Economy

Nigeria Drops on Latest Ease of Doing Business Ranking

By Dipo Olowookere

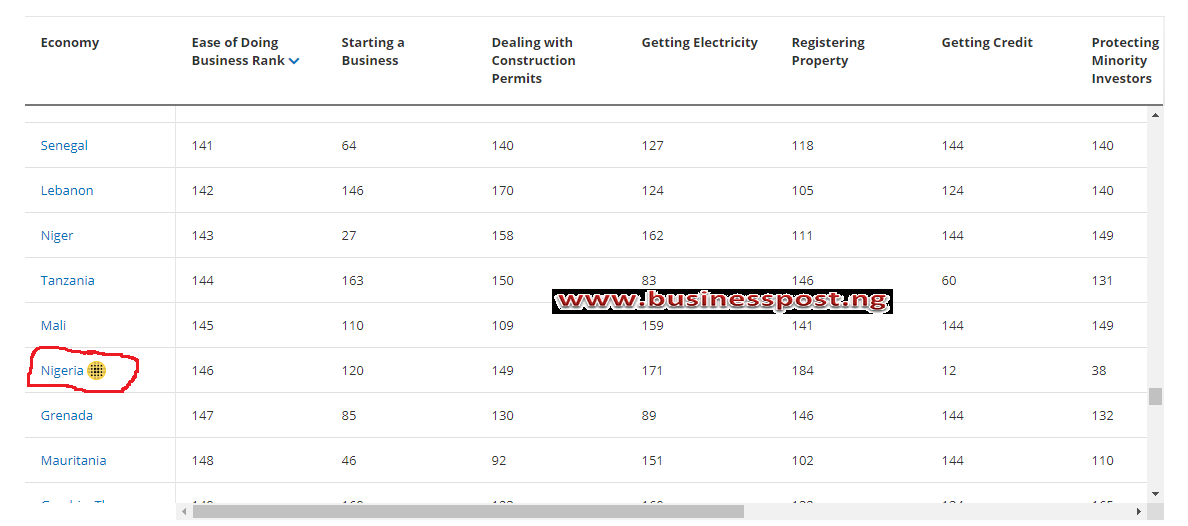

The World Bank has released its Ease of Doing Business raking for 2019 and Nigeria, which moved up by 24 steps in the 2018 log, slipped by one step in the latest standings.

Nigeria, which claimed the 145th position last year from the 190 countries surveyed, moved down to the 146th position in the new ranking.

Business Post reports that countries like Senegal, Lebanon, Niger, Tanzania and Mali claimed the 141st, 142nd, 143rd, 144th and 145th positions respectively.

Last year, when the 2018 ranking was released by the World Bank, Nigeria was among the 10 economies of the world to have recorded a significant improvement in their ease of doing business.

Economies are ranked on their ease of doing business, from 1–190. A high ease of doing business ranking means the regulatory environment is more conducive to the starting and operation of a local firm.

The rankings are determined by sorting the aggregate distance to frontier scores on 10 topics, each consisting of several indicators, giving equal weight to each topic. The rankings for all economies are benchmarked to June 2018.

Business Post reports that in the latest ranking, Mauritius was the only Sub-Saharan African economy to join the group of top 20 economies this year.

According to World Bank, Mauritius has reformed its business environment methodically over time, making reforms more than once in almost all areas measured by Doing Business over the past decade.

Following seven reforms in the area of property registration captured by Doing Business since 2005, for example, the time needed to register property has decreased more than 12 times; the time needed for business incorporation has decreased almost 10 times as a result of four reforms in starting a business.

Two economies that enter the top 20 this year, the United Arab Emirates and Malaysia, have maintained such a reform momentum.

The United Arab Emirates is the highest ranking economy in the Middle East and North Africa region, with reforms captured in four areas.

Six reforms in Malaysia were measured by Doing Business, resulting in the second highest regional improvement in the ease of doing business score.

Twelve of the top 20 economies are from the OECD high-income group; four are from East Asia and the Pacific, two are from Europe and Central Asia and one each is from Sub-Saharan Africa and the Middle East and North Africa.

In the latest report, the top three economies this year are New Zealand, Singapore and Denmark, exemplifying a business friendly environment.

World Bank said in the report that, “Substantial variations in performance among Sub-Saharan African economies present an opportunity for policy makers to learn from the experience of their neighbours.

“In the area of getting credit, for example, officials in Angola (ranked 184) and Eritrea (186) could learn from the experience of Rwanda and Zambia (both ranked 3).

“The two latter economies share many of the good practices found in OECD high income economies, including reliable secured transaction laws and robust credit information sharing available through credit bureaus or registries.”

By Adedapo Adesanya

The Nigeria Revenue Service (NRS) has introduced a 1.5 per cent stamp duty on eligible virtual asset transactions, with the tax deducted directly from the cryptocurrency purchased before it is credited to the buyer’s wallet.

According to the new guidelines issued on Monday, anyone buying Bitcoin (BTC), USDT or other cryptocurrencies in Nigeria will receive fewer digital assets due to the deduction.

This requires registered crypto exchanges and other Virtual Asset Service Providers (VASPs) to withhold the levy in the digital asset being traded and remit it to the government, marking Nigeria’s most comprehensive move yet to bring cryptocurrency transactions into the country’s tax net.

Unlike traditional taxes deducted from a customer’s bank account, the 1.5 per cent charge will be taken from the cryptocurrency itself, meaning buyers will receive less Bitcoin, USDT or other tokens than they paid for.

The tax body stated that “income tax deducted at source and stamp duty shall be remitted to the service in the originating token of the transaction.”

Besides the new stamp duty, the guidelines also clarify how income tax, Value Added Tax (VAT) and other tax obligations will apply to virtual asset activities such as trading, staking, mining and other crypto-related transactions.

To illustrate the new rule, the tax authority said a buyer who pays N1 million for one Bitcoin will receive only 0.985 BTC after 0.015 BTC is deducted as stamp duty and remitted to the government. When that Bitcoin is later sold, the next buyer will also have 1.5 per cent deducted from the cryptocurrency credited to their wallet.

The NRS said the guidelines are intended to provide clarity for taxpayers, crypto exchanges, peer-to-peer (P2P) marketplace operators, financial institutions, tax consultants and all participants in Nigeria’s virtual asset ecosystem.

According to the guidelines, the 1.5 per cent duty applies to eligible virtual asset transactions facilitated through registered exchanges and other recognised intermediaries. Where a cryptocurrency is used to complete a transaction that already attracts stamp duty under the law, the applicable duty on the underlying instrument will also be payable.

For crypto users, the implication is higher transaction costs, as eligible purchases will attract the 1.5 per cent stamp duty, while VAT on exchange service fees and income tax on taxable gains may also apply, depending on the nature of the transaction.

By Adedapo Adesanya

The Naira opened the week on a positive note, as it appreciated against the US Dollar by N3.39 or 0.25 per cent in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Monday, August 3, to N1,364.83/$1 from N1,368.22/$1 last Friday.

However, it suffered a marginal decline against the Pound Sterling in the official market during the session by 10 Kobo to close at N1,837.89/£1 compared with the preceding session’s N1,837.79/£1, and lost 6 Kobo on the Euro to sell at N1,573.93/€1, in contrast to the previous trading day’s N1,573.87/€1.

At the black market segment, the Nigerian currency traded flat against the Dollar yesterday at N1,405/$1, and at the GTBank forex counter, it was unchanged at N1,374/$1.

Interbank FX transactions increased sharply as market makers’ activities raised total Dollar volume exchanged to $137.048 million, more than 132 per cent above $58.990 million in turnover at the previous close. The surge in turnover was driven by increased deals at the NFEM window. The central bank reported that deal count at the interbank FX window rose to 138 from 67 on Friday.

As for the cryptocurrency market, major tokens advanced despite ongoing uncertainty around unresolved Coldcard wallet sweeps that have drained hundreds of Bitcoin (BTC), while traders are watching whether bitcoin can hold above $63,000 through the US session. BTC rose by 1.70 per cent to $63,765.88.

Bitcoin treasury firm Strategy disclosed Monday it sold 1,638 bitcoin for about $105 million between July 27 and Aug. 2, its third sale of 2026, per an SEC filing.

Also, an attacker has moved about 1,816 bitcoins, or roughly $114 million, from more than 5,200 addresses since July 30 in a fourth wave of sweeps targeting BTC in Coldcard-generated addresses.

Cardano (ADA) appreciated by 6.7 per cent to $0.1959, Binance Coin (BNB) gained 1.5 per cent to sell for $590.82, Solana (SOL) jumped by 1.3 per cent to $73.72, TRON (TRX) soared by 0.9 per cent to $0.3286, Dogecoin (DOGE) also grew by 0.9 per cent to $0.0703, Ripple (XRP) advanced by 0.5 per cent to $1.07, and Ethereum (ETH) rose by 0.4 per cent to $1,863.33, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) traded flat at $1.00 apiece.

By Dipo Olowookere

Bearish investor sentiment on Monday could not keep the Nigerian Exchange (NGX) Limited in the red territory, as the bourse closed higher by 0.18 per cent.

According to data from Customs Street, there were 25 price gainers and 38 price losers, indicating a negative market breadth index.

Eterna expanded by 10.00 per cent to quote at N36.30, Caverton also improved by 10.00 per cent to N5.50, Omatek soared by 9.88 per cent to trade at N1.78, AVA Capital grew by 9.70 per cent to N9.05, and Vitafoam Nigeria appreciated by 7.90 per cent to N194.00.

Conversely, Ecobank declined by 9.95 per cent to N80.10, Cadbury Nigeria went down by 9.92 per cent to N58.10, Thomas Wyatt slumped by 9.82 per cent to N3.95, Coronation Insurance depreciated by 9.80 per cent to N2.30, and CMFC dipped by 9.79 per cent to N3.50.

Yesterday, market participants transacted 923.0 million stocks for N37.9 billion in 72,544 deals compared with the 943.0 million stocks worth N46.7 billion traded in 55,480 deals last Friday.

This indicated that the number of deals increased by 30.76 per cent, the trading volume shrank by 2.12 per cent, and the trading value dropped 18.84 per cent.

Access Holdings was the most active equity on the first trading day of this week and month, with a turnover of 166.6 million units worth N4.4 billion. Honeywell Flour sold 93.6 million units for N1.6 billion, Sterling Holdco exchanged 57.1 million units valued at N455.4 million, Universal Insurance traded 51.8 million units worth N45.8 million, and Chams transacted 33.8 million units valued at N152.5 million.

But when trading activities ended for the session, the All-Share Index (ASI) went up by 446.85 points to 245,730.53 points from 245,283.68 points, and the market capitalisation jumped by N289 billion to N158.615 trillion from N158.326 trillion.