Media OutReach

DFI Retail Group Holdings Limited 2024 Preliminary Announcement of Results

The following announcement was issued today to a Regulatory Information Service approved by the Financial Conduct Authority in the United Kingdom.

Highlights

- 30% growth in underlying profit to US$201 million

- Health and Beauty delivered a stable performance

- Convenience saw strong profit growth due to favourable product mix

- Food profit improved, driven by significant Singapore Food earnings recovery

- Portfolio simplification progressed further with Yonghui and Hero Supermarket divestments

- Net cash position achieved in February 2025 with completion of Yonghui sale

- Final dividend of US¢7.00 per share

“Effective strategy execution led to strong underlying profit growth in 2024, despite a challenging retail environment. We aim to remain relevant to consumers and to increase market share further, by evolving our offering through leveraging data and expanding our omnichannel presence. We are well-positioned for sustainable growth and increased shareholder returns over the mid-term.”

John Witt

Chairman

PRELIMINARY ANNOUNCEMENT OF RESULTS

FOR THE YEAR ENDED 31 DECEMBER 2024

PERFORMANCE

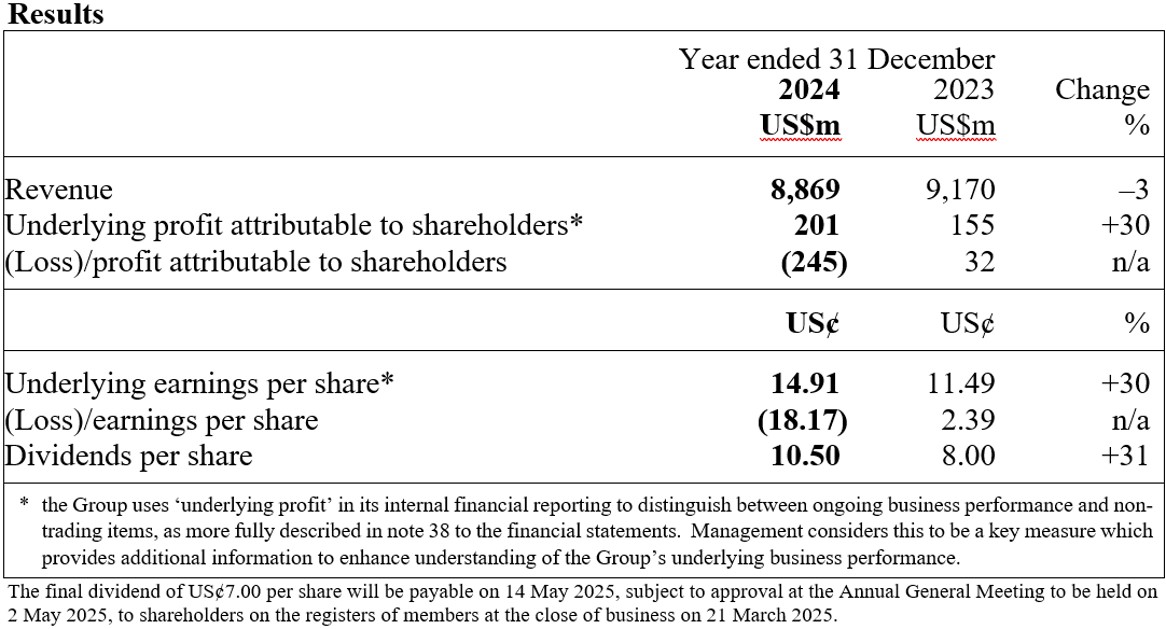

I am pleased to report that DFI Retail Group (‘DFI’ or the Group) delivered a significantly improved underlying performance and a good partial recovery in results in 2024, despite a challenging retail environment. For the full year, underlying profit attributable to shareholders reached US$201 million, a 30% increase from the previous year.

Our diverse portfolio and effective operational execution enabled us to gain market share across key businesses, even as we faced shifts in consumer behaviour and macroeconomic headwinds. Profit growth was driven by improved profit in Food and Convenience, supported by growth in digital channels.

We are confident that the Group’s new strategy will drive further profit growth in the coming years, and are particularly optimistic about the growth prospects for our Health and Beauty business, which represents 55% of the Group’s total operating profit. We also see strong growth opportunities in our Convenience business. Our other businesses continue to face challenges, but we are confident in the ability of DFI’s senior leadership team to navigate short-term uncertainties, evolve the portfolio and invest in strengthening our core businesses to drive long-term growth in shareholder value.

The Board recommends a final dividend for 2024 of US¢7.00 per share (2023 final dividend: US¢5.00).

STRATEGIC HIGHLIGHTS

Under the capable leadership of our Group Chief Executive, Scott Price, we have made significant strides in implementing our strategic framework, which centres around three core pillars:

Customer First

Across our business, we have an ongoing commitment to putting our customers first, and we have made significant progress to better serve them over the past year. The yuu Rewards loyalty programme continues to strengthen, with a substantial increase in members and the addition of a number of further partners. We have also begun harnessing our proprietary customer data to refine our product assortment and revamp our Own Brand and digital strategies. We are driving a more transparent and collaborative approach to our negotiations with suppliers, leading to a better outcome for customers. As well as better serving our customers, these efforts aim to bolster market share growth and enhance margins across our businesses.

People Led

We have refined our organisation structure over the past year. Our new senior leadership team, with its deep industry expertise, shares a vision for strategic growth and operational excellence. Key appointments across the business have strengthened our capability to drive these initiatives forward, and we have reduced spans and layers within the organisation to streamline operations and expedite decision-making. Diversity across our business has also improved significantly.

Shareholder Driven

In alignment with our strategic and capital allocation priorities, we continued to simplify the Group’s portfolio and divested our Hero Supermarket business and investment in Yonghui Superstores.

Following the disposal of Hero Supermarket, the Guardian and IKEA businesses will be our focus in Indonesia and we are confident in the long-term prospects for these two businesses to increase market share as the Indonesian market grows. These disposals allow us to reinvest in our subsidiaries’ growth, deleverage our balance sheet and grow total shareholder returns.

Sustainability remains at the top of our agenda, and we are collaborating closely with our stakeholders and setting ambitious targets across the business. There was strong progress in 2024 against the Group’s sustainability strategy in areas including emissions reduction and waste diversion. Our efforts were recognised in improvements in our ESG ratings, including a significant improvement in the Group’s S&P Global Corporate Sustainability Assessment. We will continue to promote and drive sustainable business practices in our end-to-end value chain.

GOVERNANCE AND PEOPLE

The Board and its Committees, and senior leadership team, together play a key role in delivering against our priorities. The effective execution of our strategy depends on high quality debate around the boardroom table, with strong contributions from all Directors.

There have been a number of significant Board and executive leadership changes since the start of 2024:

– In July, I succeeded Ben Keswick as Chairman. On behalf of the Board, I would like to express our gratitude to Ben for his 11 years of service as Chairman.

– I also wish to thank Adam Keswick for his contribution to the Board and Nominations Committee as he steps down.

– We welcomed Elaine Chang to the Board as an Independent Non-Executive Director and Graham Baker as a Non-Executive Director. Elaine has 30 years of leadership experience across industries such as semiconductors, digital content, e-commerce, cloud computing and artificial intelligence, and her expertise in leveraging technology to drive growth will greatly benefit the Group.

– Christian Nothhaft was appointed as a member of the Remuneration and Nominations Committees.

– Tom van der Lee took over as Group Chief Financial Officer from Clem Constantine. We thank Clem for his significant contribution, especially during the pandemic and in strengthening the Group’s financial position. Tom, who joined DFI in 2016, brings a wealth of experience from his various senior financial roles within the organisation.

– Sean Ward succeeded Jonathan Lloyd as our Company Secretary in December 2024. I want to thank Jonathan for his years of valued service.

PROSPECTS

We are pleased by the Group’s strong underlying profit growth in 2024, despite a challenging retail backdrop, providing encouraging early support for our new strategy. We aim to consolidate our position in markets such as Hong Kong where we have strong businesses, while at the same time aiming to achieve long-term growth as we expand key businesses such as Health and Beauty and Convenience.

By evolving our offerings through data-driven insights and expanding our omnichannel presence, we will remain relevant to consumers and continue capturing market share. Our deleveraged balance sheet and strategic initiatives position us well for sustainable growth and increased shareholder returns in the years to come.

I should like to express my appreciation to our shareholders, our valued partners and to the wider community for your continued support. Most of all, thanks must go to our team members, who are key to our success, for their exceptional work and unwavering commitment throughout the past year, despite challenging market conditions.

John Witt

Chairman

GROUP CHIEF EXECUTIVE’S REVIEW

INTRODUCTION

As I reflect on my first full year as DFI’s Group Chief Executive, I am incredibly proud of the significant progress we have made executing in alignment to our strategic framework: Customer First, People Led, Shareholder Driven.

Despite the challenging macroeconomic backdrop, we demonstrated resilience in our business performance, reporting underlying profit attributable to shareholders of US$201 million in 2024, up 30% year-on-year. During the year, we announced the divestment of our minority stake in Yonghui, a transaction that aligns with our strategic and capital allocation framework and enables us to reinvest in the future growth of our subsidiary businesses. While our reported results were impacted by one-off items, including fair value loss, impairment of equity interest and goodwill, we have continued to significantly deleverage our balance sheet with a net cash position following the completion of the Yonghui transaction in February 2025.

As we head into the new financial year, we remain laser focused on executing our strategic priorities to drive revenue growth and enhance profitability. Our 2025 financial guidance of US$230 million to US$270 million underlying profit attributable to shareholders, reflects our confidence in further building on our momentum and delivering greater value for our stakeholders.

STRATEGIC FRAMEWORK – KEY PROGRESS

We developed our strategic framework of Customer First, People Led, Shareholder Driven in the second half of 2023 to guide the Group’s capital allocation priorities and growth plans over the coming years. I am both pleased and proud of the progress made by the team over the past 12 months in executing on this framework.

Customer First

I continue to see value unlock across our uniquely diverse businesses across Asia. We are proud to serve millions of customers in various formats and banners with nearly 11,000 outlets across 13 markets in Asia. What stands out is our ongoing commitment to putting our customers first and serving with passion and care. Our purpose has always been part of who we are. During the year, we launched our DFI purpose to articulate it in a way that unites our organisation, which is to Sustainably Serve Asia for Generations with Everyday Moments. This statement underscores our commitment to meeting the everyday needs of our customers across Asia, while emphasising their interests in sustainable solutions.

Aligned with our purpose, we have made significant progress in a number of areas to better serve our customers over the past year.

yuu Rewards

Our yuu Rewards coalition loyalty programme continues to strengthen. In our home market of Hong Kong, total members have reached 5.3 million with over 3 million monthly active members. The active use of purchases across all our formats, restaurants and partners creates substantial volume of unique data insights. In 2024, the yuu Rewards programme in Hong Kong added a number of additional partners including Starbucks and FWD Insurance. Our members have engaged across a variety of redemption offers that incorporate new travel, entertainment and dining options, driving enhanced customer engagement.

In Singapore, the yuu Rewards programme has grown to over 1.8 million members. A number of new partners joined the programme during the year including Suntec City and Singapore Airlines.

Improving assortment

We are now leveraging our broad yuu Rewards customer data to improve assortment in our stores. At Wellcome, we have leveraged our proprietary data and cutting-edge data analytics capabilities to execute a reset of 14 categories in stores. The improved assortment has seen very encouraging initial results with uplifts in both sales and gross profits. We are now also leveraging the learnings from Wellcome to support assortment optimisation for our Health and Beauty and Convenience businesses across Hong Kong and Singapore.

Improving supplier collaboration

We are beginning to better leverage our data to support enhanced supplier collaboration. By creating a more transparent and collaborative approach to negotiations with suppliers, we are working together to drive market growth and a better outcome for customers.

Own Brand

We have reset our Own Brand strategy to better align with customer needs while delivering stronger margins for our business. By optimising our product range, redesigning packaging for greater customer appeal and maximising cross-selling opportunities across our formats, we have made meaningful improvements in margin and sales productivity, which includes a more than 300bps increase in our Food Own Brand margin and close to a 40% increase in sales productivity compared to 2023. Following the success of our reset of the Own Brand portfolio across our Food business, we have integrated the Health and Beauty Own Brand assortment into this center of excellence to replicate the same success in Health and Beauty as we reset its private label strategy.

Digital

Following our digital strategy reset in September 2023, customers are now able to access our retail portfolio through a wider range of digital assets including apps, websites and third-party platforms. Our expanded omnichannel presence includes Wellcome’s quick-commerce partnership with foodpanda, a new 7-Eleven app with approximately 137,000 monthly active users and 30,000 daily active users in Hong Kong as of December 2024. Including a new Mannings Hong Kong app and Guardian Singapore app, we have launched more than 20 new channels in 2024 across apps, websites and third-party platforms. Our strengthened digital proposition was underpinned by a 31% growth in e-commerce order volume with strong profitability turnaround.

Retail Media

DFI launched our own Retail Media network in the first quarter of 2024. Initial performance has been encouraging, with more than 100 targeted marketing campaigns sold in less than a year since the launch, supported by strong sales acceleration in the second half. We have partnered with leading suppliers such as Procter & Gamble, Unilever, Coca-Cola, Nestlé and Reckitt. Importantly, the integrated online and offline advertising proposition for Retail Media has supported the improved Return on Ad Spend for our supplier partners. We are in the early days of a potentially significant source of profit to invest in the business.

People Led

In alignment with our strategic framework, we refined our organisation structure in the second half of 2023 by moving accountability to a format structure, thereby improving agility while reducing overhead costs. Throughout 2024, we have been focused on deeply embedding our values, underpinned by our purpose statement across the Group. We have reduced spans and layers within the organisation to streamline operations and expedite decision making. Diversity representation across formats has been significantly improved to ensure local relevancy of decision-making to customers. We have strengthened our leadership succession planning and development with a meaningfully improved team member engagement score, supported by a new incentive structure for senior management that aligns with shareholder interests, based on total shareholder return and business performance targets.

Shareholder Driven

Our strategic framework has been developed with the primary aim of improving shareholder returns. We have approached capital allocation in a disciplined manner, both from a capex and working capital management perspective. Over the course of the year, we executed the divestment of a number of company-owned properties, which has supported a US$150 million reduction in net debt at the end of 2024.

Concurrently, the Group continues to execute M&A transactions in a manner that is accretive to return on capital and total shareholder return based on a strategic review of our businesses in 2024. In June 2024, the Group completed the divestment of the Hero Supermarket business in Indonesia. Post-completion, DFI’s operations in Indonesia has fully pivoted to the Guardian and IKEA businesses. In September 2024, the Group announced the divestment of its entire stake in Yonghui Superstores Co., Ltd. This transaction was subsequently completed in February 2025. The Group is in a net cash position following the completion of the Yonghui transaction.

2024 PERFORMANCE

The Group reported total revenue from subsidiaries in 2024 of US$8.9 billion, down 3% year-on-year. However, excluding the impact of a significant tobacco tax increase in Hong Kong, the divestment of our Malaysia Food business in 2023 and Hero Supermarket operation in Indonesia, operating revenue was largely stable. This broadly represents market share gains in all formats except IKEA.

Total revenue for the Group, including 100% of associates and joint ventures, was US$24.9 billion, down 6% compared to 2023, largely due to lower sales at Yonghui. Total underlying profit attributable to shareholders was US$201 million for the year, up 30% year-on-year.

The Group reported subsidiaries underlying profit attributable to shareholders of US$158 million for the full year, 42% higher than the prior year. This was driven by significant earnings recovery in Singapore Food and favourable product mix shift towards non-cigarette categories in our Convenience business, partially offset by lower contribution from Home Furnishings as a result of weak property market activity and intensifying competition.

The Group’s share of underlying profit from associates was US$43 million, down 2% year-on-year. Lower contribution from Maxim’s due to weaker mooncake sales and restaurant performance in the Chinese mainland was partially offset by reduced losses from Yonghui and a 15% profit growth at Robinsons Retail.

The Group’s reported results for the year were impacted by non-trading losses attributable to shareholders of US$445 million. This was predominantly due to loss of US$114 million associated with the divestment of Yonghui, a US$231 million impairment of interest in Robinsons Retail and US$133 million goodwill impairment of Macau and Cambodia Food businesses. These losses were partially offset by gains from divestment of Singapore property assets and the Group’s share of one-off gains from the Bank of the Philippine Islands (BPI)-Robinsons Bank merger. Despite the large non-trading losses reported, the Group is now in a net cash position following the completion of Yonghui transaction in February 2025.

The Group reported operating cash flow after lease payments of US$331 million, 21% lower than the prior year, mainly due to unfavourable movement in working capital year-end timing difference, partially offset by underlying operating profit growth. Operating cash flow after lease payments and normal capital expenditure was US$158 million, down 29% year-on-year.

ENVIRONMENTAL, SOCIAL, GOVERNANCE (ESG)

As a leading Asian retailer, we recognise our unique opportunity to promote and drive sustainable business practices in response to the preference of our customers. By positioning our ESG commitment as a core pillar of our Group Strategy, we have made meaningful progress in various initiatives, including emissions reduction and waste diversion. Our efforts are reflected in a significant improvement in the S&P Global Corporate Sustainability Assessment, with our score improving to 49 as at 8 January 2025, placing DFI in the 84th percentile within the Food and Staples Retailing industry, up from the 47th percentile in 2023.

Our strong commitment to ESG is underscored by our target to halve Scope 1 & 2 greenhouse gas (GHG) emissions by 2030 and achieve net-zero by 2050. Throughout 2024, we have made significant investments in upgrading and converting our existing refrigeration systems to more environmentally friendly options. We successfully completed trials of natural gas and ultra-low global warming potential gases as refrigerant alternatives for our food stores. Following a comprehensive analysis of our Scope 3 emissions, we have identified key product categories and realistic decarbonisation opportunities within our supply chain. For example, our Low Carbon Rice Project, launching in Thailand this year, aims to drive decarbonisation by promoting low-carbon farming practices among local farmers, implementing field monitoring and tracking to measure carbon emission reductions. We have made notable progress in improving our waste diversion and are constantly exploring innovative ways to foster a transition towards a local circular economy. Wellcome has partnered with a Hong Kong-based recycling facility to convert trimmed fats into biodiesel for powering essential generators.

While we are still early in the journey, these initiatives collectively demonstrate our efforts and commitment to serving communities sustainable and affordable products, sustaining the planet and sourcing responsibly while meeting the return objectives of our shareholders.

BUSINESS REVIEW

HEALTH AND BEAUTY

Sales for the Health and Beauty division came in slightly higher than the prior year at US$2.5 billion, with like-for-like (LFL) sales remaining broadly stable. Underlying operating profit was US$211 million for the year, slightly below 2023.

Hong Kong reported strong LFL sales performance in the first quarter, which then decelerated in the second and third quarters due to a strong comparable period in 2023 when consumption vouchers were disbursed in April and July 2023. Sales momentum improved in the fourth quarter with Mannings continuing to gain market share. Profit for the year increased 6%, attributable to gross margin improvement and disciplined cost control, despite a 2% decline in full-year LFL sales. Guided by a customer-first proposition, the Pharmacare programme reached a significant milestone since its launch in 2023. In partnership with Bupa, one of Hong Kong’s major medical insurers, the Mannings team further expanded Pharmacare into its network of more than 150,000 members. Leveraging Mannings’ position as the largest pharmacist network, the programme offers free consultations and medication for a range of common illness. The Mannings team continued to enhance in-store experience with the launch of the Health Pod at our International Finance Centre flagship store in Hong Kong. This innovative service offers an AI wellness assessment that measures over 20 metrics, followed by personalised consultations and product recommendations. Initial results have been promising, with customers using the service showing a basket size three times higher than average. In addition, the team also launched a new Mannings app in December to grow its digital footprint. LFL sales of Mannings China declined as the business pivots away from offline stores to online channels which involves the closure of the majority of its offline network.

Guardian in South East Asia reported US$857 million in sales, reflecting a 5% year-on-year increase, driven by growth in basket size across all key markets. Indonesia, in particular, saw a 17% LFL sales growth supported by increased mall traffic and strong execution of promotional campaigns. Strong profit growth was reported across most key markets, underpinned by gross margin expansion and operating leverage. In Singapore, strong commercial execution and a favourable product mix contributed to gross margin expansion, with healthcare products accounting for more than 60% of sales.

CONVENIENCE

Total Convenience sales were US$2.4 billion, representing a decline of 3% year-on-year. LFL sales were 5% behind the prior year, impacted by a decline in lower-margin cigarette volumes following tax increases in Hong Kong at the end of February 2024. Excluding cigarette sales, overall Convenience LFL sales were up 2%, with continued market share gain across markets. Convenience underlying operating profit was US$102 million for the year, an increase of 17% compared to 2023. Hong Kong operating profit has grown 10% year-on-year, driven by a favourable mix shift towards higher-margin categories, with ready-to-eat (RTE) accounting for 16% of total sales for the full year. The newly launched 7-Eleven app offers discounted RTE bundles, pre-order functions, and digital stamps for IP collectibles to drive purchase frequency and customer loyalty.

7-Eleven South China and Singapore reported largely stable LFL sales supported by robust growth in RTE, which accounted for 40% and 23% of sales, respectively. Favourable margin impact from product mix shift and ongoing cost control contributed to meaningful profit growth in both markets. 7-Eleven continued to grow its store network in the South China region with 103 net openings during the year. The Group aims to drive further network expansion primarily through a capex-light franchise model.

FOOD

Reported sales for the Food division in 2024 were US$3.1 billion, down 5% year-on-year. Excluding the impact of the divestment of the Malaysia Food business in 2023 and Hero Supermarket operation in Indonesia, revenue for the division was 2% lower than the prior year. Underlying operating profit for the division was US$58 million for the year, up from US$45 million in 2023.

While increased outbound travel of Hong Kong residents to the Chinese mainland has affected food consumption for the majority of 2024, the situation has begun to normalise with total retail sales of supermarkets in Hong Kong returning to growth in the fourth quarter of 2024. Wellcome saw improving sales momentum in the fourth quarter with full-year LFL sales marginally below those of the prior year despite challenging trading conditions. Strong in-store execution and effective promotional campaigns have supported consistent market share gain over the course of the year. The Wellcome team has strengthened its omnichannel presence through the wellcome.com.hk website, its app and a quick-commerce partnership with foodpanda, contributing to a more than 20% sales growth in overall Food e-commerce with significantly improved profitability.

South East Asia Food sales performance was adversely affected by intense competition and soft consumer sentiment due to cost-of-living pressures. Improved sales mix, effective cost control and optimisation of the store portfolio led to a meaningful earnings recovery, with Singapore Food turning profitable in the fourth quarter of 2024. The Group continues to serve the Singapore market with different propositions through its various brands.

In June 2024, the Group completed the divestment of its Hero Supermarket business in Indonesia. Post-completion, DFI’s operations in Indonesia have fully pivoted to the Guardian and IKEA businesses.

HOME FURNISHINGS

IKEA reported sales of US$701 million, representing a 12% drop compared to the prior year. Overall, LFL sales reduced by 11% in 2024. Operating profit was US$16 million, down 13% year-on-year.

IKEA’s business performance has been hampered by reduced customer traffic due to weak property market activity across regions. While IKEA Taiwan demonstrated relative resilience, sales in Hong Kong and Indonesia were affected by intensified competition and basket mix change as customers reduced purchases of big-ticket items.

In response to the challenging sales environment, the IKEA team continues to implement strong cost control measures across our markets. The IKEA Hong Kong business is pivoting towards a more value-driven omnichannel proposition to compete with Chinese mainland digital platforms. E-commerce penetration has now surpassed 10% across all markets. The IKEA Indonesia team remains focused on driving sales through enhancing store commerciality, increasing local sourcing, and adopting a more effective marketing strategy to improve local relevancy. Implementation of cost-saving measures contributed to narrowing losses compared to the prior year.

RESTAURANTS

The Group’s share of Maxim’s underlying profits was US$66 million in 2024, down from US$79 million in the prior year, largely due to lower mooncake sales and weaker restaurant performance on the Chinese mainland. Maxim’s continued to expand its presence in South East Asia, adding 76 net new stores during the year, mainly in Thailand and Vietnam. Benefiting from a diversified portfolio, restaurant sales performance in Hong Kong remained resilient despite an increase in outbound travel on weekends and public holidays.

OTHER ASSOCIATES

The Group’s share of Yonghui’s underlying losses was US$33 million for the year, compared to a US$36 million share of underlying losses in the prior year. Continued macro headwinds and intense competition led to lower LFL sales. The reduction in losses was underpinned by ongoing cost optimisation, partially offset by a decline in gross margin. The divestment of the Group’s minority stake in Yonghui was completed in February 2025.

Robinsons Retail’s underlying profit contribution was US$17 million, up 15% year-on-year. Robinsons Retail reported low single-digit growth in LFL and robust growth in operating profit driven by the Food and Drugstore segments. Reported profit contribution grew close to 90% year-on-year, supported by one-off gains following the BPI-Robinsons Bank merger in early 2024.

OUTLOOK

We have navigated 2024 with resilient business performance and continued market share gains for our key business units by proactively adapting to changing market conditions through a stronger value proposition, expanded omnichannel presence and disciplined cost control. While challenges remain, we are cautiously optimistic about the outlook for 2025. The Group expects underlying profit attributable to shareholders to be between US$230 million and US$270 million in 2025, supported by an organic revenue growth of approximately 2%.

The Group will continue to execute against its strategic framework. By enhancing the local relevancy of our product offerings, deepening monetisation of our digital assets, and executing value-enhancing M&A transactions, we have put in place solid foundations in 2024, and we remain confident in driving sustained, profitable growth and shareholder returns in the years ahead.

Scott Price

Group Chief Executive

Hashtag: #DFIRetailGroup #Mannings #Guardian #7-Eleven #Wellcome #MarketPlace #ColdStorage #Giant #IKEA #yuuRewards #Maxim’s #RobinsonsRetail

![]() https://www.dfiretailgroup.com/

https://www.dfiretailgroup.com/

The issuer is solely responsible for the content of this announcement.

DFI Retail Group

DFI Retail Group is a leading Asian retailer. At 31 December 2024, the Group, its associates and joint ventures operated over 10,700 outlets, of which more than 5,000 stores were operated by subsidiaries. The Group, together with associates and joint ventures, employed over 190,000 people, with over 45,000 people employed by its subsidiaries. The Group had total annual revenue in 2024 of US$24.9 billion and reported revenue of US$8.9 billion.

DFI Retail Group is dedicated to delivering quality, value and exceptional service to Asian consumers through a compelling retail experience, supported by an extensive store network and highly efficient supply chains.

The Group (including associates and joint ventures) operates a portfolio of well-known brands across six key divisions. The principal brands are:

Health and Beauty

- Mannings on the Chinese mainland, Hong Kong and Macau S.A.R.; Guardian in Brunei, Indonesia, Malaysia, Singapore and Vietnam.

Convenience

- 7-Eleven in Hong Kong and Macau S.A.R., Singapore and Southern China.

Food

- Wellcome and Market Place in Hong Kong S.A.R.; Cold Storage and Giant in Singapore; Lucky in Cambodia; and Robinsons in the Philippines.

Home Furnishings

- IKEA in Hong Kong and Macau S.A.R., Indonesia and Taiwan.

Restaurants

- Hong Kong Maxim’s group on the Chinese mainland, Hong Kong and Macau S.A.R., Cambodia, Laos, Malaysia, Singapore, Thailand and Vietnam.

Other Retailing

- Robinsons in the Philippines operating department stores, specialty and DIY stores.

At the heart of its business, DFI Retail Group is driven by its purpose to ‘Sustainably Serve Asia for Generations with Everyday Moments’.

The Group’s parent company, DFI Retail Group Holdings Limited, is incorporated in Bermuda and has a primary listing in the equity shares (transition) category of the London Stock Exchange, with secondary listings in Bermuda and Singapore. The Group’s businesses are managed from Hong Kong. DFI Retail Group is a member of the Jardine Matheson Group.

Investors

Christine Chung

The Taiwan-born pet mobility brand opens its first SoHo pop-up inside Flying Solo, bringing its Nordic-designed pet stroller collection to the heart of New York City.

NEW YORK, USA – Media OutReach Newswire – 02 April 2026 – FikaGO, the design-led pet mobility brand recognized across Asia and Europe, has opened its first New York City pop-up store inside Flying Solo in SoHo. The opening marks a deliberate move for a pet brand into one of the world’s most competitive retail districts.

Since entering the online American market in 2025, FikaGO has built a growing community of pet parents who see their animals as a central part of everyday life. Positioned as lifestyle essentials rather than conventional pet gear, FikaGO’s range of products is designed for people who want the best for their fur babies.

“We’ve always believed that pet products should not only be functional, but also beautifully integrated into everyday life.” — Eric Guu, Co-founder, FikaGO

SoHo was a considered choice: Flying Solo, with locations in New York and Paris, is known for championing independent design with a distinctly global sensibility.

The pop-up showcases FikaGO’s auto-folding Free To Go 2 in Sandy Beige, the brand’s bestselling product. All FikaGO’s products are manufactured using eco-friendly fabrics made from recycled materials, reflecting a commitment to sustainability. This includes their large-capacity Agile 2 pet strollers to their airline-approved Truffle carriers and the heavy-duty Kross pet wagon.

“Launching in SoHo is a meaningful milestone for us; it allows customers to truly experience the quality, design, and intention behind every FikaGO product.” — Eric Guu, Co-founder, FikaGO

As pet ownership rises globally, particularly among urban millennials and Gen Zs, demand for products that combine functionality, design, and lifestyle integration continues to grow. FikaGO was built for precisely this moment, and SoHo is precisely where that moment lives.

Visit the FikaGO pop-up at Flying Solo, 419 Broome Street, New York, or explore the full collection at https://us.fikago.com/.

Hashtag: #FikaGO #petmobilitybrand #petstroller #petcarrier #petwagon #petkennel #petbiketrailer

![]() https://us.fikago.com/

https://us.fikago.com/![]() https://www.facebook.com/FikaGO.US

https://www.facebook.com/FikaGO.US![]() https://www.instagram.com/fikago_us/

https://www.instagram.com/fikago_us/

YouTube: ![]() https://www.youtube.com/@fikago5910

https://www.youtube.com/@fikago5910

The issuer is solely responsible for the content of this announcement.

About FikaGO

FikaGO is a pet mobility brand founded in Taiwan, dedicated to crafting products that blend functionality, comfort, and modern aesthetics. With a presence across Asia and growing reach in Europe and the U.S, FikaGO is redefining everyday experiences between pets and their humans.

Media OutReach

Lee Kum Kee Celebrates Culinary Excellence at the Historic Hong Kong Debut of Asia’s 50 Best Restaurants 2026

From 23-25 March, Lee Kum Kee brought together top chefs, diverse cultures and industry communities through a range of thoughtfully curated experiences, bringing authentic Asian flavours to the global stage. As well as reaffirming the brand’s Asian roots and international perspective, its involvement reflected an enduring commitment to preserving culinary heritage and driving gastronomic innovation.

“Asian Flavour Duet“: A Culinary Journey Through Heritage and Innovation

Helping to build momentums for this year’s awards, Lee Kum Kee collaborated with Vicky Cheng, the acclaimed Executive Chef and owner of WING, to co-create the “Asian Flavour Duet”, a Hong Kong-style late-night supper party on 24 March. Hosted at two Hong Kong culinary landmarks, the experience unfolded in two chapters – “Paying Tribute to Heritage” and “Innovative Fusion” – and invited guests to explore the limitless possibilities of Asian flavour.

The evening began at the century-old Lin Heung Lau teahouse, a space filled with nostalgia and memories for generations of Hong Kongers. Chef Vicky reinterpreted classic Hong Kong late-night dishes using signature Lee Kum Kee sauces, while guests were immersed in the warmth of the historic venue.

The celebration then moved to Medora, Chef Vicky’s Western dining space, where an “Innovative Fusion” was revealed. He showcased his modern culinary philosophy by incorporating Lee Kum Kee sauces with contemporary techniques to create bold, unexpected dishes. Guests also enjoyed specially crafted cocktails infused with Lee Kum Kee sauces, alongside a delightful yet refined sauce-inspired gelato, demonstrating a harmonious interweaving of savoury, umami, sweetness and spice.

The multisensory journey seamlessly blended tradition with innovation, exploring the future of cuisine while highlighting Lee Kum Kee’s role as a global gateway to Asian culinary culture.

At the event, Dodie Hung, Executive Vice President – Corporate Affairs at Lee Kum Kee, commented, “Tonight, we are honoured to celebrate Hong Kong’s late‑night food culture with Chef Vicky and the global culinary community. From the legacy of Lin Heung Lau to the forward‑looking spirit of Medora, we are proud to be part of the creative journey and help showcase the depth of Asian flavours on the world stage.”

Celebrating a Gastronomic Brilliance with the Highest Climber Award Sponsored by Lee Kum Kee

During the awards ceremony on 25 March, Lee Kum Kee’s booth showcased a range of the brand’s acclaimed classic sauces and innovative products. Guests sampled specially crafted bites featuring Lee Kum Kee sauces, engaging directly with the flavours and techniques that have made the brand a trusted partner in both home and professional kitchens worldwide.

As part of the evening’s celebration of the region’s most exceptional culinary talents, the Highest Climber Award sponsored by Lee Kum Kee was presented to Lamdre in Beijing by Chef Park from Atomix (No.1 in North America’s 50 Best Restaurants 2025). Lambre was applauded for its pioneering plant-based dining space that promotes healthy, sustainable living while honouring Chinese biodiversity in its menus.

In addition, WING, led by Chef Vicky, achieved an impressive second place in 2026 Asia’s 50 Best Restaurants list. The restaurant had also previously ranked No. 11 on The World’s 50 Best Restaurants list in 2025, underscoring its continued international acclaim.

Building the Future Together: Deepening Global Partnerships

With the success of this prestigious awards ceremony in Hong Kong, China, Lee Kum Kee looks forward to deepening its collaboration with leading talents in the global culinary community. By continuing to champion Asian flavours and foster meaningful dialogue and exchange, the brand will continue to bring the spirit of Asian cuisine to kitchens and dining tables around the world.

Hashtag: #LeeKumKee #LKK

The issuer is solely responsible for the content of this announcement.

About Lee Kum Kee

Lee Kum Kee is the global gateway to Asian culinary culture, dedicated to promoting Chinese culinary culture worldwide. Since 1888, it has brought people together over joyful reunions, shared traditions and memorable meals. Beloved by consumers and chefs alike, Lee Kum Kee’s range of more than 300 sauces and condiments sparks creativity in kitchens everywhere, inspiring professional and home chefs to experiment, create and delight. Headquartered in Hong Kong, China and serving over 100 countries and regions, Lee Kum Kee’s rich heritage, unwavering commitment to quality, sustainable practices and “Constant Entrepreneurship” combine to enable superior experiences through Asian cuisine for people worldwide. For more information, please visit www.LKK.com.

About Asia’s 50 Best Restaurants

Launched in 2013, Asia’s 50 Best Restaurants aims to showcase the outstanding achievements and diverse culinary landscape of the region. The list is determined by the Asia’s 50 Best Restaurants Academy, a panel of over 350 culinary experts from across Asia who vote independently based on their specialised knowledge of the local dining scene. The Asia’s 50 Best Restaurants series includes the awards ceremony and list announcement, creating a premier networking platform for restaurateurs, media, seasoned travelers and culinary connoisseurs to celebrate the exceptional service, passion and talent in the dining industry.

- Herbert Vongpusanachai takes on the role of Senior Vice President for Commercial for the region, effective April 1, 2026

SINGAPORE – Media OutReach Newswire – 2 April 2026 – DHL Express, the world’s leading international express service provider, has appointed Herbert Vongpusanachai as Senior Vice President, Commercial for Asia Pacific, effective April 1, 2026. Herbert, who currently serves as Managing Director for DHL Express Thailand & Indochina, will be based in Singapore for his new role.

Herbert brings more than two decades of leadership experience within DHL Express, having successfully helmed multiple key markets across the region. He first joined the company in 2003 as Managing Director for Thailand & Indochina, later taking on leadership of Singapore in 2008, followed by Hong Kong & Macau in 2016. Since returning to lead Thailand & Indochina in 2020, he has driven sustained year‑on‑year profitable growth, transforming the cluster into one of the region’s key engines of expansion.

“Herbert has an exceptional track record of delivering strong business results while nurturing highly engaged teams across diverse markets. His deep understanding of our customers, collaborative leadership style, and ability to unearth opportunities in complex environments make him the ideal leader to drive our commercial agenda for Asia Pacific. I am confident that under his guidance, we will continue to accelerate sustainable growth across the region,” said Ken Lee, CEO for Asia Pacific, DHL Express.

In his new regional role, Herbert will shape and accelerate the commercial strategy for DHL Express across Asia Pacific by working with other functions to assess new sectors, routes and trade lanes with high potential for growth. He will focus on deepening customer engagement and supporting their expansion, while driving sustainable volume growth and advancing the adoption of new technologies to enhance commercial execution across markets. With his extensive country expertise and people‑first leadership style, Herbert is well‑positioned to support both regional and country teams in raising commercial performance to new levels.

“Asia Pacific remains an important anchor in global trade as seen in the latest DHL Global Connectedness Report, and this indicates the unwavering role of logistics to facilitate the flow of goods. With the newly introduced Heavyweight Express solution, which enables customers to ship heavyweight shipments with speed, certainty and reliability, I look forward to working alongside our talented teams to contribute to shaping the next chapter of DHL Express’s commercial success,” said Herbert Vongpusanachai, Senior Vice President – Commercial for Asia Pacific, DHL Express.

The latest DHL Global Connectedness Report shows that the region remains a major anchor of global commerce, with multiple economies rising in global connectedness rankings and Southeast Asia firmly establishing itself as a fast‑growing trade corridor. This also mirrors one of DHL Group’s strategies to better support 20 markets globally to accelerate growth; eight of them rest in Asia Pacific – underscoring the region’s critical role in DHL’s global network. As trade flows diversify and intra‑Asia integration deepens, this leadership appointment further strengthens DHL Express’s position in Asia Pacific.

Hashtag: #DHL

![]() https://group.dhl.com/en.html

https://group.dhl.com/en.html![]() https://www.linkedin.com/company/dhlexpress/

https://www.linkedin.com/company/dhlexpress/

The issuer is solely responsible for the content of this announcement.

DHL – The logistics company for the world

DHL is the leading global brand in the logistics industry. Our DHL divisions offer an unrivalled portfolio of logistics services ranging from national and international parcel delivery, e-commerce shipping and fulfillment solutions, international express, road, air and ocean transport to industrial supply chain management. With approximately 389,000 employees in more than 220 countries and territories worldwide, DHL connects people and businesses securely and reliably, enabling global sustainable trade flows. With specialized solutions for growth markets and industries including technology, life sciences and healthcare, engineering, manufacturing & energy, auto-mobility and retail, DHL is decisively positioned as “The logistics company for the world”.

DHL is part of DHL Group. The Group generated revenues of approximately 82.9 billion euros in 2025. With sustainable business practices and a commitment to society and the environment, the Group makes a positive contribution to the world. DHL Group aims to achieve net-zero emissions logistics by 2050.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn