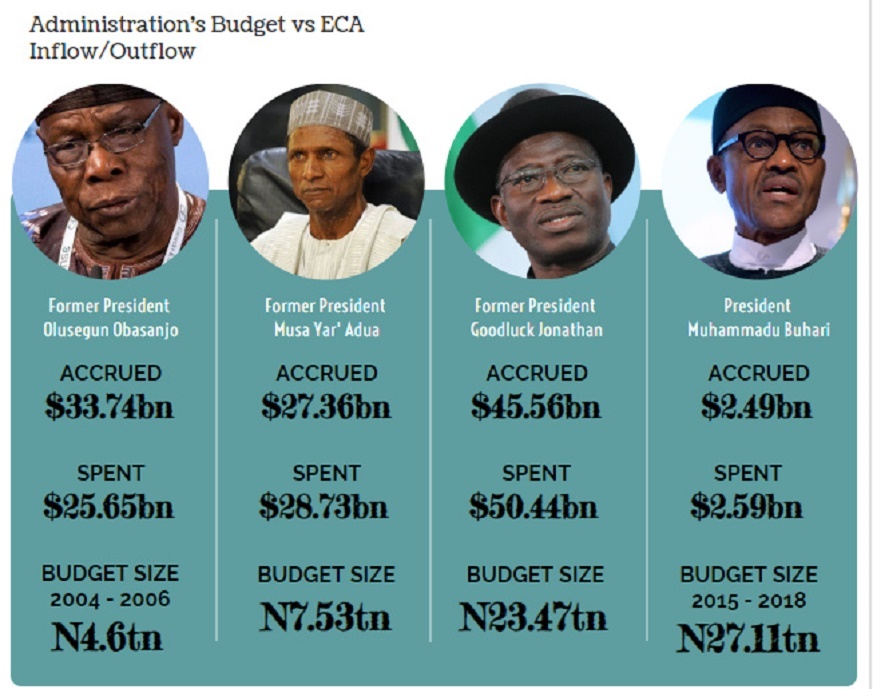

Economy

Nigeria’s Excess Crude Account Worst-Managed Funds—Report

By Modupe Gbadeyanka

The Excess Crude Account (ECA) of Nigeria has been described as the “worst-governed funds” in the world.

A report released yesterday by released today by the Natural Resource Governance Institute (NRGI) disclosed that the index assessed the governance and transparency of sovereign wealth funds in 33 countries, where Nigeria was the least.

“Colombia’s Savings and Stabilization Fund is the best-governed of the assessed funds, followed by the Ghana Stabilization Fund.

“The Qatar Investment Authority, with $330 billion in assets, and Nigeria’s Excess Crude Account were found to be the worst-governed funds.

“At least $1.5 trillion is currently managed by the 11 sovereign wealth funds NRGI researchers rated as failing,” the agency said in the statement.

It was revealed that Chile’s Codelco state mining company was listed as the best-governed of 74 extractive sector state-owned enterprises that were assessed for their disclosures and corporate governance. The Oil and Natural Gas Corporation of India came second.

Forty-eight countries’ state-owned companies received unsatisfactory ratings. The index identifies weak governance in the China National Petroleum Company, and finds failing governance in the Abu Dhabi National Oil Company, the Gabon Oil Company, Turkmengas and Saudi Aramco.

Commenting, Ernesto Zedillo, former president of Mexico and chair of NRGI’s board of directors of the agency said, “The Resource Governance Index shows us that if they are to contribute to their countries’ development, state-owned enterprises require serious reform.”

“But effective governance of the oil, gas and mining sectors is not an insurmountable challenge—the index provides many examples of developing countries defying expectations and stereotypes,” Zedillo adds.

In recommendations released with the data, NRGI called on governments to support key transparency measures (including compliance with open data standards) and for them to adopt and implement laws requiring the disclosure of the identities of the true beneficiaries of oil and mining companies.

NRGI also called for a reversal of the trend toward closing civic space in many resource-rich countries.

“Where freedoms of citizens and journalists are under attack, governance of the extractives sector is fundamentally impaired,” said Kaufmann. “Access to information on contracts, revenues, state companies and sovereign wealth funds is only valuable when citizens can hold authorities and companies to account.”

Also, the report stated that the majority of governments inadequately govern their oil, gas and mining sectors, according to the 2017 Resource Governance Index.

Sixty-six countries were found to be weak, poor or failing in their governance of extractive industries. Less than 20 percent of the 81 countries assessed achieved good or satisfactory overall ratings.

The cross-country study of extractives governance, released today by the Natural Resource Governance Institute (NRGI), is the most comprehensive of its kind to date. It is based on new research into how countries’ governance affects their potential to realize value and manage revenues from their resources. It also incorporates existing assessments of countries’ “enabling environments”—a measure of how well citizens can access and use information, freely work together to voice their concerns and hold their governments to account, and of the quality of institutions in the areas of administration, rule of law and corruption control, the statement said.

By Adedapo Adesanya

The National Insurance Commission has issued new guidelines for the collection, management, and administration of the Insurance Policyholders’ Protection Fund.

In a circular issued to all insurance institutions on Tuesday, the regulator also set May 31, 2026, as the deadline for insurers to submit their assessment returns for the 2025 financial year.

Recall that on August 5, 2025, President Bola Tinubu signed into law the Nigerian Insurance Industry Reform Act ( NIIRA 2025).

This landmark legislation repeals the Insurance Act 2003, and consolidates related provisions, ushering in a modern regulatory framework. It lays a strong foundation for sustainable growth and increased investment in the country’s insurance sector.

The commission said the guidelines were issued in exercise of its powers under the 2025 Act and other existing insurance laws and regulations to provide regulatory clarity, improve guidance, and ensure ease of compliance across the industry.

According to NAICOM, the guidelines establish a comprehensive structure for the operation of the IPPF, which serves as a statutory safety net to protect insurance policyholders in the event of distress or insolvency of a licensed insurer or reinsurer. The framework also provides direction on the reimbursement of loans by insurers and reinsurers.

NAICOM stated, “The guidelines ensure regulatory clarity, guidance and ease of compliance, as it provides a comprehensive regulatory framework for the collection, management, and administration of the Fund, which serves as a statutory safety net designed to protect insurance policyholders against distress and insolvency of a licensed insurer or reinsurer, including guidance for the reimbursement of loans by an insurer or reinsurer.

“Please be informed that the IPPF Assessment Returns in respect of the year 2025 shall be submitted to the Commission not later than 31st May 2026, while subsequent submissions shall be in line with Section 4.3 of the Guideline on Insurance Policyholders Protection Fund.”

By Adedapo Adesanya

The Dangote Refinery on Wednesday returned the petrol price to N1,200 per litre, less than 24 hours after it increased it by 5 per cent.

The private refinery had raised the ex-depot price by N75 on Tuesday, citing pressure from volatile global oil markets, but quickly brought it back to N1,200 per litre from N1,275 per litre.

The swift downward review is directly linked to a sharp drop in international crude prices. Brent crude has plunged to $95.05 per barrel, after a 13 per cent decline, while the US West Texas Intermediate (WTI) crude closed at $97.18, recording nearly a 14 per cent drop.

This development comes after US President Donald Trump announced a conditional two-week ceasefire with Iran, which eased fears of immediate supply disruptions in the global oil market.

“This will be a double-sided CEASEFIRE!” Trump said on social media, marking a sharp reversal from his earlier warning that “a whole civilisation will die tonight” if Iran failed to comply with US demands.

Iran’s Foreign Minister, Mr Abbas Araqchi, confirmed that the country would halt attacks provided strikes against Iran cease and transit through the Strait of Hormuz is coordinated by Iranian forces.

Despite the breakthrough, tensions remain elevated across the region, with several Gulf states reporting missile launches, drone activity, or issuing civil defence warnings.

While oil prices have fallen back below $100, they remain significantly elevated after surging by a record amount in March. Market analysts noted that regardless of how successful the ceasefire is, geopolitical risk related to the Strait of Hormuz is likely to remain elevated for the foreseeable future under the control of Iran.

By Adedapo Adesanya

Crude oil deliveries from the Nigerian National Petroleum Company (NNPC) Limited to the Dangote Petroleum Refinery doubled in March, boosting prospects for improved fuel availability.

This was revealed by the chief executive of Dangote Industries Limited, Mr Aliko Dangote, on Tuesday, when he received the Deputy Secretary-General of the United Nations, Mrs Amina Mohammed, at the industrial complex in Ibeju-Lekki, Lagos.

While speaking on feedstock supply, Mr Dangote commended the NNPC for increasing crude deliveries to the refinery in March, noting that volumes rose to 10 cargoes—six supplied in Naira and four in Dollars—to support domestic fuel availability, according to a statement by the Refinery.

“Last month, they gave us six cargoes for Naira and four cargoes for Dollars,” he said.

Despite the improvement, Mr Dangote noted that the supply remains below the 19 cargoes required for optimal operations, with the refinery continuing to bridge the gap through imports from the United States and other African producers.

He also expressed concern over the unwillingness of international oil companies operating in Nigeria to sell to the refinery, stating that their preference for selling crude to traders forces it to repurchase at higher costs, with broader implications for the economy.

Mr Dangote added that the refinery is seeking increased access to domestically priced crude under local currency arrangements as part of efforts to moderate fuel costs and enhance long-term energy and food security across the continent.

On her part, Mrs Mohammed underscored the strategic importance of Dangote Industries Limited -particularly Dangote Fertiliser Limited—in addressing Africa’s mounting food security challenges, while calling for stronger global partnerships to scale its impact.

Mrs Mohammed said the United Nations would prioritise amplifying scalable solutions capable of mitigating the continent’s food crisis, describing Dangote’s integrated industrial model as a critical pathway.

“I think the UN’s job here is to amplify and to put visibility on the possibilities of mitigating a food security crisis, and this is one of them,” she said. “I hope that when we go back, we can continue to engage partners and countries that should collaborate with Dangote Industries.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn