Economy

FAAC Disburses N467.85b to FG, States, LGs in August

By Modupe Gbadeyanka

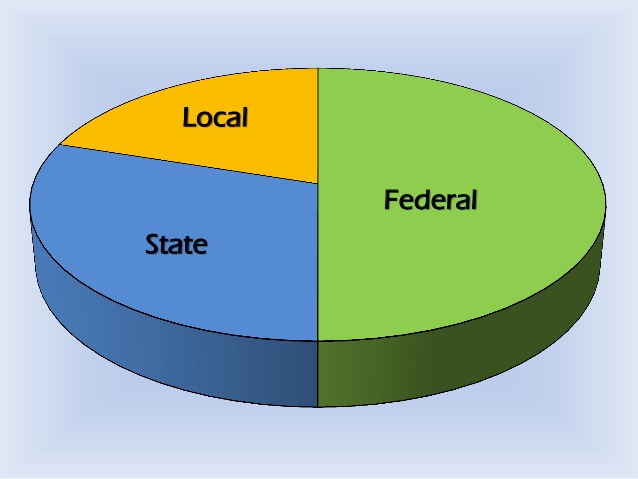

Data released on Monday, September 25, 2017, by the National Bureau of Statistics (NBS) revealed that in the month of August 2017, the Federation Account Allocation Committee (FAAC) disbursed the sum of N467.85 billion to the three tiers of government from the revenue generated in July 2017.

According to the stat office, the amount disbursed comprised of N387.32 billion from the Statutory Account and N80.53 billion from Valued Added Tax (VAT).

The agency further said no allocation was refunded to the Federal Government from the Nigerian National Petroleum Corporation (NNPC) and no amount was also shared from the Excess Petroleum Product Tax (PPT) Account.

From the disbursed amount, federal government received a total of N193.05 billion from the N467.85 billion shared.

States received a total of N130.69 billion and Local governments received N98.01 billion. The sum of N31.59 billion was shared among the oil producing states as 13 percent derivation fund.

Revenue generating agencies such as Nigeria Customs Service (NCS), Federal Inland Revenue Service (FIRS) and Department of Petroleum Resources (DPR) received N3.63 billion, N6.76 billion and N2.12 billion respectively as cost of revenue collections.

Further breakdown of revenue allocation distribution to the Federal Government of Nigeria (FGN) revealed that the sum of N162.09 billion was disbursed to the FGN consolidated revenue account; N3.44 billion shared as share of derivation and ecology; N1.72 billion as stabilization fund; N5.79 billion for the development of natural resources; and N4.18 billion to the Federal Capital Territory (FCT) Abuja.

By Adedapo Adesanya

Crude oil plummeted on Wednesday on hopes of the reopening of the Strait of Hormuz after US President Donald Trump agreed to a two-week ceasefire with Iran.

Brent crude futures moderated to $94.75 a barrel, while the US West Texas Intermediate (WTI) crude eased to $94.41 a barrel.

President Trump said on Wednesday that the US will work closely with Iran and will be talking about tariff and sanctions relief with Iran.

However, analysts cautioned that the ceasefire is a temporary two-week reprieve rather than a permanent resolution, and the global energy system remains fragile due to structural damage to regional infrastructure.

Reuters reported that Iran could open the strait in a limited and controlled way on Thursday or Friday ahead of a meeting between U.S. and Iranian officials in Pakistan.

Agence France-Presse (AFP) reported that two ships appeared to have transited the Strait of Hormuz since the US-Iran ceasefire deal. A Greek-owned bulk carrier and a Liberia-flagged vessel both transited the waterway early on Wednesday.

Meanwhile, Israel carried out its heaviest strikes on Lebanon since the conflict with Hezbollah broke out last month, even as the Iran-aligned group paused attacks on northern Israel and Israeli troops in Lebanon under the ceasefire.

Also, Saudi Arabia’s East-West Pipeline, a critical artery bypassing the Strait of Hormuz, was reportedly hit in an Iranian drone attack. Prior to the attack, the pipeline was pumping at its emergency capacity of 7 million barrels per day to bypass the shuttered strait.

The strikes occurred just hours after a US-Iran ceasefire announcement, which has so far failed to halt regional hostilities. Other facilities in the kingdom were also targeted in the wave of strikes, which the Islamic Revolutionary Guard Corps (IRGC) claimed included oil facilities owned by American companies in Yanbu.

US crude stocks rose by 3.1 million barrels to 464.7 million barrels during the week ended April 3, the Energy Information Administration (EIA) said.

By Adedapo Adesanya

The National Insurance Commission has issued new guidelines for the collection, management, and administration of the Insurance Policyholders’ Protection Fund.

In a circular issued to all insurance institutions on Tuesday, the regulator also set May 31, 2026, as the deadline for insurers to submit their assessment returns for the 2025 financial year.

Recall that on August 5, 2025, President Bola Tinubu signed into law the Nigerian Insurance Industry Reform Act ( NIIRA 2025).

This landmark legislation repeals the Insurance Act 2003, and consolidates related provisions, ushering in a modern regulatory framework. It lays a strong foundation for sustainable growth and increased investment in the country’s insurance sector.

The commission said the guidelines were issued in exercise of its powers under the 2025 Act and other existing insurance laws and regulations to provide regulatory clarity, improve guidance, and ensure ease of compliance across the industry.

According to NAICOM, the guidelines establish a comprehensive structure for the operation of the IPPF, which serves as a statutory safety net to protect insurance policyholders in the event of distress or insolvency of a licensed insurer or reinsurer. The framework also provides direction on the reimbursement of loans by insurers and reinsurers.

NAICOM stated, “The guidelines ensure regulatory clarity, guidance and ease of compliance, as it provides a comprehensive regulatory framework for the collection, management, and administration of the Fund, which serves as a statutory safety net designed to protect insurance policyholders against distress and insolvency of a licensed insurer or reinsurer, including guidance for the reimbursement of loans by an insurer or reinsurer.

“Please be informed that the IPPF Assessment Returns in respect of the year 2025 shall be submitted to the Commission not later than 31st May 2026, while subsequent submissions shall be in line with Section 4.3 of the Guideline on Insurance Policyholders Protection Fund.”

By Adedapo Adesanya

The Dangote Refinery on Wednesday returned the petrol price to N1,200 per litre, less than 24 hours after it increased it by 5 per cent.

The private refinery had raised the ex-depot price by N75 on Tuesday, citing pressure from volatile global oil markets, but quickly brought it back to N1,200 per litre from N1,275 per litre.

The swift downward review is directly linked to a sharp drop in international crude prices. Brent crude has plunged to $95.05 per barrel, after a 13 per cent decline, while the US West Texas Intermediate (WTI) crude closed at $97.18, recording nearly a 14 per cent drop.

This development comes after US President Donald Trump announced a conditional two-week ceasefire with Iran, which eased fears of immediate supply disruptions in the global oil market.

“This will be a double-sided CEASEFIRE!” Trump said on social media, marking a sharp reversal from his earlier warning that “a whole civilisation will die tonight” if Iran failed to comply with US demands.

Iran’s Foreign Minister, Mr Abbas Araqchi, confirmed that the country would halt attacks provided strikes against Iran cease and transit through the Strait of Hormuz is coordinated by Iranian forces.

Despite the breakthrough, tensions remain elevated across the region, with several Gulf states reporting missile launches, drone activity, or issuing civil defence warnings.

While oil prices have fallen back below $100, they remain significantly elevated after surging by a record amount in March. Market analysts noted that regardless of how successful the ceasefire is, geopolitical risk related to the Strait of Hormuz is likely to remain elevated for the foreseeable future under the control of Iran.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn