Banking

We’re Committed to Partnerships to Drive Sustainable Growth—Access Bank

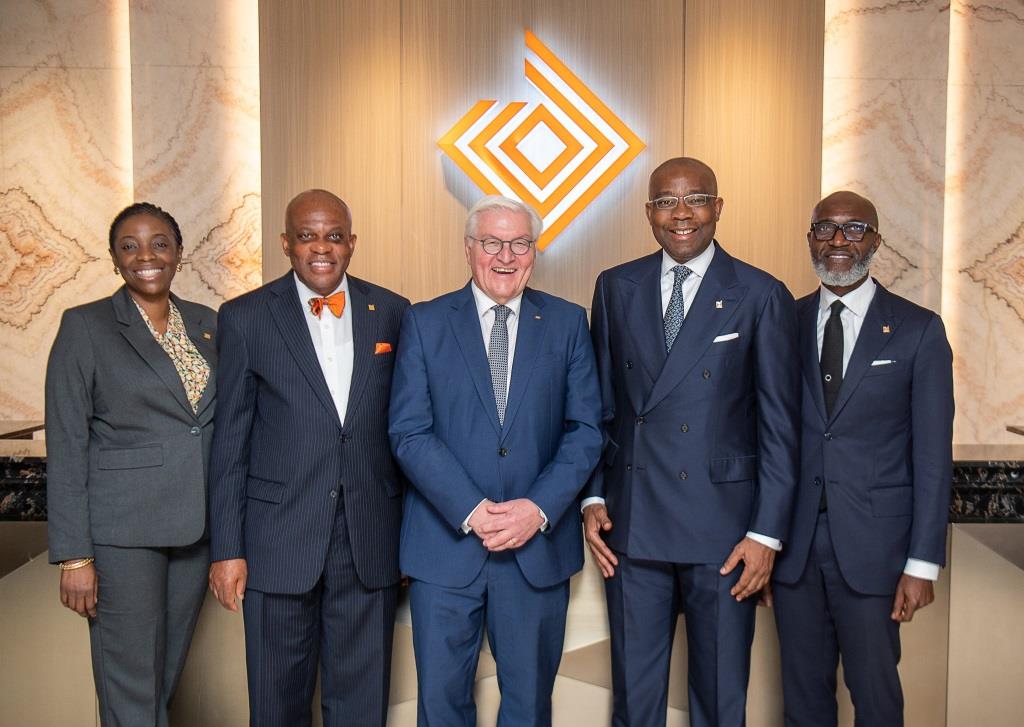

By Modupe Gbadeyanka

The chief executive of Access Bank Plc, Mr Roosevelt Ogbonna, has expressed the commitment of the company to building partnerships that drive sustainable growth.

Speaking when the lender hosted the President of Germany, Mr Frank-Walter Steinmeier, in Lagos last week, he said the organisation will always leverage its deep expertise in cross-border banking and market integration to the advantage of its customers.

“Nigeria’s position as Germany’s second-largest trading partner in Africa reflects the mutual benefits of this relationship.

“By leveraging our deep expertise in cross-border banking and market integration, Access Bank is committed to building partnerships that drive sustainable growth, innovation, and economic advancement across the continent,” Mr Ogbonna said while addressing stakeholders at a roundtable organised to welcome the German leader.

Last week, Mr Steinmeier made his first official visit to Nigeria and was welcomed by President Bola Tinubu.

President Steinmeier’s visit showcased Germany’s commitment to fostering economic partnerships in the region.

His Lagos agenda featured a landmark visit to Access Bank, as well as engagements with Nigerian startup founders and German-Nigerian business representatives to explore opportunities for trade and investment.

A central feature of the engagement at Access Bank was a business roundtable hosted by Access Bank’s leadership team and its German Desk.

The roundtable brought together German and Nigerian stakeholders, with discussions focused on two key areas: finance and energy, both of which are crucial to bolstering economic growth and innovation in the region.

President Steinmeier also received remarks from Roland Siller, CEO of DEG (German Development Bank), who elaborated on the financial synergies and products DEG provides to German and Nigerian businesses alike.

Access Bank’s German Desk, led by Sebastian Barroso da Fonseca, marked its sixth anniversary this year and has become a cornerstone for German and European businesses operating in Sub-Saharan Africa.

The Desk has provided critical support to over 100 clients, offering end-to-end financial solutions, including local funding facilitation, cash management, and seamless repatriation of funds to corporate headquarters. With operations spanning Nigeria, Angola, Ghana, South Africa, and beyond, the Desk has played an instrumental role in enabling businesses to navigate complex financial landscapes in Africa.

The engagement concluded with a Networking Reception at Access Bank’s headquarters, where delegates and stakeholders had the opportunity to engage and strengthen ties further.

Despite global challenges, Africa remains the fastest-growing economic region, with its GDP rising by 30 per cent over the past decade and average annual growth rates exceeding 5 per cent.

As a key player in the continent’s economic outlook, Nigeria continues to attract interest from global investors, and Germany has emerged as a critical economic partner in this regard.

Access Bank has strategically positioned itself as a gateway for trade and investment, leveraging its growing international footprint across 24 countries in Africa, Europe, and Asia to facilitate cross-border collaboration.

By Aduragbemi Omiyale

A collaboration to enable fast money transfers into Nigeria has been entered into between Flutterwave and Xoom, PayPal’s international digital money transfer service.

The partnership allows Xoom transfers to be converted by Flutterwave and settled locally in Naira, enabling quick transfers directly into recipients’ bank accounts at Access Bank, UBA, Zenith Bank, First Bank, GTBank, and additional participating banks across Nigeria.

The deal also enables Xoom’s global network with Flutterwave’s local payout infrastructure, allowing users globally to send funds directly into Nigerian bank accounts with improved speed and efficiency.

Nigeria is the leading remittance recipient in Sub-Saharan Africa, receiving over $20 billion in personal remittances in 2024. Despite this volume, receiving international payments has historically remained complex due to FX constraints and settlement delays. This collaboration helps address those challenges in a market of more than 232 million people, where the ICT sector is projected to contribute 21 per cent of GDP by 2027.

By combining Xoom’s expansive reach with Flutterwave’s local compliance and banking partnerships, the two companies are providing a more accessible financial corridor for the continent.

Xoom, a PayPal service, is a fast and secure international digital money transfer service that enables consumers to send money, pay bills, and reload phones for friends and family in approximately 160 markets globally.

As part of PayPal’s global payments ecosystem, Xoom leverages advanced fraud protection, compliance capabilities, and a trusted global network to help millions of customers move money quickly and securely across borders.

“We’re excited to have been chosen by Xoom for their Nigeria expansion. Millions of Nigerians rely on money from abroad to support everyday needs, whether it’s families receiving help from loved ones, freelancers getting paid for their work, or individuals earning income from the global economy. This helps make it easy and more reliable for people in Nigeria to receive funds and stay connected to opportunities beyond borders,” the chief executive of Flutterwave, Mr Olugbenga GB Agboola, stated.

By Aduragbemi Omiyale

An initiative known as Nigeria Lightning Rounds, designed to expand funding opportunities for Nigerian startups and small businesses by connecting founders with local and international investors, has been launched by ProvidusUnity Bank, in partnership with US-based global venture firm and accelerator, gener8tor.

Scheduled to be held on July 15, 2026, Nigeria Lightning Rounds will feature carefully selected startups engaging with targeted investors who have expressed interest in supporting Nigerian innovation.

Participating founders will have the opportunity to pitch their businesses through focused 15-minute virtual sessions facilitated by gener8tor and ProvidusUnity Bank’s networks.

The program will focus on high-growth sectors including fintech, healthtech, manufacturing, sustainability, and AI, but welcomes SMEs from all industries, with intending participants urged to apply via https://www.gener8tor.com/lightning-rounds/nigeria.

“We recognise that access to capital remains one of the biggest challenges facing entrepreneurs in Nigeria. Through our partnership with gener8tor, we are creating a platform that connects promising Nigerian founders with investors who can provide the support required to scale their businesses,” the Head of Business Development at ProvidusUnity Bank, Mr Ernest Elue, stated.

“The partnership reinforces ProvidusUnity Bank’s commitment to strengthening Nigeria’s entrepreneurial ecosystem by supporting innovation, enabling access to opportunities, and creating pathways for businesses with high-growth potential,” he added.

Also commenting, the Director of Lightning Rounds at gener8tor, Ms Elizabeth Larios, said, “gener8tor is thrilled to partner with ProvidusUnity Bank to extend the Lightning Rounds model into Nigeria.

“This collaboration reflects our commitment to building equitable ecosystems and driving capital to the most promising and underrepresented entrepreneurs.”

Lightning Rounds are a signature initiative of gener8tor’s investment platform, which has facilitated thousands of investor-startup meetings globally. The format is optimised to eliminate friction, reduce bias in early-stage fundraising, and help founders secure capital from investors aligned with their mission and stage. gener8tor’s previous Lightning Rounds for Nigerian Founders in 2025 featured 18 participating Investors and led to 50 investment meetings facilitated.

By Modupe Gbadeyanka

The verification of the depositors of the 46 microfinance banks, whose operating licenses were revoked by the Central Bank of Nigeria (CBN) over a week ago, has commenced.

The exercise, aimed at refunding those whose funds were trapped in the small lenders, is being conducted by the Nigeria Deposit Insurance Corporation (NDIC).

In a statement on Thursday, the agency said its staff members have been positioned at the offices of the affected banks across the country to attend to depositors.

It was disclosed that depositors of the defunct banks, who had their Bank Verification Numbers (BVNs) linked to their accounts in the failed banks, will be paid through their alternative accounts in existing banks.

However, depositors whose BVNs were not linked to their accounts in the failed banks have been encouraged to visit the affected banks’ offices with proof of account ownership, a passport photograph, verifiable means of identification (Driver’s Licence, Permanent Voter’s Card, International Passport or National ID Card) and BVN.

NDIC also stated that depositors can alternatively file their claims online through its website: www.ndic.gov.ng, to complete the Pre-Verification Claims Form by clicking on the Search Bar, and typing Pre-Verification Claims Form; opening the Form and filling in their details. They can also do so by clicking the link: https://ndic.gov.ng/ndic-pre-verification-claims-form/ or by visiting any of the NDIC offices closest to them to file their claims.

For further enquiries, the corporation can be reached on any of the following lines: 09037273810, 09038197064, 08104220807, 09064657140.