Banking

Panic as Report Suggests Heritage Bank Nears Total Collapse

By Modupe Gbadeyanka

All seems not to be well with Heritage Bank at the moment as a report released by a reputable business news platform, Proshare Nigeria, is suggesting that the bank is a walking corpse.

Already, some customers of the financial institution are contemplating taking their hard-earned funds from the lender to a safer place.

Below is the full report.

Three months ago Proshare had cause to commit resources to investigate and produce an hitherto unpublished Confidential Report on Heritage Banking Company Limited, in direct response to the promptings of the advisory board members who wanted to know the true state of the bank which had another financial institution handling clearing operations for it at some time.

By this time, and curiously; it wasn’t such a big news that some of the bank depositors had experienced recurring challenges with withdrawals and staff exits did little to help matters. Yet, the restraint was important in order to ensure and support financial system stability as well as give the institution an opportunity to execute its resolution strategies without hindrance. After all, the institutional frameworks were in place to protect depositors and the system in general.

The task involved a lot of stakeholder engagements including sources we understood to be in a position to recognize, appreciate and make informed decisions. The revelations offered little comfort from history to, interventions up to the current state. We limited ourselves however to facts, data and evidence and submitted the report.

Further to the completion of this initial review, and in the interest of giving the financial system an opportunity to resolve the bank’s challenges through normal regulatory intervention and management effort at recapitalizing the institution or determination of the banks going concern status through a merger and acquisition (M&A) arrangement; the report remained private.

The burden of a moral hazard however appeared a bigger burden than tolerable or envisaged, especially given the evident ‘sailors survival’ approach that appears to have kicked in as seen through senior management exit, non-improving conditions, non-progressing talks around mergers and acquisitions; and recapitalization plans.

It has become compelling to highlight concerns about the bank formally; with the hope that ‘some intervention’ can happen to alter the trajectory of an inevitability. and remove the spectre of a bank waiting to die that overshadows the institution, unfortunately.

Proshare’s investigation into the bank revealed a few major concerns related to corporate governance and operational stability/sustainability. The primary issues included, but were not limited to the following:

- The acquisition of Enterprise Bank which is turning out to be a major strategic error;

- HBL’s non-performing loans (NPLs) portfolio, which are amongst the most challenged in the industry. Impairment charges in H1 2018 was estimated at N37.5bn but by year end, we extrapolated that the figure should settle around N634.5m;

- The bank posted an operating loss before tax of N38.5bn in H1 2018 and a loss of N4.4bn in the unaudited figures for the month of December 2018;

- The bank’s leverage has been a major sore point for management. The banks debt to equity ratio was -0.17. The negative value reflected negative shareholders fund which could be impaired by as much as $1bn;

- Equity capital has been virtually wiped out by accumulated losses, a legacy issue;

- The bank’s regular recourse to the CBN’s short term borrowing window highlights persistent liquidity resolution issues;

- Corporate governance has been a challenge as a number of the bank’s directors have allegedly been involved in a series of poor performing insider loan transactions, and little known about such resolutions (if any);

- The bank’s 2018 unaudited financial figures shows a dire situation in several operational metrics; and

- The bank has not been engaged in direct cheque clearing for a while, HBL’s instruments have been cleared through a third party first tier bank which got a full CBN guarantee against clearing loses.

IEI’s Pound of Flesh

It is instructive to recall how this sorry pass all began. Records indicated that Heritage Bank was in a difficult place from the start. It’s managing director and chief promoter, Ifie Sekibo, was the former Executive Vice Chairman (EVC) of International Energy Insurance (IEI) Plc from where a sizable amount of the acquisition money for the old SGBN was raised. Sekibo has been in a stretch of back and forth with the Board of his former company on this subject, as the directors of the company insist that Heritage Bank should be considered as part of the assets of the Insurance group; going as far as alleging that Sekibo had invested the insurers money in the bank without the approval of then Board members; or indicating/stating IEI’s consideration in the bank acquisition, if any.

The matter of using IEI resources to acquire the former Societe Generale Bank of Nigeria (SGBN) which was renamed Heritage Banking Company Limited has been the subject of a longstanding Economic and Financial Crime Commission (EFCC) investigation and continues to hound the bank’s CEO till date. Our background work on the matter then, enabled us to sight documentations that lends credence if not validity to the role played by IEI as reflected in presentations made to its board.

Source: What Happened To The N8bn Raised by IEI Plc in 2007? – Shareholders – Proshare, May 11, 2015

Mr. Sekibo has over the past few years tried to work out an amicable settlement with the IEI Group and directors, but matters are still fluid with necessary concessions being made on both parts. That said, the CEO’s travails still continue as he has had to deal with a few other issues concerning related-party transactions that have crystallized and left the bank’s books in a difficult position.

Weak Governance and Control

Heritage Bank’s problems have most certainly not been about Sekibo, alone. Far from it, the bank’s Board of directors (including former directors) has created a permissive culture that led to this.

Heritage Bank’s erstwhile chairman was also known to have used the banks tills to acquire two electricity distribution licenses’ the underlying cash flow difficulties of the businesses were subsequently and promptly transmitted to the bank, resulting in large repayment defaults. Indeed the loans have become ‘hardcore’ non-performing assets sitting on the bank’s books and creating both liquidity and profitability difficulties.

Managers of the bank, particularly branch managers, were in the past profligate in granting authorized and unauthorized loans to associates. Temporary overdrafts (TODs) routinely skipped repayment dates while structured loans also habitually missed the terms of the loan indenture, resulting into phantom profits and worsening liquidity.

Huge public sector deposits were beauties turned into beasts. The introduction of the Treasury Single Account (TSA) policy by the federal government in 2015 subsequently left the bank’s Asset and Liability Management (ALM) position in tatters.

The TSA policy did four things to undermine the bank’s fiscal stability:

- Sharply reduced the bank’s deposits;

- Significantly raised the banks cost of Funds (CoF);

- Reduced the bank’s ability to give short term loans; and

- Weakened the bank’s already fragile profitability.

Since the bank was already nurtured on a culture of entitlement, finding strategic options to wriggle from, under the weight of government policy and patronage became impossible.

Heritage Bank’s narrow retail base and its poor quality risk assets put inevitable pressure on profitability and liquidity. To compound matters, the bank’s internal control and compliance functions appears to have operated under a cloud of breaches than in the protection of standard corporate governance requirements, as directors willy-nilly violated single obligor limits. The poor internal control and audit process and administration at the bank thus complicated an already combustible bad loan and poor liquidity situation.

Coup de Foudre (Unintended Consequence)

As a way out of its myriad of challenges, the bank fell in love with another entity, committing a tragic error. In a bold but ill-digested move, Heritage Bank decided to acquire the Asset Management Company of Nigeria’s (AMCON’s) legacy deposit money institution, Enterprise Bank, this was the decision that let all the evil spirits out of Pandora’s box. The acquisition of Enterprise Bank was the classic example of a Cobra Effect or a situation where a cure becomes worse than the original disease.

The decision to acquire Enterprise Bank for N56bn in 2014 resulted in unintended consequence. At the time, the bank’s Board rationale in acquiring Enterprise Bank from AMCON was to rapidly expand the retail end of HBL’s operations and reduce its cost to income ratio based on representations that informed their decision. That gambit has proven to be a disaster and a cautionary tale on acquiring distressed banks unfortunately.

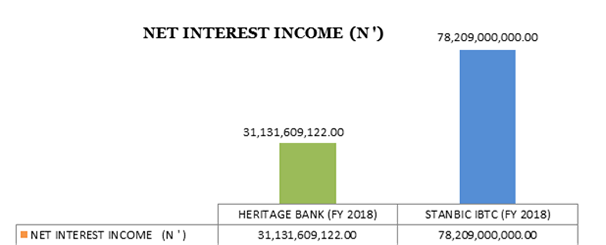

The Enterprise Bank wedlock, as consummated, turned into a fiasco as it added a further two hundred (200) branches to the banks operations and cut interest expense while improving net interest income (see chart 1 below). This led to the following outcomes:

- A sudden and significant rise in the bank’s bad debt to asset ratio;

- A leap in the bank’s debt provisioning or loan impairment requirements;

- A major rise in operational costs;

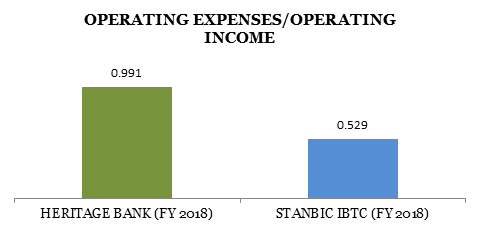

- A rise in the banks cost to income ratio (99% in FY 2018, as against the 53% of a bank like StanbicIBTC). (See chart 2 below);

- Stretching human capacity by lifting managers to their highest levels of administrative and technical (in)competence (The Peter Principle); and

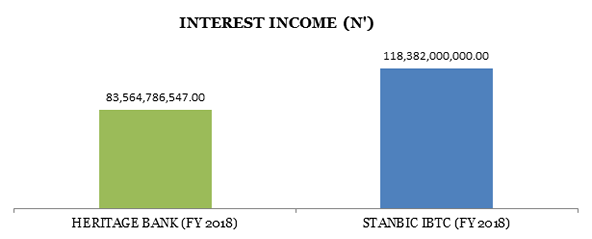

- Low Interest Income (as a result of slowing lending activities, (see chart 3) and high interest expense (as a result of a relatively low retail customer base, (see chart 4).

Chart 1 Net Interest Income FY2018, Heritage Bank and StanbicIBTC Bank

Source: Reported Financials Submitted / Estimated

Chart 2 Operating Expenses/Income FY2018,Heritage Bank and StanbicIBTC Bank

Source: Reported Financials Submitted / Estimated

Chart 3 Interest Income FY2018, Heritage Bank and StanbicIBTC Bank

Source: Reported Financials Submitted / Estimated

Biting into the Heritage Saga – What The Report Says

To understand the nexus between weak corporate governance, hubris, regulatory indulgence and Heritage Bank, the reader can send an email to re******@********ng.com for a copy of the report.

The report is an attempt at a holistic look at the banks realities and lays bare the challenges that occur when individuals and institutions fail to live up to the exacting standards that are required to turn fragile ideas into enduring legacies.

The report was carried out as an intervention guidance to prompt action from the various parties and interested entities; all in the overall interest of the financial system.

To protect the financial system from contagion, the Central Bank of Nigeria (CBN) may need to move into the affairs of Heritage Bank and any of three actions are now plausible:

- Wind up the institution with shareholders losing their money (as things stand today shareholder’s funds have been completely eroded) while depositors resort to the National Deposit Insurance Corporation (NDIC) for part recovery of deposited funds;

- Find fresh investors interested in the institution and intermediate a best effort basis sale of exiting shareholder interest and recapitalization of the institution as a going concern; and

- Liquidation of the institution and the running of the bank under a new franchise as a legacy institution managed by AMCON and available for purchase by third party investors.

The preferred solution would appear to be either the second or third options.

The second option would be of particular preference as it would not involve heavy ‘menu cost’ by way of rebranding but would involve a new ownership – Board of Directors and management staff. The fresh capital inflow would eliminate the need for initial treasury support from public coffers and would likely result in fresh/foreign capital inflows which would be beneficial for the local currency while also protecting domestic employment. This approach would appear plausible given that the CBN recently gave out new licenses to start up banks; premised on their understanding that there exist room for new entrants with fresh ideas and approach.

The CBN would however have to work fast if Heritage Bank is not to be a blight on the Governors no-failure record.

From indicators received, there is a small window to achieve a technical resolution of the Heritage Bank situation, lest it could find itself taking remedial action(s) at a much higher economic cost later than it would now.

Heritage banks weak liquidity, impaired shareholder funds and high loan impairment, according to analysts, needs action not tolerance. The time to act is now!

Source: Proshare Nigeria

NOTE: Only the first two paragraphs of this story were written by Business Post.

By Adedapo Adesanya

Zenith Bank Plc is investigating an incident involving unauthorised access to customers’ data, noting that the breach does not involve financial information and has not compromised its banking services or digital channels.

In an email sent to customers on Wednesday, the bank stated that the incident was part of a broader global cyberattack affecting multiple international organisations across various sectors.

The lender stated that it immediately activated its incident response protocols and intensified its cybersecurity and remediation efforts upon discovering the incident.

“This incident is part of a broader, global cyber-attack targeting multiple international organisations across various sectors. Upon discovery, we promptly activated our incident response protocols, cybersecurity actions and remediation efforts,” the bank said.

The bank reassured customers that its banking services and digital channels remain secure and fully operational.

As a precautionary measure, Zenith Bank advised customers to remain alert to potential phishing attempts and other forms of social engineering.

“As a precaution, we encourage our customers to remain vigilant against phishing emails, text messages, or phone calls, and never to disclose their password, PIN, One-Time Password (OTP), or other security credentials to anyone,” the bank said.

The incident is the latest in a series of cybersecurity challenges facing Nigerian financial institutions, with banks in recent months suspending their social media operations over impersonation and other fraudulent activities.

Earlier in April, the Nigeria Data Protection Commission (NDPC) said it was investigating alleged data breaches involving Sterling Bank, Remita and the Corporate Affairs Commission (CAC).

Nigerian banks have long been prime targets for cybercriminals because of the vast amounts of customer data and financial transactions they handle every day.

While many attacks have traditionally sought to steal funds, cybercriminals are increasingly targeting personal information, which can be used for identity theft, phishing schemes, account takeovers and other forms of financial fraud.

Cybersecurity threats have increasingly targeted Nigerian banks in recent years. In 2025, Union Bank of Nigeria warned customers about fraudulent websites and phishing campaigns designed to steal login credentials and personal information by impersonating the bank.

In August 2024, Guaranty Trust Bank experienced a domain-related security incident that temporarily disrupted access to its official website, although the lender assured customers that their deposits and banking services remained secure while it resolved the issue.

By Adedapo Adesanya

The chairman of First HoldCo Plc, Mr Femi Otedola, has affirmed plans to increase his 26 per cent holding in the organisation to 51 per cent, confirming a planned takeover of Nigeria’s oldest banking institution.

Mr Otedola spoke in an exclusive interview with Nairametrics published on Monday, giving a rare direction following recent speculations about the financial institution.

The milestone followed a series of share acquisitions, as Mr Otedola sought to tighten his grip as the company’s largest shareholder following the recent acquisition of additional shares worth N222.21 billion.

In the interview, the mogul said he has invested more than N600 billion of his personal wealth in First HoldCo, describing the move as a “long-term generational commitment” rather than another turnaround investment he would eventually exit.

Responding to speculation that he intends to consolidate his position in the group, Mr Otedola hinted that his investment journey is far from over.

“My investment threshold is always over and above 51 per cent,” he said. “One of my key investment principles is that firm shareholder control, with due regard for minority interest, is a key ingredient to executing reforms and restructuring to deliver value to all stakeholders.”

The businessman said the same strategy had guided his investments in African Petroleum Plc, later renamed Forte Oil Plc, where he gradually increased his shareholding from 28 per cent to 75 per cent before exiting the company in 2019.

He said he also increased his stake in Geregu Power Plc from 51 per cent to 95 per cent before reducing it to 77 per cent after the company’s public listing.

“I am on the same trajectory with First HoldCo Plc,” Mr Otedola said.

“To date, I have invested over N600 billion of my personal wealth in First HoldCo Plc — a figure that speaks not to speculation, but to unflinching confidence in the institution’s future, fundamentals and an unwavering personal commitment to its success.”

Mr Otedola said his decision to invest in First HoldCo came at a time when the institution was facing one of the most challenging periods in its history.

The billionaire steadily increased his investment in the group, accelerating his share purchases in 2026. His stake grew from 6.68 billion shares (15.95 per cent) in June 2025 to 8.06 billion shares by March 2026, then to 9.28 billion shares by June after acquiring about 1.22 billion shares in one quarter. A further purchase through Calvados Global Services last month lifted his holdings above 10 billion shares for the first time.

By Modupe Gbadeyanka

Nine persons linked to one of Nigeria’s biggest indigenous steel-and-manufacturing conglomerates, Western Metal Products Company (WEMPCO) Limited, could land in prison for allegedly defying an order of a Federal High Court protecting United Bank for Africa’s claim and disrupting the operations of a court-appointed receiver manager.

Justice Akintayo Aluko of the Federal High Court sitting in Lagos issued a stern Form 48 (Notice of Consequence of Disobedience to Order of Court), warning key directors and shareholders—including Lewis Shui Ngor Tung, Phillip Shui Che Tung, Robert Tung, Lawrence Tung, Taiwo Alli and others—that they face possible imprisonment for contempt of court after allegedly interfering with the Receiver/Manager appointed by UBA to take over key collateral assets.

The Form 48 notice, a formal warning under Nigerian civil procedure that precedes imprisonment for contempt, was published as a legal notice after personal service could evidently not be completed on the individuals, all listed at the same address: 18 Wempco Road, Ogba, Ikeja, Lagos (Federal High Court of Nigeria, Suit No. FHC/L/CS/555/26).

UBA is aggressively pursuing the recovery of syndicated and direct loan facilities amounting to about N61.5 billion (approximately $39 million) from WEMPCO and 16 related corporate entities.

Justice Aluko has already granted an Order of Mareva Injunctions freezing accounts belonging to the WEMPCO group across 27 commercial banks and fintechs.

According to MoneyCentral, UBA wants to recover the funds from 17 companies in the WEMPCO stable, from flagship Western Metal Products Company Limited down to Nigerian Enamelware Company Plc, Lagos Oriental Hotel Limited and Prime Nigeria Wood Products Co. Ltd. It disbursed the money to the firms under a Multicurrency Multiple Credit Facility Agreement dated September 30, 2019.

On April 2, 2026, the court granted UBA an interim Mareva injunction freezing up to N61.5 billion in WEMPCO-linked funds across 27 banks and fintech platforms, appointed a receiver-manager over WEMPCO’s unencumbered assets, and ordered the financial institutions to disclose any WEMPCO funds in their custody.

Anatomy of the Freeze

By the Order of April 2, 2026, Justice Aluko granted UBA ‘s Application filed on March 31, 2026. The Orders made were:

- Broad Asset Freeze (Mareva Injunction): The court restrained WEMPCO and 16 sister companies from operating accounts or transferring funds up to N61.5 billion. All 27 financial institution respondents—ranging from tier-1 banks to modern fintech processors like Moniepoint, OPay, and Kuda—must disclose and hold any balance standing to the credit of the defendants.

- Receiver/Manager Appointment: One Romeo Ese Michael, Esq., was appointed Receiver/Manager over WEMPCO’s assets not under the Multicurrency Multiple Credit Facility Agreement. This includes physical asset takeovers, such as two major Wärtsilä power generators.

Nine Names, One Address

The Form 48 lists nine individuals “to be committed” to prison for contempt, namely Lewis Shui Ngor Tung, Phillip Shui Che Tung, M.A. Ola Yusuf (Alh), Tung Lawrence Blake, Alli Aare Hadji Tokunbo, Paul Shui Po Tung, Tung Robert, Cl Ip, and Taiwo Alli.

Two names are independently identifiable in WEMPCO’s public corporate filings: Taiwo Alli is the sitting Managing Director/CEO of NGX-listed Nigerian Enamelware Company Plc — one of the 17 corporate defendants — while Robert Tung sits on that same board as a non-executive director and is one of the two brothers who built WEMPCO into its current scale.

That a sitting MD of a publicly listed Nigerian company now faces a documented risk of committal to prison over a corporate group’s unpaid debt underscores the reputational and governance stakes for WEMPCO’s listed arm, quite apart from the group’s privately held entities.

The Receiver and the 2019 Facility

The receiver-manager order points to the roots of the dispute: A Multicurrency Multiple Credit Facility Agreement dated 30 September 2019, under which UBA financed part of WEMPCO’s industrial build-out — the same period in which the group was completing major steel and power infrastructure investments.

The court’s specific mention of “two Wärtsilä engines (generators)… wherever they may be found” as receivership targets signals that WEMPCO’s captive power assets — critical to running energy-intensive steel and ceramics plants — are now squarely within the bank’s reach for recovery.

The Rise and Fall of WEMPCO Group

Few Nigerian conglomerates have as large a footprint with as little public profile as WEMPCO. The group was founded by the late Mr K.F. Tung, a Chinese-born entrepreneur who first visited Nigeria in 1967 and built an enamelware business before expanding into steel, ceramics, timber, agriculture and hospitality; he died in March 2019 at age 97, having led the group for more than five decades.

His sons, Lewis Tung and Robert Tung, subsequently took the business forward, growing it into one of Nigeria’s largest manufacturing employers, with more than 12,000-13,000 workers across 11-plus subsidiaries.

At its peak, WEMPCO was one of Nigeria’s largest diversified conglomerates, operating massive cold-rolled steel mills, enamelware plants, ceramic tile factories, nail production plants, and agricultural investments across Lagos and Ogun states.

The group owns high-profile real estate assets, including the 5-star Lagos Oriental Hotel on Victoria Island/Lekki, alongside industrial facilities spanning over 700,000 metric tonnes of steel capacity.

Over the past decade, however, severe foreign exchange shortages, cheap imported/smuggled alternatives, high energy overheads, tax defaults, and shifting government trade policies caused deep operational paralysis across WEMPCO’s 11+ subsidiaries.

As revenue collapsed, debt loads surged into hundreds of billions of Naira across the Nigerian financial sector, culminating in UBA’s enforcement actions to protect its balance sheet.

That scale is precisely why the case matters beyond the courtroom: WEMPCO is not a marginal borrower, but one of Nigeria’s largest indigenous industrial employers, and the outcome of this dispute carries direct implications for thousands of manufacturing jobs concentrated in Ogba and Ogun State.

Why This Matters: Depositor Money Is Not Free Money

The scale of UBA’s claim — N61.5 billion frozen pending trial, against a backdrop of a 2019 multicurrency facility likely running into the hundreds of billions of naira in total exposure across WEMPCO’s group structure — is a reminder of a basic truth in banking that is easy to lose sight of in a contentious court fight: the money banks lend to conglomerates like WEMPCO is not the bank’s own capital sitting idle.

It is depositors’ money — the savings of ordinary Nigerians, the working capital of small businesses, and the pension and insurance assets pooled through the banking system — recycled into loans that the bank is obligated to repay to its depositors whether or not the borrower repays the bank.

This is not an abstract concern in Nigeria’s current banking environment. The industry’s non-performing loans (NPL) ratio climbed to 8.03 per cent in January 2026 and to 9.85 per cent by February 2026, well above the Central Bank of Nigeria’s 5 per cent prudential threshold, after the CBN withdrew pandemic-era regulatory forbearance that had allowed banks to avoid classifying restructured loans as impaired.

Fitch Ratings has projected the ratio could fall back toward 5 per cent by year-end 2026, helped by fresh bank capital raised to meet the CBN’s new minimum capital requirements and by write-offs — but only if recoveries like UBA’s WEMPCO action succeed in converting non-performing exposures back into cash.

The CBN itself has warned that a stubborn rise in bad loans “could impair asset quality and weaken banks’ balance sheets,” posing systemic risk, and has pushed banks to deepen use of the Global Standing Instruction framework — precisely the kind of cross-bank fund-tracing mechanism reflected in UBA’s 27-institution Mareva order against WEMPCO — to improve recovery discipline.

Every naira UBA cannot recover from a defaulting borrower is a naira the bank must provision for out of its own capital and earnings — capital that could otherwise support new lending to other Nigerian businesses, or income that could otherwise be paid out as dividends to millions of Nigerian shareholders and pensioners with holdings in UBA stock.

Aggressive but lawful recovery action of the kind on display in the WEMPCO case is, in that sense, not simply a bank protecting its own balance sheet; it is a bank protecting the deposit base and credit capacity of the wider financial system.

Corporate Responsibility and the Nigerian Economy

Firms of WEMPCO’s scale carry an obligation that runs in both directions. On one hand, WEMPCO’s decades of investment in steel, enamelware, ceramics, wood products and hospitality have made it a genuine contributor to Nigeria’s industrial base and a major direct employer, with the group’s own account of its history stressing that it has “contributed immensely to the economy of Nigeria in particular and West Africa in general”.

On the other hand, that same scale means WEMPCO’s credit obligations were sized accordingly — a multicurrency, multi-billion-naira facility syndicated in 2019 — and the responsibility to service such facilities is inseparable from the privilege of accessing that scale of capital in the first place.

When large borrowers fall behind and resist enforcement, as UBA alleges is happening here, the costs are not confined to the bank’s shareholders.

Delayed recoveries constrain the credit banks can extend to other manufacturers, exporters and small businesses; they can pressure a bank’s capital adequacy ratios and, in aggregate across the industry, contribute to the kind of system-wide NPL pressure the CBN has flagged as a threat to financial stability.

Conversely, orderly and timely repayment — even when it requires restructuring or receivership rather than immediate cash settlement — protects the thousands of workers whose jobs depend on WEMPCO’s continued operation, preserves the bank’s capacity to keep lending into the real economy, and reinforces credit discipline across a banking sector the CBN is actively trying to strengthen after the post-forbearance clean-up.

It is worth noting that the reliefs UBA has obtained so far are interim measures granted pending a full hearing on the Motion on Notice, and that WEMPCO’s companies and the named individuals retain the right to contest the underlying claims in court.

The Bottom Line

UBA’s push to freeze N61.5 billion in WEMPCO-linked funds, install a receiver-manager over the group’s flagship steel unit, and now pursue contempt proceedings against nine individuals tied to the conglomerate marks one of the more aggressive corporate debt-recovery actions in Nigeria’s banking sector this year.

For a bank operating in an industry still working through the aftershocks of the CBN’s forbearance withdrawal and a near-10 per cent sector NPL ratio, recovering large legacy exposures is not optional housekeeping; it is central to protecting depositor funds, sustaining lending capacity and keeping Nigeria’s banking system stable.

The court’s enforcement action in UBA vs. WEMPCO marks a decisive moment for credit governance in Nigeria. With 27 financial institutions bound by court injunctions and corporate officers facing criminal contempt, UBA’s Receiver/Manager is positioned to realise underlying assets. Analysts say the outcome of this case will set a precedent for corporate debt resolution, financial system accountability, and the rule of law across Nigeria’s industrial landscape.