Economy

Nigeria FX Reserves Dip to Six-Year Low of $32.87bn

By Adedapo Adesanya

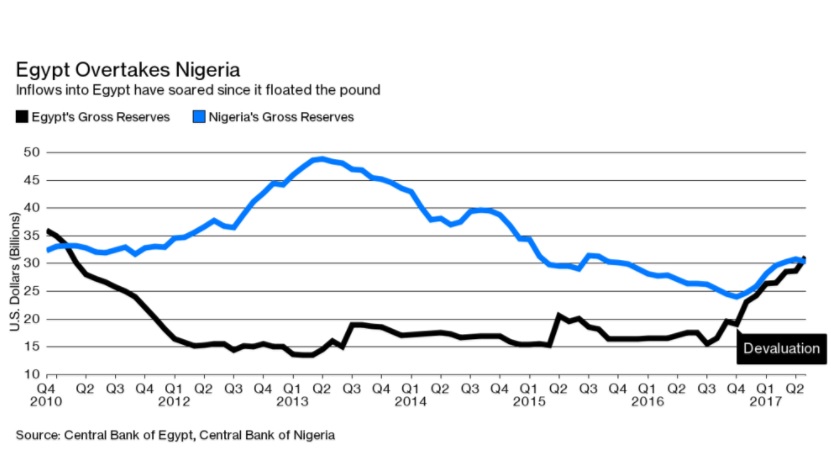

Nigeria’s foreign exchange reserves dipped to a six-year low of $32.87 billion at the end of December 2023, one of the most tumultuous years for the foreign exchange market.

According to data from the Central Bank of Nigeria (CBN), this level was last seen in September 2017 when the reserve fell to $32.17 billion.

This came as the central bank tried to prop up the Naira in a year in which it fell more than 49 per cent following a spate of devaluations after a move by the administration of Mr Bola Tinubu to unify the exchange rate and rid Africa’s largest economy of its multiple exchange rate regime.

Nigeria’s multiple FX segments are now collapsed into the Nigerian Autonomous Foreign Exchange Market (NAFEM) meaning applications for medicals, school fees, BTA/PTA, and SMEs would continue to be processed through deposit money banks (DMBs).

However, the forex crisis heightened after the country unified the rates due to low supply as players competed for scarce FX and to make their ends meet, many found their way to other unregulated segments, including the black market or the Peer-to-Peer (P2P) electronic channels.

According to Reuters, the Naira was the third worst-performing global currency in 2023.

Also, the country could not clear a substantial amount out of over $6 billion backlog of unsettled forwards, despite moves by the government to close deals to boost the forex needs of the country.

The Governor of the CBN, Mr Olayemi Cardoso, who replaced Mr Godwin Emefiele, said he would allow market forces to determine exchange rates while setting clear, transparent, and harmonised rules governing market operations.

Despite this promise, many analysts project that the Naira’s downward momentum is likely to continue through much of 2024.

There have been calls for President Tinubu to boost oil production, which stood at 1.45 million barrels as of the third quarter of 2023 and accounts for 80 per cent of Nigeria’s foreign exchange earnings.

Other measures include driving foreign investment and enacting structural reforms ranging from debt reduction to increasing the country’s tax base and cutting down on the expensive cost of governance.

By Modupe Gbadeyanka

The deadline for filing individual annual income tax returns for residents of Lagos State has again been extended to April 21, 2026.

This information was revealed via a statement signed by the Head of Corporate Communications of the Lagos State Internal Revenue Service (LIRS), Mrs Monsurat Amasa-Oyelude, on Saturday.

The agency thanked some taxpayers for their continued compliance and commitment to the filing of their individual annual income tax returns, but charged those who have yet to file theirs to do so before the new deadline.

LIRS had earlier moved the deadline from its statutory period of March 31, 2026, to April 14, 2026, but due to “the overwhelming response and to enhance taxpayer convenience, while maintaining the integrity and accuracy of submissions,” the date was moved forward to April 26.

The tax-collecting organisation said it “observed a significant increase in traffic on its eTax platform as more taxpayers endeavour to meet the filing deadline.”

“In view of this development, and to ensure that all taxpayers are provided with adequate opportunity to successfully complete their filings, LIRS hereby announces a further extension of the deadline, now set for April 21, 2026,” it stated.

The agency reiterated that all filings must be completed electronically via the LIRS eTax platform: https://etax.lirs.net, which remains the only approved channel for submission.

Taxpayers were reminded that the filing of annual income tax returns remains a statutory obligation and were encouraged to take advantage of this final extension to fulfil their civic responsibility.

By Dipo Olowookere

The Nigerian Exchange (NGX) Limited was in green on Friday after it closed higher by 0.30 per cent as a result of sustained bargain hunting.

Customs Street was up yesterday after three of the five major sectors came under buying pressure, with the consumer goods index up by 1.64 per cent, the industrial goods space up by 1.12 per cent, and the banking counter up by 0.64 per cent.

Business Post observed that profit-taking brought down the insurance by 2.61 per cent, and weakened the energy sector by 0.01 per cent.

At the close of business, the market capitalisation increased by N707 billion to N131.166 trillion from N130.459 trillion, and the All-Share Index (ASI) expanded by 1,097.86 points to 203,770.42 from 202,672.56 points.

Transactions by Nigerian stock investors shrank during the session, as 548.6 million shares worth N31.5 billion exchanged hands in 48,538 deals compared with the 652.9 million shares valued at N39.8 billion transacted in 51,101 deals a day earlier.

This implied that the trading volume went down by 15.98 per cent, the trading value depreciated by 20.85 per cent, and the number of deals crashed by 5.02 per cent.

Access Holdings finished the day as the busiest equity after selling 52.7 million units valued at N1.4 billion, Zenith Bank exchanged 47.8 million units worth N5.4 billion, UBA traded 38.9 million units for N1.8 billion, Secure Electronic Technology transacted 36.7 million units worth N35.5 million, and GTCO sold 34.9 million units valued at N4.6 billion.

The market breadth index was negative during the session with 20 price gainers and 38 price losers, indicating weak investor sentiment.

Trans Nationwide Express appreciated by 9.91 per cent to N3.77, International Breweries grew by 9.88 per cent to N13.35, Chams rose by 9.84 per cent to N3.35, Guinea Insurance improved by 9.38 per cent to N462.90, and Lafarge Africa gained 8.52 per cent to close at N233.20.

On the flip side, Omatek lost 10.00 per cent to trade at N2.07, Austin Laz declined by 9.93 per cent to N3.99, Coronation Insurance dipped by 9.88 per cent to N2.92, Zichis crashed by 9.58 per cent to N12.55, and Cornerstone Insurance retreated by 8.77 per cent to N5.20.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange closed the last trading session of the week in the southern territory after further losing 0.59 per cent on Friday, April 10.

This happened as three price decliners weakened the NASD market due to continued sell-offs. The bourse did not finish in green this week.

11 Plc lost N24.70 to close at N222.30 per share compared with the previous day’s N247.00 per share, MRS Oil dropped N1 to settle at N164.00 per unit versus Thursday’s N165.00 per unit, and Geo-Fluids decreased by 25 Kobo to N3.00 per share from N3.25 per share.

As a result, the market capitalisation shrank by N13.79 billion to N2.315 trillion from N2.329 trillion, and the NASD Unlisted Security Index (NSI) declined by 23.05 points to 3,870.45 points from 3,893.50 points.

Yesterday, there were two price gainers led by Central Securities Clearing System (CSCS) Plc, which chalked up N1.07 to sell at N64.21 per unit versus N63.50 per share, and Impresit Bakalori Plc appreciated by 22 Kobo to N2.42 per share from N2.20 per share.

The volume of securities fell by 81.9 per cent to 188,593 units from 1.04 million units, the value of securities decreased by 36.3 per cent to N25.7 million from N40.4 million, and the number of deals remained unchanged at 26 deals.

Great Nigeria Insurance (GNI) Plc was the most traded stock by value on a year-to-date basis with 3.4 billion units valued at N8.4 billion, followed by CSCS Plc with 57.6 million units exchanged for N3.9 billion, and Okitipupa Plc with 27.6 million units worth N1.8 billion.

GNI Plc was also the most traded stock by volume on a year-to-date basis with 3.4 billion units transacted for N8.4 billion, followed by Resourcery Plc with 1.1 billion units s0ld for N415.7 million and Infrastructure Guarantee Credit Plc with 400 million units traded at N1.2 billion.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn