Banking

Nigerian Banks Have 45,350 Contract Staff—Report

By Modupe Gbadeyanka

A report recently released by the National Bureau of Statistics (NBS) has showed that the number of contract staff in the Nigerian banking industry stood at 45,350 as at December 31, 2019.

According to the report, the number increased 5.03 percent from the figures realized in the third quarter of last year and marginally rose by 0.25 percent year-on-year.

Business Post gathered that in Q3 2019, the total number of contract staff in the sector stood at 43,180, and 45,238 in the fourth quarter of 2018.

In the period under review, according to the data released by the stats office last week, the total number of persons employed by banks in the country were 103,610.

Of these figures, 184 are in the executive cadre, 18,180 in the senior cadre, while 39,896 are in the junior cadre.

When Business Post put these categories of the workforce in percentage, it was discovered that contract staff accounted for 43.77 percent of the total employees in the nation’s banking sector, 38.51 percent accounted for the junior level, 17.55 percent accounted for the senior cadre, while 0.18 percent accounted for the executive category in Q4 2019.

In the preceding quarter, Q3 of 2019, the total workforce of the banking sector was 101,435, comprising 186 executive staff, 17,671 senior staff, 40,398 junior staff and 43,180 contract staff.

In the fourth quarter of 2018, the total workforce of the industry stood at 104,669 consisting of 201 in the executive level, 18,119 in the senior level, 41,111 in the junior level and 45,238 in the contract category.

Meanwhile, the NBS said in the last quarter of 2019, data on Electronic Payment Channels in the Nigeria banking space revealed that a total volume of 893,681,888 transactions valued at N48.54 trillion were recorded and it was discovered that NIBSS Instant Payments (NIP) transactions dominated the volume of transactions recorded, pulling 342,636,006 valued at N29.69 trillion.

Cheques pulled 1,936,030 worth N1.111 trillion, ATM recorded 202,373,808 transactions worth N1.651 trillion, POS recorded 129,574,015 transactions valued at N964.3 billion, Web had 28,827,240 transactions valued at N133.7 billion, mobile payments had 159,423,943 transactions worth N1.687 trillion, REMITA recorded 13,757,571 transactions valued at N5.908 trillion, while Central Pay had 153,370 transactions worth N1.4 billion.

Also, in the report, it was stated that in terms of credit to private sector, the total value of credit allocated by the bank stood at N17.19 trillion as at Q4 2019.

A breakdown showed that Oil & Gas and Manufacturing sectors got credit allocation of N3.42 trillion and N2.62 trillion respectively to record the highest credit allocation as at the period under review.

By Modupe Gbadeyanka

Monday, March 9, 2026, has been fixed by Zenith Bank Plc for its annual International Women’s Day seminar in Lagos.

The event is part of activities lined up to commemorate the 2026 International Women’s Day, themed Give to Gain.

The theme prepared for Zenith Bank’s programme is Take it, You Own it, and was designed to deepen meaningful engagement around women’s empowerment, leadership, and sustainable impact.

The workshop will include segments focused on leadership insight, professional empowerment, wellbeing, and collaboration, offering attendees opportunities to engage deeply with thought leadership and practical strategies for advancing equity.

With a carefully curated programme spanning keynote addresses, panel conversations, Q and A sessions, and creative interludes, Zenith Bank’s 2026 International Women’s Day Seminar promises to be a catalyst for meaningful action.

“International Women’s Day is a reminder that progress requires intentionality.

Give to Gain speaks to the responsibility institutions have to create real opportunities, while our theme, Take It, You Own It, challenges women to step forward boldly and lead.

“At Zenith Bank, we are deliberate about building environments where women are supported to grow, thrive, and shape outcomes, not only within our institution but across the communities and industries we serve,” the chief executive of Zenith Bank, Ms Adaora Umeoji, stated.

Over the years, the lender’s International Women’s Day initiatives have brought together women leaders, professionals, entrepreneurs, and emerging talents for dynamic dialogue, inspiration, and shared learning around gender equity, professional growth, and inclusive opportunity.

More than a commemorative gathering, the 2026 seminar is designed as a convergence of influence, insight, and inspiration, bringing together accomplished women and progressive leaders across business, governance, creative industries, technology, and social impact.

By Modupe Gbadeyanka

As part of activities commemorating International Women’s Day 2026, Ecobank Nigeria has improved its multi-award-winning gender financing initiative, Ellevate by Ecobank.

Originally launched to improve access to finance for women-owned, women-led, and women-focused small and medium-sized enterprises (SMEs) within its commercial banking segment, the enhanced Ellevate programme now adopts a broader, more inclusive structure.

The new framework extends across all business segments, positioning Ellevate as a comprehensive ecosystem designed to address the structural financing and growth barriers faced by women entrepreneurs.

The upgraded programme reinforces the bank’s long-term commitment to advancing women-led enterprises in Nigeria and across Ecobank’s pan-African footprint.

Under the expanded structure, beneficiaries will enjoy improved access to credit on competitive terms, including more flexible collateral considerations aimed at easing traditional financing constraints. Beyond lending, the programme integrates digital payment, collections, and cash management solutions to enhance operational efficiency and support scalability.

A core pillar of the enhancement is structured market access. Through the bank’s MyTradeHub online matchmaking platform and e-commerce enablement capabilities, women entrepreneurs will be better positioned to connect with customers and trade partners across Africa, facilitating cross-border expansion and participation in regional value chains.

The initiative also incorporates robust non-financial support mechanisms, including targeted training programmes, leadership development sessions, and knowledge-sharing platforms to strengthen managerial capacity and long-term sustainability.

This is complemented by access to customised wealth management advisory services, integrated insurance solutions, and a loyalty framework offering commercial incentives through select retail and lifestyle partnerships.

“Since its launch in Nigeria in July 2021, Ellevate has delivered meaningful impact for SMEs and women-led businesses.

“This next phase deepens our value proposition and reinforces our resolve to remain the preferred financial partner for women entrepreneurs,” the Managing Director of Ecobank Nigeria, Mr Bolaji Lawal, said.

“African businesswomen deserve world-class banking solutions that drive turnover, profitability, and sustainable growth. Our approach goes beyond financial inclusion to building an enabling ecosystem that enhances competitiveness and long-term resilience,” he added.

He further highlighted that Ecobank Nigeria consistently hosts flagship platforms such as Adire Lagos, Oja Oge, +234Art Fair, the Lagos Pop-Up Museum, SME Bazaar, and the Design & Build Exhibition, which provide prominent opportunities for showcasing and elevating women-owned businesses.

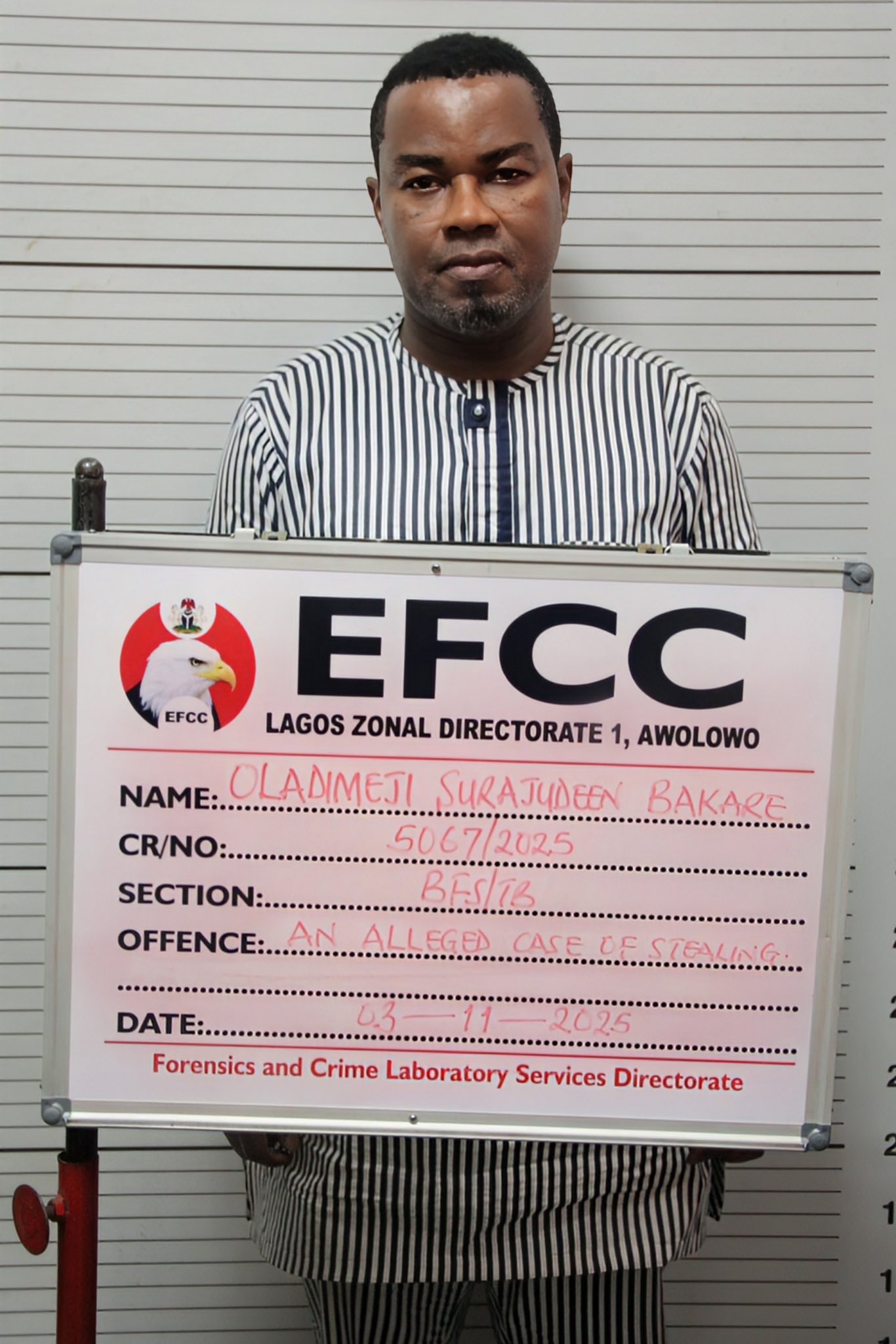

By Modupe Gbadeyanka

Two employees of FSDH Merchant Bank Limited, Mr Bakare Oladimeji Surajudeen and Mr James Olukayode Imokwede, have been arraigned by the Economic and Financial Crimes Commission (EFCC).

The suspects were brought before Justice Ismaila Ijelu of the Lagos State High Court sitting in Ikeja on Tuesday, March 3, 2026.

They were accused of stealing and retaining stolen property valued at about $306,667.81 and €50,250.

The EFCC, which received a petition from the lender, said its investigations showed that the suspects processed fraudulent transfers through the SWIFT platform to third parties.

The bank said an internal audit uncovered unauthorised debits totalling $306,667.81 and €50,250, equivalent to N527.4 million from its Letters of Credit (LC) payable accounts.

At the court yesterday, after the defendants pleaded “not guilty” to all 10-count charges preferred against them, the prosecution counsel, H. U. Kofarnaisa, asked for a trial date and also prayed that the defendants be remanded in a correctional facility pending trial.

Counsel to the first and second defendants, Oluwaseun Akintunde and Olajide S. Onasanya, informed the court that bail applications had been filed on behalf of the defendants and also urged the court to grant them bail on liberal terms.

They also prayed that the defendants be remanded in the EFCC custody pending the perfection of their bail conditions.

The prosecution counsel, however, opposed the prayers of the defence seeking the remand of the defendants in the EFCC custody, saying that “the EFCC detention facilities are overstretched.”

After listening to both parties, Justice Ijelu granted the defendants bail in the sum of N2 million each, with two sureties in like sum.

The court ordered that one of the sureties must be a relative who is gainfully employed. The sureties must provide evidence of tax payment in the last three years and must show proof of livelihood, with their residences verified.

The defendants were ordered to deposit their international passports with the court, and must not travel outside the country without the leave of the court.

The judge subsequently remanded the defendants in a correctional facility pending the perfection of their bail conditions, and adjourned the matter till March 25, 2026, for the commencement of trial.

Business Post reports that one of the counts said, “That you, Bakare Oladimeji Surajudeen and James Olukayode Imokwede, sometime in 2021 in Lagos within the jurisdiction of this court, dishonestly took the sum of N527,406,916.66, property of FSDH Merchant Bank Limited.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn