Economy

Mining Sector to Contribute $27b to GDP by 2025—FG

By Modupe Gbadeyanka

It is no doubt that a lot has not been tapped from the mining industry in Nigeria, but the present government is focusing its attention to this just as it is doing with the agricultural sector.

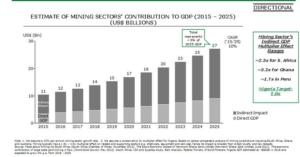

At the moment, it is estimated that the contribution of the sector to the Gross Domestic Product (GDP) of Nigeria is $13 billion.

But the Ministry of Mines and Steel Development says it hopes to push this to about $27 billion by 2025.

This was revealed in the Ministry’s Road Map released on Sunday in Abuja, which was posted on its website and analysed by Business Post.

According to the Ministry’s roadmap, the impact on GDP will be significant as industries are able to use the output of the sector better, substituting for imports.

It also noted that the successful execution of the mining plan with unlock significant value for Nigeria and the net outcome will be creation of thousands of direct jobs and potentially hundreds of thousands of indirect jobs.

The Ministry said it would execute this roadmap in stages with the first focused on bringing stability to the sector and rebuilding the country’s market confidence between 2016 and 2018.

The second phase will focus on establishing Nigeria as a competitive African mining and mineral processing centre from 2016 to 2020, while the third phase will enable Nigeria compete in the global market for refined metals and minerals from 2018 to 2030 in addition to selected ore exportation.

“To ensure effective execution of the roadmap, a committee has recommended the formation of a Mining Implementation and Strategy Team (MIST) that will be the process owner of the roadmap and will be accountable for its implementation.

“MIST, as an advisory team to the Minister, will work across multiple MDAs, stakeholders and private institutions to ensure that the full potential of the minerals, mining and metals sector is achieved,” the Ministry said.

Recall that in 2015, the sector contributed approximately 0.33 percent to the GDP of the country. This contribution is a reversal from the historically higher percentages (about 4-5% in the 1960s-70s).

However, following a decade of reforms starting in 1999, this contribution represents a cautiously optimistic restart of the development of the sector.

The decade of reform saw key changes including, the passage of a new Nigerian Minerals and Mining Act (2007), a Nigerian Mineral and Metals Policy (2008), the creation of a modern Mining Cadastre system, the refinement of the tax code, and the expansion in airborne mapping of the country to sharpen knowledge of the mineral endowments. As important as these progress steps have been, Nigeria can and should do more.

The sector faces several challenges with geosciences data and information, Industry participants, Stakeholders, Institutions, Governance and other enablers of the sector.

According to the National Bureau of Statistics (NBS), gour sub-activities make up the Mining & Quarrying sector: Crude Petroleum and Natural Gas, Coal Mining, Metal ore and Quarrying and other Minerals.

On a nominal basis, the sector grew in the Fourth Quarter of 2016 by 54.68% (year on year). This was substantially above the growth rate recorded in the corresponding quarter of 2015, when a contraction of -35.12% was recorded.

This increase may be attributable in part to negotiations with militant groups in the Niger Delta region, who had been vandalizing oil infrastructure, but who reduced their attacks in the fourth quarter following these series of negotiations.

Coal mining and Metal ore activities in nominal terms, recorded growth rates of 14.16% and 24.24% respectively, significantly higher than the third quarter growth rates of 1.06% and 17.11% respectively.

The Mining & Quarrying sector contributed 7.10% to overall GDP during the fourth quarter of 2016, higher than the contribution recorded in same quarter of 2015 at 5.18%, and its contribution in the preceding quarter of 6.23%.

In real terms, Mining and Quarrying sector recorded a decline of -12.04% (year-on-year) in the fourth quarter of 2016. Although this is significantly smaller decline than that recorded in the previous quarter, of 21.64%, it is nevertheless 3.99% points lower than the growth rate recorded in the same Quarter of 2015 of –8.05.

The contribution of Mining and Quarrying to Real GDP in the fourth quarter of 2016 stood at 7.32%, representing a decline of 0.89% points relative to the corresponding quarter of 2015 and also a decline of 1.02% points relative to the third quarter of 2016.

By Adedapo Adesanya

All insurance and reinsurance companies operating in Nigeria are required to remit 0.25 per cent of their annual net premium income to a new fund, according to new guidelines by the National Insurance Commission (NAICOM).

The insurance regulator has issued binding guidelines for a new industry-wide protection fund that will compel every licensed insurer and reinsurer in the country to make annual cash contributions, or risk losing their operating licence.

NAICOM published the framework for the Insurance Policyholders’ Protection Fund (IPPF) under the authority of the Nigerian Insurance Industry Reform Act (NIIRA) 2025, which was signed into law last August.

The guidelines, which take effect immediately, did not disclose an initial capitalisation target for the fund or a timeline for when it would be considered adequately funded for resolution purposes.

The IPPF is designed to function as a resolution backstop as a capital pool available to settle outstanding policyholder claims when a licensed insurer or reinsurer becomes insolvent or enters regulatory distress.

The mechanism addresses a longstanding vulnerability in the Nigerian market, where policyholders holding valid claims against failed insurers have historically had no guaranteed recourse.

The 0.25 per cent payments are due into designated deposit money bank accounts no later than June 30 each year.

NAICOM said it will supplement industry contributions by injecting 0.25 per cent of the balance held in the existing Security and Insurance Development Fund (SIDF) into the IPPF annually, creating a dual-stream capitalisation model.

The guidelines state explicitly that failure to remit the full assessed contribution within the stipulated timeframe shall constitute grounds for suspension or cancellation of an operator’s licence. The same penalty framework applies to defaults on any loans extended from the fund.

Day-to-day management of the IPPF will be delegated to an independent professional Fund Manager, subject to a minimum paid-up capital threshold of N5 billion.

Investment activity is restricted to low-risk, government-backed instruments. This is a deliberate constraint intended to preserve liquidity and protect the fund from market volatility.

Members are bound by a Code of Conduct that bars them from using their positions for personal advantage or to direct decisions in favour of any insurer, reinsurer, or connected party.

The guidelines introduce a mandatory early-warning mechanism: insurance operators who become aware of imprudent practices within their organisations or elsewhere in the industry are required to report such conduct to NAICOM within five working days.

The commission has provided explicit anti-retaliation protections, stating that no whistleblower shall be subjected to retaliation, intimidation, or any form of adverse action for making a disclosure.

By Modupe Gbadeyanka

President Bola Tinubu has been called on to use his influence to halt the passage of the proposed Customs, Excise and Tariff Amendment (CETA) Bill.

The proposed piece of legislation is currently before the National Assembly, and it seeks to introduce a percentage levy per litre of the retail price on non-alcoholic beverages.

In an outlined advertorial published in key newspapers, the Organised Private Sector of Nigeria urged the federal government to engage with the leadership of the parliament to stop the ongoing legislative process with a view to stepping down the CETA Bill, thus allowing the executive-led fiscal reforms to be fully integrated and aligned.

The OPS comprises the Manufacturers Association of Nigeria (MAN), Nigerian Association of Chambers of Commerce, Industry, Mines and Agriculture (NACCIMA), Nigeria Employers’ Consultative Association (NECA), Nigerian Association of Small Scale Industrialists (NASSI), and the Nigerian Association of Small and Medium Enterprises (NASME).

In the advertorial signed by the presidents of all members of the group, it was submitted that allowing for more talks would strengthen policy coherence, enhance predictability, and improve the effectiveness of the nation’s excise framework.

It was stressed that halting the bill would also encourage structured, evidence-based engagement with industry stakeholders, thereby ensuring that any future measures will effectively balance revenue generation, public health objectives, and economic sustainability.

“While we fully support well-designed fiscal reforms and evidence-based public health interventions, we are concerned that the Bill, in its current form, raises significant social, economic, administrative, and legal issues that could undermine Your Excellency’s broader fiscal reform objectives,” the body stated.

While calling on the government to restrain the Senate from proceeding with the process, the organisation noted that the proposed levy would therefore constitute a regressive measure, reducing consumer purchasing power without providing viable alternatives or meaningful public health support.

Commenting on the impact of such a levy on industry stability, investment, and employment, OPS stated that the sector was already under severe pressure from exchange rate adjustments, high energy costs, and rising prices of imported inputs, packaging materials, and machinery.

“An additional excise burden would further increase production costs, reduce capacity utilisation, delay or cancel planned investments, and threaten the livelihoods of thousands of small distributors, retailers, and informal traders who depend on high-volume, low-margin sales.

“These pressures would inevitably be passed on to consumers through higher prices, leading to reduced demand and potential further job losses across the value chain,” it stated.

While commending the president for the leadership and bold economic reforms undertaken since assuming office in 2023, it noted that the reforms have played an important role in restoring macroeconomic stability and rebuilding confidence within the business community.

By Adedapo Adesanya

Three stocks further weakened the NASD Over-the-Counter (OTC) Securities Exchange by 1.12 per cent on Wednesday, April 8, with the Unlisted Security Index (NSI) down by 44.43 points to 3,930.91 points from the previous day’s 3,975.34 points, and the market capitalisation went down by N26.59 to N2.351 trillion from N2.378 trillion.

MRS Oil lost N11.00 during the session to close at N161.00 per share compared with Tuesday’s closing price of N172.00 per share, Central Securities Clearing System (CSCS) Plc dipped by N3.74 to N67.95 per unit from N71.69 per unit, and Afriland Properties Plc fell by N1.10 to sell at N15.95 per share versus N17.05 per share.

There were two gainers at the midweek trading session, led by IPWA Plc, which appreciated by 55 Kobo to N6.61 per unit from N6.06 per unit, and First Trust Mortgage Bank Plc improved its value by 4 Kobo to N2.32 per share from N2.28 per share.

Yesterday, the volume of securities rose by 620.4 per cent to 5.7 million units from 797,264 units, the value of securities increased by 25.1 per cent to N32.7 million from N26.1 million, and the number of deals climbed by 12.1 per cent to 37 deals from the preceding session’s 33 deals.

Great Nigeria Insurance (GNI) Plc ended the day as the most traded stock by value on a year-to-date basis with 3.4 billion units sold for N8.4 billion, trailed by CSCS Plc with 57.2 million units exchanged for N3.9 billion, and Okitipupa Plc with 27.5 million units traded for N1.8 billion.

GNI Plc also finished the session as the most traded stock by volume on a year-to-date basis with 3.4 billion units valued at N8.4 billion, followed by Resourcery Plc with 1.1 billion units worth N415.7 million, and Infrastructure Guarantee Credit Plc with 400 million units transacted for N1.2 billion.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn