Economy

ENGIE, Fenix Seal Acquisition to Power African Homes

By Dipo Olowookere

The duo of ENGIE and Fenix International have completed their acquisition agreement aimed at providing delivered clean, safe and affordable energy and financial services to over one million people living in Africa.

The deal will accelerate and expand Fenix’s ability to scale off-grid energy and financial services and allow the firm gain access to ENGIE’s supply chain, expertise, long-term capital investments and talent across the energy value chain.

While ENGIE is a global utility company, Fenix International, on the other hand, is an off-grid energy leader.

Fenix is the first Solar Home System (SHS) company to join a major worldwide energy company.

Aligned with ENGIE’s core values, the Fenix team and mission will remain unchanged and at the heart of the company. Fenix headquarters and key offices are anchored in Africa, close to their customers and operations, so that Fenix can continue its pursuit of an exceptional customer experience.

CEO of ENGIE Africa, Bruno Bensasson, stated that, “Closing this acquisition gives us the go-ahead to accelerate access to energy through Fenix’s strong solar home system model. Until now, availability of capital has been a major hurdle in the solar home system business, a constraint that we are now helping to remove.

“We believe this is a major step along the path to universal energy access. The dramatically falling price of solar panels and batteries, combined with the inclusive “pay-as-you-go” financing platform created by Fenix, make solar home systems a key part of the energy mix for Africa’s future in combination with grid extension and micro-grids.”

“Lyndsay Handler, CEO of Fenix International, said, “It’s unacceptable that over 600 million people across Africa lack access to energy. By joining forces with ENGIE, we aim to bring affordable energy and other life-changing products to millions of people living off-grid.

“Realizing this ambitious vision will require significant commercial investment and innovation in product, last-mile distribution, inclusive financing and customer experience. With this agreement, ENGIE will provide the support, expertise and opportunities the Fenix team needs to innovate in these areas and rapidly scale the business.”

Fenix’s flagship product, ReadyPay Power, is one of the most affordable solar home systems on the off-grid market. Customers pay as little as $0.19 per day to access power for lighting, phone charging, and products such as TVs and radios.

After 24-36 months of payments, customers own the solar home system outright. Based on the credit score customers establish while paying off their power systems, they are able to purchase upgrades to their energy system, energy-efficient appliances, or other life-changing financial products.

ReadyPay Power, by providing off-grid families with clean, affordable energy and a safer home environment, is a natural fit with ENGIE’s goal to provide decarbonised, decentralised energy using the latest digital technologies.

As Fenix officially joins the ENGIE group of companies, Lyndsay said further that, “It is a privilege to be a part of a bold global energy company with over 50 years’ experience with energy in Africa. Over 100 years ago, Ford set out on a mission to make cars affordable in America.

“MTN have made telecommunications and Mobile Money affordable to all across Africa, and today Tesla is working to make rockets and electric cars affordable. Together, Fenix and ENGIE want to make modern energy radically affordable to all.”

By Adedapo Adesanya

Manufacturers are yet to benefit from relief on the burden of multiple taxes and levies despite the enactment of the Nigeria Tax Act 2025, according to the Manufacturers Association of Nigeria (MAN).

The association, in its Manufacturers CEO Confidence Index (MCCI) report for the second quarter of 2026, said manufacturers continued to face multiple tax collectors and regulatory agencies during the period.

Director-General of MAN, Mr Segun Ajayi-Kadir, said the new tax law, which was expected to reduce the burden of multiple taxation, had yet to deliver the intended benefits.

“Manufacturers complained that they were still met with multiple tax collectors and regulators in Q2 2026. It follows that the implementation of the Nigeria Tax Act 2025 is yet to achieve its objective of relieving manufacturers of the burden of taxes and levies,” he said.

According to the report, Nigeria’s business environment remains largely unsupportive of manufacturing growth, with local sourcing of raw materials emerging as the only indicator that recorded noticeable improvement.

MAN, however, warned that the gains in local sourcing could be undermined by worsening insecurity in parts of the country.

The association attributed the improvement largely to persistent foreign exchange constraints, which have forced many manufacturers to source inputs locally.

Despite this, it said excessive regulation and multiple taxation continue to weigh heavily on manufacturers.

The report showed that manufacturers recorded a modest increase in sales volume during the second quarter, but rising production, distribution and logistics costs continued to erode profitability.

It added that capacity utilisation, production levels, investment and employment remained broadly unchanged during the review period.

MAN further observed that although recent foreign exchange reforms had helped stabilise the naira, inadequate foreign currency supply remained a major constraint to manufacturing operations.

Other key challenges identified in the report include poor infrastructure, high production costs, raw material shortages and unfavourable trade policies.

The association said the findings underscore the continued pressure on manufacturers despite recent fiscal and foreign exchange reforms, stressing the need for more effective implementation of policies aimed at improving the operating environment for the real sector.

By Adedapo Adesanya

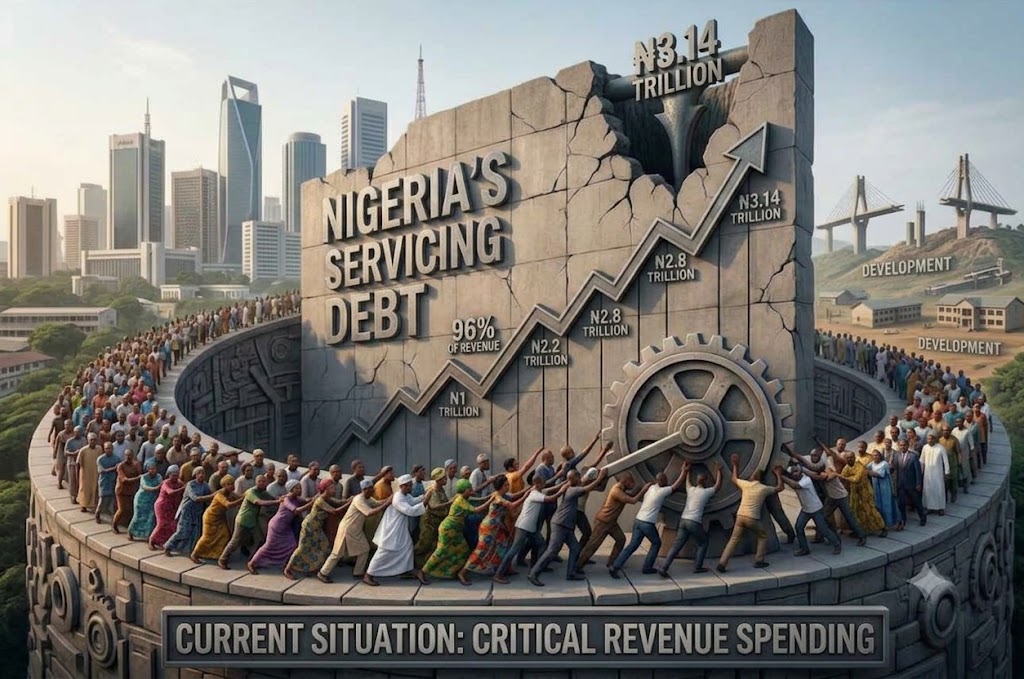

The federal government spent N3.14 trillion on servicing its domestic debt in the first quarter (Q1) of 2026, according to the Debt Management Office (DMO).

The figure, contained in the DMO’s latest domestic debt service report for Q1 2026, comprised N2.97 trillion in interest payments and N169.68 billion in principal repayments.

According to the report, the government spent N741.82 billion on domestic debt service in January before the figure rose to N967.67 billion in February.

Debt service increased further to N1.43 trillion in March, bringing total spending for the quarter to N3.14 trillion.

The March figure represented a 47.7 per cent increase from the N967.67 billion recorded in February and was 92.7 per cent higher than the N741.82 billion spent in January.

The debt office said interest payments accounted for approximately 94.6 per cent of the total domestic debt service during the quarter.

Treasury bills accounted for the largest share of interest payments at N1 trillion, while interest payments on Federal Government bonds stood at N1.96 trillion.

The government also paid N4.24 billion in interest on FGN savings bonds during the period.

The debt management body said the principal component of the debt service comprised N169.68 billion in repayments on local-denominated promissory notes.

Overall, domestic debt service rose significantly throughout the quarter, with March alone accounting for nearly half of the N3.14 trillion spent between January and March.

By Aduragbemi Omiyale

The Director-General of the Securities and Exchange Commission (SEC), Mr Emomotimi Agama, has outlined how the Federal Capital Territory Administration (FCTA) can leverage Nigeria’s capital market to raise long-term funds for critical infrastructure projects instead of relying solely on annual budgetary allocations.

According to Mr Agama, the capital market offers the FCT a sustainable financing model for roads, rail, housing, water, transport and other infrastructure through instruments such as infrastructure bonds, green bonds, real estate investment trusts (REITs), asset recycling and tokenised municipal securities.

Speaking at the Abuja Business and Investment Summit and Expo (ABIE 2026) in Abuja, the SEC chief noted that Abuja’s development demonstrates that economic growth is driven by investment, stressing that “cities are not built by budgets alone. Cities are built by capital markets.”

He advised the FCT to establish a long-term infrastructure bond programme backed by dedicated revenue sources such as ground rents, tenement rates, tolls, parking fees and land-use charges, noting that this would enable the territory to finance major projects without overburdening annual budgets.

“A budget can only spend what a single year has collected. A bond can spend what 30 years will collect,” Mr Agama said, explaining that infrastructure projects generate long-term economic value that can be used to service debt over time.

The SEC boss said the territory could also access cheaper financing through green and sustainability-linked bonds for projects including mass transit, light rail, solar-powered street lighting, waste-to-energy facilities and water infrastructure.

He further proposed the creation of an FCT Real Estate Investment Trust to unlock value from Abuja’s extensive property portfolio while giving ordinary Nigerians an opportunity to invest in the city’s real estate market.

Mr Agama also urged Abuja Investments Company Limited (AICL) to consider listing some of its businesses or establishing a listed infrastructure fund, saying this would raise capital without increasing government debt while improving corporate governance and transparency.

On the long-abandoned Millennium Tower project, he said the estimated over N400 billion completion cost should not be viewed as a budgetary burden but as an investment opportunity that could be financed through a special purpose vehicle and offered to investors via the capital market.

“The question is not whether Nigeria can afford the Millennium Tower. The question is whether we will let ordinary Nigerians own it,” he said.

Mr Agama further proposed an asset recycling programme under which completed income-generating public assets, including terminals, markets, commercial properties and the International Conference Centre, could be securitised or concessioned to institutional investors, with proceeds reinvested in new infrastructure.

He also called on the FCT to pioneer a regulated tokenised municipal bond programme that would allow citizens to invest as little as N10,000 through mobile phones in specific infrastructure projects.

According to him, the recently enacted Investments and Securities Act (ISA) 2025 has strengthened the legal framework for sub-national governments to access the capital market while providing enhanced investor protection and clearer regulation of digital assets.

Mr Agama disclosed that Nigeria’s capital market has grown significantly, with total market capitalisation exceeding N217 trillion as of May 2026, comprising about N160.5 trillion in equities and N56.7 trillion in bonds.

He said recent reforms, including the migration to a T+1 settlement cycle and regulatory measures to deepen market participation, have improved market efficiency and strengthened investor confidence.

The SEC DG assured the FCTA of the commission’s readiness to provide technical support for structuring and registering capital market instruments, saying the agency would work closely with the territory to unlock financing for infrastructure projects.

He added that Nigeria’s capital market remains critical to mobilising domestic savings for national development, insisting that “money is not scarce; delivery capacity is scarce, and financing follows delivery capacity.”