Economy

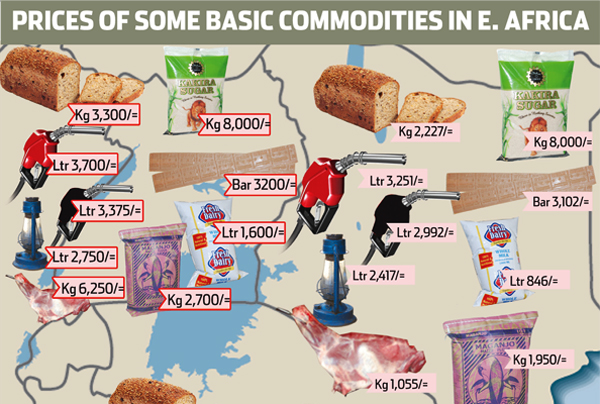

Drought Pushing Food Prices up Sharply in East Africa

By Dipo Olowookere

Drought throughout East Africa has sharply curbed harvests and pushed the prices of cereals and other staple foods to unusually high levels, posing a heavy burden to households and special risks for pastoralists in the region.

Local prices of maize, sorghum and other cereals are near or at record levels in swathes of Ethiopia, Kenya, Somalia, South Sudan, Uganda and the United Republic of Tanzania, according to the latest Food Price Monitoring and Analysis Bulletin (FPMA).

Inadequate rainfall in most areas of the sub-region has put enormous strain on livestock and their keepers. Poor livestock body conditions due to pasture and water shortages and forcible culls mean animals command lower prices, leaving pastoralists with even less income to purchase basic foodstuffs.

“Sharply increasing prices are severely constraining food access for large numbers of households with alarming consequences in terms of food insecurity,” said Mario Zappacosta, FAO senior economist and coordinator of the Global Information and Early Warning System.

The trends in East Africa, where prices of staple cereals have doubled in some town markets, stand in marked contrast to the stable trend of FAO’s Food Price Index, which measures the monthly change in international prices of a basket of traded food commodities.

The difference is due to the drought that is hammering the sub-region, where food stocks were already depleted by the strong El Niño weather event that ended only last year. Poor and erratic rainfall in recent months, crucial for local growing seasons, are denting farm output.

Somalia’s maize and sorghum harvests are estimated to be 75 percent down from their usual level, and some 6.2 million people, more than half of the country’s total population, now face acute food insecurity, with the majority of those most affected living in rural areas.

Soaring prices

The FPMA Bulletin tracks food price trends on a granular level and in local terms, with an eye to flagging instances where the prices of essential food commodities increase sharply or are abnormally high.

In Mogadishu, prices of maize increased by 23 percent in January, and. the increase was even sharper in the main maize producing region of Lower Shabelle. Overall, in key market towns of central and southern Somalia, coarse grain prices in January have doubled from a year earlier.With an earlier than usual depletion of household stocks during the coming lean season and preliminary weather forecasts raising concerns for the performance of the next rainy season, prices are likely to further escalate in the coming months.

Maize prices in Arusha, United Republic of Tanzania, have almost doubled since early 2016, while they are 25 percent higher than 12 months earlier in the country’s largest city, Dar Es Salaam.

In South Sudan, food prices are now two to four times above their levels of a year earlier, exacerbated by ongoing insecurity and the significant depreciation of the local currency.

In Kenya, where eastern and coastal lowlands as well as some western areas of the Rift Valley all suffered below-average rainfall, maize prices are up by around 30 percent, with the increase somewhat contained somewhat thanks to sustained imports from Uganda.

Cereal prices aren’t the only ones rising. Beans now cost 40 percent more in Kenya than a year earlier, while in Uganda – where maize prices are now up to 75 percent higher than a year earlier – and increasing around the key border trading hub of Busia, the prices of beans and cassava flour are both about 25 percent higher than a year ago in the capital city, Kampala.

Double jeopardy for pastoralists

Drought-affected pastoral areas in the region face even harsher conditions.

In Somalia, goat prices are up to 60 percent lower than a year ago, while in pastoralist areas of Kenya the prices of goats declined by up to 30 percent over the last twelve months.

Shortages of pasture and water caused livestock deaths and reduced body mass, prompting herders to sell animals while they can, as is also occurring in drought-wracked southern Ethiopia. This also pushes up the prices of milk, which is, for instance, up 40 percent on the year in Somalia’s Gedo region.

Lower income from livestock collides with higher prices for cereals and other staple foods in a wrenching shock to terms of trade for pastoralist households. A medium-sized goat in Somalia’s Buale market was worth 114 kilograms of maize in January 2016, but at today’s prices can be traded for only 30 kilograms of the grain.

FAO uses its proprietary FPMA Tool, accessible to the public online, to monitor local markets and gather data for more than 1350 domestic price series in 91 countries around the globe in order to produce its Indicator of Food Price Anomalies.

By Adedapo Adesanya

Crude oil plummeted on Wednesday on hopes of the reopening of the Strait of Hormuz after US President Donald Trump agreed to a two-week ceasefire with Iran.

Brent crude futures moderated to $94.75 a barrel, while the US West Texas Intermediate (WTI) crude eased to $94.41 a barrel.

President Trump said on Wednesday that the US will work closely with Iran and will be talking about tariff and sanctions relief with Iran.

However, analysts cautioned that the ceasefire is a temporary two-week reprieve rather than a permanent resolution, and the global energy system remains fragile due to structural damage to regional infrastructure.

Reuters reported that Iran could open the strait in a limited and controlled way on Thursday or Friday ahead of a meeting between U.S. and Iranian officials in Pakistan.

Agence France-Presse (AFP) reported that two ships appeared to have transited the Strait of Hormuz since the US-Iran ceasefire deal. A Greek-owned bulk carrier and a Liberia-flagged vessel both transited the waterway early on Wednesday.

Meanwhile, Israel carried out its heaviest strikes on Lebanon since the conflict with Hezbollah broke out last month, even as the Iran-aligned group paused attacks on northern Israel and Israeli troops in Lebanon under the ceasefire.

Also, Saudi Arabia’s East-West Pipeline, a critical artery bypassing the Strait of Hormuz, was reportedly hit in an Iranian drone attack. Prior to the attack, the pipeline was pumping at its emergency capacity of 7 million barrels per day to bypass the shuttered strait.

The strikes occurred just hours after a US-Iran ceasefire announcement, which has so far failed to halt regional hostilities. Other facilities in the kingdom were also targeted in the wave of strikes, which the Islamic Revolutionary Guard Corps (IRGC) claimed included oil facilities owned by American companies in Yanbu.

US crude stocks rose by 3.1 million barrels to 464.7 million barrels during the week ended April 3, the Energy Information Administration (EIA) said.

By Adedapo Adesanya

The National Insurance Commission has issued new guidelines for the collection, management, and administration of the Insurance Policyholders’ Protection Fund.

In a circular issued to all insurance institutions on Tuesday, the regulator also set May 31, 2026, as the deadline for insurers to submit their assessment returns for the 2025 financial year.

Recall that on August 5, 2025, President Bola Tinubu signed into law the Nigerian Insurance Industry Reform Act ( NIIRA 2025).

This landmark legislation repeals the Insurance Act 2003, and consolidates related provisions, ushering in a modern regulatory framework. It lays a strong foundation for sustainable growth and increased investment in the country’s insurance sector.

The commission said the guidelines were issued in exercise of its powers under the 2025 Act and other existing insurance laws and regulations to provide regulatory clarity, improve guidance, and ensure ease of compliance across the industry.

According to NAICOM, the guidelines establish a comprehensive structure for the operation of the IPPF, which serves as a statutory safety net to protect insurance policyholders in the event of distress or insolvency of a licensed insurer or reinsurer. The framework also provides direction on the reimbursement of loans by insurers and reinsurers.

NAICOM stated, “The guidelines ensure regulatory clarity, guidance and ease of compliance, as it provides a comprehensive regulatory framework for the collection, management, and administration of the Fund, which serves as a statutory safety net designed to protect insurance policyholders against distress and insolvency of a licensed insurer or reinsurer, including guidance for the reimbursement of loans by an insurer or reinsurer.

“Please be informed that the IPPF Assessment Returns in respect of the year 2025 shall be submitted to the Commission not later than 31st May 2026, while subsequent submissions shall be in line with Section 4.3 of the Guideline on Insurance Policyholders Protection Fund.”

By Adedapo Adesanya

The Dangote Refinery on Wednesday returned the petrol price to N1,200 per litre, less than 24 hours after it increased it by 5 per cent.

The private refinery had raised the ex-depot price by N75 on Tuesday, citing pressure from volatile global oil markets, but quickly brought it back to N1,200 per litre from N1,275 per litre.

The swift downward review is directly linked to a sharp drop in international crude prices. Brent crude has plunged to $95.05 per barrel, after a 13 per cent decline, while the US West Texas Intermediate (WTI) crude closed at $97.18, recording nearly a 14 per cent drop.

This development comes after US President Donald Trump announced a conditional two-week ceasefire with Iran, which eased fears of immediate supply disruptions in the global oil market.

“This will be a double-sided CEASEFIRE!” Trump said on social media, marking a sharp reversal from his earlier warning that “a whole civilisation will die tonight” if Iran failed to comply with US demands.

Iran’s Foreign Minister, Mr Abbas Araqchi, confirmed that the country would halt attacks provided strikes against Iran cease and transit through the Strait of Hormuz is coordinated by Iranian forces.

Despite the breakthrough, tensions remain elevated across the region, with several Gulf states reporting missile launches, drone activity, or issuing civil defence warnings.

While oil prices have fallen back below $100, they remain significantly elevated after surging by a record amount in March. Market analysts noted that regardless of how successful the ceasefire is, geopolitical risk related to the Strait of Hormuz is likely to remain elevated for the foreseeable future under the control of Iran.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn