Banking

Ecobank, Code 14 Labs to Deepen Coding Education in Nigeria

By Modupe Gbadeyanka

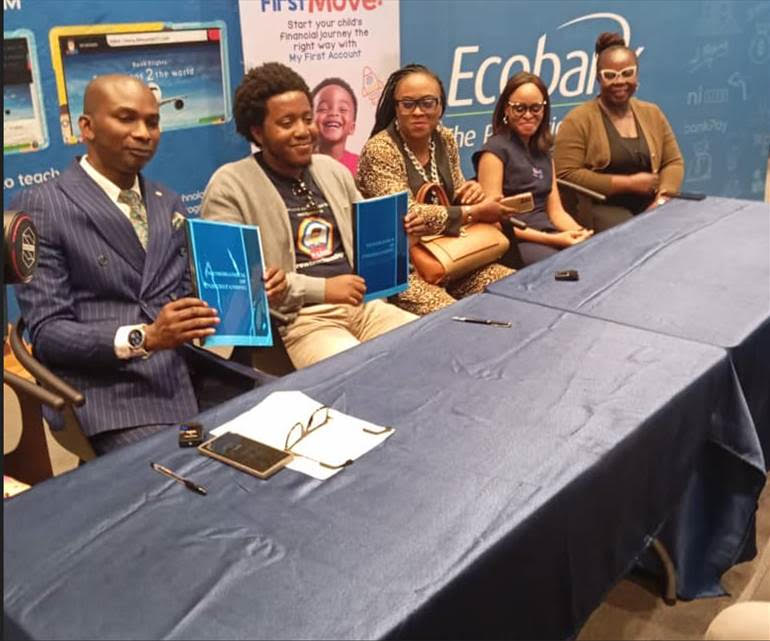

Efforts are being made by Ecobank Nigeria and Code 14 Labs to deepen coding education in the country by providing affordable annual training and proficiency certification to students.

The lender, in a statement, said it would provide nationwide and pan-African access to coding education, utilizing its extensive operational network across the continent.

In turn, Code 14 Labs will supply its educational technology and trusted community to ensure high-quality teaching that delivers tangible learning outcomes for students and reassurance for parents.

Both parties recently met in Lagos to seal a Memorandum of Understanding (MoU) to kick off the partnership.

Parents and guardians wishing to have their wards participate in the programme are encouraged to open Ecobank’s MyFirst Account—a specialized high yield savings product designed for children under 16.

The Head of Consumer Banking at Ecobank Nigeria, Ms Aeola Ogunyemi, who represented the Head of Consumer Products and Segments, Mr Victor Yalokwu, said the collaboration reflects the bank’s commitment to bridging the digital divide, promoting inclusion, and preparing the next generation for a tech-driven future.

He also highlighted how the collaboration aligns with Ecobank’s mission to equip children with the skills necessary to thrive in an increasingly digital world.

“At Ecobank, we recognize that financial literacy and digital education are intertwined. This belief led to the creation of the MyFirst Account, a product aimed at children under 16 to encourage smart financial habits from an early age.

“By introducing students to coding through Code 14’s innovative mobile app, we’re not just teaching coding skills, but also nurturing problem-solving abilities, creativity, and digital confidence,” Mr Yalokwu noted.

The Executive Director of Research and Technology at Code 14 Labs, Mr Otaru Daudu, praised the partnership and expressed confidence that, with the support of additional partners like the British Council and the Teachers Registration Council of Nigeria (TRCN), they will achieve their goal of training 50,000 learners to proficiency level in HyperText Markup Language (HTML) and Cascading Style Sheets (CSS), essential programming languages for global internet communication.

He emphasised that Code 14 Labs is committed to scaling critical education components through technology-driven inclusion.

By Adedapo Adesanya

Nigerian business-banking unicorn, Moniepoint, is eyeing a considerable foothold in East Africa as it completed the acquisition of a 78 per cent stake in Kenya’s Sumac Microfinance Bank.

The deal was finalised on Thursday and provides Moniepoint with a deposit-taking licence, an essential requirement for its credit-led expansion strategy.

The acquisition of Sumac allows Moniepoint to bypass the Central Bank of Kenya’s (CBK) policy to halt new licences to new foreign players. It will also ease worries after its move to buy payments firm Kopo Kopo failed.

By securing a majority stake in the 20-year-old institution, Moniepoint gains the regulatory infrastructure needed to deploy its high-velocity lending model to Kenya’s small and medium -sized enterprises (SMEs).

Sumac is a tier-three lender, and with its existing branch network and regulatory standing, the lender offers Moniepoint one of the ways to scale in a region increasingly shaped by digital-first credit.

The move also signals the company’s ambition to build a cross-border ecosystem that captures the entire merchant value chain, rather than solely on transaction fees.

Moniepoint’s entry into Kenya follows its acquisition of Orda, a cloud-based restaurant software provider for an undisclosed sum earlier this week, in a push to tap into the billion-dollar restaurants’ economy.

The company plans to export its business-in-a-box strategy, which integrates inventory management, payroll, and working capital by combining Orda’s vertical Software as a Service (SaaS) capabilities with Sumac’s banking infrastructure.

Orda will be rebranded Moniebook for Restaurants and integrated into Moniebook, Moniepoint’s business management platform. Orda will continue to operate as a standalone business until the full integration is completed in the coming months.

Orda currently operates in Nigeria and Kenya, but the acquisition only covers its Nigerian operations. However, with its presence in Kenya, it may set the tone for the acquisition of that subsidiary.

By Adedapo Adesanya

The Governor of the Central Bank of Nigeria (CBN), Mr Yemi Cardoso, said the central bank would now focus on a five-point policy agenda aimed at consolidating recent macroeconomic gains and steering the country toward sustained stability.

Mr Cardoso, while speaking at the 2026 Monetary Policy Forum held in Abuja on Thursday, set out the lender’s next phase of reforms anchored on inflation control, exchange rate stability, stronger reserves, deeper financial markets, and improved policy effectiveness.

The forum, themed Strengthening Nigeria’s Macroeconomic Stability Through Effective Monetary Policy: The Roles of Critical Stakeholders, brought together fiscal authorities, financial institutions, private sector players, and development partners.

He said the CBN will be positioning its five-point agenda as the cornerstone of the next phase of economic management.

Mr Cardoso said while recent reforms had delivered measurable improvements across key indicators, the focus had now shifted to consolidation.

He identified the five priorities as anchoring inflation firmly on a downward path to single-digit levels, sustaining exchange rate stability, strengthening external reserves through organic inflows, deepening interbank market development, and enhancing the transmission of monetary policy.

According to Mr Cardoso, the priorities reflect a deliberate strategy to entrench stability and improve the efficiency of the monetary framework. “The journey is far from complete. Our next phase is focused on consolidation,” Cardoso said, stressing that maintaining discipline and consistency would be critical to achieving durable outcomes.

He noted that the bank’s tightening measures and foreign exchange reforms had already begun to yield results, with inflation moderating, reserves strengthening, and market confidence improving.

However, he cautioned that sustaining these gains would require strong coordination between monetary and fiscal authorities.

Mr Cardoso emphasised that macroeconomic stability could not be achieved in isolation, describing it as a shared responsibility among policymakers, financial institutions, and the broader economic system.

He said disciplined fiscal operations, aligned policy actions, and continuous stakeholder engagement would be essential in delivering on the Bank’s objectives.

The CBN governor also highlighted the importance of deepening the interbank market to improve liquidity distribution and enhance the effectiveness of policy signals across the financial system.

He added that strengthening monetary policy transmission mechanisms would ensure that policy decisions translate more efficiently into real sector outcomes, including price stability and economic growth.

On external buffers, Mr Cardoso said the bank would continue to prioritise reserve accretion through sustainable sources, including improved foreign exchange inflows and enhanced market confidence. He explained that stronger reserves would provide a critical cushion against external shocks and support exchange rate stability.

The CBN chief further stressed that the success of the consolidation phase would depend on sustained collaboration across institutions.

He reaffirmed the apex bank’s commitment to orthodox monetary policy, transparency, and institutional credibility, noting that the reforms undertaken so far were necessary to correct past distortions and lay the foundation for long-term economic resilience.

By Modupe Gbadeyanka

In a bid to strengthen the Naira and ensure transparency, traceability, and effective monitoring of all transactions, the Central Bank of Nigeria (CBN) has directed all International Money Transfer Operators (IMTOs) in the country to open Naira settlement accounts for all transactions.

In a circular dated Tuesday, March 24, 2026, the apex bank said IMTOs have till May 1, 2026, to fully adhere to this directive and others.

It noted that transactions must be “routed strictly through their designated settlement accounts, maintained with Authorised Dealer Banks (ADBs) in Nigeria.”

With this development, diaspora remittances must be paid to beneficiaries in the local currency.

“All transactions arising from international money transfer operations, including disbursements to beneficiaries and any related settlements, must be processed exclusively through the IMTO’s settlement account(s) held with any ADB of their choice.

“IMTOs may use their discretion to designate their existing accounts or open new settlement accounts and may operate accounts with multiple ADBs in line with their business strategy,” the central bank emphasised.

“Settlement accounts shall only be credited with remittance flows and proceeds of foreign exchange conversions by licensed IMTOs (or their agents) with authorised market participants in the Nigerian Foreign Exchange Market (NFEM),” the notice also declared.

It stressed further that, “IMTOs shall ensure that their settlement accounts are properly designated for this purpose and operated in accordance with existing regulatory guidelines. A list of designated settlement accounts shall be advised by each licensed 1MTO to the Director, Trade and Exchange Department, and updated regularly as necessary.”

The CBN said to “support market efficiency and enhance pricing outcomes for 1MTO transactions, ADBs may process foreign currency transfers from 1MTO settlement accounts to other ADBs and approved market participants, including licensed BDCs.”

“IMTOs shall observe real-time market prices from the Bloomberg BMATCH and utilise this as guidance for pricing transactions with their customers and Authorised Dealers.

“This will improve price discovery, reduce information asymmetry between 1MTOs and banks, and encourage increased participation in the official FX market,” the disclosure stated.

Concluding, the apex bank said, “All IMTOs are required to ensure full compliance with this directive and maintain adequate records of related transactions for regulatory review and audit purposes,” reminding them to “maintain acceptable standards and comply with AML/CFT/CPF requirements.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn