Feature/OPED

Listicle: Five Stress-Busting Hacks for Busy Executives

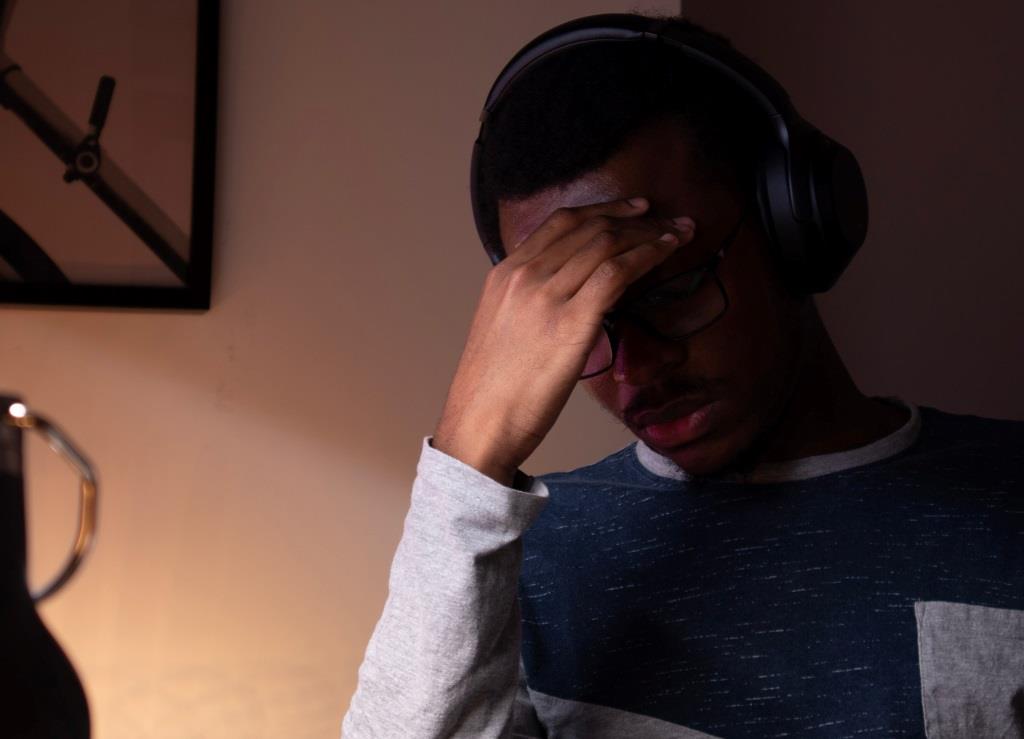

We’re all seeing first-hand how businesses have been hard hit by the COVID-19 pandemic. Downsizing, budget cuts, long working hours and increased competition are just some of the issues that companies are now facing.

Employees who are grateful to still have their jobs are working extra hard to navigate in between the intense demand — and this can be stressful.

The adoption of remote working models has also increased stress levels for some. Many of us are now participating in more meetings (often back-to-back) and engaging with emails more than ever before — well before and after working hours. Working remotely can be incredibly demanding on executives as it blurs the boundaries between work and home life.

Services like SweepSouth Connect, an innovative on-demand platform, afford busy executives the flexibility of booking a pre-vetted household or outdoor service professional at any time. This offers convenience as routine household tasks can be delegated with a sense of trust. This way, time is saved and stress is reduced as items are checked off the to-do list.

Besides getting an extra set of hands, there are other things that busy executives can do to ease the side effects of stress. Here are five of them.

Exercise regularly: Exercise helps reduce stress hormones and makes the body stronger physically. It also helps build immunity against diseases and improves the quality of sleep. For most busy executives, the goal will be to plan to exercise regularly at least three times a week. Vigorous workouts, jogging or just a stroll can help as muscular relaxations that help deal with anxiety and depression.

Take breaks: Taking breaks can actually boost your performance at work. Getting up from your desk and walking around to clear your head, going outside for a few minutes to get some fresh air, and observing micro-breaks while working have a positive effect on your level of productivity. It might not be a long holiday but it can help decrease exhaustion momentarily.

Eat healthy: Many are stress-eating and gaining weight during the pandemic. An unpredictable lifestyle is synonymous with a busy executive and this in turn affects eating habits. Ensure that meals are balanced, do not eat too late in the evening, watch your portion size, and make sure that you become a fan of fruits and vegetables. Try not to skip breakfast, avoid or limit caffeine, and make sure that alcohol intake is moderated.

Get better organised: It is always great to plan your day the night before. Also, having a mental note of what to do might not be enough to navigate through the day. For a busy executive, a to-do list helps in prioritising urgent and important tasks — this can be done with old-fashioned pen and paper or through an app. Plan for what you can only allocate your time to rather than overbooking yourself. Being proactive by anticipating possible inadequacies on the job also helps in reducing stress levels.

Get enough sleep: Work stress can make it difficult to sleep and even cause insomnia. A regular sleeping routine helps reduce stress. Sleep deprivation can cause tiredness, lack of creativity and can be detrimental to work performance. Consider sticking to an early bedtime and reading a book or meditating before sleeping. Making the room more conducive for sleeping and eating long before bedtime are solutions for achieving a good sleep that reduces stress levels.

The result of stress on the lives of executives can lead to an array of health problems, low energy, demotivation and a lack of inspiration. Busy executives will need to get better at managing their time and lives in order to plan to complete more in a shorter amount of time even as they reduce stress.

Feature/OPED

Refining Without Relief: How Global Oil Wars, Market Structure, and Monopoly Risks Still Drive Fuel Prices in Nigeria

By Blaise Udunze

The vision was bold. The expectation was clear. And the promise was powerful. When the Dangote Refinery began operations, it was hailed as Nigeria’s long-awaited escape from decades of energy contradiction, which involves exporting crude oil while importing refined fuel at high costs. It was meant to guarantee supply, stabilise prices, conserve foreign exchange, and most importantly, deliver relief to ordinary Nigerians.

What appears to be a distinct contradiction is that, despite months into its operation, a different reality is emerging, with fuel prices rising sharply. Inflationary pressures are intensifying. This occurrence has forced Nigerians to ask a difficult question once again, one that calls for an urgent answer. Why does a country that produces and refines crude oil still suffer the consequences of global oil shocks?

Looking at the trend, it is clear that the answer lies not just in geopolitics, but in the deeper structure of Nigeria’s oil economy, where global pricing, policy gaps, and now the looming risk of monopoly intersect.

With the recent development, the latest alarming surge in petrol prices has been driven largely by escalating tensions in the Middle East. This is particularly the U.S-Israel strikes on Iran and retaliatory measures from Tehran. A well-known fact is that at the centre of the crisis is the Strait of Hormuz, a vital oil transit route through which a significant portion of global supply flows. Any disruption, even a speculative one, triggers immediate spikes in crude prices.

Within a week, oil prices jumped from the mid-$60 range to nearly $120 per barrel. For global markets, this is expected. For Nigeria, it is devastatingly ironic. Because, despite having crude oil in abundance and despite refining it locally, Nigeria remains fully exposed, and this has continued to re-echo the same ironic question.

In a rare moment of corporate candour, the refinery’s leadership acknowledged this reality. The plant is deeply affected by global shocks. Crude oil, even when sourced locally, is priced at international benchmarks. Shipping costs have surged dramatically, from about $800,000 per tanker to as high as $3.5 million. Insurance premiums have climbed, and logistics have become significantly more expensive, with total costs further driving higher.

Even more revealing is the refinery’s sourcing structure. Only about 30 per cent – 35 per cent of crude comes from the Nigerian government supply under the crude-for-naira framework. A significant portion is still purchased in U.S. dollars on the open market, while another 30 per cent – 40 per cent is sourced internationally, including from the United States and other regions. This means the refinery is not insulated; it is integrated into the global oil system. The implication is unavoidable as local refining has not translated into local pricing control.

The impact on Nigerians has been immediate and severe, as petrol prices have surged from under N800 earlier in the year to over N1,200, and in some regions, it is even more alarming when the prices skyrocketed close to N1,400 per litre. Within weeks, multiple price increases have been recorded, driven largely by global crude price spikes and rising logistics costs. Doubtless, the country has witnessed the consequences ripple across the economy as transport fares rise, food prices increase, businesses struggle with higher operating costs, and inflation accelerates.

The development has attracted the attention of the labour unions and the organised private sector, prompting them to raise concerns and alarm about the consequences of job losses, business closures, and worsening hardship if the trend continues with each passing day, witnessing a daily increase and causing possible artificial scarcity.

Nigeria remains trapped in a painful contradiction. It produces crude oil. It refines crude oil. Yet it cannot protect its citizens from global oil volatility. As Aliko Dangote himself acknowledged, Nigeria has no direct role in the conflict driving these price increases, yet it bears the consequences due to global economic interdependence.

In a real sense, this is the deeper tragedy, as Nigeria has achieved capacity without control.

At the heart of the issue is a structural reality: crude oil is priced globally, not locally. Even under the crude-for-naira arrangement, pricing is benchmarked against international rates. This means refineries pay global crude prices, fuel prices reflect global market conditions, and domestic consumers absorb international shocks. In essence, Nigeria has moved refining home without bringing pricing sovereignty with it.

To be fair, the Dangote Refinery has played a stabilising role. Nigeria still enjoys relatively lower petrol prices compared to many global markets. In several countries, supply disruptions have led to panic buying and rationing, while Nigeria has maintained a consistent supply. As the refinery’s CEO aptly noted, what is worse than $120 oil is no oil. The refinery has prevented scarcity, but it has not prevented high prices. Availability, in this case, has not equated to affordability, which is the painful part for the citizens.

While much of the current debate focuses on pricing, another critical issue is quietly taking shape, which is the risk of market concentration. Dangote Refinery deserves credit for its scale and ambition, but scale brings power, and power demands oversight. If fuel importers are gradually pushed out and no competing refineries emerge at scale, Nigeria could find itself transitioning from a public sector monopoly to a private sector dominance led by a single player.

Nigeria has seen this pattern before. In the cement industry, increased domestic production did not necessarily translate into lower prices. Limited competition allowed prices to remain elevated despite local capacity. The same risk now looms in the downstream oil sector. Without competition, price-setting power becomes concentrated, supply risks increase, and consumer protection weakens. In a country with fragile regulatory institutions, this is not a theoretical concern; it is a real and present danger.

No one should perceive this wrongly, because it is important, however, not to misplace blame. It should be made known that the Dangote Refinery is not a charity; it is a private enterprise operating within market realities. It must recover its investment, manage costs, and deliver returns. Its exposure to global pricing is not a failure of intent but a function of the system within which it operates.

The real issue lies in the structure of the market and the absence of sufficient competition.

It is no longer news that Nigeria’s downstream sector is now largely deregulated following the removal of fuel subsidies. While deregulation has reduced government fiscal burden and encouraged private investment, it has also exposed consumers to price volatility and limited the scope for intervention, as this has continued to cause pain. Markets, in theory, deliver efficiency, but in practice, they require competition and effective regulation to function properly. Without these, deregulation can simply replace one form of inefficiency with another.

Nigeria does not need to weaken Dangote Refinery; it needs to multiply it. The goal should be to build a competitive refining ecosystem to replace one dominant structure with another. The truth is not far from this, as part of a lasting solution, it requires encouraging new refinery investments, removing bottlenecks for players such as BUA and modular refineries, ensuring transparent crude allocation, providing open access to pipelines and storage infrastructure, and enforcing strong antitrust regulations.

Competition remains the most effective regulator of price, which is sacrosanct, and it protects consumers, strengthens supply security, and reduces systemic risk.

This must also be perceived beyond competition, which calls for the government to act strategically. The fact is that when supplying crude to local refineries at discounted or stabilised rates, expanding naira-based transactions, and introducing temporary relief measures during global crises are all viable options that must be put into consideration. Energy is too critical to be left entirely to market forces, especially in a developing economy where millions are highly vulnerable to economic shocks.

It is time that Nigerians understood that the nation’s refining crisis has been decades in the making, and it cannot be solved by a single refinery, no matter how large. If asked, it will be said that this is a fact that can’t be argued. The Dangote Refinery is undoubtedly a turning point, but it will only remain so if it is embedded within broader systemic reform. Otherwise, Nigeria risks replacing one form of dependency with another, from import dependence to domestic concentration.

The question is no longer whether Nigeria can refine crude oil. It can. The real question is whether Nigeria can build a system that ensures fair pricing, competitive markets, consumer protection, and economic resilience, as these are exactly the core answers.

If global conflicts continue to dictate local fuel prices, if monopoly risks go unchecked, and if citizens remain vulnerable despite abundant resources, then the promise of local refining will remain unfulfilled, as it will bring no expected relief.

What is playing out is the well-known fact that in refining, as in democracy, concentration of power is dangerous. And in both, the strongest safeguard remains the same: competition, transparency, and institutions that serve the public interest.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com

By Louis Strydom

Last year, I argued in my piece Lean Carbon, Just Power that a limited and temporary increase in African carbon emissions is justified to meet the continent’s urgent electrification needs.

That position was not a retreat from climate ambition. It laid out a credible lean-carbon pathway that reconciles power systems development realities with climate arithmetic.

The central question remains: not whether emissions must fall, but how much temporary headroom is tolerable to accelerate energy prosperity for a continent responsible for roughly 4% of global CO2.

The flexibility equation

The future of Africa’s electrification is neither “all renewables tomorrow” nor “gas indefinitely”. Intermittent renewables alone cannot power the continent’s fragile grids at scale. Solar and wind require highly dispatchable power capacity to ensure the reliability of the system.

The real choice is not between renewables and fossil fuels in the abstract; it is between flexible firm power that complements solar and wind, and the de facto alternative: the increasing reliance on high-emissions diesel backup and widespread grid instability.

I argue that a realistic transition strategy must embrace “a capped carbon overdraft”: a strictly bounded, time-limited deployment of flexible power plants running on gas that supports the deployment of renewables and declines according to a binding schedule. This strategy means accepting minimal, temporary emissions to allow for a faster, cleaner and more resilient clean transition.

The response to this argument drew serious scrutiny. Three objections deserve a direct answer.

First: Does the case for flexible thermal power hold on a full life cycle basis?

It does. Our power system studies in Nigeria, Mozambique, and Southern Africa consistently reach the same conclusion – the least-cost long-term system is renewables-led, with flexible engines balancing variability. That holds across capital, fuel, maintenance, carbon pricing, and decommissioning. South Africa’s Integrated Resource Plan 2025, approved in October, makes the point concretely: it projects 105 GW of new capacity by 2039 with renewables as backbone, yet includes 6 GW of gas-to-power by 2030 explicitly for grid stability. Even the continent’s most industrialised economy concludes it needs dispatchable thermal capacity to underpin a renewables-heavy system. The question is not whether firm power is needed, but how to make it as clean and flexible as possible.

Second: Does this argument talk over Africa’s ambition to leapfrog fossil fuels?

No. It is designed around that ambition. Wärtsilä launched the world’s first large-scale 100% hydrogen-ready engine power plant concept in 2024, certified by TÜV SÜD, with orders opening in 2025. Ammonia engine tests now demonstrate up to 90% greenhouse gas reductions versus diesel. These are not roadmaps. They are ready-to-use technologies. The honest difficulty is timing. Sub-Saharan grids averaged 56 hours of monthly outages in 2024. The African diesel generator market is growing at nearly 7% a year, projected to reach 1.3 billion dollars by 2030. Nigerian businesses spend up to 40% of operational costs on fuel for backup power. That is the real counterfactual – not a continent neatly powered by sun and wind, but a billion-dollar diesel habit deepening every year the grid stays unreliable. Even Germany is tendering 10 GW of hydrogen-ready gas plants with mandated conversion by 2035 to 2040. If Europe’s largest economy needs transitional thermal flexibility to backstop an 80% renewables target, insisting low-income African nations skip that step is not climate leadership. It is development deferred.

Third: Does the carbon comparison include full life cycle methane?

It must. Methane leakage materially worsens the climate profile of gas-to-power because methane is a far more potent greenhouse gas than CO₂. If leakage exceeds a few per cent of production, gas loses its advantage over coal on a 20-year timeframe.

But the IEA notes that 40% of fossil methane emissions could be eliminated at no net cost with existing technology. My claim that gas has a lower footprint than coal is conditional on aggressive methane management – eliminating flaring and venting, enforcing measurement under frameworks like the EU Methane Regulation and OGMP 2.0. Without those conditions, the arithmetic fails. But the real choice in most African markets is not between pristine gas and pristine renewables. It is between ageing coal, a growing fleet of unregulated diesel generators, and new fuel-flexible plants that start or transition to gas and convert to hydrogen or ammonia on a contractual schedule. Displacing diesel and coal with well-managed gas in future-fuel-ready engines cuts CO₂, local pollution, and water use now, while building the infrastructure for fuels that eliminate fossil dependence.

The critics are right to demand rigour, full life cycle accounting, methane transparency, and credible timelines. Those are exactly the conditions that make a lean-carbon pathway work. Africa does not seek permission to pollute. It seeks the tools to end energy poverty while peaking emissions early and declining fast. Build engine power plants that run on available fuel today. Mandate their conversion tomorrow. The carbon overdraft stays small. The payback stays fast. And the technology to switch to sustainable fuels is already here.

Louis Strydom is the Director of Growth and Development for Africa and Europe at Wärtsilä Energy

You’re back home after mudik (homecoming), the suitcases are unpacked, and the excitement of being with family for Eid already feels like a long time ago. But just because Eid is over doesn’t mean the special connection of being with family has to fade. Here are the best group chat features for beating the post-Raya blues.

-

Keep The Vibe Going by Sharing Ramadan Highlights

-

Keep the Memories Rolling with Status: Your Status feed doesn’t have to go quiet just because you’re back home. Post the most memorable throwback photos from the Eid reunion and add questions to spark responses like “What was your favourite Raya dish?” Add music and stickers to Status to keep the energy alive.

-

Express Yourself with Text Stickers: Turn inside jokes, family slogans, or a favourite Eid quote into a Text Sticker. It’s a quick, personalised way to add some warmth and humour to the group chat.

-

Skip the Stock Cards, Use Meta AI for a Personal Touch: Don’t just send a generic “Hi” or “Good morning” in the family chat. Use Meta AI to make your personalised greeting card or quickly transform a single photo into an animated image to send a heartfelt, animated check-in.

-

Schedule The Next Reunion

-

Plan Your Next Post-Raya Get-Together: The blues often hit when the fun ends. Keep spirits up by creating a new Event in the group chat right away. Add event reminders so everyone doesn’t miss the opportunity to connect.

-

Schedule a Call, Don’t Just Say “Call Me”: Carry on the family tradition of staying connected, even when you’re miles apart. Tap + then Schedule a call in the Calls tab to lock in a regular “Post-Raya Check-in” video call. Send a reminder so everyone can join on time.

-

Keep the Raya Spirit Alive by Getting Everyone Involved

-

Assign yourself a fun “tag” in the family group: Are you the one who always ends up cooking? Or the one who plans the itinerary for family trips? Or the master of GIFs who keeps everyone amused? Use the Member Tag feature in the group to give yourself a witty, funny, or practical role—”Next Event Planner” or “Tech Support Guru,” maybe?. Member tags can be customised for each group you’re in.

-

Share a Spontaneous ‘I Miss You’ Video: Did you just see something that reminded you of the reunion? Press and hold the camera icon to record a spontaneous Video Notes message. It’s faster than typing and instantly brings warmth and real-time emotion back into the group.

-

Digital Hugs: Making the Long-Distance Moment Count

-

Share a Moving Memory: Don’t just send a still photo. Share a Live or Motion Photo to capture the ambient sound and movement of a recent Eid moment. It makes your memories feel more vivid, personal, and real—a perfect antidote to feeling disconnected.

-

Your Group Chat Background: Create a vibe with Meta AI: Don’t settle for a plain background for your family group chat. Use Meta AI to generate unique, custom chat wallpapers that reflect something uniquely memorable to your family: be it food, travel or a sport that unites everyone. Every time you open the chat, you’ll feel the warmth, not the distance.

-

Make Sure No One Misses Out

No More FOMO: Send the Conversation History: Just added a family member who couldn’t make it to mudik? When adding a new member, you can now send up to 100 recent messages with the Group Message History feature. No need to recap; let them catch up instantly and feel included from the first tap.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn