his remarks, the Speaker of the Rivers State House of Assembly, Mr Martin Amaewhule, acknowledged that the 2026 Appropriation Bill was presented later than expected but assured the Governor that the legislature would expedite its consideration in the interest of the people of Rivers State.

By Adedapo Adesanya

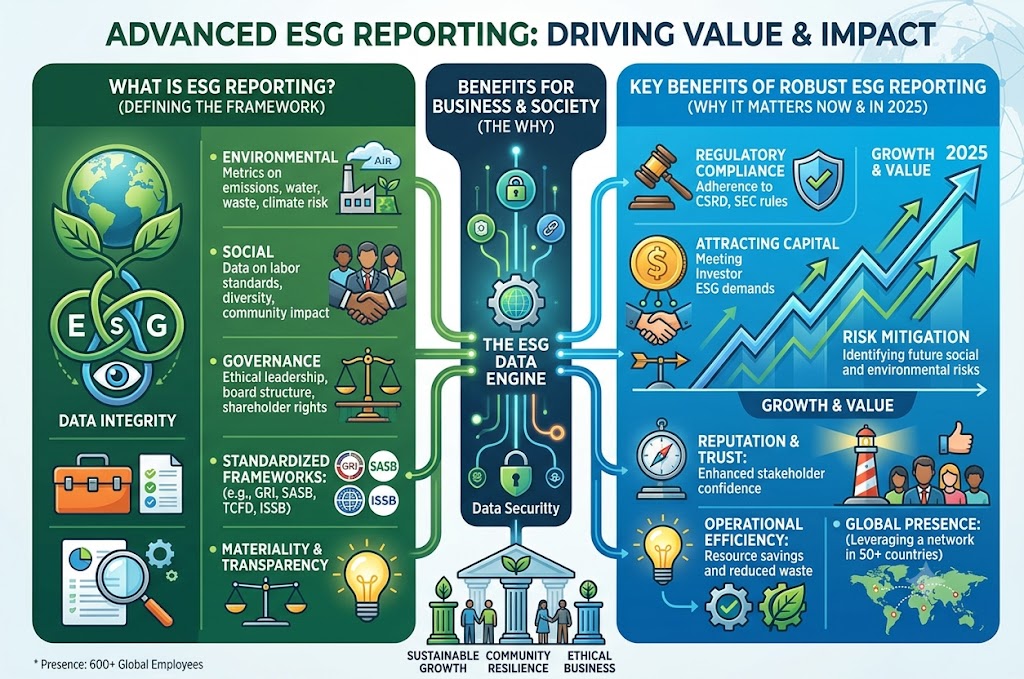

The Securities and Exchange Commission (SEC) has unveiled plans to make sustainability reporting mandatory for large public interest entities from 2027.

This comes as Nigeria moves to align its corporate disclosure framework with global environmental, social and governance (ESG) reporting standards.

The phased implementation will begin with voluntary adoption by early adopters and large public interest entities before becoming mandatory in 2027. The requirement will extend to other public interest entities in 2028 and small and medium-scale enterprises (SMEs) by 2030.

The Director-General of the SEC, Mr Emomotimi Agama, disclosed this at the 2026 Financial Institutions Training Centre (FITC) Sustainability and ESG Conference 3.0, themed ‘Building a Sustainable Africa: Integrating Environmental Stewardship, Social Investment, and Strong Governance for a Prosperous Future’ in Lagos.

Mr Agama said Nigeria’s sustainability disclosure regime is being aligned with the International Sustainability Standards Board (ISSB) framework, including IFRS S1 and IFRS S2, which have emerged as the global benchmark for sustainability reporting.

He said that institutional investors increasingly consider ESG performance a key determinant of capital allocation rather than a peripheral corporate responsibility issue, noting that the price of entry is disclosure.

He said the reforms would strengthen investor confidence and position Nigerian businesses to access global capital markets, where sustainability disclosures are becoming an essential investment requirement.

According to him, Nigeria’s capital market has recorded significant expansion, with market capitalisation growing from about N130 trillion to nearly N160 trillion following recent market reforms, while assets under management have surpassed N9 trillion.

To deepen sustainable finance, Agama said the commission was promoting infrastructure, green and municipal bonds, alongside infrastructure-focused investment funds, to mobilise long-term capital for critical national projects.

He added that the commission would also encourage investments in the blue economy and support financing for the power sector through green energy bonds, project bonds and public-private investment structures.

The SEC chief cited the recent launch of the Nigerian Exchange (NGX) Impact Board as another milestone in advancing sustainable finance and urged companies, regulators and investors to move beyond commitments by embedding sustainability into governance, operations and investment decisions.