Banking

Keystone Bank Adds ‘Cheque Deposit’ Feature to Mobile App

By Modupe Gbadeyanka

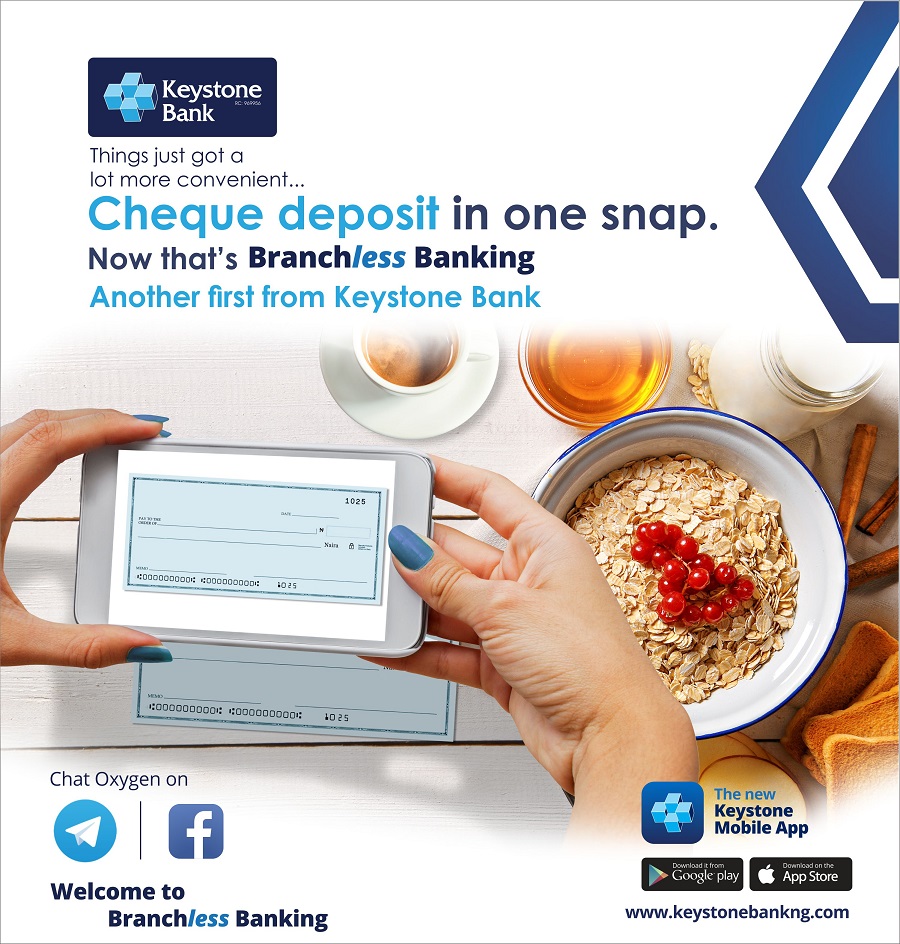

Nigeria’s most innovative banking services provider, Keystone Bank Limited, has introduced ‘Cheque Deposit’ feature in its mobile banking application, the new ‘Keystone Mobile App’.

The feature, which is another first from the financial institution and in the Nigerian banking sector, enables customers to pay cheques into their accounts at their convenience through their mobile phones even with zero data.

Speaking on the development, the Group Managing Director/CEO of Keystone Bank Limited, Dr Obeahon Ohiwerei, said the new feat is in demonstration of the bank’s commitment to continuously deliver superior and innovative banking solutions to its customers.

“The Keystone Bank brand is built on meeting and exceeding customer expectations by providing simple and convenient banking services at all times.

“With the new cheque deposit feature, you have one less reason to make that trip to the bank.

“In our fast-paced and evolving digital world, service literally has to be at the speed of thought; the rules of engagement are changing so fast that customer expectations are as diverse as our lifestyles and choices.

“It is no longer a question of stepping out to the bank but about the convergence of innovative services, digital technology and Omni-channel platforms coming to us at breakneck speed.

“Mobile Banking for one isn’t entirely new in the industry, but there is no end to innovation in delivering customer convenience; at Keystone Bank that’s what sets us apart and that shall continue to be our strength.

“We are determined to be your preferred bank; dependable, responsive and always within reach,” Mr Ohiwerei stated.

Other notable features of the mobile app are zero data banking (which enables customers enjoy banking services on their mobile phones without data), easy account opening, convenient self- booking and liquidation of fixed deposits, an expanded list of bills-payment options and easy activation of standing instructions and recurrent future payments.

Others include a “Switch Card ON/OFF option” which allows users to disable their cards temporarily if missing & re-enable at the click of a button, the “Hide Balance Feature” which is an additional safeguard against third-party viewing and the “Meet Your Relationship Manager Option” which allows users to call, text and email their account officers right within the app.

The lender prides itself as the first in the sector to introduce the Zero Data Banking feature and a Chat-bot feature called OXYGEN which enables banking on Telegram and Facebook.

Keystone Bank is a technology and service-driven commercial bank offering convenient and reliable solutions to its customers.

By Adedapo Adesanya

The Governor of the Central Bank of Nigeria (CBN), Mr Yemi Cardoso, said the central bank would now focus on a five-point policy agenda aimed at consolidating recent macroeconomic gains and steering the country toward sustained stability.

Mr Cardoso, while speaking at the 2026 Monetary Policy Forum held in Abuja on Thursday, set out the lender’s next phase of reforms anchored on inflation control, exchange rate stability, stronger reserves, deeper financial markets, and improved policy effectiveness.

The forum, themed Strengthening Nigeria’s Macroeconomic Stability Through Effective Monetary Policy: The Roles of Critical Stakeholders, brought together fiscal authorities, financial institutions, private sector players, and development partners.

He said the CBN will be positioning its five-point agenda as the cornerstone of the next phase of economic management.

Mr Cardoso said while recent reforms had delivered measurable improvements across key indicators, the focus had now shifted to consolidation.

He identified the five priorities as anchoring inflation firmly on a downward path to single-digit levels, sustaining exchange rate stability, strengthening external reserves through organic inflows, deepening interbank market development, and enhancing the transmission of monetary policy.

According to Mr Cardoso, the priorities reflect a deliberate strategy to entrench stability and improve the efficiency of the monetary framework. “The journey is far from complete. Our next phase is focused on consolidation,” Cardoso said, stressing that maintaining discipline and consistency would be critical to achieving durable outcomes.

He noted that the bank’s tightening measures and foreign exchange reforms had already begun to yield results, with inflation moderating, reserves strengthening, and market confidence improving.

However, he cautioned that sustaining these gains would require strong coordination between monetary and fiscal authorities.

Mr Cardoso emphasised that macroeconomic stability could not be achieved in isolation, describing it as a shared responsibility among policymakers, financial institutions, and the broader economic system.

He said disciplined fiscal operations, aligned policy actions, and continuous stakeholder engagement would be essential in delivering on the Bank’s objectives.

The CBN governor also highlighted the importance of deepening the interbank market to improve liquidity distribution and enhance the effectiveness of policy signals across the financial system.

He added that strengthening monetary policy transmission mechanisms would ensure that policy decisions translate more efficiently into real sector outcomes, including price stability and economic growth.

On external buffers, Mr Cardoso said the bank would continue to prioritise reserve accretion through sustainable sources, including improved foreign exchange inflows and enhanced market confidence. He explained that stronger reserves would provide a critical cushion against external shocks and support exchange rate stability.

The CBN chief further stressed that the success of the consolidation phase would depend on sustained collaboration across institutions.

He reaffirmed the apex bank’s commitment to orthodox monetary policy, transparency, and institutional credibility, noting that the reforms undertaken so far were necessary to correct past distortions and lay the foundation for long-term economic resilience.

By Modupe Gbadeyanka

In a bid to strengthen the Naira and ensure transparency, traceability, and effective monitoring of all transactions, the Central Bank of Nigeria (CBN) has directed all International Money Transfer Operators (IMTOs) in the country to open Naira settlement accounts for all transactions.

In a circular dated Tuesday, March 24, 2026, the apex bank said IMTOs have till May 1, 2026, to fully adhere to this directive and others.

It noted that transactions must be “routed strictly through their designated settlement accounts, maintained with Authorised Dealer Banks (ADBs) in Nigeria.”

With this development, diaspora remittances must be paid to beneficiaries in the local currency.

“All transactions arising from international money transfer operations, including disbursements to beneficiaries and any related settlements, must be processed exclusively through the IMTO’s settlement account(s) held with any ADB of their choice.

“IMTOs may use their discretion to designate their existing accounts or open new settlement accounts and may operate accounts with multiple ADBs in line with their business strategy,” the central bank emphasised.

“Settlement accounts shall only be credited with remittance flows and proceeds of foreign exchange conversions by licensed IMTOs (or their agents) with authorised market participants in the Nigerian Foreign Exchange Market (NFEM),” the notice also declared.

It stressed further that, “IMTOs shall ensure that their settlement accounts are properly designated for this purpose and operated in accordance with existing regulatory guidelines. A list of designated settlement accounts shall be advised by each licensed 1MTO to the Director, Trade and Exchange Department, and updated regularly as necessary.”

The CBN said to “support market efficiency and enhance pricing outcomes for 1MTO transactions, ADBs may process foreign currency transfers from 1MTO settlement accounts to other ADBs and approved market participants, including licensed BDCs.”

“IMTOs shall observe real-time market prices from the Bloomberg BMATCH and utilise this as guidance for pricing transactions with their customers and Authorised Dealers.

“This will improve price discovery, reduce information asymmetry between 1MTOs and banks, and encourage increased participation in the official FX market,” the disclosure stated.

Concluding, the apex bank said, “All IMTOs are required to ensure full compliance with this directive and maintain adequate records of related transactions for regulatory review and audit purposes,” reminding them to “maintain acceptable standards and comply with AML/CFT/CPF requirements.”

By Aduragbemi Omiyale

The dissolution of the board of Union Bank of Nigeria (CBN) by the Central Bank of Nigeria (CBN) in January 2024 has been nullified by a Federal High Court in Lagos.

In a judgment on Wednesday, Justice Chukwujekwu Aneke ordered the immediate reinstatement of the affected board members.

This ruling has now invalidated all actions taken by the central bank regarding the lender’s leadership change.

Justice Aneke held that the apex bank had no authority to remove the board members, declaring the CBN’s action as “ultra vires.”

Over two years ago, the central bank changed the boards of Union Bank, Polaris Bank, and Keystone Bank, accusing them of violating “sections of the Banks and Other Financial Institutions Act (BOFIA) 2020.”

The sacking of the Union Bank board happened after it was speculated that its acquisition by Titan Trust Bank was suspicious, with some alleging that the embattled former Governor of the CBN, Mr Godwin Emefiele, sold the lender to a proxy.

“This action became necessary due to the non-compliance of these banks and their respective boards with the provisions of Section 12(c), (f), (g), (h) of the Banks and Other Financial Institutions Act, 2020. The Bank’s infractions vary from regulatory non-compliance, corporate governance failure, disregarding the conditions under which their licenses were granted, and involvement in activities that pose a threat to financial stability, among others,” a part of the statement issued by the Acting Director for Corporate Communications at the CBN, Mrs Sidi Ali Hakama, said.

Later, the apex bank appointed Ms Yetunde Oni as the chief executive of Union Bank, with Mannir Ubali Ringim appointed as an executive director.

After the CBN’s action, Titan Trust Bank, Luxis International, and Magna International, which are the core shareholders of Union Bank, challenged the legality of the action in court.

They asked the court to restrain the CBN, Union Bank and the appointed directors from taking further steps pending the determination of the suit.

At today’s judgment, Justice Aneke granted this prayer, restraining the central bank, its agents and appointees from taking any further steps concerning the financial institution, including actions relating to its proposed recapitalisation or any associated measures.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn