Feature/OPED

Eze Chikamnayo: The Archetypal Chichidodo

By Okechukwu Ukpabi

The more things change, the more they stay the same, the French writer, Jean-Baptiste Alphonse Karr, wrote in 1849. It is, therefore, not surprising that nine years after he was fuming in the mouth in political fits, he will resort to the same crass tactics of name-calling, absolute falsehood, and dubious claims to be noticed in 2023, barely two months of he and his ilk falling from power.

Like the typical bird, chichidodo, in Ayi Kwei Armah’s novel, The Beautiful Ones Are Not Yet Born, that screams its lungs out in protestation of shit, yet feasts on maggots so is the fate of Eze Chikamnayo, a failed commissioner of (mis)information under the calamitous rule of the immediate past administration in Abia state.

Chikamnayo is regarded in many quarters as a metaphor for confusion, ironic hypocrisy, a wolf in sheep’s clothing, a ghost in human flesh, a doppelganger and a political maggot who grows best in the foul-smelling lavatory of hypocrisy and patronizing intrusiveness.

For clarity and for those who may not be in the know of the character and content of the roguish and tout-like Mr. Chikamnayo, he once postured as a rabid vuvuzela of decency and accountability. He was up in arms against some of the people who were in government in Abia state but ended up being a diseased defender of the same ruinous years in the state as Commissioner of Information.

Owing to the fact that proverbs (ilu) are “the salt with which words are eaten,” it is appropriate to remind Mr. Chikamnayo, whose law practice remains at best a charge and bail affairs that, Ijiji na-enweghi onye ndumodu na-eso ozu ala n’inyi (A fly that has no counsellor follows the corpse to the grave.)

In the event he fails to grasp the import of the above, then it is instructive that he knows that, O bulu na i taa m aru n’ike, ma i zeghi nshi; mu taa gi aru n’isi, agaghi m ezere uvulu (If you bite me on the butt, despite the danger of sinking your teeth into the faecal matter, then if I bite you on the head, I will disregard the danger of sinking my teeth into the cerebral matter.)

On July 25, the propagandist of the last locust era went caustic in a piece of lies, conjectures and insidious intrusiveness against not just the Office of the Governor of Abia State but the person of His Excellency, Dr Alex Otti. Ordinarily, it is a piece borne of inherent mischief and pathological disorder. But like in all situations of aru (madness), it requires a potent, no less corrosive, but effective in curing.

Otti the democrat

We no longer live in an age without meaning and where there is a struggle for definition. But unfortunately, Mr. Chikamnayo is unaware of this when he sounded like a bad record player that Governor Otti is not a democrat for insisting that those who presided over the Abia patrimony in the immediate past eight years should account for their years in office.

Unlike those he served, Dr Otti has always trusted in the sacredness of the ballot as a veritable means of electing leaders. And on each occasion he ran for the governorship, he worked in consonance with the laid down guidelines, shrugging off thuggery, ballot snatching and attempting to induce electoral officials, which are hallmarks of Chikamnayo’s horde.

Regrettably, for the purveyors of the ancien regime in Abia, the democratic credentials of Governor Otti remain unassailable. When they were trying to undermine the people’s wish, especially in Obingwa Local Government Area in the last election, Candidate Otti, as he then was, trusted in the integrity of the electoral umpire to do what was right by law, and the INEC did, and the whole shroud of an attempt to manipulate, induce and subvert the credibility of the ballot by Mr Chikamnayo’s crowd of the indolent failed, and the rest is their being of office and power.

What manner of democrat did Mr Chikamnayo serve under who hires and fires Local Government Area Transition Committee Chairmen barely after 20 days? So much for a democrat who failed to hold council polls until the dying embers of a pathetic period in office. Because the madman knows no shame, he prances about in the marketplace with his phallus dangling proudly to the shame of his kith and kin. Such is the folly of Chikamnayo!

No brainer on accounts

It is a surprise that Mr. Chikamnayo is adept at finances yet could not offer such services in the administrations he served. Well, his financial ability is but a stinking lavatory of moral excrement. His claims of how much the Abia statement government has garnered is rusty and pale into the pitiable pit the government he served left it.

For the avoidance of doubt, the Okezie Ikpeazu empire, which he was a part of, left a humongous debt burden of N191.24bn and an empty treasury when he handed over the affairs of the state to Dr. Otti on May 29.

It is an incontrovertible fact that the sum of N77,927,939,042.82 was owed banks in the country, N71,022,162,441.01 was owed as domestic debt while external debts liabilities was put at N42,289,206, 109.84. A further breakdown of the indebtedness shows that of the N77,927,939,042.82 owed banks, United Bank for Africa accounted for N8,012,830,371.44; Zenith Bank N21,557,168,761.71; Union Bank N597,637,399.55 and Central Bank of Nigeria N47,760,302,510.12.

For the domestic debt obligation, salaries and subvention arrears stand at N18,162,102,692.92; pension arrears N21,283,876,789.80; gratuity arrears N27,012,996,061.64; and contractors arrears N4,563,186,896.65.

The good news is that Dr Otti towers above the mediocrities of Chikamnayos in financial mileage, business acumen and governance provenance. Blocking leakages in the area of ghost workers and revenue loss in the scatter-gun administration of parks will not be sacrificed on the altar of political expediency. The former (mis)information commissioner can be forgiven since the order and lawful means are anathema to him and his congress of baboons. The hard work of resetting the Abia Project will not be mortgaged for those who have no scruples.

The failed SDP political hawker without scruples can bray from now till eternity; his shenanigans to be noticed is what it is –nothing!

Dr Otti is leading a team of dedicated men and women working with surgical precision to diagnose the Abia predicament and unleash the creative and industrious energies of Abians; there is a sense of a powerful current tearing down an old decrepit system; he is building a new ordered freedom based on the rule of law and human rights. And not a thousand clanging cymbals of Chikamnayo and the tribe of the aggrieved will stop the Abia Renaissance.

Mr Ukpabi, a public affairs commentator, wrote in from Ohafia, Abia State

By Henry Obiekea

Nigeria’s banking industry is entering one of the most significant transformation periods since the 2005 banking consolidation exercise. The Central Bank of Nigeria’s (CBN) ongoing recapitalisation programme is more than a regulatory requirement—it is a strategic investment in the country’s financial future. If implemented successfully, it has the potential to strengthen financial stability, deepen credit access, improve investor confidence, and support a more inclusive and resilient economy.

In March 2024, the CBN announced new minimum capital requirements for commercial, merchant and non-interest banks. Under the new framework, international commercial banks are required to maintain a minimum paid-up capital of ₦500 billion, national commercial banks ₦200 billion, and regional commercial banks ₦50 billion. Merchant banks are required to hold ₦50 billion, while national and regional non-interest banks are required to maintain ₦20 billion and ₦10 billion respectively. The policy reflects the realities of today’s economy, where inflation, currency depreciation and expanding financial demands have significantly altered the capital required to support sustainable banking operations.

Many institutions have responded through rights issues, public offers, private placements, mergers and acquisitions in pursuit of the revised capital requirements. Beyond regulatory compliance, the exercise is already encouraging stronger governance, better capital planning and increased investor participation within Nigeria’s financial markets.

The recapitalisation conversation, however, extends beyond deposit money banks. The CBN has also introduced revised capital requirements for microfinance banks, recognising the critical role they play in extending financial services to underserved individuals, nano businesses and small enterprises. As the financial landscape becomes increasingly digital, stronger capital bases will enable these institutions to invest in technology, cybersecurity, risk management and product innovation while maintaining public confidence.

For Nigeria’s rapidly growing fintech ecosystem, although they are subject to different licensing frameworks depending on their operations, the broader regulatory direction is equally clear. Institutions that facilitate payments, tech-enabled banking, lending and savings are expected to maintain governance, capital and consumer protection standards appropriate to their respective licensing frameworks. This evolution is essential as fintechs continue to account for a growing share of financial transactions and provide services to millions of previously underserved Nigerians. Collectively, these reforms present a unique opportunity to reshape Nigeria’s financial ecosystem.

A stronger banking sector creates stronger economic outcomes. Well-capitalised financial institutions are better positioned to finance infrastructure, manufacturing, agriculture, housing and technology. They possess greater capacity to absorb economic shocks, support long-term lending and withstand periods of market volatility. More importantly, they can extend larger volumes of prudently underwritten credit to businesses that create jobs and stimulate economic growth.

For small and medium-sized enterprises, which contribute significantly to Nigeria’s GDP and employment, improved access to financing remains one of the greatest growth enablers. Recapitalisation should not be assessed solely by stronger balance sheets, but also by the extent to which additional capital supports productive economic activity.

Despite remarkable progress over the last decade, millions of Nigerians remain underserved by formal financial institutions. Expanding financial inclusion requires complementary approaches across commercial banks, microfinance banks, fintechs and other regulated financial institutions. Achieving meaningful inclusion requires collaboration across commercial banks, microfinance banks, fintech companies and regulators. Each institution serves different customer segments, yet all contribute towards a common objective: bringing more Nigerians into the formal financial system.

At FairMoney Microfinance Bank, recapitalisation aligns with our continued investment in responsible lending, digital banking capabilities, sound risk management and financial inclusion. We believe technology can complement prudent credit assessment and help extend access to financial services for eligible individuals and businesses.

As the recapitalisation programme progresses, success should ultimately be measured by broader outcomes: stronger institutions, deeper financial inclusion, increased SME financing, enhanced consumer confidence and sustained economic growth. Capital itself does not transform economies; how that capital is deployed does.

The Federal Government and the Central Bank of Nigeria have introduced reforms aimed at strengthening the long-term resilience of the financial sector. Continued implementation of these reforms will be important in supporting financial stability and sustainable sector growth. These decisions require vision, consistency and regulatory discipline. While the adjustment process may present short-term challenges for some institutions, the long-term benefits for financial stability, investor confidence and economic development far outweigh the costs.

Nigeria possesses one of Africa’s most dynamic financial services sectors. With stronger capital foundations, responsible innovation and continued collaboration between regulators and financial institutions, the country is well positioned to build a banking ecosystem capable of supporting its development ambitions, empowering millions more individuals and businesses, and supporting inclusive economic development over the long term.

Henry Obiekea is the Managing Director of FairMoney Microfinance Bank

By Sani Abdulrazak, PhD

People go through watershed moments sometimes when the cacophony of politics attempts to drown the cadence of progress; it becomes more serious when chimaera masquerades as certainty, but it is a known fact after all that the loudest voices are most times not necessarily the wisest.

Kaduna seems to have arrived at one of those moments. The propagandist opposition within the state is trying very hard to burnish manifestoes and criticisms wrapped in hyperbole and rehearsed until it begins to mistake itself for truth.

Yet, history has always been an unforgiving arbiter. It has an uncanny habit of stripping rhetoric naked, leaving only the vestiges of deeds. It is against that backdrop that one is compelled to reflect, not on who shouts the loudest, especially on social media, but on who has quietly altered the landscape of the beautiful crocodile state. That, conceivably, is the choice before Kaduna State.

Education hewn the destiny of a society, long before it is announced in boardrooms. Governor Uba Sani of Kaduna State appears to appreciate this axiom. As if constructing hundreds of classrooms, renovating neglected schools, expanding access to education and reviving projects abandoned to bureaucratic torpor is not remarkably astral, his administration has gone further to make tertiary education more affordable through the reduction of tuition fees in state-owned institutions. That single decision has become a bulwark against hopelessness for thousands of families. Parents breathe easier, students remain in school instead of abandoning their dreams, enrolment has received fresh impetus, and human capital has become a little less hostage to economic adversity.

Even the reconstruction of roads within Ahmadu Bello University, despite its federal status, speaks of governance that refuses to hide behind jurisdictional caveats. Curiously, while lecture halls become fuller, some critics remain engrossed in composing jeremiads, as though hashtags now award degrees and social media threads have replaced convocation ceremonies. If this does not deserve another term, then perhaps Kaduna should entrust its classrooms to keyboard warriors instead?

A sector that defies drama, yet consequentially integral in Kaduna State is healthcare. Primary Healthcare Centres have continued to receive upgrades, sixteen general hospitals have witnessed rehabilitation, the once-abandoned 300-bed Specialist Hospital has emerged from years of limbo, health insurance coverage has expanded considerably, and investments in personnel and equipment continue with assiduity. Yet, one occasionally encounters the strange absurdity wrapped as opposition, that government should be judged not by functioning hospitals but by the virulence of online criticism. It is almost as though some believe ailments or surgeries retreat before social media posts. Should we now replace stethoscopes with microphones or social media posts and call it healthcare?

If there is any sector that more clearly illustrates the difference between governance and grandstanding in Kaduna State, it is agriculture. Mechanisation, dry-season farming, free fertiliser distribution, value addition, the Special Agro-Industrial Processing Zone and renewed support for farmers all point towards a carefully crafted paradigm rather than an accidental policy.

There is a metamorphosis taking place in rural communities indeed. While genuine farmers harvest maize, ginger and tomatoes, critics harvest conspiracy theories with astonishing alacrity. One group tills the soil and produces food; the other tills public resentment. Since when did viral posts become a substitute for fertile fields?

They wouldn’t want to take their ballyhoo to infrastructure for sure, because infrastructure refuses to remain invisible no matter how determined propaganda may be. Roads snake through communities once forgotten, bridges reconnect places long separated, water projects restore hope where scarcity once seemed ineluctable, and abandoned projects have gradually returned from institutional comatose. Yet there exists a peculiar group of disgruntled politicians that notices every pothole repaired only long enough to ask why another one still exists somewhere else. It is a curious predilection, almost quixotic, to dismiss completed projects because perfection has not yet arrived. Must development now apologise for not occurring overnight?

Security remains man’s most delicate labyrinth, and perhaps the easiest subject upon which to score political points. No responsible leader claims absolute victory against insecurity, yet few can deny that many communities once deserted have gradually witnessed the return of farming, commerce and social interaction. Such progress may not satisfy those addicted to political apoplexy, but it certainly matters to the farmer returning to his land after years of displacement. Or should insecurity be preserved simply because it offers better campaign material?

Economic governance, that complex yet rarely glamorous aspect of governance, is not left out. Increased internally generated revenue, prudent expenditure, strategic partnerships, capital investments and fiscal discipline have gradually strengthened Kaduna’s financial architecture. International partners investing in Kaduna State seldom do so because of slogans, but because of credibility. Sadly, the numbers don’t lie as data is a very stubborn thing. Are spreadsheets now expected to consult political parties before balancing their figures, or should economic data also join the opposition?

Youth empowerment deserves equal reflection. With a skills acquisition centre in each of the three senatorial zones of the state, entrepreneurship support, digital innovation and targeted interventions for small businesses, an attempt is being made to replace dependency with productivity. The apotheosis of governance is not the endless distribution of charity but the deliberate creation of opportunity. Young people increasingly seek tools and training against tokenism and expectancy. Still, some measure empowerment only by the number of campaign T-shirts distributed during election season. Have branded caps suddenly become the highest form of economic policy?

The choice before Kaduna State is simpler than it first appears. Shall we exchange reduced tuition fees for recycled promises? Shall rehabilitated hospitals be traded for rehearsed indignation? Shall roads surrender to rhetoric, farms to social media debates, security gains to sensationalism, and fiscal prudence to flamboyant bombast? Shall tangible progress bow before political charlatanry merely because criticism aims to be louder than construction?

For our democracy to grow further, we must come to a non-negotiable conclusion that the ballot is not an instrument for rewarding the most eloquent critic, but for judging the most effective steward. How promising can stewardship be when classrooms are expanding, hospitals are reopening, roads are stretching farther, farmers are receiving greater support, communities are gradually becoming safer, and opportunities are multiplying.

The evidence before us is not ephemerally ethereal, but enduringly concrete. And so, the lingering questions refuse to disappear: if this is not the direction Kaduna should continue, then what is? If these are not the footprints of purposeful leadership, whose are? If measurable progress has become insufficient, what miracle remains outstanding? And if the answer lies somewhere beyond Governor Uba Sani, then who, exactly, has presented Kaduna with a more convincing testament than the one already written across its schools, hospitals, farms, roads and communities?

Sani Abdulrazak, PhD, is a writer, researcher and a public affairs analyst based in Zaria, Kaduna State.

By Blaise Udunze

From a general observation, comparisons are powerful political tools. They simplify complex realities, inspire supporters and shape public perception. Another side of this is that they can also become misleading when symbolism replaces substance.

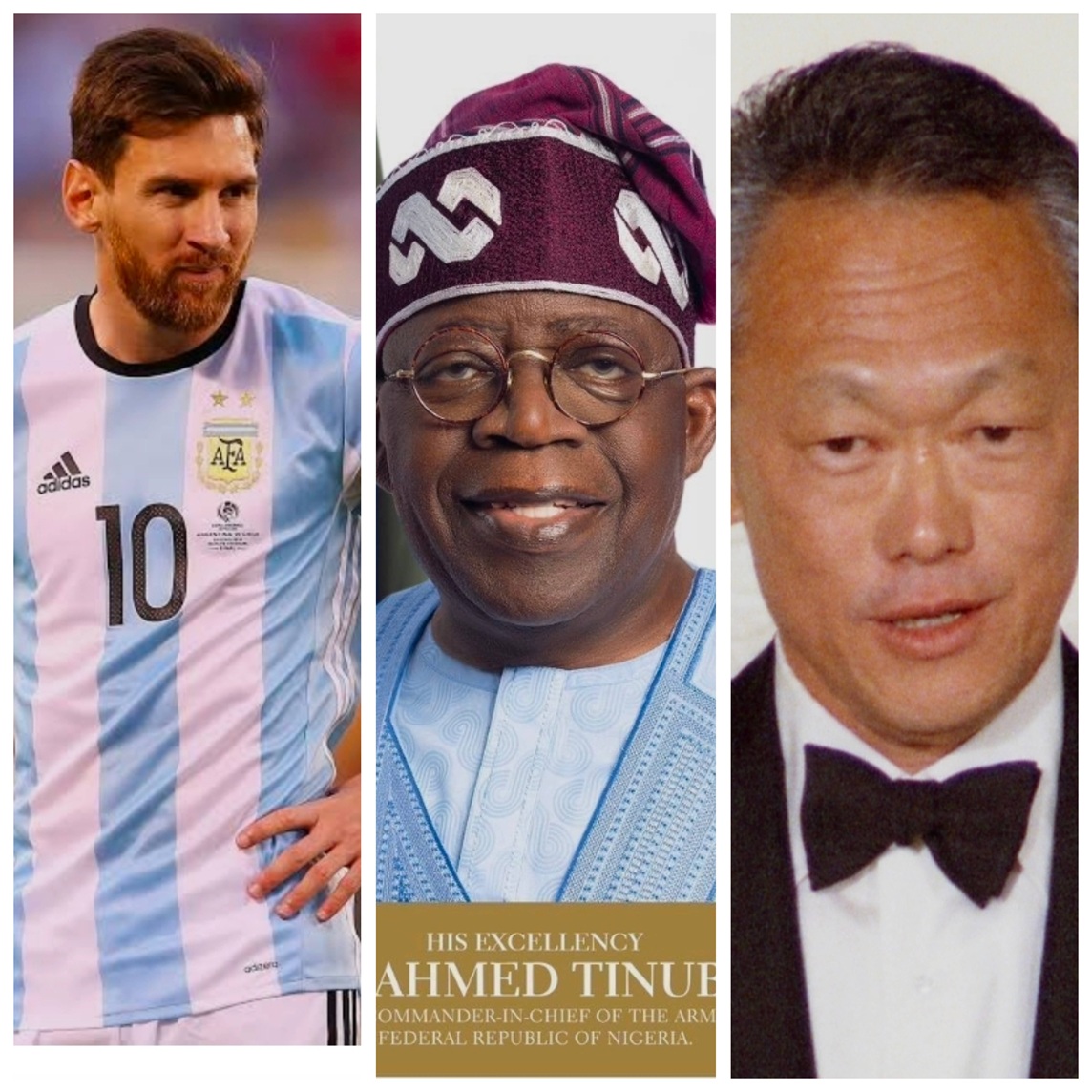

The latter appears to be the objective behind two recent interventions in defence of his excellency, President Bola Ahmed Tinubu. Respectfully, it was observed that veteran journalist Martin Oloja likened Tinubu’s political journey to that of football icon Lionel Messi. He portrayed him as a resilient strategist whose patience and tactical brilliance eventually produced victory. As this now appears to be a trend, Imo State Governor Hope Uzodimma further elevated the narrative, comparing Tinubu to Singapore’s founding Prime Minister, Lee Kuan Yew. He didn’t stop at that; rather further argued that today’s painful reforms would eventually transform Nigeria just as Lee transformed Singapore. They are compelling analogies.

Unfortunately, it was observed that both began to unravel once governance, not politics, was used as the standard of measurement.

It is a known fact to the world that Lionel Messi is celebrated not because he endured criticism or finally lifted the World Cup after years of disappointment. He is celebrated because his greatness is measurable. His goals are counted. His assists are recorded. His trophies are displayed, and not just that, his records speak louder than the opinions of his admirers, which may have taken a different turn now after the outcome of the 2026 FIFA World Cup.

The same is also true of Lee Kuan Yew. History has shown that he is not revered because he introduced difficult reforms or enjoyed the support of loyal political allies. Governor Hope should be reminded that Lee is remembered because he fundamentally transformed Singapore. Amongst his achievements were transforming a poor trading port into one of the world’s richest, cleanest, safest and most efficiently governed nations.

Lee’s records speak for him because under his leadership, Singapore built world-class infrastructure, an incorruptible public service, globally competitive education, affordable housing, investor confidence and one of the highest standards of living anywhere in the world.

Neither Messi nor Lee Kuan Yew became legends through carefully crafted narratives. Yes, they became legends because the evidence became impossible to dispute. That is precisely where comparisons with President Tinubu become difficult.

It is an error to assume that winning elections is the same as winning governance, and at the same time, political brilliance may secure power, but only effective leadership secures history’s approval.

For millions of Nigerians, governance is not measured by campaign strategy or political resilience. It is measured by the realities they confront every morning.

Can they afford food? Can they pay transport fares? Can they pay rent with the current landlords’ economy? Can they keep their businesses open? Can they sleep or travel freely without fear of kidnapping? Can they find jobs after graduation? Can they access reliable electricity and healthcare? These are the scoreboards by which governments are judged.

Supporters of the Tinubu administration frequently point to encouraging macroeconomic indicators. Foreign reserves have improved. Government revenues have risen. States now receive significantly larger allocations through the Federation Account Allocation Committee (FAAC). Well, these ‘achievements’ will be reviewed soon through the lens of news narratives. International financial institutions have welcomed several policy reforms. The removal of fuel subsidy and exchange-rate liberalisation are presented as courageous decisions that previous administrations avoided.

These developments deserve acknowledgement. Yet macroeconomic improvements are not the same as improvements in citizens’ welfare.

In reality, an economy cannot be declared successful merely because government revenues have increased while household purchasing power continues to deteriorate, as this would be a complete aberration.

Again, it is considered an anomaly that Nigeria reports stronger fiscal numbers, but millions of families continue to struggle with soaring food prices, rising transport costs, expensive housing, high electricity tariffs and shrinking disposable incomes.

Statistics may comfort policymakers. They rarely comfort hungry citizens. Messi never celebrated possession statistics after losing a match; rather, he cried and cried over losing the opportunity of winning the trophy at the concluded 2026 FIFA World Cup. To him, results mattered.

The reality is that governments should be judged by the same principle. This is open to dispute, but of a truth, Governor Uzodimma’s comparison to Lee Kuan Yew deserves even closer scrutiny because it raises an important question, though it may appear hard to answer.

If Tinubu is Nigeria’s Lee Kuan Yew, where is Nigeria’s Singapore? What exactly made Lee Kuan Yew exceptional? Was it simply his willingness to implement painful reforms? Certainly not.

Many leaders across the developing world have introduced painful reforms. Very few transformed their countries.

One thing stands out here: Lee’s legacy rests on outcomes, not intentions. Judging from all indications, it is obvious that his reforms dramatically reduced corruption, attracted investment, strengthened institutions, expanded industrialisation, improved education, guaranteed affordable public housing and steadily raised incomes across generations. Unlike Nigeria’s ongoing experience, Singapore’s rise was not a promise repeatedly postponed to the future. Citizens experienced tangible improvements in their daily lives. That is why history celebrates Lee Kuan Yew. Nigeria’s present reality tells a different story.

It is glaring and ironic that despite improved fiscal revenues, many Nigerians continue to grapple with rising inflation, worsening poverty, declining purchasing power, youth unemployment, struggling businesses and persistent insecurity. If they must know, these are not merely economic statistics; they are the lived realities by which citizens judge any government.

The Lee Kuan Yew comparison also overlooks perhaps the most important ingredient behind Singapore’s success, which is primarily the institutions.

It is obvious and practically doubtful if Governor Uzodinma’s kind of Singapore is the same as the one on which its transformation was built upon an efficient bureaucracy, disciplined public institutions, predictable regulation, meritocracy, uncompromising anti-corruption enforcement and consistent long-term planning as championed by Lee Kuan Yew. An honest question here is, can the same be said of Nigeria today?

The truth is not far-fetched; Nigeria is nothing close to it because the realities and lived experiences of Nigerians are that the country continues to grapple with weak institutions, policy inconsistency, bureaucratic inefficiency, corruption concerns and widespread insecurity.

His impeccable achievements are built on the institutions; hence, without institutional transformation, every effort to invoke Lee Kuan Yew risks confusing aspiration with achievement.

One common trend witnessed lately is that the supporters of the administration often argue that Nigerians must be patient because meaningful reforms require time. That argument deserves consideration.

Let it also be made known that patience should never become an endless substitute for accountability. Citizens are also entitled to ask whether the sacrifices demanded today are producing measurable improvements tomorrow.

History remembers leaders not because they prescribed hardship, but because that hardship ultimately produced prosperity for those alive and not for the dead.

Another weakness in both comparisons is the tendency to confuse political mastery with administrative excellence. These are totally two different things, because when it comes to winning elections, it requires coalition building, negotiation and political calculation. Whilst running a nation demands competent institutions, sound economic management, transparency, public trust and measurable improvements in living standards.

Again, the two are not the same, and for this reason, many exceptional politicians have governed poorly. Many successful administrators never became political giants. Democracy ultimately rewards governance, not political mythology.

This is not to suggest that President Tinubu’s administration has achieved nothing. Tax reforms, infrastructure investments, fiscal restructuring and efforts to stabilise public finances represent important policy initiatives whose long-term impact remains to be seen. Well, acknowledging those initiatives is consistent with honest public discourse.

Equally important, however, is recognising that millions of Nigerians continue to judge the administration through the realities and their lived experiences rather than the promises they hear.

Football supporters judged Lionel Messi by the trophies in the cabinet. In like manner, history judges Lee Kuan Yew by the Singapore he built. The same measure should be applied in this nation, as Nigerians will judge President Tinubu by the Nigeria he leaves behind.

The key metric here is that if inflation falls sustainably, poverty declines significantly, insecurity is substantially reduced, electricity becomes more reliable, industries expand, jobs multiply, and citizens regain confidence in the future, history will acknowledge those achievements without requiring comparisons to Messi or Lee Kuan Yew.

Neither Messi nor Lee Kuan Yew needed political allies to persuade the world of their greatness, and that distinguishes both as the greatest of all time (GOAT).

Their records spoke for themselves. Political endorsements may dominate today’s headlines. History, however, listens only to evidence. Even Messi needed trophies. Lee Kuan Yew needed results. Nigerian leaders should be judged by no lesser standard.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com