General

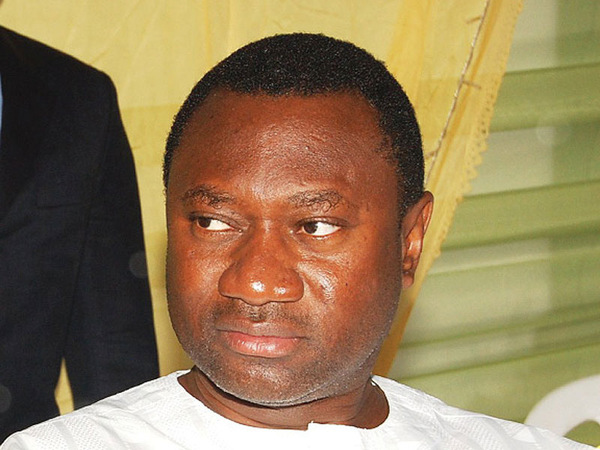

Day I Lost Everything—Femi Otedola Reveals

By Dipo Olowookere

Life was rosy for Femi Otedola until it took a sudden turn leaving him billions in the red. He had to start all over again.

The article below tells his story and it first appeared in Forbes Africa and was reproduced by CNBC Africa.

In 2008, a shipment containing one million tons of diesel set sail, heading for the shores of Nigeria. The owner of the vessel, Mr Femi Otedola, Chairman of Forte Oil, a petroleum and power generation company, had grown the company to one of the largest in Nigeria, with over 500 gas stations, according to Forbes. The growth had been rapid and profits were at an all-time high. Then disaster struck.

“I had about 93 percent of the diesel market on my fingertips. All of a sudden oil prices collapsed and I had over one million tons of diesel on the high seas and the price dropped from $146 to $34,” says Otedola.

That was only the beginning of his problems. The naira was subsequently devalued and interest began to skyrocket. When the dust settled, Mr Otedola had lost over $480 million due to the plunge in oil prices, $258 million through the devaluation of the naira, a further $320 million due to accruing interest and then finally $160 million when the stocks crashed.

“I had two options, either to commit suicide or to weather the storm. I decided to weather the storm. I just knew it was a phase I had to go through. You see God prepares you for greater things and of course experience is the best teacher so I had to learn my lessons. I took the bitter pill,” he says.

Mr Otedola was now $1.2 billion in debt. He sought solace in the only thing that had set him on the path to discovering oil, destiny.

“You cannot compete with destiny, so it was my destiny to make billions every month and lose billions as well. I said to myself ‘I was not going to have friends and enemies, I was only going to have competitors.”

At the age of six, Mr Otedola had already discovered his knack for business. He would provide manicure and pedicure services to his father and his friends and write them a receipt for payment. On his birthday, while all his friends wanted toys, Mr Otedola asked his father for a briefcase instead. His father, Mr Michael, as the Governor of Lagos State, was a respected man. Now, his son’s public fall threatened to destroy that name.

“After I lost the money, something that struck me was that my father had always been my role model in life and the first thing I had to do was to protect his name. He had a policy; honesty was the best policy, so I had to protect that name and his integrity.”

Just after the global banking crisis had struck, the Nigerian government established the Asset Management Corporation of Nigeria (AMCON) to buy up distressed loans. Mr Otedola’s loan was sold to AMCON, by the bank he blamed for his demise.

“Experience is the best teacher. I didn’t have a proper structure and I also put the blame on the banks for not advising me. All they were interested in was the profits. They were not interested in sustainability of the business, they were short-sighted and all they were interested in was throwing money at me. So they never advised me,” says Mr Otedola.

The banks had to shave off about $400 million from the debt leaving Mr Otedola $800 million in the red. AMCON offered him a restructuring deal, which Mr Otedola declined. He opted instead to repay what he owed and start all over again.

“So we got a reputable firm to value my assets. I had about 184 flats, which I gave up. I was the largest investor in the Nigerian banking sector, which I gave up, I was also a major shareholder of Africa Finance Corporation and I was the Chairman of Transcorp Hilton. I was a shareholder in Mobil Oil Nigeria Limited, the second largest shareholder in Chevron Texaco, Visafone and several companies which they valued, and I had to give up to repay the debt.”

Mr Otedola was left with two properties, his office space and a 34-percent stake in African Petroleum, which he rebranded, to Forte Oil in 2010.

In 2014, Mr Otedola bounced back to reclaim his place on the FORBES rich list and currently has a net worth of $1.8 billion, according to the FORBES wealth unit in the United States. These days, he is much wiser; there are systems in place to prevent a similar collapse of his mammoth oil empire.

According to the mogul, the day he lost everything was the day he learned his biggest lesson. It taught him that he could overcome anything

http://www.cnbcafrica.com/news/western-africa/2016/11/12/femi-otedola-on-the-day-he-lost-everything/

By Modupe Gbadeyanka

Members of the public have been invited to submit memoranda and policy proposals on the proposed National Policing Bill.

The Chairman of the Working Group, Mr Femi Gbajabiamila, announced this on Monday after the team’s meeting at the State House in Abuja.

The group, headed by the Chief of Staff to President Bola Tinubu, is calling for input from Nigerians as part of efforts to establish a comprehensive legal and operational framework for state policing.

It is reviewing the Police Act 2020, the Police Service Commission framework, police regulations, and other relevant laws to support the development of an effective, modern policing system.

The proposed framework will set national minimum standards, define state readiness and grant certification, clarify jurisdictional responsibilities, ensure independent oversight, uphold human rights, and guarantee sustainable funding. It would also spell out an orderly transition to a dual-policing structure.

The call for memoranda will run for two weeks, allowing citizens, professionals, civil society, security agencies, state and local governments, academics, and other stakeholders to contribute. Submissions will be reviewed and integrated into the draft bill, which will then be subject to further national consultation before being finalised and sent to the National Assembly.

The Working Group has adopted a seven-week work programme running from July 27 to September 14, 2026. The draft Executive Bill is scheduled for presentation to President Bola Ahmed Tinubu on September 3, 2026, with national consultations to follow before the final approval.

The new National Policing Bill will set out requirements for recruitment, training, oversight, funding, and transition arrangements to ensure credible, effective, and accountable policing nationwide.

“A proposed State Police Service must demonstrate that it has credible arrangements for recruitment, vetting, training, pay, pensions, equipment, custody, complaints, discipline, data, firearms control, independent oversight and financial sustainability before it begins policing,” Mr Gbajabiamila said.

The representative of the Nigeria Governors’ Forum and Governor of Ogun State, Dapo Abiodun, who described State Police as a landmark reform, described the initiative as one of the defining reforms of President Tinubu’s administration.

Responding to concerns about federal overreach, he clarified that there is no Federal attempt to control State Police. He added that the proposed legislation is intended to provide an operational framework rather than centralise control.

Prince Lateef Fagbemi, the Attorney-General of the Federation and Minister of Justice, said the proposed National Policing Bill is designed to guarantee the security of lives and property while ensuring that the establishment of state police does not become a tool for political persecution.

The Attorney-General added that states not immediately ready to establish their own police services would continue to benefit from the presence of the Federal Police until they meet the required standards.

Other participants at the meeting included the Inspector General of Police, Tunji Disu; President of the Nigerian Bar Association, Afam Osigwe; Chairman, Policy Advisory Committee, Justice Abdullahi Liman (rtd); Professor Olu Ogunsakin, Head, Nigeria Police Reform Secretariat; Senior Special Assistant to the President on Planning and Research, Nnadubem Moghalu; and Brigadier General Olutayo Muyiwa Adesuyi, representing the National Security Adviser.

By Adedapo Adesanya

The Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) says it recorded a 30 per cent reduction in gas imbalance on the country’s Western Network following the conclusion of its first-half 2026 Nigerian Gas Network Reconciliation (NGNR) Workshop.

The workshop brought together gas transporters, suppliers, shippers and off-takers to reconcile gas volumes traded between January and June 2026, while introducing a Network Entry/Exit Point Measurement Infrastructure Audit Template aimed at improving metering accuracy and accountability across the gas transmission network.

In a communiqué issued after the workshop, the authority said participants also reviewed the performance of the Nigerian Gas Transmission Network, assessed progress on major pipeline infrastructure projects, and received updates on the ELPS Gas Shrinkage Factor and Hydraulic Modelling Project.

Discussions focused on addressing metering gaps, improving network visibility through Supervisory Control and Data Acquisition (SCADA) integration, and enhancing system reliability ahead of the commissioning of the Ajaokuta-Kaduna-Kano (AKK) Pipeline System.

The workshop adopted key resolutions, including the execution of outstanding Network Exit Agreements, mandatory submission of measurement audit templates and closer collaboration among industry stakeholders to improve network pressure management.

Speaking at the closing session on behalf of the authority’s chief executive, Mr Rabiu A. Umar, the Director of Transportation Systems and Networks, Mr Joseph G. Musa, said the biannual reconciliation exercise had become critical to promoting equitable gas transactions, transparency, investor confidence and efficient network operations.

Mr Musa noted that since the NGNR process was introduced in 2023, it had significantly improved gas measurement, strengthened regulatory compliance through consequence management, reduced operational imbalances and contributed to a more reliable domestic gas supply.

The workshop concluded with participants adopting the reconciled H1 2026 gas volumes, reaffirming the authority’s commitment to a transparent, efficient and reliable domestic gas market.

By Modupe Gbadeyanka

An investment that supports growing food and agriculture companies across Africa that strengthen agricultural value chains has been made by Swedfund.

The organisation is putting down about $12 million to strengthen climate resilience in African food systems through the Acumen Resilient Agriculture Fund II (ARAF II).

By improving access to markets, finance and essential services, these companies help smallholder farmers become more resilient to climate and economic shocks.

Over 30 million smallholder farmers operate across Sub-Saharan Africa, accounting for 80 per cent of all farms and producing 70 per cent of the region’s food (IFAD). Yet many face limited access to finance, quality inputs, reliable buyers and market information. At the same time, they are among those most exposed to climate change and weather-related shocks, which threaten harvests, incomes and food security.

The investment has an ambition to reach around four million smallholder farmers through ARAF II’s portfolio companies. It also aims to meet the criteria of the 2X Challenge, which promotes investments that support women’s economic empowerment.

ARAF II invests in businesses that address key gaps in agricultural value chains, from improving market access and reducing post-harvest losses to expanding financial and digital services for farmers. By helping these businesses grow, the investment aims to improve productivity, strengthen local value chains and increase the resilience of food systems.

Swedfund invests alongside other development finance institutions and investors to help mobilise long-term capital for businesses that often struggle to access financing despite their potential to strengthen food security, climate resilience and economic development across Africa.

“Climate change is already affecting the livelihoods of millions of smallholder farmers across Africa. Investing in businesses that improve access to markets, finance and agricultural services helps farmers strengthen their resilience, increase productivity and build more stable incomes. That is essential for more resilient food systems,” the Investment Director of Food Systems and Strategic Investments at Swedfund, Ms Helen Hagos, said.