Banking

Panic as Report Suggests Heritage Bank Nears Total Collapse

By Modupe Gbadeyanka

All seems not to be well with Heritage Bank at the moment as a report released by a reputable business news platform, Proshare Nigeria, is suggesting that the bank is a walking corpse.

Already, some customers of the financial institution are contemplating taking their hard-earned funds from the lender to a safer place.

Below is the full report.

Three months ago Proshare had cause to commit resources to investigate and produce an hitherto unpublished Confidential Report on Heritage Banking Company Limited, in direct response to the promptings of the advisory board members who wanted to know the true state of the bank which had another financial institution handling clearing operations for it at some time.

By this time, and curiously; it wasn’t such a big news that some of the bank depositors had experienced recurring challenges with withdrawals and staff exits did little to help matters. Yet, the restraint was important in order to ensure and support financial system stability as well as give the institution an opportunity to execute its resolution strategies without hindrance. After all, the institutional frameworks were in place to protect depositors and the system in general.

The task involved a lot of stakeholder engagements including sources we understood to be in a position to recognize, appreciate and make informed decisions. The revelations offered little comfort from history to, interventions up to the current state. We limited ourselves however to facts, data and evidence and submitted the report.

Further to the completion of this initial review, and in the interest of giving the financial system an opportunity to resolve the bank’s challenges through normal regulatory intervention and management effort at recapitalizing the institution or determination of the banks going concern status through a merger and acquisition (M&A) arrangement; the report remained private.

The burden of a moral hazard however appeared a bigger burden than tolerable or envisaged, especially given the evident ‘sailors survival’ approach that appears to have kicked in as seen through senior management exit, non-improving conditions, non-progressing talks around mergers and acquisitions; and recapitalization plans.

It has become compelling to highlight concerns about the bank formally; with the hope that ‘some intervention’ can happen to alter the trajectory of an inevitability. and remove the spectre of a bank waiting to die that overshadows the institution, unfortunately.

Proshare’s investigation into the bank revealed a few major concerns related to corporate governance and operational stability/sustainability. The primary issues included, but were not limited to the following:

- The acquisition of Enterprise Bank which is turning out to be a major strategic error;

- HBL’s non-performing loans (NPLs) portfolio, which are amongst the most challenged in the industry. Impairment charges in H1 2018 was estimated at N37.5bn but by year end, we extrapolated that the figure should settle around N634.5m;

- The bank posted an operating loss before tax of N38.5bn in H1 2018 and a loss of N4.4bn in the unaudited figures for the month of December 2018;

- The bank’s leverage has been a major sore point for management. The banks debt to equity ratio was -0.17. The negative value reflected negative shareholders fund which could be impaired by as much as $1bn;

- Equity capital has been virtually wiped out by accumulated losses, a legacy issue;

- The bank’s regular recourse to the CBN’s short term borrowing window highlights persistent liquidity resolution issues;

- Corporate governance has been a challenge as a number of the bank’s directors have allegedly been involved in a series of poor performing insider loan transactions, and little known about such resolutions (if any);

- The bank’s 2018 unaudited financial figures shows a dire situation in several operational metrics; and

- The bank has not been engaged in direct cheque clearing for a while, HBL’s instruments have been cleared through a third party first tier bank which got a full CBN guarantee against clearing loses.

IEI’s Pound of Flesh

It is instructive to recall how this sorry pass all began. Records indicated that Heritage Bank was in a difficult place from the start. It’s managing director and chief promoter, Ifie Sekibo, was the former Executive Vice Chairman (EVC) of International Energy Insurance (IEI) Plc from where a sizable amount of the acquisition money for the old SGBN was raised. Sekibo has been in a stretch of back and forth with the Board of his former company on this subject, as the directors of the company insist that Heritage Bank should be considered as part of the assets of the Insurance group; going as far as alleging that Sekibo had invested the insurers money in the bank without the approval of then Board members; or indicating/stating IEI’s consideration in the bank acquisition, if any.

The matter of using IEI resources to acquire the former Societe Generale Bank of Nigeria (SGBN) which was renamed Heritage Banking Company Limited has been the subject of a longstanding Economic and Financial Crime Commission (EFCC) investigation and continues to hound the bank’s CEO till date. Our background work on the matter then, enabled us to sight documentations that lends credence if not validity to the role played by IEI as reflected in presentations made to its board.

Source: What Happened To The N8bn Raised by IEI Plc in 2007? – Shareholders – Proshare, May 11, 2015

Mr. Sekibo has over the past few years tried to work out an amicable settlement with the IEI Group and directors, but matters are still fluid with necessary concessions being made on both parts. That said, the CEO’s travails still continue as he has had to deal with a few other issues concerning related-party transactions that have crystallized and left the bank’s books in a difficult position.

Weak Governance and Control

Heritage Bank’s problems have most certainly not been about Sekibo, alone. Far from it, the bank’s Board of directors (including former directors) has created a permissive culture that led to this.

Heritage Bank’s erstwhile chairman was also known to have used the banks tills to acquire two electricity distribution licenses’ the underlying cash flow difficulties of the businesses were subsequently and promptly transmitted to the bank, resulting in large repayment defaults. Indeed the loans have become ‘hardcore’ non-performing assets sitting on the bank’s books and creating both liquidity and profitability difficulties.

Managers of the bank, particularly branch managers, were in the past profligate in granting authorized and unauthorized loans to associates. Temporary overdrafts (TODs) routinely skipped repayment dates while structured loans also habitually missed the terms of the loan indenture, resulting into phantom profits and worsening liquidity.

Huge public sector deposits were beauties turned into beasts. The introduction of the Treasury Single Account (TSA) policy by the federal government in 2015 subsequently left the bank’s Asset and Liability Management (ALM) position in tatters.

The TSA policy did four things to undermine the bank’s fiscal stability:

- Sharply reduced the bank’s deposits;

- Significantly raised the banks cost of Funds (CoF);

- Reduced the bank’s ability to give short term loans; and

- Weakened the bank’s already fragile profitability.

Since the bank was already nurtured on a culture of entitlement, finding strategic options to wriggle from, under the weight of government policy and patronage became impossible.

Heritage Bank’s narrow retail base and its poor quality risk assets put inevitable pressure on profitability and liquidity. To compound matters, the bank’s internal control and compliance functions appears to have operated under a cloud of breaches than in the protection of standard corporate governance requirements, as directors willy-nilly violated single obligor limits. The poor internal control and audit process and administration at the bank thus complicated an already combustible bad loan and poor liquidity situation.

Coup de Foudre (Unintended Consequence)

As a way out of its myriad of challenges, the bank fell in love with another entity, committing a tragic error. In a bold but ill-digested move, Heritage Bank decided to acquire the Asset Management Company of Nigeria’s (AMCON’s) legacy deposit money institution, Enterprise Bank, this was the decision that let all the evil spirits out of Pandora’s box. The acquisition of Enterprise Bank was the classic example of a Cobra Effect or a situation where a cure becomes worse than the original disease.

The decision to acquire Enterprise Bank for N56bn in 2014 resulted in unintended consequence. At the time, the bank’s Board rationale in acquiring Enterprise Bank from AMCON was to rapidly expand the retail end of HBL’s operations and reduce its cost to income ratio based on representations that informed their decision. That gambit has proven to be a disaster and a cautionary tale on acquiring distressed banks unfortunately.

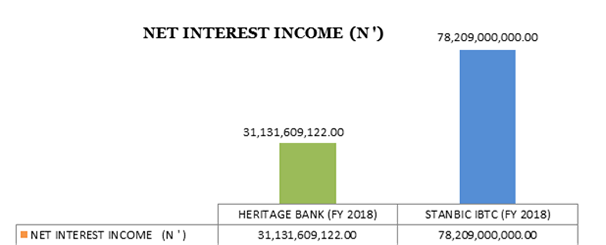

The Enterprise Bank wedlock, as consummated, turned into a fiasco as it added a further two hundred (200) branches to the banks operations and cut interest expense while improving net interest income (see chart 1 below). This led to the following outcomes:

- A sudden and significant rise in the bank’s bad debt to asset ratio;

- A leap in the bank’s debt provisioning or loan impairment requirements;

- A major rise in operational costs;

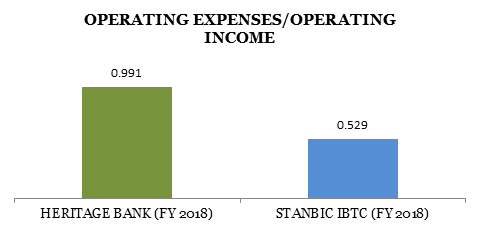

- A rise in the banks cost to income ratio (99% in FY 2018, as against the 53% of a bank like StanbicIBTC). (See chart 2 below);

- Stretching human capacity by lifting managers to their highest levels of administrative and technical (in)competence (The Peter Principle); and

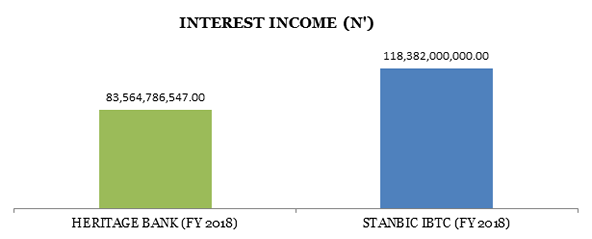

- Low Interest Income (as a result of slowing lending activities, (see chart 3) and high interest expense (as a result of a relatively low retail customer base, (see chart 4).

Chart 1 Net Interest Income FY2018, Heritage Bank and StanbicIBTC Bank

Source: Reported Financials Submitted / Estimated

Chart 2 Operating Expenses/Income FY2018,Heritage Bank and StanbicIBTC Bank

Source: Reported Financials Submitted / Estimated

Chart 3 Interest Income FY2018, Heritage Bank and StanbicIBTC Bank

Source: Reported Financials Submitted / Estimated

Biting into the Heritage Saga – What The Report Says

To understand the nexus between weak corporate governance, hubris, regulatory indulgence and Heritage Bank, the reader can send an email to [email protected] for a copy of the report.

The report is an attempt at a holistic look at the banks realities and lays bare the challenges that occur when individuals and institutions fail to live up to the exacting standards that are required to turn fragile ideas into enduring legacies.

The report was carried out as an intervention guidance to prompt action from the various parties and interested entities; all in the overall interest of the financial system.

To protect the financial system from contagion, the Central Bank of Nigeria (CBN) may need to move into the affairs of Heritage Bank and any of three actions are now plausible:

- Wind up the institution with shareholders losing their money (as things stand today shareholder’s funds have been completely eroded) while depositors resort to the National Deposit Insurance Corporation (NDIC) for part recovery of deposited funds;

- Find fresh investors interested in the institution and intermediate a best effort basis sale of exiting shareholder interest and recapitalization of the institution as a going concern; and

- Liquidation of the institution and the running of the bank under a new franchise as a legacy institution managed by AMCON and available for purchase by third party investors.

The preferred solution would appear to be either the second or third options.

The second option would be of particular preference as it would not involve heavy ‘menu cost’ by way of rebranding but would involve a new ownership – Board of Directors and management staff. The fresh capital inflow would eliminate the need for initial treasury support from public coffers and would likely result in fresh/foreign capital inflows which would be beneficial for the local currency while also protecting domestic employment. This approach would appear plausible given that the CBN recently gave out new licenses to start up banks; premised on their understanding that there exist room for new entrants with fresh ideas and approach.

The CBN would however have to work fast if Heritage Bank is not to be a blight on the Governors no-failure record.

From indicators received, there is a small window to achieve a technical resolution of the Heritage Bank situation, lest it could find itself taking remedial action(s) at a much higher economic cost later than it would now.

Heritage banks weak liquidity, impaired shareholder funds and high loan impairment, according to analysts, needs action not tolerance. The time to act is now!

Source: Proshare Nigeria

NOTE: Only the first two paragraphs of this story were written by Business Post.

By Adedapo Adesanya

Top financial services provider in Nigeria, Stanbic IBTC, has reiterated its commitment to empowering businesses, strengthening key sectors and positioning Nigeria as a competitive player in the global economy.

This came on the back of the 2026 edition of the Nigeria Business Summit from Wednesday, April 1 to Thursday, April 2, 2026, at the Landmark Event Centre, Victoria Island, Lagos. The two-day summit brought together industry leaders, policymakers, entrepreneurs and stakeholders across multiple sectors to explore sustainable business practices, foster economic growth and unlock global trade opportunities.

With the theme, Nigeria Means Business: Powering Sectors, Growing Sustainable SMEs & Unlocking Global Trade, the summit addressed critical issues across key sectors, including agribusiness, renewable energy, trade and Africa–China banking, as well as ICT and telecommunications. Additional sessions covered areas such as family business sustainability, artificial intelligence, employee value banking, insurance, pension and wealth management.

The event featured a keynote address by the Minister of Finance and Coordinating Minister of the Economy, Mr Wale Edun, who emphasised the urgent need for Nigeria to reposition itself as a leading export-driven economy to achieve sustained growth.

“Our true potential lies in becoming a leading export economy,” Edun stated. “Increased participation in regional and global trade will be critical to diversifying foreign exchange earnings and driving inclusive growth.”

He noted that while Nigeria’s GDP growth has improved to approximately 4 per cent, it remains below the level required to significantly reduce poverty. According to him, the country’s economic strategy is now shifting from stabilisation to growth acceleration, with trade expansion playing a central role.

Mr Edun highlighted ongoing reforms, including improved foreign reserves, rising non-oil revenues and renewed investor confidence, as indicators of a more resilient economy. However, he stressed that enhancing trade competitiveness would require continued investment in infrastructure, logistics and policy coordination.

He also highlighted the importance of small and medium-sized enterprises (SMEs), which account for over 90 per cent of businesses, noting that inclusive growth will depend on stronger collaboration between the public and private sectors.

Participants engaged in a rich line-up of activities, including expert presentations, panel discussions and high-level networking opportunities. Highlights of the summit included the Africa Trade Barometer presentation, client testimonial showcases and insightful discussions on the state of the African economy and intra-African trade opportunities.

Breakout sessions on agribusiness, ICT and healthcare, Africa-China banking and trade, as well as renewable energy, provided attendees with deeper, practical insights into some of the most critical sectors driving Nigeria’s economic future.

Speaking at the event, Mr Chuma Nwokocha, chief executive of Stanbic IBTC Holdings, represented by the organisation’s Chief Finance and Value Management Officer, Mr Kunle Adedeji, emphasised the importance of collaboration and innovation in driving sustainable growth.

“This summit has reinforced the importance of creating platforms where ideas can flourish, and businesses can grow sustainably. By working together, we can unlock new opportunities and drive economic advancement across Nigeria and the African continent,” he said.

The summit also spotlighted practical strategies for integrating sustainability into business operations, encouraging organisations to adopt environmentally conscious practices while maintaining profitability and competitiveness.

Mr Remy Osuagwu, Executive Director, Business & Commercial Banking, expressed satisfaction at the level of interest from participants, a critical element for a successful summit.

“From our conversations on energy and healthcare to the deep dives into trade, Africa-China relations, and agribusiness, Day 1 has offered perspectives that were both insightful and practical. I believe we’re all leaving with a stronger understanding of the opportunities emerging across our industries,” he said.

He acknowledged the level of engagement, questions, contributions and willingness of participants to share experiences, describing this as the real power of the Nigeria Business Summit, and a solid foundation for tomorrow.

The Chief Executive of Stanbic IBTC Bank, Mr Wole Adeniyi, who was represented by Mrs Bunmi Dayo-Olagunju, Deputy Chief Executive of Stanbic IBTC Bank, opened Day Two of the Nigeria Business Summit by highlighting the focus of the summit’s SME Day.

“Today, we build on Day One’s momentum with conversations that are equally critical for the future – from the dynamics of family businesses to the growing influence of artificial intelligence; the evolution of insurance, and the emerging space of electric vehicle banking.”

She further added, “Our goal on Day Two is simple: to explore what’s next. To understand how these developments will shape our businesses and how we can position ourselves ahead of the curve.”

By Dipo Olowookere

Tech enthusiasts interested in participating in the Take on Squad Hackathon, organised by Guaranty Trust Holding Company (GTCO) Plc, can now enter the contest via the official portal at https://squadco.com/hackathon.

The programme enters its third edition in 2026, and the theme for this year is Smart Systems: The Intelligent Economy, according to a statement issued by the organisers.

The hackathon brings together developers, designers and entrepreneurs across Nigeria in a collaborative environment to build practical solutions across key sectors, including financial services, healthcare, commerce and digital inclusion.

Participants are challenged to design and build intelligent, data-driven solutions that transform how communities engage with money.

It is part of the organisation’s commitment to fostering innovation, empowering talent, and supporting the development of technology-driven solutions that address real-world challenges across Africa.

“Today’s dynamic, digitally driven world demands continuous innovation, which is shaping how economies grow, how businesses scale, and how societies evolve.

“Through Take on Squad Hackathon, we are deliberately investing in the ideas and talent that will define the future.

“Our objective is not simply to encourage innovation, but to enable its translation into scalable solutions that deliver real and measurable impact.

“This reflects GTCO’s role as a financial services platform that connects capital, capability, and creativity to drive sustainable progress,” the Managing Director of HabariPay, Ms Eduofon Japhet, stated.

The social coding event remains a cornerstone of HabariPay’s mission to foster creativity and problem-solving among emerging tech talents. Competing teams will leverage Squad’s advanced APIs to create scalable digital tools that address everyday challenges faced by businesses and individuals.

Through initiatives such as this, GTCO continues to position itself at the intersection of finance, technology and enterprise, actively shaping the future of digital transformation in Africa.

By Dipo Olowookere

Banking services will not be interrupted throughout the Easter public holidays, from Friday, April 3, to Monday, April 6, 2026, for any reason, Ecobank Nigeria has assured its customers.

In a message over the weekend, the member of Africa’s leading pan-African banking group, Ecobank Transnational Incorporated, said customers would continue to enjoy quality service delivery during the period.

It noted that its secure and robust digital platforms would remain fully operational to support financial activities during the festive period.

All digital channels, including the Ecobank Mobile App, Ecobank Business App, USSD *326#, Ecobank Online, OmniPlus, Omnilite, EcobankPay, Ecobank Cards, ATMs, PoS terminals, and over 35,000 Ecobank Xpress Point agent locations nationwide, will remain accessible throughout the holiday, the financial institution further said, urging customers to conveniently conduct transactions at any time using this wide range of digital solutions.

Ecobank customers were encouraged to maximise the bank’s alternative channels for transfers, bill payments, airtime purchases, card services, and account management.

They were also advised to stay vigilant by shopping only on trusted websites; avoiding the sharing of PINs, passwords, and one-time passwords (OTPs); refraining from banking on public Wi-Fi networks; being cautious of urgent or emotionally charged messages; and regularly monitoring their account activity.

“Customers will continue to enjoy a full bouquet of services during the holiday, including local and international funds transfers, bill payments, airtime top-ups, merchant payments, balance enquiries, account statements, and cardless cash withdrawals via ATMs,” the Head of Products & Analytics, Consumer & Commercial Banking at Ecobank Nigeria, Mr Victor Yalokwu, stated.

“We understand that festive seasons come with increased financial activity, and our priority is to ensure our customers enjoy fast, reliable, and secure banking wherever they are.

“Our digital channels are designed to support uninterrupted transactions, and we have strengthened our systems to guarantee optimal performance throughout the Easter break,” he added.

Mr Yalokwu noted that, “Ecobank remains committed to providing innovative financial solutions and exceptional customer service. We wish all our customers and partners a peaceful and joyful Easter celebration.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn