Economy

Impact of COVID-19 on Debt Capital Markets in Africa

Traditionally, corporates and states in Africa use debt capital markets to raise huge funding. As the coronavirus bites harder against the increasing debt-to-GDP ratios coupled with increasing risks in African countries, the pricing of new issuances in the international debt capital markets became relatively unattractive.

Consequently, African governments turned to other concessionary sources like the International Monetary Fund (IMF), World Bank and Development Finance Institutions for funding.

Africa’s depiction of the international debt capital markets is dominated by sovereign issuances. While its debt capital markets offer investors better returns than in developed markets, its domestic markets remain shallow and least diversified compared to other emerging and frontier markets. Also, African corporates are less likely to raise substantial amounts of funding via debt capital markets due to various reasons including lack of depth in the domestic markets and institutional weaknesses.

Between 2014 and 2018, sovereign bonds accounted for 51.5 per cent of the total $140.3 billion raised from 437 international bond transactions in Africa. Within 2016 and 2018, African issuers raised about $120 billion of non-local currency debt which further culminated to $245.9 billion of non-local currency debt from 759 issues within the last decade. The largest sovereign issuer of non-local currency debt in 2019 was Egypt raising $8.2 billion. Next to Egypt is South Africa which raised $5 billion in September of the same year from its largest-ever Eurobond issuance.

However, in 2020, the effect of COVID-19 impacted the African economy resulting in a pullback from African markets as countries faced crisis on all levels including health and social services. These unprecedented shocks call for a temporary debt standstill for all African countries as economic fundamentals deteriorated. A 2020 study on the economic impact of COVID-19 by the African Union (AU) showed that while countries in Africa could lose up to $500 billion, they may be forced to borrow heavily to survive after the pandemic, hence the need for the debt standstill—suspension of debt service.

For example, Mozambique’s debt overtook its overall economic output as its debt-to-GDP ratio, which was 100 per cent in 2018 billowed to 130 per cent in 2020; even as the country struggles to repay its $14 billion external debt. Asides from Mozambique, there are other poor and highly indebted African countries with little fiscal space to provide a robust response and recovery from the pandemic. Some of these countries like Angola, Djibouti, Congo, Cabo Verde, and Egypt have a higher than 100 per cent external debt-to-GDP ratio, yet, they still seek more funds.

Consequently, the G-20 agreed to suspend debt repayment for the world’s 75 poorest countries until the end of 2020. UN Secretary-General António Guterres further advised that debt suspension should be extended to all developing countries, while the UN Economic Commission for Africa (ECA) recommended a complete temporary debt standstill for two years for all African countries, without exception.

Over the years, there have been calls by multilateral institutions for debt forgiveness for Africa’s most impoverished states. However, some experts opine that such cancellation or debt standstill would be perceived as a default in today realities of the international capital markets and will greatly compromise the future access of African countries to international markets. For example, states like Benin and Ghana which were able to access capital markets over the past year at 5.75 per cent for 7 years (€500 million) and 8.875 per cent for 40 years ($750 million) respectively might find it difficult to do so if they are perceived to be in default. On the other hand, perception of default would likely also be priced into future borrowings by African countries.

Following the above, in April 2020, China, which accounts for most of the lending to African countries through its China Development Bank and the Export-Import Bank of China, expressed a willingness to provide Africa debt relief, but not forgiveness. In June, China offered to cancel Africa’s interest-free loans, which is less than 5 per cent of Africa’s debt to China, based on bilateral negotiations.

With the already rising value of the total public debts in many African countries, to combat the prevailing crisis of the coronavirus, some African countries opted for multilateral financing. One of such countries is Nigeria. The country, in the second quarter of 2020, requested $6.9 billion of multilateral financing from the International Monetary Fund (IMF), World Bank and African Development Bank (AfDB) to minimise the impact of the upsurge of the global pandemic.

Source: NBS

Part of these funds was to establish a $1.2 billion COVID-19 crisis intervention fund to upgrade healthcare facilities across the country and to provide intervention funds to the 36 states including the Federal Capital Territory (FCT).

Similarly, against the backdrop of the pandemic, the African Union launched several programmes, like the African Union Development Agency (AUDA-NEPAD) COVID-19 Response Plan to help countries fight the pandemic and recover better. Using Nigeria as a case study, activities in the domestic bond market significantly increased year-on-year given the relatively low yields in the market. In H1 2020, seven corporate bond issuances were raised to the tune of N152.7 billion compared to N54 billion raised in three issuances in the corresponding period of the previous year.

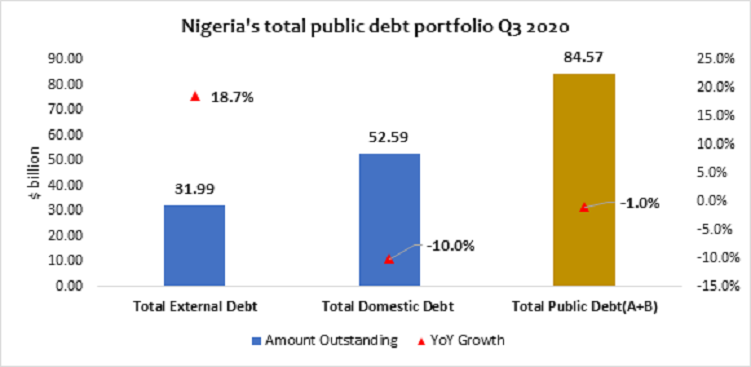

According to the data by the Debt Management Office (DMO), the nation’s debt stock data at the third quarter (Q3) 2020 showed that the total public debt portfolio of the federal and state government combined stood at N32.22 trillion ($84.57 billion), an increase of 22.9 per cent but a decrease of 1 per cent in dollar equivalent due to the different exchange rate values within the periods.

Nigeria’s total public debt showed that $31.99 billion (or 37.82 per cent of the debt) was external while $52.59 billion (or 62.18 per cent of the debt) was domestic. Further disaggregation of Nigeria’s foreign debt showed that $16.74 billion of the debt was multilateral; $502.38 million was bilateral (AFD) and another $3.26 billion bilateral from the Exim Bank of China, JICA, India, and KFW while $11.17 billion was commercial which are Eurobonds and Diaspora Bonds.

The debt conundrum leaves Africa in a dilemma considering the rising budget deficits coupled with the need to fund the deficits. If Africa is to stop depending on donors and multilateral funds to finance its economic development, it needs to evolve towards market-based financing for the quantum of financing required. In addition, African countries need to promote market-friendly policies that will attract capital to underserved sectors and allow the states to focus its limited financing on priority sectors such as education, health, and social services.

By Adedapo Adesanya

The Lagos Chamber of Commerce and Industry (LCCI) has noted that the N15.52 trillion allocation to debt servicing in the 2026 budget remains a significant fiscal burden.

LCCI Director-General, Mrs Chinyere Almona, said this on Tuesday in Lagos via a statement in reaction to the nation’s 2026 budget of N58.18 trillion, hinging the success of the 2026 budget on execution discipline, capital efficiency, and sustained support for productive sectors.

She noted that the budget was a timely shift from macroeconomic stabilisation to growth acceleration, reflecting growing confidence in the economy.

She lauded its emphasis on production-oriented spending, with capital expenditure of N26.08 trillion, representing 45 per cent of total outlays, and significantly outweighing non-debt recurrent expenditure of N15.25 trillion.

According to Mrs Almona, this composition supports infrastructure development, industrial expansion, and productivity growth.

However, she explained that the N15.52 trillion allocation to debt servicing underscored the need for stricter borrowing discipline, enhanced revenue efficiency, and expanded public-private partnerships to safeguard investments that promote growth.

She added that a further review of the 2026 budget revealed relatively optimistic macroeconomic assumptions that may pose fiscal risks.

“The oil price benchmark of $64.85 per barrel, although lower than the $75.00 benchmark in the 2025 budget, appears optimistic when compared with the 2025 average price of about $69.60 per barrel and current prices around $60 per barrel.

“This raises downside risks to oil revenue, especially since 35.6 per cent of the total projected revenue is expected to come from oil receipts.

“Similarly, the oil production benchmark of 1.84 million barrels per day is significantly higher than the current level of approximately 1.49 million barrels per day.

“Achieving this may be challenging without substantial improvements in security, infrastructure integrity, and sector investment,” she said.

Mrs Almona said the exchange rate assumption of N1,512 to the Dollar, compared with N1,500 in the 2025 budget and about N1,446 per Dollar at the end of November, suggests expectations of a mild depreciation.

She said while this may support Naira-denominated revenue, it also increases the cost of imports, debt servicing, and inflation management, with broader macroeconomic implications.

The LCCI DG added that the inflation projection of 16.5 per cent in 2026, up from 15.8 per cent in the 2025 budget and a current rate of about 14.45 per cent, appeared optimistic, particularly in a pre-election year.

She also expressed concern about Nigeria’s historically weak budget implementation capacity, likely to be further strained by the combined operation of multiple budget cycles within a single year.

Looking ahead, Mrs Almona identified agriculture and agro-processing, manufacturing, infrastructure, energy, and human capital development as key drivers of growth in 2026.

She said that unlocking these sectors would require decisive execution—scaling irrigation and agro-value chains, reducing power and logistics costs for manufacturers, and aligning education and skills development with private-sector needs.

The LCCI head stressed the need to resolve issues surrounding the Naira for crude, increase the supply of oil to local refineries to boost local refining capacity and conserve the substantial foreign exchange used for fuel imports.

“Overall, the 2026 Budget presents a credible opportunity for Nigeria to transition from recovery to expansion.

“Its success will depend less on the size of allocations and more on execution discipline, capital efficiency, and sustained support for productive sectors.

By Dipo Olowookere

The Nigerian Exchange (NGX) Limited witnessed Santa Claus rally on Wednesday after it closed higher by 0.12 per cent.

Strong demand for Nigerian stocks lifted the All-Share Index (ASI) by 185.70 points during the pre-Christmas trading session to 153,539.83 points from 153,354.13 points.

In the same vein, the market capitalisation expanded at midweek by N118 billion to N97.890 trillion from the preceding day’s N97.772 trillion.

Investor sentiment on Customs Street remained bullish after closing with 36 appreciating equities and 22 depreciating equities, indicating a positive market breadth index.

Guinness Nigeria chalked up 9.98 per cent to trade at N318.60, Austin Laz improved by 9.97 per cent to N3.20, International Breweries expanded by 9.85 per cent to N14.50, Transcorp Hotels rose by 9.83 per cent to N170.90, and Aluminium Extrusion grew by 9.73 per cent to N16.35.

On the flip side, Legend Internet lost 9.26 per cent to close at N4.90, AXA Mansard shrank by 7.14 per cent to N13.00, Jaiz Bank declined by 5.45 per cent to N4.51, MTN Nigeria weakened by 5.21 per cent to N504.00, and NEM Insurance crashed by 4.74 per cent to N24.10.

Yesterday, a total of 1.8 billion shares valued at N30.1 billion exchanged hands in 19,372 deals versus the 677.4 billion shares worth N20.8 billion traded in 27,589 deals in the previous session, implying a slump in the number of deals by 29.78 per cent, and a surge in the trading volume and value by 165.72 per cent and 44.71 per cent apiece.

Abbey Mortgage Bank was the most active equity for the day after it sold 1.1 billion units worth N7.1 billion, Sterling Holdings traded 127.1 million units valued at N895.9 million, Custodian Investment exchanged 115.0 million units for N4.5 billion, First Holdco transacted 40.9 million units valued at N2.2 billion, and Access Holdings traded 38.2 million units worth N783.3 million.

By Adedapo Adesanya

Nigerian food and beverage company, Rite Foods Limited, has extended warm Yuletide greetings to Nigerians as families and communities worldwide come together to celebrate the Christmas season and usher in a new year filled with hope and renewed possibilities.

In a statement, Rite Foods encouraged consumers to savour these special occasions with its wide range of quality brands, including the 13 variants of Bigi Carbonated Soft Drinks, premium Bigi Table Water, Sosa Fruit Drink in its refreshing flavours, the Fearless Energy Drink, and its tasty sausage rolls — all produced in a world-class facility with modern technology and global best practices.

Speaking on the season, the Managing Director of Rite Foods Limited, Mr Seleem Adegunwa, said the company remains deeply committed to enriching the lives of consumers beyond refreshment. According to him, the Yuletide period underscores the values of generosity, unity, and gratitude, which resonate strongly with the company’s philosophy.

“Christmas is a season that reminds us of the importance of giving, togetherness, and gratitude. At Rite Foods, we are thankful for the continued trust of Nigerians in our brands. This season strengthens our resolve to consistently deliver quality products that bring joy to everyday moments while contributing positively to society,” Mr Adegunwa stated.

He noted that the company’s steady progress in brand acceptance, operational excellence, and responsible business practices reflects a culture of continuous improvement, innovation, and responsiveness to consumer needs. These efforts, he said, have further strengthened Rite Foods’ position as a proudly Nigerian brand with growing relevance and impact across the country.

Mr Adegunwa reaffirmed that Rite Foods will continue to invest in research and development, efficient production processes, and initiatives that support communities, while maintaining quality standards across its product portfolio.

“As the year comes to a close, Rite Foods Limited wishes Nigerians a joyful Christmas celebration and a prosperous New Year filled with peace, progress, and shared success.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism9 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn