Economy

Quickly Settle Rift with Senate to Save Economy, LCCI Tells FG

By Dipo Olowookere

The presidency has been charged to, as a matter of urgent public importance, resolve its issues with the Senate over the confirmation of members of some boards and agencies, including that of the Monetary Policy Council (MPC).

This Monday, the council could not meet to make decisions on monetary policies for the country, a thing observers said was dangerous to the economy.

Since this Monday, the Nigerian Stock Exchange (NSE) has closed in the red zone, with some analysts attributing this to the gradual loss of investors’ confidence in the economy as a result of cancellation of the MPC meeting because the council lacked quorum to seat.

President Muhammadu Buhari had in 2017 sent names of people to fill the vacant positions in the council, but the Senate did not attend to the nominees because of its rift with the presidency.

The upper parliament wants Mr Ibrahim Magu removed as the Acting Chairman of the Economic and Financial Crimes Commission (EFCC), but the President has refused. His name was sent to the Senate two times, but was rejected by the red chamber.

At a press briefing on Wednesday on the state of the economy, President of the Lagos Chamber of Commerce and Industry (LCCI), Mr Babatunde Paul Ruwase, appealed to both parties to sheath their swords.

He said the crisis was already affecting the nation’s economy.

“The disagreement between the presidency and the Senate over the confirmation of nominees for heads of some agencies is beginning to take its toll on the economy.

“For instance, the Central Bank of Nigeria (CBN) suspended its first MPC meeting for this year scheduled for January 22 and 23 due to its inability to form a quorum as a result of non-confirmation of nominees by the Senate.

“The MPC has the mandate to review economic and financial conditions of the economy, make decisions on policies for the economy in the short and medium terms, review regularly the CBN monetary policy framework and adopt changes when necessary.

“The failure of the MPC to meet as scheduled has adverse effect on stakeholders in the financial sector and the economy in general.

“We call on the presidency and the Senate to quickly resolve their differences in the interest of public,” Mr Ruwase said at the event.

On the incessant scarcity of petrol in the country, the LCCI boss said, “We have concerns over the reluctance of government to liberalise the sector and open it up to private sector participation.

“The concentration of petroleum products supply in the Nigerian National Petroleum Corporation remains a major cause for concern. The arrangement is an inherent entrenchment of state monopoly in the NNPC to the detriment of private investors.

“The midstream and downstream petroleum sector currently suffers from regulatory regime which is negatively impacting growth, investment and job creation in the sector.

“The current model of managing the downstream petroleum sector is not sustainable. It is at variance with the present administration’s vision to diversify the economy and create jobs.

“It perpetuates the phenomenon of rent economy and is detrimental to economic competition. The truth is that the citizens are the ultimate beneficiaries of a competitive market environment.”

By Adedapo Adesanya

The Federation Account Allocation Committee (FAAC) distributed about N2.550 trillion from the revenue generated by the nation in June 2026 to the three tiers of government after its July meeting in Abuja.

A statement signed by the Director of Press in the Office of the Accountant General of the Federation, Mr Bawa Mokwa, “The N2.550 trillion total distributable revenue comprised N1.809 trillion in distributable statutory revenue and N740.724 billion in distributable Value Added Tax (VAT) revenue.”

It was gathered that a total gross revenue of N4.500 trillion was available in June 2026, with deductions for the cost of collection amounting to N160.744 billion, and transfers and refunds at N1.789 trillion.

According to a communiqué after the gathering, gross statutory revenue of N3.700 trillion was received in June 2026, N1.049 trillion higher than the N2.651 trillion received in the preceding month, while gross revenue of N799.746 billion was generated from VAT, N56.058 billion higher than the N743.688 billion recorded in May 2026.

It was stated that from the N2.550 trillion total distributable revenue, the federal government received N923.438 billion, the state governments got N838.208 billion, while the local government councils were given N591.390 billion, with N197.610 billion allocated to the benefiting states as 13 per cent of mineral derivation revenue.

From the N1.809 trillion distributable statutory revenue, the federal government went away with N849.366 billion, states shared N430.810 billion, local councils took N332.136 billion, while the benefiting states got N197.610 billion as derivation revenue.

From the N740.724 billion distributable VAT earnings, the central government got N74.072 billion, the states received N407.398 billion, and the local government councils were allocated N259.253 billion.

The communiqué further stated that in June 2026, collections from Companies Income Tax (CIT), Capital Gains Tax (CGT), Stamp Duties (SDT), Petroleum Royalties, Gas Flare Penalties, Rent, Mineral Oil Royalties (MOR), Value Added Tax (VAT), Import Duty, and Common External Tariff (CET) Levies increased significantly, while Petroleum Profit Tax (PPT), Hydrocarbon Tax (HT), Mineral Royalties, and Fees declined considerably. Excise Duty recorded only a marginal increase.

By Adedapo Adesanya

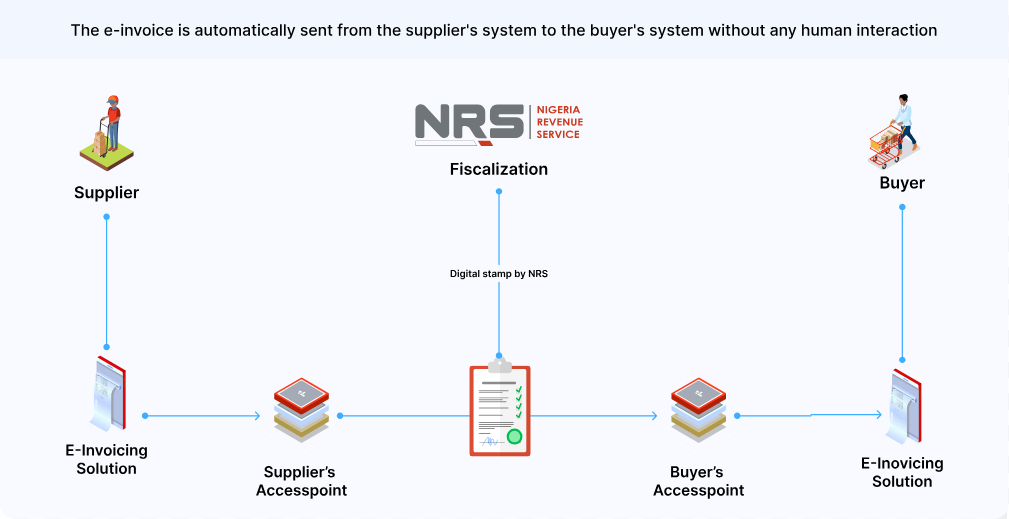

The Nigeria Revenue Service (NRS) says the rollout of electronic invoicing (e-invoicing) will strengthen tax compliance, curb revenue leakages and improve transparency in tax administration as it moves to fully digitise the country’s tax system.

The Project Lead for the NRS e-Invoicing Project, Mr Mohammed Bawa, stated this at the DigiTax E-Invoicing Compliance Breakfast Session held in Lagos on Wednesday.

The event, organised by DigiTax, an NRS-accredited e-invoicing platform, formed part of efforts to support the agency’s ongoing education and sensitisation campaign on the e-invoicing mandate.

Mr Bawa said the initiative aligns with global trends in tax digitisation and is expected to help improve Nigeria’s tax-to-GDP ratio, which remains one of the lowest in Africa.

According to him, the system will provide the NRS with greater visibility into transactions across sectors, formalise activities within the informal economy and standardise invoice formats nationwide using globally recognised invoice schemas.

He added that e-invoicing would improve operational efficiency for both businesses and tax authorities while supporting the NRS’ transition from manual and electronic tax administration processes to a fully automated system-to-system interaction model.

Mr Bawa noted that the legal framework for implementation is backed by the Nigeria Tax Administration Act, which prescribes penalties for non-compliance.

He disclosed that the NRS has completed onboarding large taxpayers and is preparing to enforce compliance with defaulting entities.

According to him, medium taxpayers are expected to begin compliance in the third quarter of 2026, while onboarding of emerging taxpayers will commence in 2027, with full adoption targeted for all taxpayers by the end of 2028.

Mr Bawa urged taxpayers yet to be onboarded onto the platform to begin the process and work with accredited service providers to ensure compliance.

On his part, Country Director of DigiTax Nigeria, Mr Olumide Akinsola, urged businesses to look beyond their internal systems and assess the compliance status of suppliers and counterparties.

He warned that businesses whose suppliers fail to transmit invoices through the MBS platform risk losing eligibility to claim Value Added Tax (VAT) input credits on such transactions, describing the resulting supply chain exposure as a significant commercial risk that many organisations have yet to quantify.

Mr Akinsola also announced the launch of DigiTax’s white paper, The State of E-Invoicing Readiness in Nigeria, which examines compliance adoption trends and the readiness gap across different taxpayer segments.

He added that DigiTax operates in Nigeria, Kenya, Zambia and the United Arab Emirates (UAE), noting that experience from those markets shows businesses that integrate early are better positioned to avoid disruptions when enforcement begins.

By Aduragbemi Omiyale

The names of about 100,000 companies registered by the Corporate Affairs Commission (CAC) are about to be deleted for inactivity, especially for failing to file their annual tax returns, Business Post reports.

This information was disclosed by the CAC via a notice signed by its management on Wednesday, July 15, 2026.

The list contains organisations like the Nigeria-Poland Chamber of Trade Invest Ltd, Alariwo of Afrika Ltd, Ovation Sports International, First Union Pension Fund Administrators, Investopedia Limited, Baptist High School Abuja Ltd, and Yobe Aluminium Manufacturing Industries Ltd, amongst others.

In the statement, the commission said its decision to strike off the names of the affected firms from the register aligns with the provisions of Section 692(3) (3) and (4) of the Companies and Allied Matters Act (CAMA), 2020.

However, the affected companies can still salvage the situation by filing all outstanding annual returns and regularising their records within 90 days.

“Please note that companies that fail to comply within the stipulated timeline shall be struck off the register without further notice,” it declared, expressing its continued commitment to providing prompt and efficient registration and regulatory services to the satisfaction of its valued customers.

See the full list below: