Economy

Oil Jumps 2% as Russia Announces Production Cut

By Adedapo Adesanya

Oil rose more than 2 per cent on Friday as Russia announced plans to reduce crude production next month after the West imposed price caps on the country’s crude and fuel.

Brent crude futures rose by $1.89 or 2.2 per cent to $86.39 a barrel, while the US West Texas Intermediate crude futures (WTI) were up by $1.66 or 2.1 per cent to $79.72 a barrel.

Brent posted a weekly gain of 8.1 per cent, while WTI gained 8.6 per cent.

Russia will cut crude oil production by half a million barrels per day starting in March, a little over two months after the world’s major economies imposed a price cap on the country’s seaborne exports.

“We will not sell oil to those who directly or indirectly adhere to the principles of the price ceiling,” Russian Deputy Prime Minister Alexander Novak said in a statement. “In relation to this, Russia will voluntarily reduce production by 500,000 barrels per day in March. This will contribute to the restoration of market relations.”

The cut is equivalent to about 5 per cent of Russian oil output.

Last year, the European Union (EU) agreed to phase out all seaborne imports of Russian crude oil within the following six months as part of unprecedented Western sanctions aimed at reducing Russia’s ability to fund its war in Ukraine.

The drop in the supply of Russian oil will mean more competition for barrels from other sources, such as the Middle East, that Europe, the United Kingdom and other Western countries now need.

The production cut indicates that the European bloc’s recent price cap and ban on Russian oil products, which came into effect on February 5, have had some impact.

Russia’s output last year defied predictions of a decline, but its oil sales will prove more difficult in the face of the new sanctions.

Prices were pressured due to weak demand data from China and recession fears in the United States. China’s Producer Price Index (PPI) was down 0.8 per cent from a year earlier, extending the 0.7 per cent drop the prior month, even though manufacturing activity returned to growth in January.

Amid this, investment bank Goldman Sachs lowered its Brent 2023 price forecast to $92 a barrel from $98 and its 2024 price forecast to $100 from $105.

The Organisation of the Petroleum Exporting Countries (OPEC) is also confident that oil may resume its rally in 2023 as Chinese demand recovers after COVID curbs were scrapped and lack of investment limits growth in supply, with Reuters reporting that a growing number see a possible return to $100 a barrel.

Top oil producer, the US added the most oil rigs in a week since June. The total oil and gas rig count, an early indicator of future output, rose two to 761 in the week to February 10.

Economy

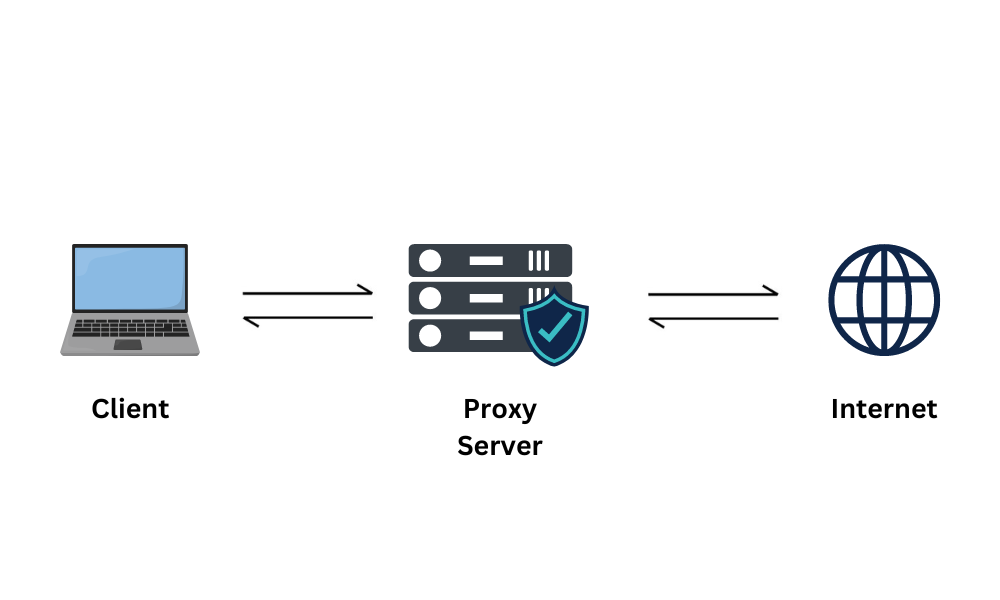

Binance Connectivity in 2026: Why Some Traders Now Rely on Proxy Servers and What to Watch For

Binance is still the world’s largest cryptocurrency exchange by trading volume, but access to it has become one of the more complicated conversations in the digital asset space. Some countries retain full access. Others sit in a grey zone where the platform loads but key features are missing. A few, including Nigeria at various points in the last two years, have moved between “available” and “restricted” on very short notice.

The result is that a growing number of traders, particularly in markets where regulatory action has been sharp and sudden, have begun using proxy servers to manage their connection to the exchange. The practice is more common than most traders will admit publicly. This article walks through why it is happening, the actual mechanics, the risks that come attached, and what to check before setting anything up.

Why Some Regions Restrict Binance Access

Binance operates in more than 100 countries, but the list of jurisdictions with full or partial blocks has been growing rather than shrinking. It is worth understanding that a full block is only one form of restriction.

- International sanctions. Binance is prohibited from serving customers in countries such as Iran, Cuba and North Korea under OFAC rules, with additional UN and EU sanction regimes layered on.

- Regulatory exits. In some markets, Binance either did not obtain or did not pursue local licensing. The United States saw the earliest such move, with Binance withdrawing and being replaced by a separate US-facing platform in 2019.

- Government bans. Some governments have moved quickly and with minimal notice. Nigeria transitioned from active access to a heavily restricted status over the course of a few days in early 2024, following a broader crackdown by authorities on cryptocurrency platforms, a case that traders here remember well.

- Binance Futures. Not available in 44 countries, including all EU member states, the UK, Australia and Canada.

- Staking and lending. Disabled in the UK, Canada, Australia and Japan.

- Fiat deposits. Removed in a number of markets, including the eurozone and Canada.

For Nigerian traders in particular, the ongoing tension between the Central Bank of Nigeria, the Securities and Exchange Commission and international exchanges has produced a shifting landscape. Access that works today is not guaranteed to work next month, and prudent traders have started to prepare for both scenarios.

How Proxy Servers Enter the Conversation

A Binance proxy server sits between your device and the exchange. Instead of your real IP address reaching Binance, the proxy’s IP does. From Binance’s perspective, the connection appears to originate wherever the proxy is located. For traders in restricted regions, this becomes a way to route their connection through a country where the exchange remains accessible.

Geographic access is not the only reason traders use proxies, though it is the most common.

Controlling API Rate Limits

Binance allows 1,200 requests per minute per IP. For traders running bots across multiple pairs simultaneously, that ceiling is reached quickly. Rotating proxies spread requests across different IPs so the bot continues without being throttled.

Running Multiple Accounts

Binance tracks multiple accounts originating from the same IP address. Traders operating several accounts use different proxies for each to keep the accounts from being associated with one another.

Accessing Region-Specific Features

Available tokens, trading pairs and pricing vary across regions. Traders can view and interact with region-specific offerings by routing through the relevant location.

Keeping WebSocket Connections Stable

Real-time price feeds and order book data run over WebSocket connections. Binance may throttle these if requests from a single IP look irregular. Clean residential IPs help hold those streams stable and reduce reconnection loops.

Security and Account Risks Traders Should Watch

Binance Uses Multiple Signals to Detect Location

IP is only one factor. On mobile, Binance also verifies GPS location, SIM card country code and device fingerprint. Mismatches raise flags. A proxy IP that shows the United States while the SIM card is registered in a restricted country is exactly the kind of inconsistency the system is designed to catch.

Mid-Session IP Switching Can Trigger Verification

Changing IPs while already logged in is one of the fastest ways to receive an additional verification prompt or a temporary account freeze. This is why sticky sessions matter — holding a single IP for an extended period rather than rotating aggressively.

Dirty IPs Are a Real Problem

Not every proxy IP is clean. Shared or previously compromised addresses may already have a history of suspicious activity attached, and Binance may have flagged them before you connect. A provider with a well-maintained IP pool reduces this risk substantially.

Funds Can Be Frozen

Binance may freeze accounts quickly if it detects unusual activity or determines that the account is being accessed from a restricted region. Recovery through support can take time, and in some cases access is not restored at all.

Choosing Between Residential, Mobile and Datacenter Proxies

Residential Proxies

Residential proxies use IP addresses assigned to real home internet connections. They appear as normal user traffic and are much harder for Binance to flag. This is the most common recommendation for traders needing consistent access. They are slower than datacenter and more expensive.

Mobile Proxies

Mobile proxies use IPs from real cellular carriers. Because mobile networks share IPs across many users naturally, distinguishing individual traffic is difficult. These are the strongest choice for traders in higher-risk areas who prioritise clean connections. They are also the most expensive option.

Datacenter Proxies

Datacenter proxies are fast and cheap, but Binance has invested heavily in detecting them. They originate from server farms rather than real devices, which makes them straightforward to identify as non-human traffic. They can still work for casual browsing and API data collection, but they are more likely to be blocked for account access in restricted regions.

What to Watch For When Setting Up

Match Your Proxy Location to Your KYC Country

If your account was verified with documents from one country and your proxy routes you through another, the mismatch can trigger review. Choose a proxy address that lines up with the country on your account.

Use Sticky Sessions for Account Access

Proxies that rotate IPs frequently are useful for scraping and bot work, less useful for logins. For anything involving direct account access, use sticky sessions that hold the same IP throughout the session. Quality providers offer sessions up to 24 hours.

Test the Connection Before Trading

Before using real money, confirm that the proxy is not leaking your real IP and is functioning as expected. A basic IP leak test will show what Binance actually sees when you log in. Several free tools online can display your visible IP and location.

Disable GPS on Mobile

If you are using the Binance app on a mobile device, turn off location services for the app. GPS data reveals your true location, and if it does not match the proxy location, Binance’s system will notice.

Pick a Provider With Clean IPs

Avoid free proxies. Their reputations are almost universally poor and their integrity questionable. Paid providers maintain IP pools and replace flagged addresses on an ongoing basis. Look for providers who are transparent about how they source IPs and who offer some form of IP quality filtering.

Final Thoughts

Proxy servers can be useful for traders dealing with Binance connectivity issues, but they are not a guaranteed solution and they come with real risks. The platform’s detection systems are more sophisticated than most users realise, and a poorly configured setup can create more problems than it solves, from repeated verification prompts to account freezes.

If you go this route, the setup matters more than the proxy itself. Having a proxy is not enough. Match the proxy location to your KYC country, use sticky sessions, and choose a provider with clean IPs for stability.

For most traders, residential proxies are the sensible starting point. They are reasonably reliable, sufficiently anonymous, and priced within reach. Traders in higher-risk regions or those needing additional trust signals may consider mobile proxies. Datacenter proxies are best reserved for tasks that do not involve direct account access.

The Nigerian context in particular calls for caution. Regulatory positions can change quickly, and traders who set up their connectivity today should also be prepared for the possibility that the ground shifts again. Backup plans, cold storage discipline, and awareness of the local legal landscape are as important as any proxy configuration.

By Adedapo Adesanya

Luno Nigeria has received Approval in Principle (AIP) from the Securities and Exchange Commission (SEC) through admission into its Accelerated Regulatory Incubation Programme (ARIP), marking a significant milestone in the country’s evolving digital asset regulatory landscape.

The approval follows an extensive engagement process between the company and the regulator and represents a major step in Luno Nigeria’s regulatory journey. As a result, it becomes the first global cryptocurrency exchange to be admitted.

Nigeria has a sordid regulatory minefield when it comes to digital assets; while it encourages new technologies, it has not fully lifted restrictions placed on crypto transactions via official channels.

Admission into ARIP means the cryptocurrency platform has met the commission’s requirements to participate in the programme and is authorised to operate within its defined scope, subject to ongoing compliance obligations and regulatory conditions, thus limiting full utilisation.

Founded in Africa in 2013, Luno has operated in Nigeria since 2015 and was among the first cryptocurrency exchanges to serve the Nigerian market. It was affected by a blanket ban announced by the Central Bank of Nigeria (CBN). The company said the latest approval reinforces its commitment to operating within Nigeria’s emerging regulatory framework for digital assets.

Commenting on the development, the chief executive of Luno Nigeria, Mr Ayotunde Alabi, described the approval as a landmark achievement for the company.

“This is an important milestone for Luno Nigeria and a strong validation of our commitment to building responsibly in one of Africa’s most important cryptocurrency markets. Admission into ARIP gives us a clearer regulatory pathway, strengthens trust with customers and partners, and provides a stronger foundation for the next phase of our growth, particularly as we expand our focus on institutional and B2B opportunities,” Mr Alabi said.

He expressed appreciation to the regulator for its continued engagement throughout the approval process and commended the Luno team for its resilience and commitment in achieving the milestone.

Luno said the regulatory approval comes at a time when it is expanding its business-to-business operations by engaging banks, fintech companies, payment providers, asset managers and corporate institutions seeking digital asset solutions.

According to the company, increasing regulatory clarity has become a key requirement for institutional adoption of digital assets. It noted that admission into ARIP would strengthen its ability to provide compliant digital asset infrastructure, including stablecoin applications, treasury solutions, crypto-as-a-service offerings and secure access to digital assets.

The Accelerated Regulatory Incubation Programme is the SEC’s regulatory sandbox designed to accelerate the onboarding of digital asset and investment service providers, including Virtual Asset Service Providers and tokenised product platforms.

The initiative enables the commission to assess emerging technologies and business models in a controlled environment while ensuring adequate investor protection and market integrity.

Building on the initial licensing rollout in 2024, Luno’s admission into the second batch of the programme underscores Nigeria’s efforts to establish a structured and transparent regulatory framework for the digital asset ecosystem, while strengthening confidence among investors, institutional partners and other market participants.

By Aduragbemi Omiyale

The Nigerian Exchange (NGX) Regulation Limited has allowed the trading in the shares of Fortis Global Insurance Plc.

This followed the completion of the share capital reconstruction of the organisation, which triggered the suspension a few weeks ago.

In a notice dated June 17, 2026, NGX RegCo announced the suspension of the underwriting company because of the exercise.

Yesterday, another notice was issued to inform the investing public of the lifting of the embargo on the securities of the organisation.

A total of 12,911,030,586 ordinary shares of Fortis Global Insurance were delisted, with 3,227,757,647 ordinary shares relisted at N3.96 per share.

“We refer to our market bulletin with reference number NGXREG/IRD/MB68/26/6/17, dated June 17, 2026, wherein the Market was notified that trading in the shares of Fortis Global Insurance Plc was placed on suspension effective Wednesday, June 17, 2026, in preparation for the share reconstruction of the company’s issued shares.

“The market is hereby notified that the entire 12,911,030,586 ordinary shares of Fortis Global Insurance were delisted from the daily official list of Nigerian Exchange Limited (NGX) on July 2, 2026, while the newly reconstructed issued share capital of 3,227,757,647 ordinary shares of 50 Kobo each were also listed on the daily official list of NGX at N3.96 per share.

“The delisting of 12,911,030,586 ordinary shares and listing of 3,227,757,647 ordinary shares on NGX is pursuant to the approval received from the company’s shareholders at its Extraordinary General Meeting (EGM) of April 4, 2025, and the no-objection received from the Securities and Exchange Commission (SEC).

“Consequently, following the completion of the share reconstruction, the suspension placed on the securities of the company has been lifted,” the circular signed by Bonaventure Onwuji, on behalf of the Head of Issuer Regulation Department at NGX RegCo, stated.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz4 years ago

Showbiz4 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn