Banking

Debit Cards: Still Driving Financial Inclusion

The last decade witnessed tremendous changes in the nation’s banking landscape. The number of bank customers has grown, agency banking has gained a foothold and cheques have given way to transfers, particularly through SMS banking and mobile apps. Debit cards, however, remained a constant feature during this period.

Debit cards are financial instruments issued by commercial banks to their customers to enable seamless transaction outside the banking halls. Debit cards have proven reliable in banking and other financial transactions. It is today acknowledged as a viable tool in the quest to drive financial inclusion in Nigeria.

Financial inclusion refers to a situation by which individuals and businesses can access appropriate, affordable and timely financial products and services. These products and services include savings, credit, insurance, equity and pension.

The objective of financial inclusion is to capture the unbanked into the formal banking space and ensure the availability of more financial products to the underbanked. As the World Bank notes, access to a transactional account is the first step towards broader financial inclusion.

Several initiatives have been deployed by the Central Bank of Nigeria (CBN) to drive these financial inclusion objectives, especially payments. Debit cards have proven a critical tool in driving financial inclusion in emerging markets such as Nigeria.

While debit cards were at some points the exclusive preserve of a few, it is today almost ubiquitous. This is due largely to the pioneering efforts of Interswitch Group to place debit cards in the hands of many Nigerians with the introduction of Verve card.

Verve card is not just a domestic card with lower transactional fees, it is highly secure and tailored to cater to the market nuances. It is not surprising therefore that Verve quickly captured an appreciable portion of the market.

Inevitably, as more Nigerians added debit cards to their wallets, information and knowledge about financial services, payment patterns and transaction history emerged. Infrastructure and technology to support the usage also expanded with the deployment of more payment channels across the nation. Interswitch ensured that the Verve card was compatible with a majority, if not all of the payment channels.

Today, with a debit card, cardholders do not have to travel to their banks’ branches to carry out most of their financial transactions. With a debit card, cardholders can make cashless payments for their purchases at the point of sale and small scale business owners can build transaction history with which they can access credit facilities and scale their businesses.

The debit card can be incorporated to underwrite insurance policies and provide various cover to the cardholder. Pensioners can use their debit cards to access their periodic pension payments after retirement. In some cases, the debit card is used as a form of electronic identity (eID). It can be used to access grants, and agricultural resources such as fertilizers, equipment lease, seedlings, etc.

Undoubtedly, debit cards are an effective force in driving financial inclusion.

As debit card payment transaction success increased, cardholders’ confidence grew. Subsequently, it became easier to convince others to come into the formal banking space to enjoy the convenience that the cards offered.

Verve’s intervention in the payment card space proved a game-changer. It became commonplace to see the blue-collar worker and the white-collared counterpart on the same queue to use the ATM. It was no longer strange to see the driver and his boss making payments using PoS at the stores. In the financial services space, debit cards are revolutionary.

Figures on digital payment from the National Bureau of Statistics and the CBN for Q3 2020 showed that digital payment figures for the period was N320 trillion, with ATM transactions accounting for a big chunk of the total transactions. This is not surprising with the significant increase in the use of PoS, USSD and card-based web payments.

The debit card is an enabler. Verve card is a leveler. While the debit card has empowered people to carry out financial transactions seamlessly, the Verve card has ensured that this easy, convenient and secured way service offering came within the reach of all Nigerians, who desired it.

Yes, there is more to be done. The regulatory is on the right path with policies aimed at strengthening and deepening the efficiency of the nation’s e-payment system. New players are emerging and there is an increase in the issuance of cards, both debit and credit. It is clear, agency banking is on the rise, the number of touchpoints are increasing and options are growing. The future of cards, at this time, appears secure and bright.

By Modupe Gbadeyanka

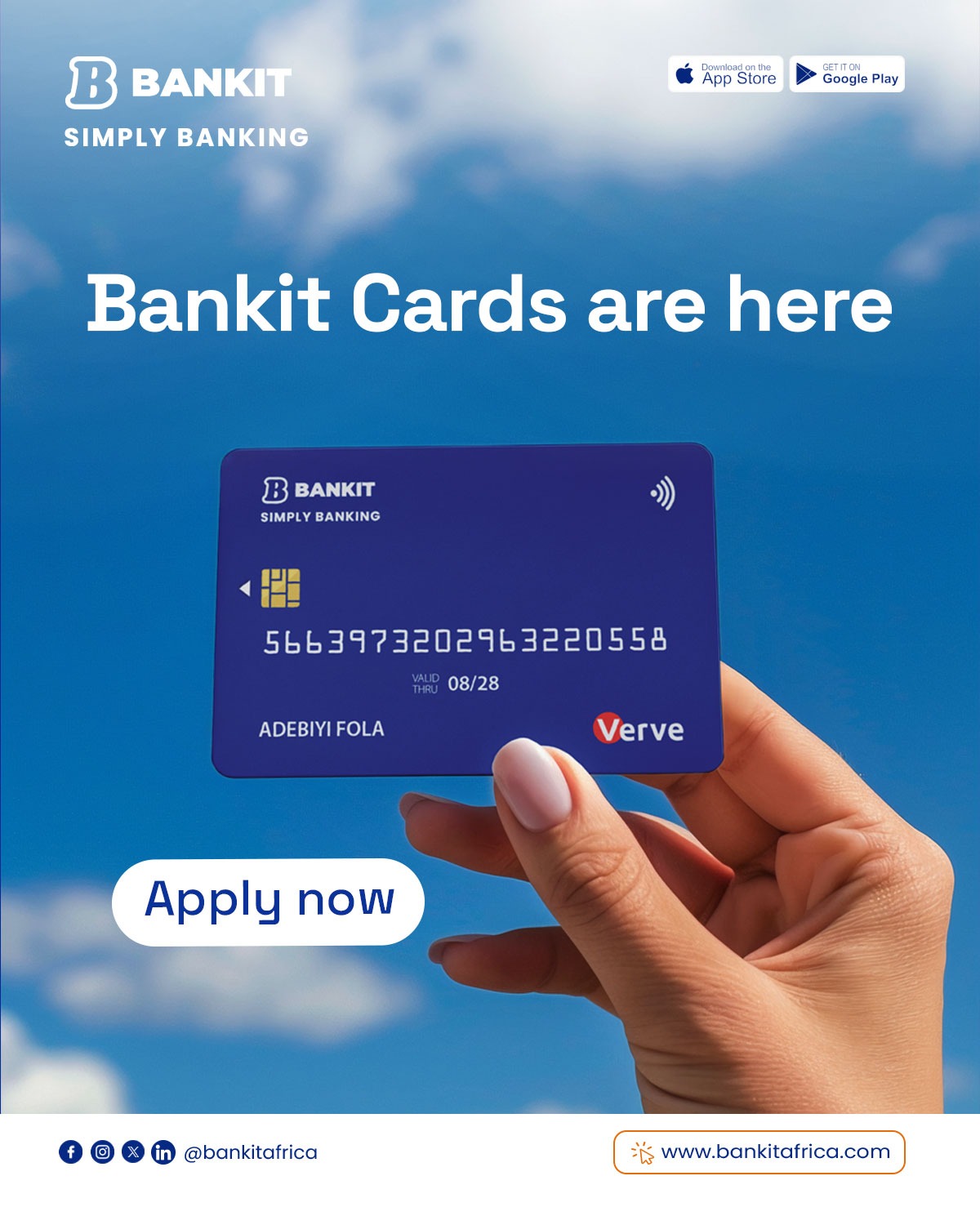

As part of its commitment to delivering fast, secure, and truly accessible financial solutions at scale, Bankit has introduced a smart payment card.

It is completely free to customers, with no card issuance fee required and can be delivered nationwide at no extra cost.

Fully integrated with the Bankit app, the new payment cards enable users to carry out a wide range of transactions with ease, including ATM withdrawals, POS payments, and online purchases, while also allowing real-time tracking and management of spending.

The introduction of Bankit Cards marks a significant evolution of the platform’s already strong offering, which has seen widespread adoption for its instant transfers, seamless bill payments, and secure digital transactions.

By eliminating the cost barrier typically associated with card ownership, Bankit is setting a new benchmark for value in Nigeria’s digital banking space while extending its capabilities into everyday physical and online payments.

The Head of Marketing at Bankit, Mr Kingsley Ezenwa, described the initiative as a bold step toward deepening customer trust and accelerating financial inclusion.

“The launch of Bankit cards, completely free for our customers, is a defining moment in our growth journey. We are not just introducing a new product; we are removing barriers and expanding access to modern financial tools for millions of Nigerians,” he said.

He emphasised that the decision to waive both card and delivery fees reflects Bankit’s broader philosophy of putting customers first while building a truly inclusive financial ecosystem.

“Our users already trust Bankit for seamless transfers and bill payments. By making our cards free, we extend that value into everyday spending online, offline, and anywhere payments are required without adding any extra cost burden,” he added.

As Nigeria’s fintech landscape becomes increasingly competitive, Bankit continues to distinguish itself through simplicity, affordability, and superior user experience. The platform’s rapid growth is driven by its ability to anticipate and respond to the evolving needs of modern consumers who demand fast, reliable, and cost-effective financial services.

At the core of Bankit’s offering is a strong commitment to security. The platform integrates advanced protection systems, including real-time transaction monitoring, multi-layer authentication, and robust encryption protocols designed to safeguard user funds and data at every touchpoint.

“Security remains at the heart of everything we do. While we are making access easier and more affordable, we are also ensuring that our users enjoy the highest level of protection, delivering not just convenience, but true peace of mind,” Mr Ezenwa further stated.

With increasing adoption across individuals and small businesses, Bankit is quickly becoming Nigeria’s preferred fintech choice, playing a key role in driving financial inclusion and accelerating the transition to a cashless, digitally empowered economy.

“Bankit is scaling rapidly because we understand the needs of modern consumers. Simplicity, reliability, innovation and now affordability are what set us apart. Offering these cards free of charge is another step toward becoming Nigeria’s leading digital banking solution,” he concluded.

VALR, Africa’s largest crypto exchange by trade volume, has integrated with Onafriq, the continent’s leading digital payments gateway. This partnership enables VALR users across Africa to fund their accounts directly through mobile money in local currencies, significantly broadening access to digital financial services for millions of people.

Mobile Money’s Role in African Financial Inclusion

Mobile money serves as a foundational element of financial services in Africa, facilitating everyday transactions, remittances, savings, and credit in areas with limited traditional banking access. According to the GSMA’s State of the Industry Report on Mobile Money 2025, global registered mobile money accounts reached 2.1 billion by the end of 2024, with over half a billion monthly active users. The sector processed approximately 108 billion transactions valued at more than $1.68 trillion in 2024, reflecting 20% year-on-year growth in volume and 16% in value.

In Sub-Saharan Africa, mobile money continues to drive substantial economic impact, contributing around $190 billion to GDP in 2023 alone. This growth is supported by interoperable networks that enable payments across major local currencies, including the Kenyan Shilling, Nigerian Naira, Ghanaian Cedi, and Ugandan Shilling, and through mobile money platforms such as M-Pesa and MTN MoMo. In the majority of these markets, mobile money usage for domestic transactions far outweighs traditional methods such as credit cards and direct bank transfers, according to complementary insights from the World Bank’s Global Findex 2025 report, making acceptance of mobile money crucial to successful market entry.

Onafriq operates Africa’s largest digital payments network, connecting nearly 1 billion mobile money wallets across 43 markets. The integration utilises this extensive infrastructure to allow direct, local-currency deposits to VALR, settled in stablecoins or selected crypto, streamlining access and reducing dependence on conventional banking systems.

Enabling Broader Participation in VALR’s Financial Product Suite

Through this integration, with VALR and Onafriq processing all settlements using stablecoins, users in supported markets can deposit funds via mobile money and engage with VALR’s comprehensive offerings. These include spot and margin trading for Bitcoin and over 100 crypto assets, tokenised real-world assets such as gold, equities, and private credit, yield products like lending and staking, and VALR Pay for efficient payments.

By integrating mobile money on-ramps, the partnership facilitates easier entry into global digital markets using established local payment methods.

VALR’s Leadership in Promoting Financial Inclusion

VALR holds a prominent position in Africa’s digital asset sector, serving over 1.7 million registered users and 2,000 corporate and institutional clients worldwide. Licensed by South Africa’s Financial Sector Conduct Authority (FSCA) and with regulatory approval in Europe, VALR is dedicated to building inclusive financial systems.

“VALR’s partnership with Onafriq deepens our reach across Africa and the world, connecting many more countries and people to VALR’s wide array of crypto asset services and infrastructure,” said Farzam Ehsani, Co-Founder and CEO of VALR. “Mobile money has already reshaped financial access across the African continent. By enabling direct connections in local currencies, we offer millions a practical pathway to Bitcoin, stablecoins, tokenised gold, and more, as well as innovative financial tools, supporting greater economic participation for everyone.”

Onafriq’s Founder and CEO, Dare Okoudjou, highlighted the significance of the partnership for financial connectivity across the continent. “We are truly excited to welcome VALR onto the Onafriq Network, enabling their clients across Africa to transact freely with the 1bn mobile wallet users and hundreds of thousands of businesses already on Onafriq’s network. VALR is a recognised pioneer and leader of Blockchain and Stablecoin technologies on the continent and we look forward to working with them to bring the many benefits of these technologies to people and businesses across Africa.”

By Adedapo Adesanya and Modupe Gbadeyanka

The Central Bank of Nigeria (CBN) has described rumours that Polaris Bank Limited failed to meet the recapitalisation deadline on March 31, 2026, as fake news.

The banking sector regulator in a post via its social media handle on X, formerly known as Twitter, on Thursday also said reports that notable businessman, Mr Razaq Okoya, was planning to acquire the financial institution were false.

There were reports on Wednesday that Polaris Bank, which was created after the operating licence of Skye Bank was revoked by the CBN in 2018, could not meet the deadline to raise its capital base.

The central bank gave banks two years to increase their minimum capital requirements based on their licence coverage.

For lenders with an international licence, they were to boost their capital base from N25 billion to N500 billion, while national banks were asked to have at least N200 billion, with regional lenders N50 billion.

The deadline was March 31, 2026, and according to the CBN, about 33 banks scaled through, raising about N4.65 trillion.

An X user had written that, “Polaris Bank is currently undergoing a liquidation process for not able to comply with the Central Bank of Nigeria recapitalisation requirements, and the bank would be put under NDIC to be liquidated. The bank licence might also be revoked soon. But billionaire Razaq Okoya has made a bid to purchase the bank, reinstate it, [and] also to comply with the CBN requirements. This deal is said to be finalised the moment NDIC and other shareholders agree with what Razaq Okoya is ready to offer.”

While reacting to the above, the CBN said, “This content is fake. Let the public be guided. The Nigerian banking system is safe and secure.”

In 2024, the banking sector regulator appointed new chief executives for three banks, including Polaris Bank, after the dissolution of their boards and managements over the non-compliance of these banks and their respective boards with the provisions of Section 12(c), (f), (g), (h) of the Banks and Other Financial Institutions Act, 2020. The others were Union Bank and Keystone Bank.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn