Economy

Nigerians Defy Central Bank, Flock to Bitcoin

By: Gerelyn Terzo of Sharemoney

Bitcoin, the leading cryptocurrency, has seen its value balloon by more than 100% year-to-date, soaring to an all-time high of more than USD 60,000.

Nigerians, many of whom are battling poverty, would be hard-pressed to miss out on those gains. This is especially true considering that the unemployment rate in the most populous African nation was 33.3% as of last quarter, with more than 23 million Nigerians out of work.

Enter bitcoin, which has been a safe-haven investment as well as a faster and cheaper payment method for the growing segment of the population that is catching on.

In fact, Nigeria last year rose to the top of the heap for bitcoin trading at $400 million in volume, surpassing transactional volume in nearly every other jurisdiction — with the exception of the United States and Russia — as traditional asset classes lose their appeal in comparison and the local currency, the naira, remains under pressure.

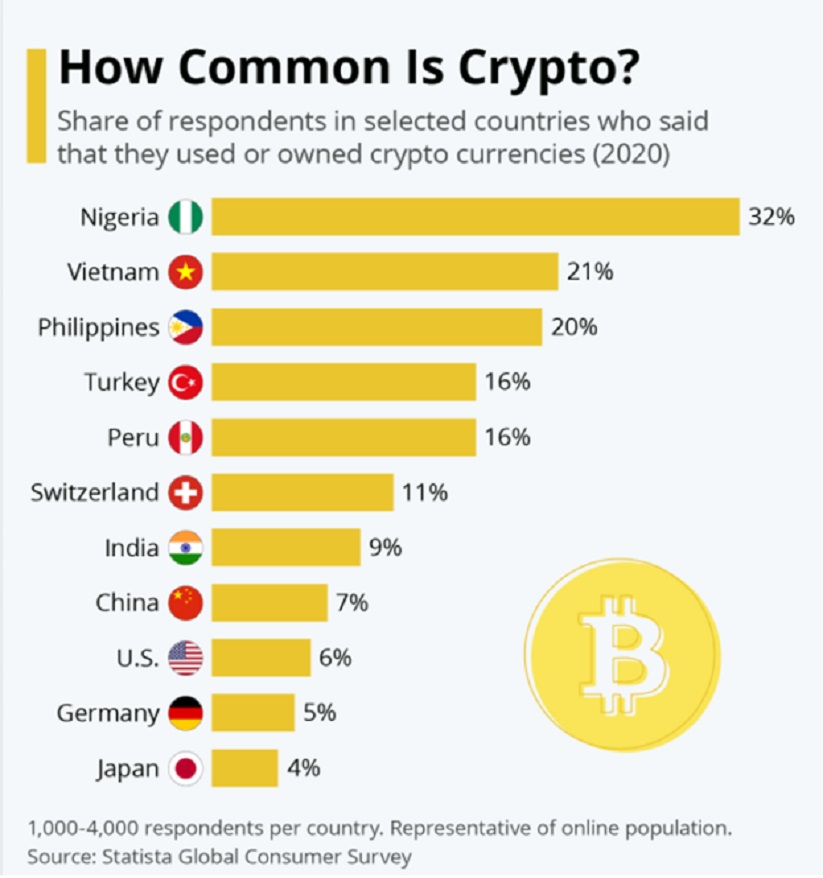

Nearly one-third of Nigerians who participated in a Statista poll said that they used or owned cryptocurrencies, more than any other country represented in the survey.

Source: Statista

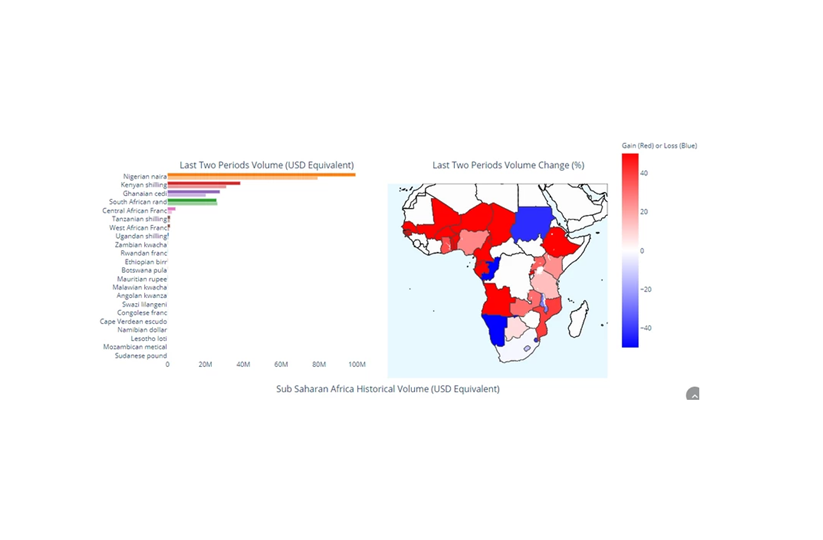

Nigeria also stands out in all of Africa, as the top peer-to-peer bitcoin trading nation on the continent based on bitcoin trading volume.

Nigeria’s P2P BTC trading volume surpassed USD 99 million in the first quarter of 2021. Kenya is a distant second at $34.8 million followed by Ghana and South Africa at $27.4 million and $25.8 million, respectively.

Source: Business Insider/Useful Tulips

The robust bitcoin trading activity in Nigeria has earned the country the title of Africa’s Bitcoin Nation. A 27-year-old Nigerian office worker who was spotlighted by the AFP, Chigoziri Okeke, described how he first invested in cryptocurrencies five years ago with the intention of just making a payment.

When his crypto wallet’s value increased by 10% in a few short days, however, he was hooked and started directing a percentage of his salary toward the market. Today, this investor’s crypto portfolio is worth USD 50,000, comprising various digital assets.

In addition, Google searches of bitcoin in Nigeria surpass that of any other jurisdiction, according to Nairametrics.com. Bitcoin appeals especially to the West African nation’s millennial generation, who are looking to the flagship cryptocurrency as a store-of-value asset as well as a way to circumvent the hoops they must jump through to open a traditional investment account.

With the bitcoin price most recently hovering at USD 60,000, Nigerians have reason to be excited. At this price, one bitcoin could reportedly buy someone a three-bedroom apartment in Lagos’ Ajah neighbourhood.

Unstable Fiat Currency

A big part of bitcoin’s popularity is due to Nigeria’s unstable naira. The International Monetary Fund (IMF) has drawn a line in the sand, stating that Nigeria’s fiat currency is “overvalued” by more than 18%. The IMF wants Nigeria to devalue its fiat currency, but the African nation’s government has said no way.

Nigerian President Muhammadu Buhari blames “global outflows” triggered by COVID-19 for the unstable naira and believes that devaluing it further after doing so twice in 2020 would only exacerbate the already sky-high inflation rate, which is currently in the double-digits at more than 17%. This would weaken Nigerians’ purchasing power even more. Nigeria’s central bank slashed the naira’s value by close to one-quarter last year.

Meanwhile, not only has bitcoin been generating returns hand over fist, but it has also been thrust into the global spotlight amid the SARS-related protests in Nigeria.

According to reports, Nigeria thwarted financial payments toward police brutality protests, which only led the supporters to donate bitcoin instead. Twitter and Square CEO Jack Dorsey backed this movement, which only brought more attention to the country and cryptocurrencies.

Source: CoinGecko/TradingView

Mixed Signals

Nigeria’s central bank has been highly critical of bitcoin, warning as recently as February that “cryptocurrencies are largely speculative, anonymous and untraceable.”

Nonetheless, the Central Bank of Nigeria can’t stop the population from accessing the flagship cryptocurrency, thanks to the peer-to-peer nature of bitcoin, which was inherently designed to circumvent third-party service providers like banks.

Bitcoin creator Satoshi Nakamoto, whose real identity remains a mystery, defined the first cryptocurrency in the whitepaper, which was published in 2008, saying:

“A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.”

The Central Bank of Nigeria has since backtracked from its remarks slightly, maintaining that it has not placed a blanket ban on cryptocurrency trading. It is a tangled web, however. The central bank instead said that it is doubling down on a 2017 law that bans institutions supporting cryptocurrency transactions.

Even though institutions might be banned from supporting cryptocurrency trading, individuals are still free to trade them. The central bank is sending mixed signals, to say the least, as local banks were instructed by the central bank to refrain from doing business with customers who transact in cryptocurrencies.

“The CBN did not place restrictions from use of…cryptocurrencies and we are not discouraging people from trading in it. What we have just done was to prohibit transactions on cryptocurrencies in the banking sector,” stated Adamu Lamtek, according to Decrypt, citing Today NG.

Since the restrictions were imposed on Nigeria’s crypto trading industry, rather than disappearing, the industry has flexed its muscle for its nimble nature. In a few short months, they have been quick to build P2P exchanges that circumvent the crypto ban on financial institutions.

The restrictions have funnelled more activity to over-the-counter (OTC) venues while a makeshift P2P market is similarly expanding. Danny Oyekan, the founder of global social payments application Coins App, is cited by Decrypt as saying,

“So basically, the ban only forced the fiat channels underground.”

Source: Twitter

In Nigeria, cryptocurrencies are regulated by the country’s own Securities and Exchange Commission, which last year stated that it would classify cryptocurrencies as securities unless they are proven otherwise by the asset’s issuer or sponsor. In February, Nigeria’s SEC said that crypto regulation was going to be placed on the back-burner amid the central bank’s crypto crackdown.

Despite the uncertainty, Nigerians are showing no signs of relenting in their pursuit to own bitcoin and are increasingly relying on P2P trading platforms to do just that.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange was down by 2.48 per cent on Friday, June 19, with the Unlisted Security Index shedding 108.36 points to close at 4,252.73 points compared with the previous day’s 4,361.09 points.

During the trading day, the market capitalisation of the OTC securities exchange dropped 2.18 per cent or N67.29 billion to settle at N2.552 trillion, in contrast to Thursday’s N2.609 trillion.

The alternative stock market was in the red yesterday after finishing with three price losers led by Central Securities Clearing System (CSCS) Plc, which gave up N8.57 to trade at N77.77 per share versus the preceding day’s N86.34. FrieslandCampina Wamco Nigeria Plc lost N8.19 to quote at N170.00 per unit compared with the previous session’s N178.19 per unit, and Food Concepts Plc crashed by 26 Kobo to end at N2.51 per share versus N2.77 per share.

Business Post reports that there were also three price gainers during the session, led by Golden Capital Plc, which chalked up 67 Kobo to sell at N13.67 per unit versus N13.00 per unit. Afriland Properties Plc gained 65 Kobo to trade at N16.85 per share compared with the previous price of N16.20 per share, and MRS Oil added 3 Kobo to close at N142.23 per unit versus N142.00 per unit.

The volume of trades was up by 20.3 per cent on Friday to 954,106 units from 792,835 units, and the number of deals increased by 75 per cent to 35 deals from 20 deals, while the value of transactions went down by 12.9 per cent to N42.7 million from N49.0 million.

The most traded stock by value on a year-to-date basis was Great Nigeria Insurance (GNI) Plc, with 3.4 billion units worth N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units sold for N6.5 billion, and CSCS Plc with 67.8 million units exchanged for N4.7 billion.

The most traded stock by volume on a year-to-date basis was also GNI Plc, with 3.4 billion units valued at N8.4 billion, followed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units transacted for N415.7 million.

By Dipo Olowookere

The local stock exchange remained in the red on Friday after it further depreciated by 0.62 per cent due to panic sell-offs in some bellwether equities.

NAHCO lost 10.00 per cent to trade at N148.50, Royal Exchange depreciated by 10.00 per cent to N1.53, GTCO slumped by 9.97 per cent to N115.55, First Holdco dropped 9.84 per cent to quote at N55.00, and Neimeth slipped by 9.60 per cent to N28.12.

On the flip side, Deap Capital increased by 9.89 per cent to N4.89, RT Briscoe expanded by 9.62 per cent to N13.10, International Energy Insurance advanced by 7.43 per cent to N5.06, Jaiz Bank gained 7.14 per cent to sell for N9.00, and Living Trust Mortgage Bank rose by 5.26 per cent to N4.00.

During the session, the energy index chalked up 2.35 per cent, but this was not enough to lift the Nigerian Exchange (NGX) Limited when the closing gong was struck by 4 pm to signify the close of trading activities.

This was because the banking sector lost 4.41 per cent, the insurance counter shed 1.52 per cent, the industrial goods space declined by 0.71 per cent, and the consumer goods segment tumbled by 0.13 per cent.

Consequently, the All-Share Index (ASI) contracted by 1,463.45 points to 235,941.27 points from 237,404.92 points, and the market capitalisation retreated by M939 billion to N151.327 trillion from N152.266 trillion.

The activity chart was topped by Access Holdings, which posted a turnover of 65.0 million shares valued at N1.5 billion. Zenith Bank sold 35.2 million stocks worth N3.9 billion, Sterling Holdings exchanged 28.4 million equities for N217.8 million, UBA transacted 16.3 million shares valued at N650.7 million, and GTCO traded 14.0 million stocks worth N1.8 billion.

In all, investors transacted 440.4 million equities for N24.7 billion in 50,273 deals, in contrast to the 691.6 million equities valued at N116.9 billion traded in 50,025 deals on Thursday, implying an uptick in the number of deals by 0.50 per cent, and a decrease in the trading volume and value by 36.32 per cent and 78.87 per cent, respectively.

By Adedapo Adesanya

The Naira again depreciated against the United States Dollar by N7.16 or 0.53 per cent in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Friday, June 19, to N1,370.46/$1 from the previous day’s N1,363.30/$1.

In the same vein, the Nigerian currency lost N9.07 against the Pound Sterling at the official market yesterday to trade at N1,814.76/£1 compared with Thursday’s closing price of N1,805.69/£1, and crashed against the Euro by N6.43 to settle at N1,571.50/€1 versus N1,565.07/€1.

Also, the Naira weakened against the greenback in the black market during the session by N5 to sell for N1,390/$1, in contrast to the preceding day’s N1,385/$1, and at the GTBank FX desk, it shed N3 to close at N1,376/$1 versus N1,373/$1.

The official market’s FX liquidity has been facing pressure over the last three trading sessions, contributing to a decline in the official exchange rate due to rising demand for foreign payments.

FX reserves rose to $51.03 billion, the highest level since January 20, 2009, according to data obtained from the Central Bank of Nigeria (CBN). The figure also represents the highest since the beginning of the year and under the administration of the current Governor of CBN, Mr Yemi Cardoso.

The latest figure underscores the steady strengthening of Nigeria’s external buffers, which continues to reinforce investor confidence in the Nigerian economy and support exchange rate stability.

Meanwhile, the cryptocurrency market was mixed, with Bitcoin (BTC) up by 0.8 per cent to $63,225.80 after trading activity was relatively subdued due to a US federal holiday, as the absence of stock and bond market activity led to quieter conditions across crypto markets, even though digital assets continue to trade around the clock.

Further, TRON (TRX) also gained 0.8 per cent to sell at $0.3230, Binance Coin (BNB) jumped 0.5 per cent to $579.84, and Ethereum (ETH) appreciated by 0.1 per cent to $1,704.23.

On the flip side, Ripple (XRP) declined by 0.9 per cent to $1.13, Cardano (ADA) shed 0.8 per cent to trade at $0.1611, Solana (SOL) fell by 0.1 per cent to $69.23, and Dogecoin (DOGE) slipped by 0.1 per cent to $0.0831, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) remained unchanged at $1.00 each.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn