Economy

Naira Slides to N452.67/$1 at I&E, N770 at P2P, N745 at Black Market

By Adedapo Adesanya

The value of the Naira to the United States Dollar has started to decline in the different segments of the foreign exchange ((forex) market as a result of renewed scarcity of FX in the system.

In the past week, the Central Bank of Nigeria (CBN) had tried to improve the situation, but counter policies have reignited the flames and they could burn down the system.

On Tuesday, the domestic currency depreciated against the greenback at the black market, Peer-to-Peer (P2P), and the Investors and Exporters (I&E) windows of the market.

The demand for forex as the market heads into the Yuletide weakened the Nigerian currency against the Dollar at the I&E window yesterday by N1.67 or 0.26 per cent as it closed at N452.67/$1 compared with Monday’s rate of N451/$1.

Data published by FMDQ Securities Exchange showed that the FX turnover for yesterday was $134.04 million, 94.6 per cent or $65.46 million more than the $69.18 million published on Monday.

In the P2P segment, the average exchange rate of the Naira to the Dollar was N770/$1, in contrast to the N768/$1 it was transacted in the preceding session, indicating a decline of N2.

Also, in the parallel market, the local currency lost N1 against the American currency yesterday to sell for N745/$1 compared with the previous day’s value of N744/$1.

However, in the interbank window, the Nigerian Naira closed flat against the Pound Sterling and the Euro at N544.46/£1 and N474.89/€1, respectively.

Meanwhile, in the cryptocurrency market, transactions were mixed, with Dogecoin (DOGE) going down by 2.7 per cent to $0.0727, and Cardano (ADA) losing 2.3 per cent to trade at $0.2516.

Further, Solana (SOL) recorded a 2.1 per cent slump to quote at $12.08, and Ripple (XRP) fell by 0.5 per cent to settle at $0.3423.

But Bitcoin (BTC) jumped by 0.4 per cent to $16,845.51, Ethereum (ETH) improved by 0.3 per cent to $1,211.99, Litecoin (LTC) grew by 0.2 per cent to $65.18, and Binance Coin (BNB) added 0.03 per cent to trade at $248.74.

As for the US Dollar Tether (USDT) and Binance USD (BUSD), they remained unchanged at $1.00 each.

By Adedapo Adesanya

The Nigeria Revenue Service (NRS) and the Joint Revenue Board (JRB) have issued new guidelines clarifying the taxation of virtual assets in Nigeria.

The guidelines provide an administrative framework for the taxation of virtual assets and specify the tax obligations of individuals and businesses operating in the sector.

According to a public notice issued by the two agencies, the framework covers registration, reporting and record-keeping requirements, valuation principles and the tax treatment of virtual asset transactions.

It applies to taxpayers, Virtual Asset Service Providers (VASPs), peer-to-peer (P2P) marketplace operators, tax practitioners and other persons engaged in virtual asset-related activities.

The NRS and JRB said the guidelines were developed in line with the provisions of the Nigeria Tax Act 2025 and the Nigeria Tax Administration Act 2025.

The two bodies said the release was aimed at providing clarity, certainty and consistency in the administration of Nigeria’s tax laws as the country’s virtual asset ecosystem continues to evolve.

The agencies added that the framework would promote voluntary compliance, enhance transparency and support the development of a fair and efficient tax system for digital asset transactions.

They urged all affected taxpayers and stakeholders to familiarise themselves with the guidelines and ensure compliance with the applicable tax obligations.

The guidelines are available on the official websites of the two agencies.

By Adedapo Adesanya

Manufacturers are yet to benefit from relief on the burden of multiple taxes and levies despite the enactment of the Nigeria Tax Act 2025, according to the Manufacturers Association of Nigeria (MAN).

The association, in its Manufacturers CEO Confidence Index (MCCI) report for the second quarter of 2026, said manufacturers continued to face multiple tax collectors and regulatory agencies during the period.

Director-General of MAN, Mr Segun Ajayi-Kadir, said the new tax law, which was expected to reduce the burden of multiple taxation, had yet to deliver the intended benefits.

“Manufacturers complained that they were still met with multiple tax collectors and regulators in Q2 2026. It follows that the implementation of the Nigeria Tax Act 2025 is yet to achieve its objective of relieving manufacturers of the burden of taxes and levies,” he said.

According to the report, Nigeria’s business environment remains largely unsupportive of manufacturing growth, with local sourcing of raw materials emerging as the only indicator that recorded noticeable improvement.

MAN, however, warned that the gains in local sourcing could be undermined by worsening insecurity in parts of the country.

The association attributed the improvement largely to persistent foreign exchange constraints, which have forced many manufacturers to source inputs locally.

Despite this, it said excessive regulation and multiple taxation continue to weigh heavily on manufacturers.

The report showed that manufacturers recorded a modest increase in sales volume during the second quarter, but rising production, distribution and logistics costs continued to erode profitability.

It added that capacity utilisation, production levels, investment and employment remained broadly unchanged during the review period.

MAN further observed that although recent foreign exchange reforms had helped stabilise the naira, inadequate foreign currency supply remained a major constraint to manufacturing operations.

Other key challenges identified in the report include poor infrastructure, high production costs, raw material shortages and unfavourable trade policies.

The association said the findings underscore the continued pressure on manufacturers despite recent fiscal and foreign exchange reforms, stressing the need for more effective implementation of policies aimed at improving the operating environment for the real sector.

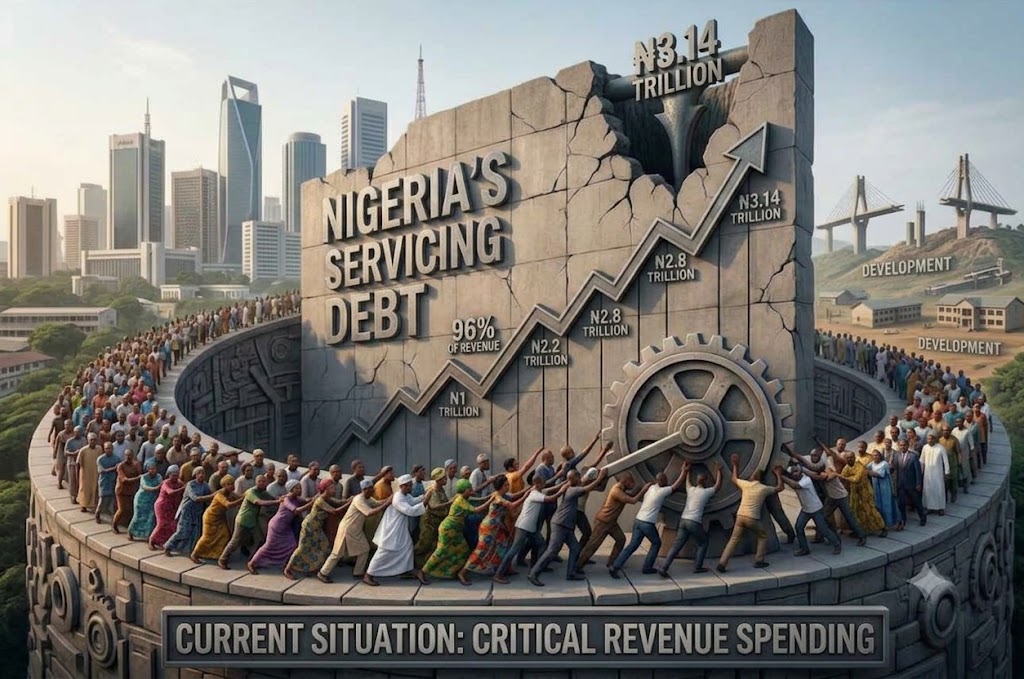

By Adedapo Adesanya

The federal government spent N3.14 trillion on servicing its domestic debt in the first quarter (Q1) of 2026, according to the Debt Management Office (DMO).

The figure, contained in the DMO’s latest domestic debt service report for Q1 2026, comprised N2.97 trillion in interest payments and N169.68 billion in principal repayments.

According to the report, the government spent N741.82 billion on domestic debt service in January before the figure rose to N967.67 billion in February.

Debt service increased further to N1.43 trillion in March, bringing total spending for the quarter to N3.14 trillion.

The March figure represented a 47.7 per cent increase from the N967.67 billion recorded in February and was 92.7 per cent higher than the N741.82 billion spent in January.

The debt office said interest payments accounted for approximately 94.6 per cent of the total domestic debt service during the quarter.

Treasury bills accounted for the largest share of interest payments at N1 trillion, while interest payments on Federal Government bonds stood at N1.96 trillion.

The government also paid N4.24 billion in interest on FGN savings bonds during the period.

The debt management body said the principal component of the debt service comprised N169.68 billion in repayments on local-denominated promissory notes.

Overall, domestic debt service rose significantly throughout the quarter, with March alone accounting for nearly half of the N3.14 trillion spent between January and March.