Economy

Impact of COVID-19 on Debt Capital Markets in Africa

Traditionally, corporates and states in Africa use debt capital markets to raise huge funding. As the coronavirus bites harder against the increasing debt-to-GDP ratios coupled with increasing risks in African countries, the pricing of new issuances in the international debt capital markets became relatively unattractive.

Consequently, African governments turned to other concessionary sources like the International Monetary Fund (IMF), World Bank and Development Finance Institutions for funding.

Africa’s depiction of the international debt capital markets is dominated by sovereign issuances. While its debt capital markets offer investors better returns than in developed markets, its domestic markets remain shallow and least diversified compared to other emerging and frontier markets. Also, African corporates are less likely to raise substantial amounts of funding via debt capital markets due to various reasons including lack of depth in the domestic markets and institutional weaknesses.

Between 2014 and 2018, sovereign bonds accounted for 51.5 per cent of the total $140.3 billion raised from 437 international bond transactions in Africa. Within 2016 and 2018, African issuers raised about $120 billion of non-local currency debt which further culminated to $245.9 billion of non-local currency debt from 759 issues within the last decade. The largest sovereign issuer of non-local currency debt in 2019 was Egypt raising $8.2 billion. Next to Egypt is South Africa which raised $5 billion in September of the same year from its largest-ever Eurobond issuance.

However, in 2020, the effect of COVID-19 impacted the African economy resulting in a pullback from African markets as countries faced crisis on all levels including health and social services. These unprecedented shocks call for a temporary debt standstill for all African countries as economic fundamentals deteriorated. A 2020 study on the economic impact of COVID-19 by the African Union (AU) showed that while countries in Africa could lose up to $500 billion, they may be forced to borrow heavily to survive after the pandemic, hence the need for the debt standstill—suspension of debt service.

For example, Mozambique’s debt overtook its overall economic output as its debt-to-GDP ratio, which was 100 per cent in 2018 billowed to 130 per cent in 2020; even as the country struggles to repay its $14 billion external debt. Asides from Mozambique, there are other poor and highly indebted African countries with little fiscal space to provide a robust response and recovery from the pandemic. Some of these countries like Angola, Djibouti, Congo, Cabo Verde, and Egypt have a higher than 100 per cent external debt-to-GDP ratio, yet, they still seek more funds.

Consequently, the G-20 agreed to suspend debt repayment for the world’s 75 poorest countries until the end of 2020. UN Secretary-General António Guterres further advised that debt suspension should be extended to all developing countries, while the UN Economic Commission for Africa (ECA) recommended a complete temporary debt standstill for two years for all African countries, without exception.

Over the years, there have been calls by multilateral institutions for debt forgiveness for Africa’s most impoverished states. However, some experts opine that such cancellation or debt standstill would be perceived as a default in today realities of the international capital markets and will greatly compromise the future access of African countries to international markets. For example, states like Benin and Ghana which were able to access capital markets over the past year at 5.75 per cent for 7 years (€500 million) and 8.875 per cent for 40 years ($750 million) respectively might find it difficult to do so if they are perceived to be in default. On the other hand, perception of default would likely also be priced into future borrowings by African countries.

Following the above, in April 2020, China, which accounts for most of the lending to African countries through its China Development Bank and the Export-Import Bank of China, expressed a willingness to provide Africa debt relief, but not forgiveness. In June, China offered to cancel Africa’s interest-free loans, which is less than 5 per cent of Africa’s debt to China, based on bilateral negotiations.

With the already rising value of the total public debts in many African countries, to combat the prevailing crisis of the coronavirus, some African countries opted for multilateral financing. One of such countries is Nigeria. The country, in the second quarter of 2020, requested $6.9 billion of multilateral financing from the International Monetary Fund (IMF), World Bank and African Development Bank (AfDB) to minimise the impact of the upsurge of the global pandemic.

Source: NBS

Part of these funds was to establish a $1.2 billion COVID-19 crisis intervention fund to upgrade healthcare facilities across the country and to provide intervention funds to the 36 states including the Federal Capital Territory (FCT).

Similarly, against the backdrop of the pandemic, the African Union launched several programmes, like the African Union Development Agency (AUDA-NEPAD) COVID-19 Response Plan to help countries fight the pandemic and recover better. Using Nigeria as a case study, activities in the domestic bond market significantly increased year-on-year given the relatively low yields in the market. In H1 2020, seven corporate bond issuances were raised to the tune of N152.7 billion compared to N54 billion raised in three issuances in the corresponding period of the previous year.

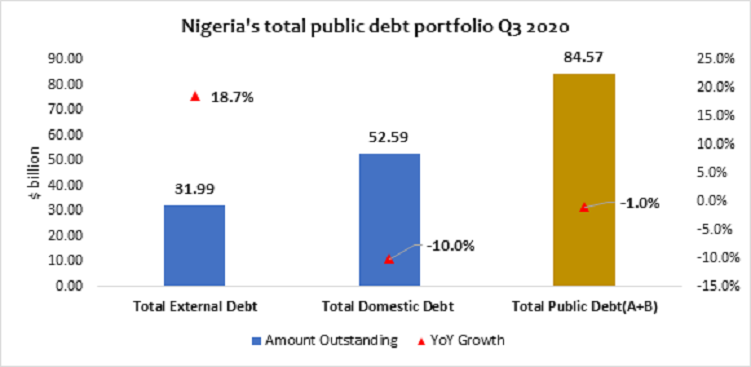

According to the data by the Debt Management Office (DMO), the nation’s debt stock data at the third quarter (Q3) 2020 showed that the total public debt portfolio of the federal and state government combined stood at N32.22 trillion ($84.57 billion), an increase of 22.9 per cent but a decrease of 1 per cent in dollar equivalent due to the different exchange rate values within the periods.

Nigeria’s total public debt showed that $31.99 billion (or 37.82 per cent of the debt) was external while $52.59 billion (or 62.18 per cent of the debt) was domestic. Further disaggregation of Nigeria’s foreign debt showed that $16.74 billion of the debt was multilateral; $502.38 million was bilateral (AFD) and another $3.26 billion bilateral from the Exim Bank of China, JICA, India, and KFW while $11.17 billion was commercial which are Eurobonds and Diaspora Bonds.

The debt conundrum leaves Africa in a dilemma considering the rising budget deficits coupled with the need to fund the deficits. If Africa is to stop depending on donors and multilateral funds to finance its economic development, it needs to evolve towards market-based financing for the quantum of financing required. In addition, African countries need to promote market-friendly policies that will attract capital to underserved sectors and allow the states to focus its limited financing on priority sectors such as education, health, and social services.

By Adedapo Adesanya

Nigerian businessman and chief executive of Dangote Industries Limited, Mr Aliko Dangote, has unveiled plans for a new phase of investments and acquisitions as the conglomerate pushes towards its target of generating $100 billion in annual revenue by 2030.

Mr Dangote disclosed this while receiving a delegation of senior executives from global investment banking and financial services firm Goldman Sachs, led by co-chief executive of Goldman Sachs International and Global Co-Head of Investment Banking, Mr Anthony Gutman, during a tour of the Dangote Petroleum Refinery & Petrochemicals and Dangote Fertiliser Limited complex in Lagos.

Speaking after the visit, Mr Dangote said the refinery and associated industrial facilities underscore the transformative impact of long-term investment in Africa, stressing that the group’s ambitions extend beyond its current strategic plan.

“No matter how we try to explain what we have built, you cannot fully appreciate it until you see it. But this is only the beginning. We need to look beyond 2030.

“The next phase of our journey will include new investments and acquisitions as we continue to scale the business,” he said.

He added that detailed internal modelling had reinforced management’s confidence that the Group’s target of generating $100 billion in annual revenue by 2030 was achievable.

According to him, the projections were based on conservative assumptions and had strengthened the company’s conviction to pursue an even more ambitious long-term growth strategy.

Mr Dangote also revealed that the strong participation of employees in the refinery’s recent private placement reflected growing internal confidence in the company’s long-term strategy and future prospects.

The Goldman Sachs delegation, after an extensive tour of the 700,000 barrels-per-day refinery, described the project as an extraordinary achievement.

“It is extraordinary what Mr Dangote and the whole organisation have achieved. The ambition, the scale of the project, the quality of the project and the culture of the people is very impressive,” the executives said.

According to a statement issued by Dangote Group on Friday, the delegation was led by Mr Anthony Gutman and included Mr Adib N. Zouein, Co-Head of EMEA Emerging Markets Regional Sales and Head of the Middle East and North Africa region for Global Banking & Markets Public; Mr Ryad Yousuf, Global Head of FICC Sales Strats and Structuring; and Mr Jimi Adesanya, Head of Sub-Saharan Africa Sales (excluding South Africa).

The visitors were received by Dangote; Group Vice President, Oil & Gas, Mr Devakumar Edwin; Managing Director and Chief Executive Officer of Dangote Petroleum Refinery & Petrochemicals, Mr David Bird; Group Executive Director, Oil & Gas, Ms Fatima Aliko Dangote; Chief of Staff to the President/CEO, Ibrahim Dikko; Group Chief Branding and Communication Officer, Mr Anthony Chiejina; Group Chief Economist, Mr Hassan Mahmud; Group Chief Strategy Officer, Mr Aliyu Suleiman; and Head of Administration, Dangote Petroleum Refinery & Petrochemicals, Mr Musa Bala, among other senior executives.

By Adedapo Adesanya

The Senate Public Accounts Committee has heard that Nigeria spent N1.16 trillion on fuel subsidy in 2021, while N1.20 trillion was deducted from federation crude oil sales proceeds during the same period.

The disclosure came from the Chairman of the Revenue Mobilisation Allocation and Fiscal Commission (RMAFC), Mr Mohammed Bello Shehu, during the committee’s ongoing investigation into the 2021 to 2023 Nigeria Extractive Industries Transparency Initiative (NEITI) audit reports on the oil and gas sector.

According to the commission, crude and petroleum product losses cost N16.2 billion, pipeline repairs accounted for N22.05 billion, while strategic stock holding attracted N6.75 billion.

The revelations come against the backdrop of Nigeria’s long-running fuel subsidy regime, which successive governments maintained to keep the pump price of petrol artificially low despite mounting fiscal pressures.

Over the years, subsidy payments consumed trillions of Naira, significantly reducing revenues available to the three tiers of government and contributing to widening budget deficits.

The issue reached a turning point in May 2023 when President Bola Tinubu announced the removal of fuel subsidy during his inauguration speech, declaring that “fuel subsidy is gone.” The decision followed years of concerns over the rising cost of the programme, allegations of fraud, and repeated recommendations by fiscal authorities and international financial institutions that the subsidy had become unsustainable.

The removal triggered a sharp increase in the pump price of Premium Motor Spirit (petrol), leading to higher transportation and living costs across the country. In response, the federal government introduced a series of palliative measures, including cash transfers, support for mass transit, and wage-related interventions, while arguing that savings from the subsidy would be redirected to infrastructure, education, healthcare, and other critical sectors of the economy.

The commission also argued that the current method of calculating the 13 per cent derivation fund undermines the constitutional intention of the policy.

Meanwhile, the committee stood down the Niger Delta Development Commission’s presentation until next Wednesday to allow lawmakers review its submission.

The committee also expressed displeasure over the absence of the Auditor-General of the Federation, warning that he must appear before lawmakers next Tuesday or face compulsory appearance through the constitutional powers of the National Assembly.

By Adedapo Adesanya

Businesses in the country expect the Naira to gradually appreciate against the US Dollar between now and January 2027, according to the Central Bank of Nigeria’s (CBN) July 2026 Business Expectations Survey Report released on Thursday.

The report showed that the Business Confidence Index (BCI) remained positive throughout the review period despite perceived macroeconomic challenges. It noted that all sectors expressed optimism about the economy, with the electricity, gas and water sector posting the highest Business Confidence Index of 59.4 points and the strongest expansion prospects for August 2026.

According to the report, “In July 2026, the Business Confidence Index was 5.7 points, reflecting continued optimistic sentiment among formal businesses.”

It attributed the positive sentiment mainly to increased demand (22.3 per cent), economic diversification (21.4 per cent), and improved access to finance (15.0 per cent). However, respondents identified inflation (27.7 per cent), energy-related challenges (23.4 per cent), insecurity (22.4 per cent), and heightened geopolitical uncertainties (16.5 per cent) as the major factors weighing on business confidence.

On the outlook by broad sector, the central bank said confidence remained positive across all sectors in July. The Industry sector recorded a modest improvement, with its index rising to 11.5 points from 10.5 points, while the Services sector increased to 3.6 points from 2.9 points.

By contrast, the Agriculture sector recorded a significant moderation, with its index falling to 3.4 points from 12.2 points.

Despite this, the apex bank said the six-month outlook remained upbeat, with confidence indices across all sectors indicating positive expectations over the review period.

On the macroeconomic outlook by region, the report noted a divergence in sentiment, with businesses in Northern Nigeria expressing stronger confidence than their Southern counterparts in July. Nevertheless, respondents across all regions maintained positive expectations for August.