Economy

Nigerians Defy Central Bank, Flock to Bitcoin

By: Gerelyn Terzo of Sharemoney

Bitcoin, the leading cryptocurrency, has seen its value balloon by more than 100% year-to-date, soaring to an all-time high of more than USD 60,000.

Nigerians, many of whom are battling poverty, would be hard-pressed to miss out on those gains. This is especially true considering that the unemployment rate in the most populous African nation was 33.3% as of last quarter, with more than 23 million Nigerians out of work.

Enter bitcoin, which has been a safe-haven investment as well as a faster and cheaper payment method for the growing segment of the population that is catching on.

In fact, Nigeria last year rose to the top of the heap for bitcoin trading at $400 million in volume, surpassing transactional volume in nearly every other jurisdiction — with the exception of the United States and Russia — as traditional asset classes lose their appeal in comparison and the local currency, the naira, remains under pressure.

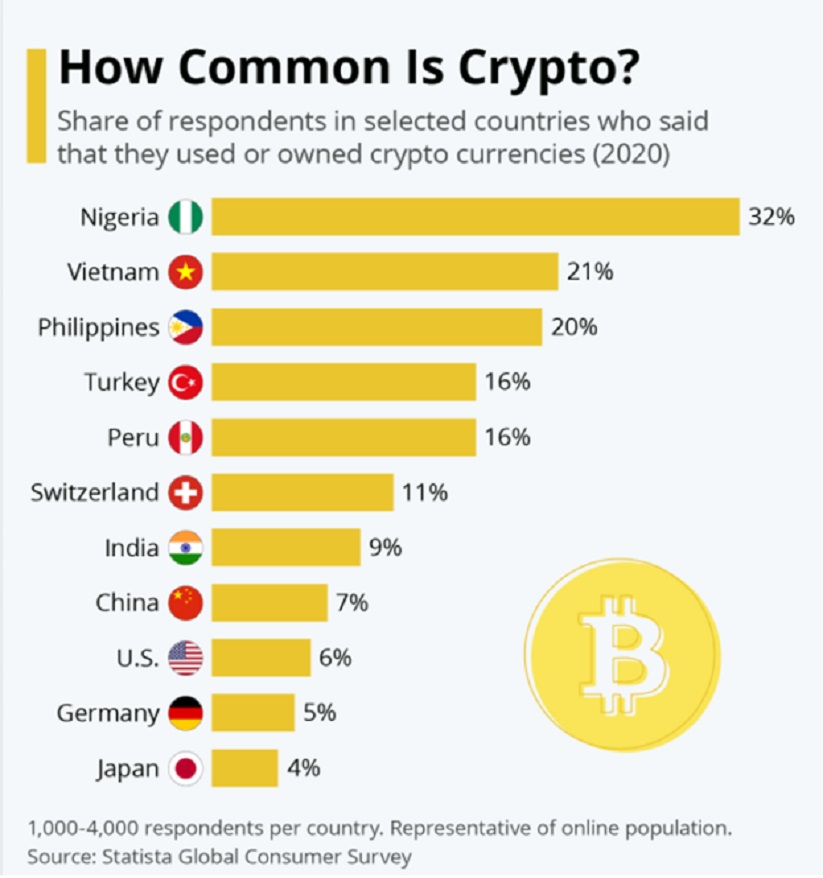

Nearly one-third of Nigerians who participated in a Statista poll said that they used or owned cryptocurrencies, more than any other country represented in the survey.

Source: Statista

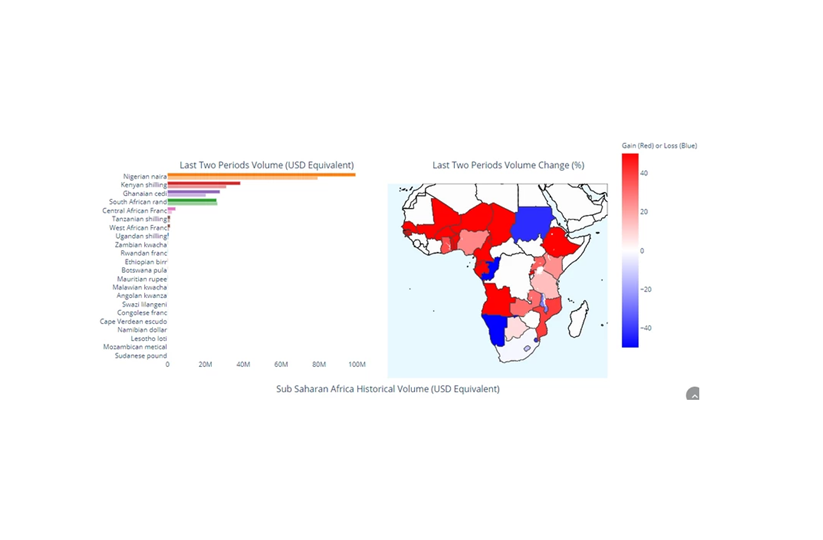

Nigeria also stands out in all of Africa, as the top peer-to-peer bitcoin trading nation on the continent based on bitcoin trading volume.

Nigeria’s P2P BTC trading volume surpassed USD 99 million in the first quarter of 2021. Kenya is a distant second at $34.8 million followed by Ghana and South Africa at $27.4 million and $25.8 million, respectively.

Source: Business Insider/Useful Tulips

The robust bitcoin trading activity in Nigeria has earned the country the title of Africa’s Bitcoin Nation. A 27-year-old Nigerian office worker who was spotlighted by the AFP, Chigoziri Okeke, described how he first invested in cryptocurrencies five years ago with the intention of just making a payment.

When his crypto wallet’s value increased by 10% in a few short days, however, he was hooked and started directing a percentage of his salary toward the market. Today, this investor’s crypto portfolio is worth USD 50,000, comprising various digital assets.

In addition, Google searches of bitcoin in Nigeria surpass that of any other jurisdiction, according to Nairametrics.com. Bitcoin appeals especially to the West African nation’s millennial generation, who are looking to the flagship cryptocurrency as a store-of-value asset as well as a way to circumvent the hoops they must jump through to open a traditional investment account.

With the bitcoin price most recently hovering at USD 60,000, Nigerians have reason to be excited. At this price, one bitcoin could reportedly buy someone a three-bedroom apartment in Lagos’ Ajah neighbourhood.

Unstable Fiat Currency

A big part of bitcoin’s popularity is due to Nigeria’s unstable naira. The International Monetary Fund (IMF) has drawn a line in the sand, stating that Nigeria’s fiat currency is “overvalued” by more than 18%. The IMF wants Nigeria to devalue its fiat currency, but the African nation’s government has said no way.

Nigerian President Muhammadu Buhari blames “global outflows” triggered by COVID-19 for the unstable naira and believes that devaluing it further after doing so twice in 2020 would only exacerbate the already sky-high inflation rate, which is currently in the double-digits at more than 17%. This would weaken Nigerians’ purchasing power even more. Nigeria’s central bank slashed the naira’s value by close to one-quarter last year.

Meanwhile, not only has bitcoin been generating returns hand over fist, but it has also been thrust into the global spotlight amid the SARS-related protests in Nigeria.

According to reports, Nigeria thwarted financial payments toward police brutality protests, which only led the supporters to donate bitcoin instead. Twitter and Square CEO Jack Dorsey backed this movement, which only brought more attention to the country and cryptocurrencies.

Source: CoinGecko/TradingView

Mixed Signals

Nigeria’s central bank has been highly critical of bitcoin, warning as recently as February that “cryptocurrencies are largely speculative, anonymous and untraceable.”

Nonetheless, the Central Bank of Nigeria can’t stop the population from accessing the flagship cryptocurrency, thanks to the peer-to-peer nature of bitcoin, which was inherently designed to circumvent third-party service providers like banks.

Bitcoin creator Satoshi Nakamoto, whose real identity remains a mystery, defined the first cryptocurrency in the whitepaper, which was published in 2008, saying:

“A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.”

The Central Bank of Nigeria has since backtracked from its remarks slightly, maintaining that it has not placed a blanket ban on cryptocurrency trading. It is a tangled web, however. The central bank instead said that it is doubling down on a 2017 law that bans institutions supporting cryptocurrency transactions.

Even though institutions might be banned from supporting cryptocurrency trading, individuals are still free to trade them. The central bank is sending mixed signals, to say the least, as local banks were instructed by the central bank to refrain from doing business with customers who transact in cryptocurrencies.

“The CBN did not place restrictions from use of…cryptocurrencies and we are not discouraging people from trading in it. What we have just done was to prohibit transactions on cryptocurrencies in the banking sector,” stated Adamu Lamtek, according to Decrypt, citing Today NG.

Since the restrictions were imposed on Nigeria’s crypto trading industry, rather than disappearing, the industry has flexed its muscle for its nimble nature. In a few short months, they have been quick to build P2P exchanges that circumvent the crypto ban on financial institutions.

The restrictions have funnelled more activity to over-the-counter (OTC) venues while a makeshift P2P market is similarly expanding. Danny Oyekan, the founder of global social payments application Coins App, is cited by Decrypt as saying,

“So basically, the ban only forced the fiat channels underground.”

Source: Twitter

In Nigeria, cryptocurrencies are regulated by the country’s own Securities and Exchange Commission, which last year stated that it would classify cryptocurrencies as securities unless they are proven otherwise by the asset’s issuer or sponsor. In February, Nigeria’s SEC said that crypto regulation was going to be placed on the back-burner amid the central bank’s crypto crackdown.

Despite the uncertainty, Nigerians are showing no signs of relenting in their pursuit to own bitcoin and are increasingly relying on P2P trading platforms to do just that.

By Aduragbemi Omiyale

One of the newest members of the Nigerian Exchange (NGX) Limited, Zichis Agro-Allied Industries Plc, has confirmed its intention to approach the capital market to raise funds, subject to shareholder and regulatory approval.

However, it denied reports suggesting it’s “set to undertake an Initial Public Offering (IPO) or related capital raising activity.”

In a notice on Monday, the firm affirmed proposing “to seek shareholders’ approval at its forthcoming Annual General Meeting (AGM) to raise additional capital, which may be through equity, debt, or a combination of both, subject to regulatory approvals and market conditions.”

“At this stage, the structure, timing, and details of any such capital raising have not been finalised, and no specific transaction has been concluded,” a part of the statement signed by the company secretary, Solomon Itsede, stressed.

Zichis expressed its commitment to upholding “the highest standards of corporate governance, transparency, and timely disclosure.”

“Accordingly, any material corporate actions or capital market activities will be formally communicated through the appropriate regulatory channels,” it said, advising shareholders and the investing public “to rely solely on official disclosures and filings made by the company through the NGX and other authorised regulatory platforms when making investment decisions.”

Zichis welcomed the “continued interest of investors and market participants in its operations and performance,” promising to remain focused on delivering sustainable value through disciplined strategic execution.

It also lauded the continued support of its shareholders, saying it remains committed to maintaining transparency in all its communications.

By Adedapo Adesanya

The Nigerian Electricity Regulatory Commission (NERC) has issued a directive to ensure transparency in reporting the Regional Electricity Transmission Loss Factor, as it remains above the 7 per cent threshold.

In a public notice posted on its official X (formerly Twitter) on Monday, the order, contained in No. NERC/2026/026 is aimed at improving transparency and efficiency in Nigeria’s power grid through enhanced reporting of Regional Transmission Loss Factors (TLF).

The regulator disclosed that the order is backed by the provisions of the Electricity Act 2023, which enables the commission to regulate, monitor, and ensure efficiency in the power sector.

According to the statement, the Data from the Nigerian Independent System Operator (NISO) indicate that the national average TLF was 8.71 per cent in 2024 but was reduced to 7.24 per cent in 2025.

The statement added that the report exceeds the 7 per cent benchmark approved by NERC in the Multi-Year Tariff Order (MYTO).

The statement reads, “The Order dated 8 April 2026 establishes a formal framework for reporting transmission losses across regions operated by the Transmission Company of Nigeria (TCN).

“Taking effect from 13 April 2026, the Order is backed by provisions of the Electricity Act 2023, which empower NERC to regulate, monitor, and ensure efficiency in the electricity market.”

The directive reads, “NISO to install smart meters at all boundary regional interconnection points by December 2026 to accurately measure energy flows for each region of the transmission network.

“NISO to measure and document all energy flow of power transformers at transmission substations.

“NISO to file quarterly reports on TLF to NERC on a regional basis.”

It added, “TCN to file an action plan by July 2026 on the reduction of TLF to a value within the 7 per cent approved benchmarks in the regions.

“TCN to ensure that TLF across transmission regions shall not exceed 6.5 per cent by December 2026.”

NERC concluded that the order is designed to strengthen accountability in transmission operations and support better grid performance through structured loss reporting.

By Adedapo Adesanya

Nigerian businessman, Mr Aliko Dangote, is planning to list shares of his $20 billion oil refinery on multiple African stock exchanges.

The landmark cross-border public offering on the continent was disclosed by the chief executive of the Nairobi Securities Exchange (NSE), Mr Frank Mwiti, following a meeting held last week in Lagos between Mr Dangote and several heads of African exchanges.

Last year, Mr Dangote unveiled plans to list a 10 per cent stake in his Lagos-based refinery on the Nigerian Exchange this year.

According to a Bloomberg report, citing an email from the chief executive of FirstCap, Mr Ukandu Ukandu, Stanbic IBTC Capital Limited, Vetiva Advisory Services Limited, and FirstCap Limited have been appointed as advisers for the initial public offering of Dangote Petroleum Refinery and Petrochemicals FZE.

Mr Mwiti said the proposed listing is designed to cut across multiple markets and deepen investor participation across the continent.

“The plan is to structure a pan-African IPO,” he said.

Bloomberg also reported that a spokesman for the Dangote Group confirmed that discussions had taken place between Mr Dangote and exchange officials but declined to provide further details.

In February 2026, Mr Dangote said that the IPO could be launched within the next five months.

“But individually Nigerians too will have an opportunity in the next maximum four or five months, they will actually be able to buy their shares,” he said at the time.

He added that investors would have flexibility in how they receive returns.

“People will have a choice either to get their dividends in naira or to get their dividends in dollars because we earn in Dollars.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn