Feature/OPED

Increasing Competition Policy Enforcement Across Africa

By Angelo Tzarevski

Competition policy continues to be viewed by regulators as a key driver of economic growth globally. Across Africa, competition policy enforcement is increasingly being employed as a tool to boost economic performance and promote the revitalization of trade and industry following the devastating impact of COVID-19.

The effects of the pandemic have led to negative economic growth in a number of African jurisdictions, and have given rise to opportunistic, anticompetitive behaviours such as unreasonable price increases and price gouging, coordination amongst competitors, and other unsavoury business practices that erode competition.

Over the past two years, African competition regulators have actively engaged in efforts to address these pandemic-related effects, however, there has also been a general upward trend in competition policy enforcement across the continent. A number of African jurisdictions have strengthened their competition and antitrust regimes by way of amendments to existing legislation, the introduction of new laws and regulations, and renewed fervour and political will to enforce existing laws.

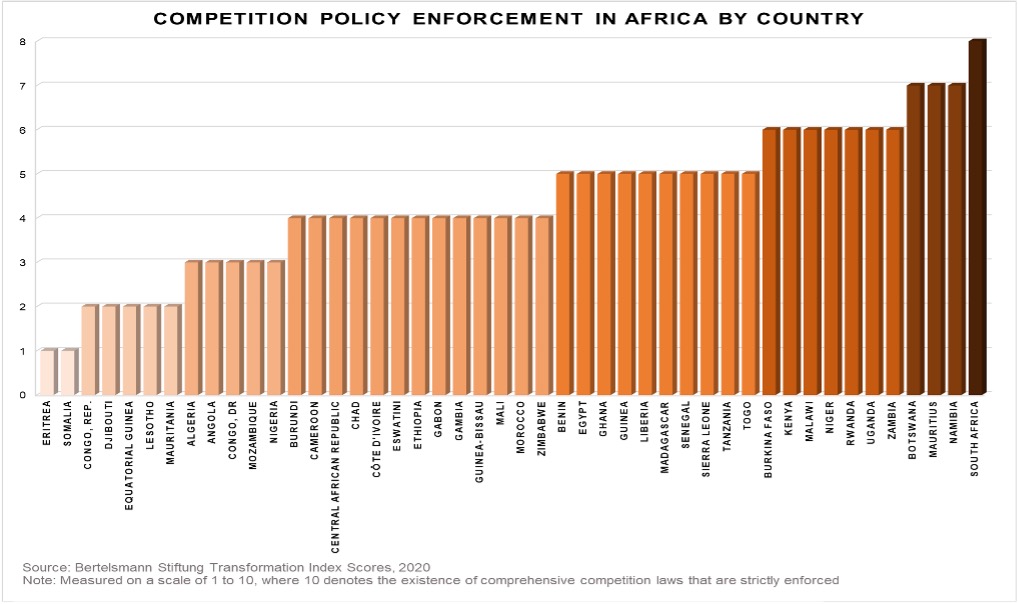

Matrices used to analyse economic transformation, such as the Bertelsmann Transformation Index, have noted the existence of comprehensive competition laws that are enforced (to some degree), in at least 46 African jurisdictions.

This is reflected by the enforcement scores for each of the 46 countries listed in the graph below, measured on a scale of 1 to 10, where 10 denotes the existence of comprehensive competition laws that are strictly enforced.

As indicated, almost half of the jurisdictions received a score of five or higher, demonstrating robust enforcement across much of the continent. Additionally, a review of historical scores indicates a year-on-year increase in respect of a number of African jurisdictions, with countries such as Eswatini, Ethiopia and Namibia each ranking higher than the previous year.

This upward trend in enforcement is highlighted by a number of significant recent developments in competition law regulation around the continent.

On 6 September 2021, the COMESA Competition Commission issued its first penalty for failure to notify a transaction within the prescribed time periods, which amounted to 0,05% of the parties’ combined turnover in the common market in the 2020 financial year. This was imposed in relation to the proposed acquisition by Helios Towers Limited of the shares of Madagascar Towers SA and Malawi Towers Limited.

The authority’s decision to impose a penalty in this matter is a clear shift towards stricter enforcement of merger regulations. This has been observed for some time, with the authority increasingly approaching parties on the basis of publicly available information and requesting further information about transactions to enable it to assess whether the transactions are notifiable.

Until the Helios Towers decision, the authority generally adopted a softer stance in relation to the timing of merger notifications. The decision to penalize the parties is intended to deter future violations of the competition regulations and signal to market participants that the authority will enforce the regulations more vigorously.

In Mozambique, almost seven years after the promulgation of competition legislation, the Competition Regulatory Authority became operational in January 2021. Shortly after that, the authority amended its merger filing fees on 16 August 2021.

Prior to the amendment, there had been significant concern around the exorbitant filing fees of 5% of merging parties’ turnover.

Following the amendment, the applicable filing fee was changed to 0.11% of the turnover in the year before filing, with a maximum limit of MZN 2.25 million. This move highlighted the authority’s willingness to be receptive to changing market and economic conditions and valid concerns surrounding competition policy.

Further, the rapid rise in the digital economy has resulted in some competition authorities acknowledging that the regulation of digital markets necessitates a more nuanced approach. In May 2021, the South African Competition Commission launched a market inquiry into online intermediation platforms, which focuses on digital platforms that intermediate transactions between businesses and consumers. The scope of the inquiry includes e-commerce marketplaces, online classifieds, travel and accommodation aggregators, food delivery and App stores.

The Malawi Competition and Fair Trade Commission submitted itself to a Voluntary Peer Review, through a tool used by the United Nations Conference on Trade and Development, which evaluates the competition law and policy of a country, as well as its institutional arrangements and effectiveness in competition law enforcement. The Review began in October 2020 and was finalised in July 2021.

Following the conclusion of the Review, the UNCTAD issued a report to the Malawian authority, where it made recommendations in respect of (amongst other things): (i) the substantial amendment or repeal of the Competition and Fair Trading Act; (ii) the Commission’s budget; and (iii) the Commission’s approach to dispute resolution and adjudication.

The review process sought to identify areas of improvement in Malawi’s legal and institutional framework in order to enhance the quality and competency of competition law and policy in Malawi. Amendments to the competition law regime in Malawi are anticipated in the coming years.

In a move toward enhancing the efficiency and effectiveness of its enforcement activities, the Competition Authority of Kenya operationalised an Informant Reward Scheme on 1 January 2021. The scheme provides a mechanism and framework for informants to receive financial incentives in exchange for actionable information in the course of the Competition Authority’s investigations. The Scheme is targeted at persons with credible intelligence regarding restrictive trade practices, mainly cartel-like conduct.

An informant who provides intelligence leading to the closure of an investigation through penalization is entitled to up to 1% of the administrative penalty imposed by the Authority, which payment has been capped at KSH 1 million. Globally, similar schemes have been instrumental in uncovering and prosecuting cartel behaviour and bolstering competition law enforcement, generally. The implementation of a scheme in Kenya reflects the competition authority’s increasing appetite to enforce the regime and root out restrictive practices.

These recent developments in competition policy enforcement draw attention to the continent’s collective enthusiasm in ensuring competition compliance, and its determination in promoting and protecting more effective economies.

We anticipate this trend will continue, with more intensive competition policy enforcement becoming predominant across the region. As competition authorities gain traction in the execution of their mandates, businesses transacting in Africa should ensure that they are fully compliant with all competition laws and regulations.

Angelo Tzarevski is Associate Director, and Zareenah Rasool, Candidate Attorney, Competition & Antitrust Practice, Baker McKenzie Johannesburg

By Louis Strydom

Last year, I argued in my piece Lean Carbon, Just Power that a limited and temporary increase in African carbon emissions is justified to meet the continent’s urgent electrification needs.

That position was not a retreat from climate ambition. It laid out a credible lean-carbon pathway that reconciles power systems development realities with climate arithmetic.

The central question remains: not whether emissions must fall, but how much temporary headroom is tolerable to accelerate energy prosperity for a continent responsible for roughly 4% of global CO2.

The flexibility equation

The future of Africa’s electrification is neither “all renewables tomorrow” nor “gas indefinitely”. Intermittent renewables alone cannot power the continent’s fragile grids at scale. Solar and wind require highly dispatchable power capacity to ensure the reliability of the system.

The real choice is not between renewables and fossil fuels in the abstract; it is between flexible firm power that complements solar and wind, and the de facto alternative: the increasing reliance on high-emissions diesel backup and widespread grid instability.

I argue that a realistic transition strategy must embrace “a capped carbon overdraft”: a strictly bounded, time-limited deployment of flexible power plants running on gas that supports the deployment of renewables and declines according to a binding schedule. This strategy means accepting minimal, temporary emissions to allow for a faster, cleaner and more resilient clean transition.

The response to this argument drew serious scrutiny. Three objections deserve a direct answer.

First: Does the case for flexible thermal power hold on a full life cycle basis?

It does. Our power system studies in Nigeria, Mozambique, and Southern Africa consistently reach the same conclusion – the least-cost long-term system is renewables-led, with flexible engines balancing variability. That holds across capital, fuel, maintenance, carbon pricing, and decommissioning. South Africa’s Integrated Resource Plan 2025, approved in October, makes the point concretely: it projects 105 GW of new capacity by 2039 with renewables as backbone, yet includes 6 GW of gas-to-power by 2030 explicitly for grid stability. Even the continent’s most industrialised economy concludes it needs dispatchable thermal capacity to underpin a renewables-heavy system. The question is not whether firm power is needed, but how to make it as clean and flexible as possible.

Second: Does this argument talk over Africa’s ambition to leapfrog fossil fuels?

No. It is designed around that ambition. Wärtsilä launched the world’s first large-scale 100% hydrogen-ready engine power plant concept in 2024, certified by TÜV SÜD, with orders opening in 2025. Ammonia engine tests now demonstrate up to 90% greenhouse gas reductions versus diesel. These are not roadmaps. They are ready-to-use technologies. The honest difficulty is timing. Sub-Saharan grids averaged 56 hours of monthly outages in 2024. The African diesel generator market is growing at nearly 7% a year, projected to reach 1.3 billion dollars by 2030. Nigerian businesses spend up to 40% of operational costs on fuel for backup power. That is the real counterfactual – not a continent neatly powered by sun and wind, but a billion-dollar diesel habit deepening every year the grid stays unreliable. Even Germany is tendering 10 GW of hydrogen-ready gas plants with mandated conversion by 2035 to 2040. If Europe’s largest economy needs transitional thermal flexibility to backstop an 80% renewables target, insisting low-income African nations skip that step is not climate leadership. It is development deferred.

Third: Does the carbon comparison include full life cycle methane?

It must. Methane leakage materially worsens the climate profile of gas-to-power because methane is a far more potent greenhouse gas than CO₂. If leakage exceeds a few per cent of production, gas loses its advantage over coal on a 20-year timeframe.

But the IEA notes that 40% of fossil methane emissions could be eliminated at no net cost with existing technology. My claim that gas has a lower footprint than coal is conditional on aggressive methane management – eliminating flaring and venting, enforcing measurement under frameworks like the EU Methane Regulation and OGMP 2.0. Without those conditions, the arithmetic fails. But the real choice in most African markets is not between pristine gas and pristine renewables. It is between ageing coal, a growing fleet of unregulated diesel generators, and new fuel-flexible plants that start or transition to gas and convert to hydrogen or ammonia on a contractual schedule. Displacing diesel and coal with well-managed gas in future-fuel-ready engines cuts CO₂, local pollution, and water use now, while building the infrastructure for fuels that eliminate fossil dependence.

The critics are right to demand rigour, full life cycle accounting, methane transparency, and credible timelines. Those are exactly the conditions that make a lean-carbon pathway work. Africa does not seek permission to pollute. It seeks the tools to end energy poverty while peaking emissions early and declining fast. Build engine power plants that run on available fuel today. Mandate their conversion tomorrow. The carbon overdraft stays small. The payback stays fast. And the technology to switch to sustainable fuels is already here.

Louis Strydom is the Director of Growth and Development for Africa and Europe at Wärtsilä Energy

You’re back home after mudik (homecoming), the suitcases are unpacked, and the excitement of being with family for Eid already feels like a long time ago. But just because Eid is over doesn’t mean the special connection of being with family has to fade. Here are the best group chat features for beating the post-Raya blues.

-

Keep The Vibe Going by Sharing Ramadan Highlights

-

Keep the Memories Rolling with Status: Your Status feed doesn’t have to go quiet just because you’re back home. Post the most memorable throwback photos from the Eid reunion and add questions to spark responses like “What was your favourite Raya dish?” Add music and stickers to Status to keep the energy alive.

-

Express Yourself with Text Stickers: Turn inside jokes, family slogans, or a favourite Eid quote into a Text Sticker. It’s a quick, personalised way to add some warmth and humour to the group chat.

-

Skip the Stock Cards, Use Meta AI for a Personal Touch: Don’t just send a generic “Hi” or “Good morning” in the family chat. Use Meta AI to make your personalised greeting card or quickly transform a single photo into an animated image to send a heartfelt, animated check-in.

-

Schedule The Next Reunion

-

Plan Your Next Post-Raya Get-Together: The blues often hit when the fun ends. Keep spirits up by creating a new Event in the group chat right away. Add event reminders so everyone doesn’t miss the opportunity to connect.

-

Schedule a Call, Don’t Just Say “Call Me”: Carry on the family tradition of staying connected, even when you’re miles apart. Tap + then Schedule a call in the Calls tab to lock in a regular “Post-Raya Check-in” video call. Send a reminder so everyone can join on time.

-

Keep the Raya Spirit Alive by Getting Everyone Involved

-

Assign yourself a fun “tag” in the family group: Are you the one who always ends up cooking? Or the one who plans the itinerary for family trips? Or the master of GIFs who keeps everyone amused? Use the Member Tag feature in the group to give yourself a witty, funny, or practical role—”Next Event Planner” or “Tech Support Guru,” maybe?. Member tags can be customised for each group you’re in.

-

Share a Spontaneous ‘I Miss You’ Video: Did you just see something that reminded you of the reunion? Press and hold the camera icon to record a spontaneous Video Notes message. It’s faster than typing and instantly brings warmth and real-time emotion back into the group.

-

Digital Hugs: Making the Long-Distance Moment Count

-

Share a Moving Memory: Don’t just send a still photo. Share a Live or Motion Photo to capture the ambient sound and movement of a recent Eid moment. It makes your memories feel more vivid, personal, and real—a perfect antidote to feeling disconnected.

-

Your Group Chat Background: Create a vibe with Meta AI: Don’t settle for a plain background for your family group chat. Use Meta AI to generate unique, custom chat wallpapers that reflect something uniquely memorable to your family: be it food, travel or a sport that unites everyone. Every time you open the chat, you’ll feel the warmth, not the distance.

-

Make Sure No One Misses Out

No More FOMO: Send the Conversation History: Just added a family member who couldn’t make it to mudik? When adding a new member, you can now send up to 100 recent messages with the Group Message History feature. No need to recap; let them catch up instantly and feel included from the first tap.

By Olumide Balogun

Nigerians are natural explorers. Whether finding the best supplier in Balogun market, hunting down a recipe for party jollof, or looking for the most affordable flight out of Lagos, we are always searching.

Today, human curiosity is expanding, and the way Nigerians express it is evolving. We are speaking to our phones, snapping photos of things we like, and asking incredibly complex questions. For the Nigerian business owner, understanding this shift is a massive opportunity to get discovered by eager customers.

Here are four ways AI is rewriting how Nigerians search, along with simple steps to ensure your business is exactly what they find.

1. Visual Discovery is the New Normal

People are increasingly using their cameras to discover the world around them. Picture someone spotting a brilliant pair of sneakers in traffic and wanting to know exactly where to buy them. Today, shoppers simply take out their phones and search visually.

Tools like Google Lens now process over 25 billion visual searches every single month, and many of these searches are from people looking to make a purchase.

How to adapt: Your product’s visual appeal is paramount. Make sure you upload clear, high-quality images of your products to your website and social media. When a customer snaps a picture of a bag that looks like the one you sell, having great photos ensures your business pops up in their visual search results.

2. Conversations Replace Simple Keywords

Shoppers are asking highly nuanced, conversational questions. They are typing queries like, “Where can I find affordable leather shoes in Ikeja that are open on Sundays and do home delivery?”

To handle these detailed questions, new features like AI Overviews act like a superfast librarian that has read everything on the web. It provides users with a perfectly organised summary and links to dig deeper.

How to adapt: Answer your customers’ questions before they even ask. Create detailed, helpful content on your website and fully update your Google Business Profile. List your opening hours, delivery areas, and unique services clearly. This ensures the technology easily finds your details and recommends your business when a customer asks a highly specific question.

3. Intent Matters More Than Exact Words

Predicting every single word a customer might use to find your product is a huge task for any business owner. Thankfully, modern search technology focuses on the underlying need behind a search.

If someone searches for “how to bring small dogs on flights,” AI understands that the person likely needs to buy an airline-approved pet carrier. The technology looks at the true intent of the shopper.

How to adapt: You no longer need to obsess over guessing exact keywords. By using AI-powered campaigns, you allow the technology to understand your products and match them to the customer’s true needs. Your business will show up for highly relevant searches, bringing you customers who are actively looking for solutions you provide.

4. Smart Assistants Handle the Heavy Lifting

Running a business in Nigeria requires incredible hustle. Managing digital marketing on top of daily operations takes significant time and energy. The next frontier in digital advertising introduces agentic capabilities, which hold a simple promise of delivering better results for your business with much less effort.

The technology now acts as your personalised assistant.

How to adapt: You can simplify your marketing by using the Power Pack of AI-driven campaigns, including Performance Max. You simply provide your business goals, your budget, and your creative assets like photos and videos. The AI automatically finds new, high-value customers across Google Search, YouTube, and the web. It adapts your ads in real time to match exactly what the shopper is looking for, allowing you to focus on running your business.

The language of curiosity is constantly expanding. Nigerians are discovering brands in entirely new ways using cameras, voice notes, and highly specific questions. By understanding these behaviours and embracing helpful AI tools, you can let the technology connect eager customers directly to your digital doorstep.

Olumide Balogun is a Director at Google West Africa

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn