Economy

Impact of COVID-19 on Debt Capital Markets in Africa

Traditionally, corporates and states in Africa use debt capital markets to raise huge funding. As the coronavirus bites harder against the increasing debt-to-GDP ratios coupled with increasing risks in African countries, the pricing of new issuances in the international debt capital markets became relatively unattractive.

Consequently, African governments turned to other concessionary sources like the International Monetary Fund (IMF), World Bank and Development Finance Institutions for funding.

Africa’s depiction of the international debt capital markets is dominated by sovereign issuances. While its debt capital markets offer investors better returns than in developed markets, its domestic markets remain shallow and least diversified compared to other emerging and frontier markets. Also, African corporates are less likely to raise substantial amounts of funding via debt capital markets due to various reasons including lack of depth in the domestic markets and institutional weaknesses.

Between 2014 and 2018, sovereign bonds accounted for 51.5 per cent of the total $140.3 billion raised from 437 international bond transactions in Africa. Within 2016 and 2018, African issuers raised about $120 billion of non-local currency debt which further culminated to $245.9 billion of non-local currency debt from 759 issues within the last decade. The largest sovereign issuer of non-local currency debt in 2019 was Egypt raising $8.2 billion. Next to Egypt is South Africa which raised $5 billion in September of the same year from its largest-ever Eurobond issuance.

However, in 2020, the effect of COVID-19 impacted the African economy resulting in a pullback from African markets as countries faced crisis on all levels including health and social services. These unprecedented shocks call for a temporary debt standstill for all African countries as economic fundamentals deteriorated. A 2020 study on the economic impact of COVID-19 by the African Union (AU) showed that while countries in Africa could lose up to $500 billion, they may be forced to borrow heavily to survive after the pandemic, hence the need for the debt standstill—suspension of debt service.

For example, Mozambique’s debt overtook its overall economic output as its debt-to-GDP ratio, which was 100 per cent in 2018 billowed to 130 per cent in 2020; even as the country struggles to repay its $14 billion external debt. Asides from Mozambique, there are other poor and highly indebted African countries with little fiscal space to provide a robust response and recovery from the pandemic. Some of these countries like Angola, Djibouti, Congo, Cabo Verde, and Egypt have a higher than 100 per cent external debt-to-GDP ratio, yet, they still seek more funds.

Consequently, the G-20 agreed to suspend debt repayment for the world’s 75 poorest countries until the end of 2020. UN Secretary-General António Guterres further advised that debt suspension should be extended to all developing countries, while the UN Economic Commission for Africa (ECA) recommended a complete temporary debt standstill for two years for all African countries, without exception.

Over the years, there have been calls by multilateral institutions for debt forgiveness for Africa’s most impoverished states. However, some experts opine that such cancellation or debt standstill would be perceived as a default in today realities of the international capital markets and will greatly compromise the future access of African countries to international markets. For example, states like Benin and Ghana which were able to access capital markets over the past year at 5.75 per cent for 7 years (€500 million) and 8.875 per cent for 40 years ($750 million) respectively might find it difficult to do so if they are perceived to be in default. On the other hand, perception of default would likely also be priced into future borrowings by African countries.

Following the above, in April 2020, China, which accounts for most of the lending to African countries through its China Development Bank and the Export-Import Bank of China, expressed a willingness to provide Africa debt relief, but not forgiveness. In June, China offered to cancel Africa’s interest-free loans, which is less than 5 per cent of Africa’s debt to China, based on bilateral negotiations.

With the already rising value of the total public debts in many African countries, to combat the prevailing crisis of the coronavirus, some African countries opted for multilateral financing. One of such countries is Nigeria. The country, in the second quarter of 2020, requested $6.9 billion of multilateral financing from the International Monetary Fund (IMF), World Bank and African Development Bank (AfDB) to minimise the impact of the upsurge of the global pandemic.

Source: NBS

Part of these funds was to establish a $1.2 billion COVID-19 crisis intervention fund to upgrade healthcare facilities across the country and to provide intervention funds to the 36 states including the Federal Capital Territory (FCT).

Similarly, against the backdrop of the pandemic, the African Union launched several programmes, like the African Union Development Agency (AUDA-NEPAD) COVID-19 Response Plan to help countries fight the pandemic and recover better. Using Nigeria as a case study, activities in the domestic bond market significantly increased year-on-year given the relatively low yields in the market. In H1 2020, seven corporate bond issuances were raised to the tune of N152.7 billion compared to N54 billion raised in three issuances in the corresponding period of the previous year.

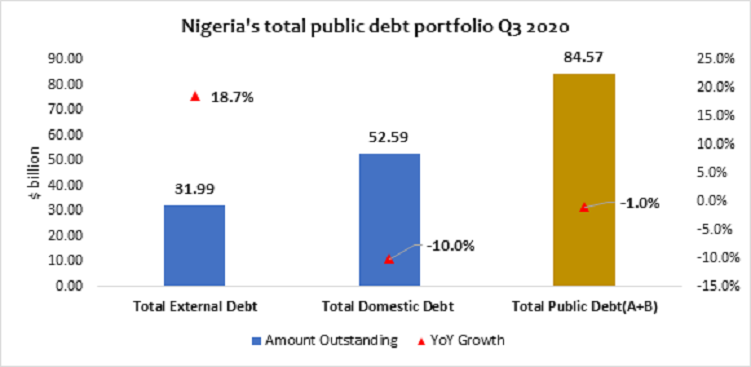

According to the data by the Debt Management Office (DMO), the nation’s debt stock data at the third quarter (Q3) 2020 showed that the total public debt portfolio of the federal and state government combined stood at N32.22 trillion ($84.57 billion), an increase of 22.9 per cent but a decrease of 1 per cent in dollar equivalent due to the different exchange rate values within the periods.

Nigeria’s total public debt showed that $31.99 billion (or 37.82 per cent of the debt) was external while $52.59 billion (or 62.18 per cent of the debt) was domestic. Further disaggregation of Nigeria’s foreign debt showed that $16.74 billion of the debt was multilateral; $502.38 million was bilateral (AFD) and another $3.26 billion bilateral from the Exim Bank of China, JICA, India, and KFW while $11.17 billion was commercial which are Eurobonds and Diaspora Bonds.

The debt conundrum leaves Africa in a dilemma considering the rising budget deficits coupled with the need to fund the deficits. If Africa is to stop depending on donors and multilateral funds to finance its economic development, it needs to evolve towards market-based financing for the quantum of financing required. In addition, African countries need to promote market-friendly policies that will attract capital to underserved sectors and allow the states to focus its limited financing on priority sectors such as education, health, and social services.

By Adedapo Adesanya

Four securities weakened the NASD Over-the-Counter (OTC) Securities Exchange by 1.95 per cent on Friday, erasing N41.17 billion from the bourse, which had its market capitalisation at N2.567 trillion compared with the previous session’s N2.618 trillion.

In the same vein, the NASD Unlisted Security Index (NSI) decreased at the close of business by 85.28 points to 4,277.07 points from 4,362.32 points.

The price decliners were led by 11 Plc, which gave up N20.50 to sell at N200.50 per share compared with the preceding day’s N221.00 per share, FrieslandCampina Wamco Nigeria Plc dropped N16.94 to close at N155.20 per unit versus Thursday’s closing price of N172.14 per unit, Central Securities Clearing System (CSCS) Plc went down by N2.11 to N84.68 per share from N86.79 per share, and Afriland Properties Plc lost 11 Kobo to end at N16.74 per unit, in contrast to the N16.85 per unit it closed a day earlier.

During the trading day, the value of transactions jumped by 172.1 per cent to N29.9 million from the preceding session’s N10.9 million, and the volume of trades soared by 136.5 per cent to 955,096 units from the previous 403,901 units, while the number of deals went down by 11.4 per cent to 31 deals from 35 deals.

Great Nigeria Insurance (GNI) Plc remained the most active stock by value on a year-to-date basis, with 3.4 billion units valued at N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units worth N6.5 billion, and CSCS Plc with 68.6 million units sold for N4.7 billion.

GNI Plc also ended the session as the most traded stock by volume on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, trailed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units transacted for N415.7 million.

By Dipo Olowookere

The last trading session of this week on the floor of the Nigerian Exchange (NGX) Limited ended on a negative note, with a 0.66 per cent loss on Friday.

This was influenced by sustained selling pressure and cautious trading, which forced investors into profit-taking.

Data obtained by Business Post showed that the energy sector fell by 4.66 per cent, the insurance counter dipped by 2.23 per cent, the consumer goods index depreciated by 0.96 per cent, and the banking segment shed 0.28 per cent, while the industrial goods space remained unchanged.

At the close of business, the All-Share Index (ASI) of Nigeria’s stock exchange went down by 1,531.81 points to 232,049.02 points from 233,580.83 points, and the market capitalisation dropped N983 billion to settle at N148.905 trillion compared with Thursday’s N149.888 trillion.

Aradel was the worst-performing equity after it lost 10.00 per cent to close at N1,417.50. International Energy Insurance slipped by 9.95 per cent to N5.79, Trans-Nationwide Express depreciated by 9.89 per cent to N3.28, eTranzact crashed by 9.79 per cent to N14.75, and UPDC slumped by 9.72 per cent to N28.12.

The best-performing equity for the day was Universal Insurance, which gained 6.32 per cent to close at N1.01, McNichols grew by 5.52 per cent to N8.60, Linkage Assurance expanded by 4.67 per cent to N1.57, NGX Group appreciated by 4.35 per cent to N120.00, and Transcorp increased by 3.62 per cent to N41.50.

As look at the activity level indicated that investors traded 388.7 million stocks worth N18.4 billion in 44,631 deals compared with the 393.7 million stocks valued at N19.2 billion executed in 45,813 deals a day earlier, representing a decline in the trading volume, value, and number of deals by 1.27 per cent, 4.17 per cent, and 2.58 per cent, respectively.

By Adedapo Adesanya

The Naira recorded a loss of 82 Kobo or 0.06 per cent against the United States Dollar in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Friday, June 26, exchanging at N1,380.93/$1, in contrast to the previous day’s rate of N1,380.11/$1.

Equally, the domestic currency further weakened against the Pound Sterling in the official FX market yesterday by N6.06 to settle at N1,824.90/£1 versus the preceding session’s N1,818.84/£1, and lost N10.74 on the Euro to sell at N1,577 .58/€1 versus N1,566.84/€1.

At the GTBank forex counter, the Naira depreciated against the greenback during the session by N4 to close at N1,387/$1, in contrast to Thursday’s value of N1,383/$1, and at the parallel market, it was unchanged at N1,395/$1.

Interbank FX activity among financial institutions has fluctuated amid a sharp slowdown in forex market interventions by the Central Bank of Nigeria (CBN), as it allows demand and supply to move the market.

Also, a stronger greenback has generally put significant pressure on emerging-market currencies.

Nigeria has accessed the first tranche of a proposed $5 billion derivatives financing arrangement with First Abu Dhabi Bank PJSC, the largest lender in the United Arab Emirates (UAE).

The $5 billion facility, approved by the National Assembly earlier this year, is part of the federal government’s plan to diversify external financing sources and reduce borrowing costs. Structured as a Total Return Swap with First Abu Dhabi Bank, proceeds are earmarked for refinancing debt and supporting infrastructure financing.

If the proceeds are brought into the country through the official FX market, the transaction will increase the currency reserves or Dollar liquidity.

At the cryptocurrency market, Solana (SOL) grew by 2.2 per cent to $71.92, Cardano (ADA) gained 1.1 per cent to trade at $0.1474, Ripple (XRP) also appreciated by 1.1 per cent to $1.05, Dogecoin (DOGE) expanded by 0.9 per cent to $0.0755, and Ethereum (ETH) improved by 0.4 per cent to $1,578.84.

On the flip side, TRON (TRX) slid 0.6 per cent to $0.3203, Binance Coin (BNB) slumped by 0.3 per cent to $564.33, and Bitcoin fell by 0.2 per cent to $60,219.37, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) traded flat at $1.00 each.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn