Economy

NGX Group Tasks FG on More Friendly Market Policies

By Aduragbemi Omiyale

The Nigerian Exchange (NGX) Group Plc has tasked the federal government, under the leadership of President Bola Tinubu, to come up with more friendly market policies to attract foreign investment inflows.

At its Annual General Meeting (AGM) in Lagos on Friday, the chairman of the organisation, Mr Umaru Kwairanga, assured that the company would work with the government to achieve this goal.

He lauded the various reforms of this administration that have resulted in the impressive performance of the market.

“The capital market community is excited by the new government and the steps it has so far taken with respect to the economy as reflected in the tremendous growth in our market indicators.

“As a group, we are committed to working with the government to stimulate further growth in the economy, and address higher capital costs, as this will go a long way to enhance Nigeria’s credit profile and create a favourable environment for both domestic and foreign investors,” he said.

But Mr Kwairanga noted that the federal government needs to eke out more friendly market policies that will engender growth as the consistent and faithful implementation of market policies will help businesses to thrive.

He added that the group was hopeful that the planned Initial Public Offer (IPO) of the NNPC Limited would be fast-tracked by the Tinubu-led administration.

Speaking on the performance of the group, Mr Kwairanga noted that the organisation demonstrated resilience in 2022, achieving a 10.3 per cent increase in gross earnings to N7.5 billion, despite a challenging economic environment.

Its total revenue grew primarily due to a 6.8 per cent increase in revenue to N6.2 billion and a 30.1 per cent increase in other income to N1.3 billion.

The growth in its revenue was further bolstered by a 51.2 per cent increase in treasury investment income and a 9.0 per cent increase in transaction fees. However, its total expenses rose by 35.5 per cent to N8.8 billion, primarily due to interest costs on borrowed funds used for strategic acquisitions.

“Achieving an efficient capital mix and broadening our access to capital remain fundamental to our mission.

“The board will continue to assist the Management team in addressing long-term risks, strengthening the global NGX brand, and assessing progress toward our goal of being Africa’s preferred exchange hub,” remarked Mr Kwairanga.

While welcoming the new board members, he commended the contributions of the outgoing board members to the growth and development of the organization.

Commending the group’s performance, the Group Chief Executive Officer, Mr Oscar Onyema, said the performance reflects NGX Group’s commitment towards driving growth in Nigeria and Africa’s capital markets. Onyema further added that the group is proud to have generated multiple income streams that enabled it to overcome economic headwinds.

Speaking on the group’s outlook, he expressed optimism about the opportunities and challenges ahead and emphasized the group’s commitment to leveraging its strengths and expertise to drive growth and value creation in Nigeria and other financial markets in Africa.

“NGX Group will continue supporting its operating subsidiaries, associates, and investee companies to deliver sustainable value creation for its shareholders. We will look to enhance our performance by continuously striving to optimize operations, increase revenue streams and expand our market reach.

“We are confident that these measures will enable us to build on the positive momentum we have achieved in recent years and drive growth in 2023 and beyond,” he said.

Shareholders approved all resolutions on the agenda, including the appointment of six Directors of Nigerian Exchange Group Plc: Mr Nonso Okpala (Non-Executive Director), Mr Sehinde Adenagbe (Non-Executive Director), Mr Ademola Babarinde (Non-Executive Director), Mrs Mosun Belo – Olusoga (Independent Non-Executive Director), Mr Mohammed Garuba (Non-Executive Director) and Mrs Fatima Wali- Abdurraham (Independent Non-Executive Director).

By Adedapo Adesanya

The Dangote Refinery on Wednesday returned the petrol price to N1,200 per litre, less than 24 hours after it increased it by 5 per cent.

The private refinery had raised the ex-depot price by N75 on Tuesday, citing pressure from volatile global oil markets, but quickly brought it back to N1,200 per litre from N1,275 per litre.

The swift downward review is directly linked to a sharp drop in international crude prices. Brent crude has plunged to $95.05 per barrel, after a 13 per cent decline, while the US West Texas Intermediate (WTI) crude closed at $97.18, recording nearly a 14 per cent drop.

This development comes after US President Donald Trump announced a conditional two-week ceasefire with Iran, which eased fears of immediate supply disruptions in the global oil market.

“This will be a double-sided CEASEFIRE!” Trump said on social media, marking a sharp reversal from his earlier warning that “a whole civilisation will die tonight” if Iran failed to comply with US demands.

Iran’s Foreign Minister, Mr Abbas Araqchi, confirmed that the country would halt attacks provided strikes against Iran cease and transit through the Strait of Hormuz is coordinated by Iranian forces.

Despite the breakthrough, tensions remain elevated across the region, with several Gulf states reporting missile launches, drone activity, or issuing civil defence warnings.

While oil prices have fallen back below $100, they remain significantly elevated after surging by a record amount in March. Market analysts noted that regardless of how successful the ceasefire is, geopolitical risk related to the Strait of Hormuz is likely to remain elevated for the foreseeable future under the control of Iran.

By Adedapo Adesanya

Crude oil deliveries from the Nigerian National Petroleum Company (NNPC) Limited to the Dangote Petroleum Refinery doubled in March, boosting prospects for improved fuel availability.

This was revealed by the chief executive of Dangote Industries Limited, Mr Aliko Dangote, on Tuesday, when he received the Deputy Secretary-General of the United Nations, Mrs Amina Mohammed, at the industrial complex in Ibeju-Lekki, Lagos.

While speaking on feedstock supply, Mr Dangote commended the NNPC for increasing crude deliveries to the refinery in March, noting that volumes rose to 10 cargoes—six supplied in Naira and four in Dollars—to support domestic fuel availability, according to a statement by the Refinery.

“Last month, they gave us six cargoes for Naira and four cargoes for Dollars,” he said.

Despite the improvement, Mr Dangote noted that the supply remains below the 19 cargoes required for optimal operations, with the refinery continuing to bridge the gap through imports from the United States and other African producers.

He also expressed concern over the unwillingness of international oil companies operating in Nigeria to sell to the refinery, stating that their preference for selling crude to traders forces it to repurchase at higher costs, with broader implications for the economy.

Mr Dangote added that the refinery is seeking increased access to domestically priced crude under local currency arrangements as part of efforts to moderate fuel costs and enhance long-term energy and food security across the continent.

On her part, Mrs Mohammed underscored the strategic importance of Dangote Industries Limited -particularly Dangote Fertiliser Limited—in addressing Africa’s mounting food security challenges, while calling for stronger global partnerships to scale its impact.

Mrs Mohammed said the United Nations would prioritise amplifying scalable solutions capable of mitigating the continent’s food crisis, describing Dangote’s integrated industrial model as a critical pathway.

“I think the UN’s job here is to amplify and to put visibility on the possibilities of mitigating a food security crisis, and this is one of them,” she said. “I hope that when we go back, we can continue to engage partners and countries that should collaborate with Dangote Industries.”

By Aduragbemi Omiyale

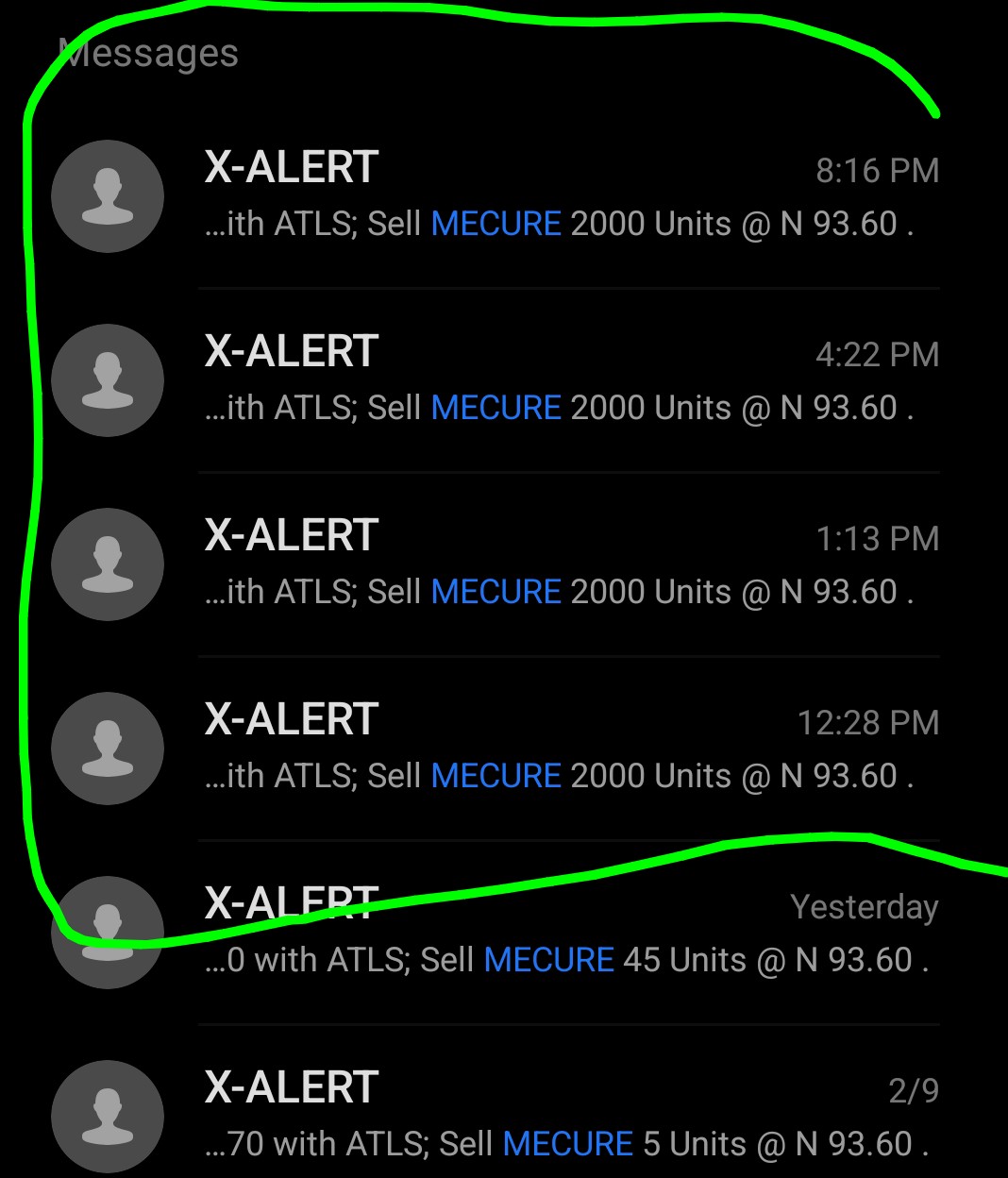

The Securities and Exchange Commission (SEC) has approved a 50 per cent hike in the X-Alert service fee per transaction in the Nigerian capital market.

The X-Alert fee is a flat rate charged for sending real-time SMS/email notifications for transactions to investors from both buy and sell sides.

It was introduced by the Nigerian Exchange (NGX) to replace percentage-based charges, aimed at increasing transparency and reducing total transaction costs for investors.

Investors were earlier charged N4 per SMS, but the country’s apex capital market regulator has approved a 50 per cent increase in X-Alert service fee, meaning the new rate is N6 per SMS.

Business Post gathered from one of the players in the ecosystem that the effective date for the new price was Thursday, March 26, 2026.

“We wish to inform you of a revision to the X-Alert (SMS) service fee applicable to transactions executed on the Nigerian Exchange (NGX).

“Following approval by the Securities and Exchange Commission (SEC), the X-Alert fee has been reviewed upward from N4.00 to N6.00 per transaction,” the notice sighted by this newspaper read.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn