Economy

Finance Minister Insists Nigeria Does Not Have Debt Problem

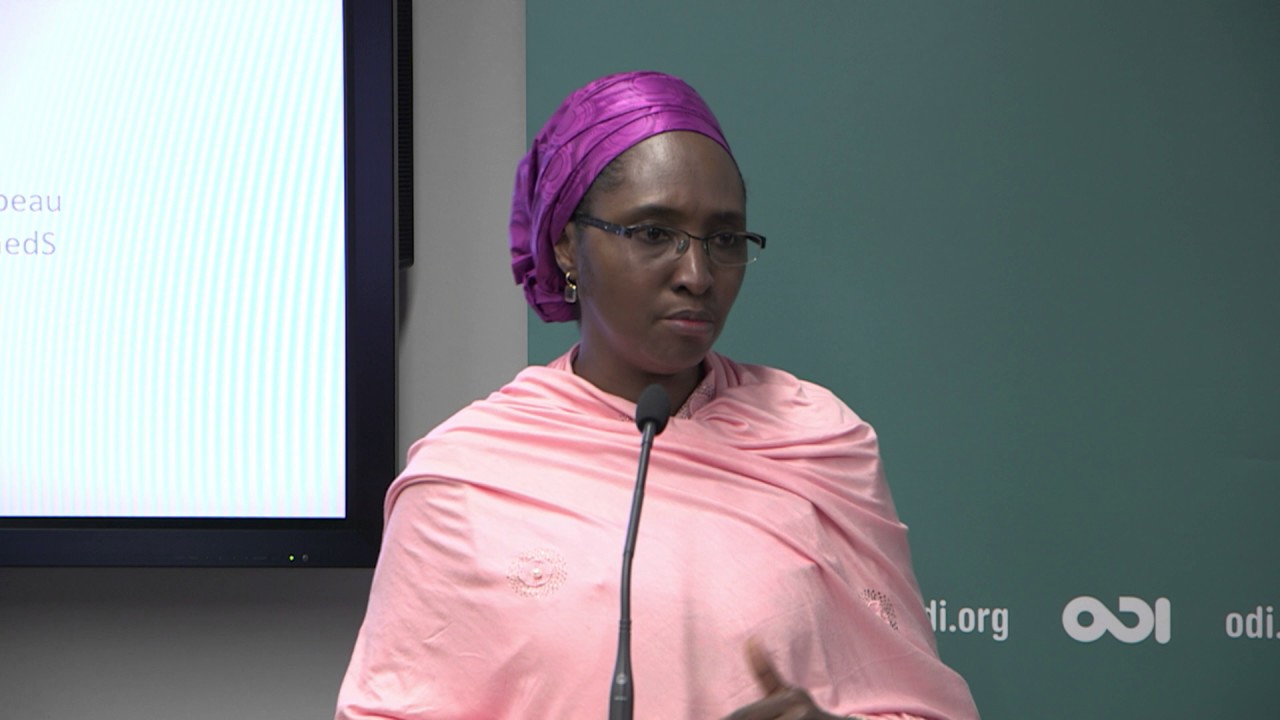

By Modupe Gbadeyanka

The federal government has reiterated its determination to keep the debts of Nigeria within sustainable levels so as not to put the nation into trouble in the short, mid and long term.

This assurance was given by the Minister of Finance, Budget and National Planning, Mrs Zainab Ahmed at the International Monetary Fund (IMF)-World Bank Annual Meetings held from October 11 to 17, 2021, in the United States.

The Finance Minister led a delegation from Nigeria to the meetings, including the Permanent Secretary, Finance, Mr Aliyu Ahmed; Director-General of the Budget Office, Mr Ben Akabueze; the Nigerian Deputy Ambassador; Director International Economic Relations Department of the Ministry and others.

According to Mrs Ahmed, Nigeria does not have a debt problem but how to generate revenue, reiterating the commitment of the fiscal authorities towards increasing revenue generation while ensuring sustainable deficit and debt levels.

She stated that to address the revenue issue in the medium term, the central government under the leadership of Mr Muhammadu Buhari launched the Strategic Revenue Growth Initiative (#SRGI).

The Minister disclosed that this and other steps taken by the government has allowed international investors to be optimistic about the country’s credit status and have shown interest in engaging the government, stressing that this was confirmed at the hybrid Eurobond global investors meeting and roadshow organized by the Nigeria Debt Management Office (DMO) in New York.

“Nigeria has demonstrated deep resilience amid the COVID-19 pandemic and commitment to sound policy and improving governance, positioning the continent’s largest economy and the most populous nation at the forefront of the post-pandemic recovery with key structural reforms rolled out that include steps towards cost-reflective tariffs in the power sector, and the recently enacted Petroleum Industry Act,” the Minister said at the investor meeting.

She stated that, “Nigeria has a broad and diversified economy across sectors contributing to macroeconomic resilience, with oil and gas contributing only 8.34 per cent to real GDP (gross domestic product) in the first half of 2021.”

“Post COVID-19 recovery has been aided by the pick-up in non-oil activity in information and communications, mining and quarrying, accommodation and food services, transportation and storage, education and trade,” Mrs Ahmed said.

“Nigeria continues to diversify and grow the non-oil-and-gas sectors of the economy through continued economic reform policies under the Buhari administration,” the Minister added.

By Adedapo Adesanya

The Nigeria Customs Service (NCS) has intensified its nationwide sensitisation campaign on the implementation of the Green Tax Surcharge and related fiscal adjustments ahead of the policy’s commencement on July 1, 2026.

The service disclosed this in a statement published on its official X handle on Monday, saying the initiative is aimed at promoting environmental sustainability, reducing carbon emissions and encouraging the importation of cleaner vehicles into the country in line with global environmental standards.

According to the statement, the latest sensitisation programme was held at the Apapa Area Command on Friday, June 26, 2026, under the theme, “Implementation of the Green Tax Surcharge and Related Fiscal Adjustments.”

The event brought together customs officers, licensed customs agents, freight forwarders, importers and other key stakeholders to familiarise them with the new policy ahead of its implementation.

Representing the Comptroller-General of Customs, Mr Adewale Adeniyi, the Zonal Coordinator for Zone A, Mr Mohammed Babadende, said the exercise was organised to ensure stakeholders fully understand the policy and its implementation framework before it takes effect.

“This sensitisation is designed to ensure that every stakeholder clearly understands the policy before implementation. Our objective is to eliminate uncertainty, promote voluntary compliance and guarantee uniform application of the Green Tax Surcharge across all commands,” Mr Adeniyi said.

He stressed that effective stakeholder engagement would help ensure a seamless rollout of the policy while improving compliance across the country’s ports and border stations.

Delivering a technical presentation, the Comptroller in charge of Tariff, System Audit and Coordination, Mr Murtala Muazu, explained that the Green Tax Surcharge differs from conventional fiscal measures and would therefore require a separate assessment process.

Mr Muazu disclosed that the agency has introduced a simplified implementation mechanism through the Harmonised System (HS) Code declaration platform to facilitate accurate assessment and ease compliance by importers and clearing agents.

He further revealed that the federal government has simultaneously reviewed existing import charges on vehicles to cushion the effect of the new environmental levy.

According to him, import levies on vehicles have been reduced from 20 per cent to 10 per cent, while duties on used vehicles have been cut from 15 per cent to five per cent.

The customs said the reductions are intended to offset the impact of the Green Tax Surcharge while supporting legitimate trade and ensuring businesses are not unduly burdened by the new policy.

Area Controllers who attended the sensitisation programme urged importers, licensed customs agents and members of the public to support the initiative, noting that the reduction in import levies would lower the cost of doing business, facilitate legitimate trade and ultimately contribute to reducing transportation costs across the country.

Stakeholders at the event welcomed the initiative but called for sustained public awareness campaigns to ensure broader understanding, minimise confusion and encourage voluntary compliance as the rollout date approaches.

The Green Tax Surcharge is scheduled to take effect on July 1, 2026, as part of the federal government’s broader efforts to promote environmentally friendly transportation and align Nigeria’s import policies with global climate and sustainability objectives.

By Dipo Olowookere

The three busiest equities on the floor of the Nigerian Exchange (NGX) Limited last week were Access Holdings, Fidelity Bank, and Chams Holdco.

The trio accounted for 20.90 per cent and 5.69 per cent of the total trading volume and value, respectively, after trading 485.749 million units worth N7.656 billion in 17,843 deals.

In the week, investors transacted 2.324 billion shares valued at N134.486 billion in 249,328 deals versus the 3.075 billion shares worth N254.614 billion executed in 287,157 deals in the previous week.

The financial services space led the activity chart with 1.523 billion stocks sold for N47.542 billion in 105,230 deals, contributing 65.53 per cent and 35.35 per cent to the total trading volume and value, respectively. The ICT industry exchanged 198.821 million shares worth N32.622 billion in 29,905 deals, and the consumer goods sector posted a turnover of 151.635 million shares worth N10.933 billion in 23,951 deals.

In the five-day trading week, 22 equities appreciated versus 11 equities a week earlier, 57 equities depreciated versus 78 equities of the previous week, and 67 equities remained unchanged versus 57 equities in the preceding week.

McNichols gained 26.47 per cent to trade at N8.60, International Energy Insurance appreciated by 14.43 per cent to N5.79, GTCO expanded by 10.69 per cent to N127.90, First Holdco jumped by 10.00 per cent to N55.00, and Airtel Africa also climbed 10.00 per cent to settle at N4,358.80.

On the flip side, Trans-Nationwide Express declined by 26.79 per cent to N3.28, Deap Capital slipped by 23.31 per cent to N3.75, Abbey Mortgage Bank lost 20.30 per cent to trade at N8.05, Aradel Holdings contracted by 19.00 per cent to N1,417.50, and Regency Assurance dropped 18.56 per cent to close at 79 Kobo.

The All-Share Index (ASI) and the market capitalisation, which measures the performance level of Customs Street, depreciated last week by 1.65 per cent and 1.60 per cent each to 232,049.02 points and N148.905 trillion, respectively.

Similarly, all other indices finished lower except the CG, banking, AFR Bank Value, AFR Div Yield and MERI Value indices, which grew by 2.40 per cent, 3.51 per cent, 3.28 per cent, 9.93 per cent and 0.56 per cent, respectively.

By Adedapo Adesanya

The Centre for the Promotion of Private Enterprise (CPPE) has cautioned against the Senate’s resolution seeking to ban the importation of textile fabrics, warning that such a move could be counterintuitive as it would undermine key industries, threaten millions of jobs and fail to revive Nigeria’s struggling textile sector.

According to the chief executive of the think-tank, Mr Muda Yusuf, while the objective of revitalising the textile industry was commendable, an outright import prohibition would likely create more economic challenges than solutions.

The Senate had urged the federal government to implement an import ban for an initial period of five years. The motion, sponsored by Senator Sunday Katung, is to create a protected window for domestic cotton farmers and local textile mills to scale up production.

Mr Yusuf noted that the import ban wasn’t the major driving force behind the country’s ailing textile sector, adding that it was driven mainly by structural constraints such as high energy costs, poor infrastructure, expensive credit and obsolete technology.

Other factors, he said, driving the decline of the sector included logistics bottlenecks, smuggling and policy inconsistency, rather than import competition.

According to him, restricting textile imports will disrupt production across the country’s garment, fashion, tailoring, furniture and interior design industries, which depend heavily on imported fabrics as production inputs.

He said that Nigeria’s fashion, garment-making and tailoring industry, valued at about N10 trillion, supported an estimated 10 million livelihoods and represented one of the country’s most vibrant creative economy sectors.

He further stated that the sector generates significant domestic value addition through design, tailoring, branding, embroidery, merchandising and retailing, often exceeding the value of the imported textile inputs.

“Restricting textile imports would increase production costs, reduce consumer choice and threaten thousands of micro, small and medium enterprises engaged in fashion, tailoring and garment manufacturing,” he said.

Mr Yusuf added that textile fabrics were also critical inputs for the furniture and interior design industry, valued at about N7 trillion, warning that supply disruptions would weaken the competitiveness of manufacturers.

He further noted that imported textile fabrics already attracted a combined Import Duty and Import Adjustment Tax of between 35 per cent and 45 per cent, yet the existing tariff protection had not restored the competitiveness of local textile manufacturers.

“The core problem lies in production economics rather than import penetration. An import ban addresses the symptom while leaving the underlying causes unresolved,” he said.

Mr Yusuf also maintained that local textile manufacturers currently lacked the capacity to meet the quantity, quality and diversity of fabrics required by the country’s fashion, garment, furniture and interior design industries.

He warned that an outright import ban could therefore create supply shortages and negatively affect downstream sectors that generated significantly more employment than textile manufacturing itself.

The CPPE boss advocated a comprehensive value-chain strategy to revive the textile industry and called for the restoration of domestic cotton production through improved security, mechanisation, better seedlings, extension services and guaranteed off-take arrangements.

He also stressed the need for affordable long-term financing, access to modern technology, a reliable energy supply and a more competitive operating environment for manufacturers.

Among other recommendations, Yusuf urged the government to prioritise locally produced textiles and garments for uniforms used by the military, paramilitary agencies, schools and other public institutions.

He also recommended the establishment of a Textile Competitiveness Fund financed from textile-related import tax revenues to support technology upgrades and industry modernisation.

Other measures proposed include strengthening border enforcement to curb smuggling and implementing reforms aimed at reducing energy and financing costs while improving industrial infrastructure.

Mr Yusuf stressed that sustainable revival of Nigeria’s textile industry would depend on improving competitiveness rather than imposing additional import restrictions.

He warned that a blanket import ban could encourage smuggling, reduce customs revenue and weaken a broader value chain that contributed substantially to employment and economic growth.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn